Europe Automotive Electronics Market Size, Share, Trends & Growth Forecast Report, Segmented By Vehicle Type, Sales Channel, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis Forecast (2026 to 2034)

Market Size, 2025

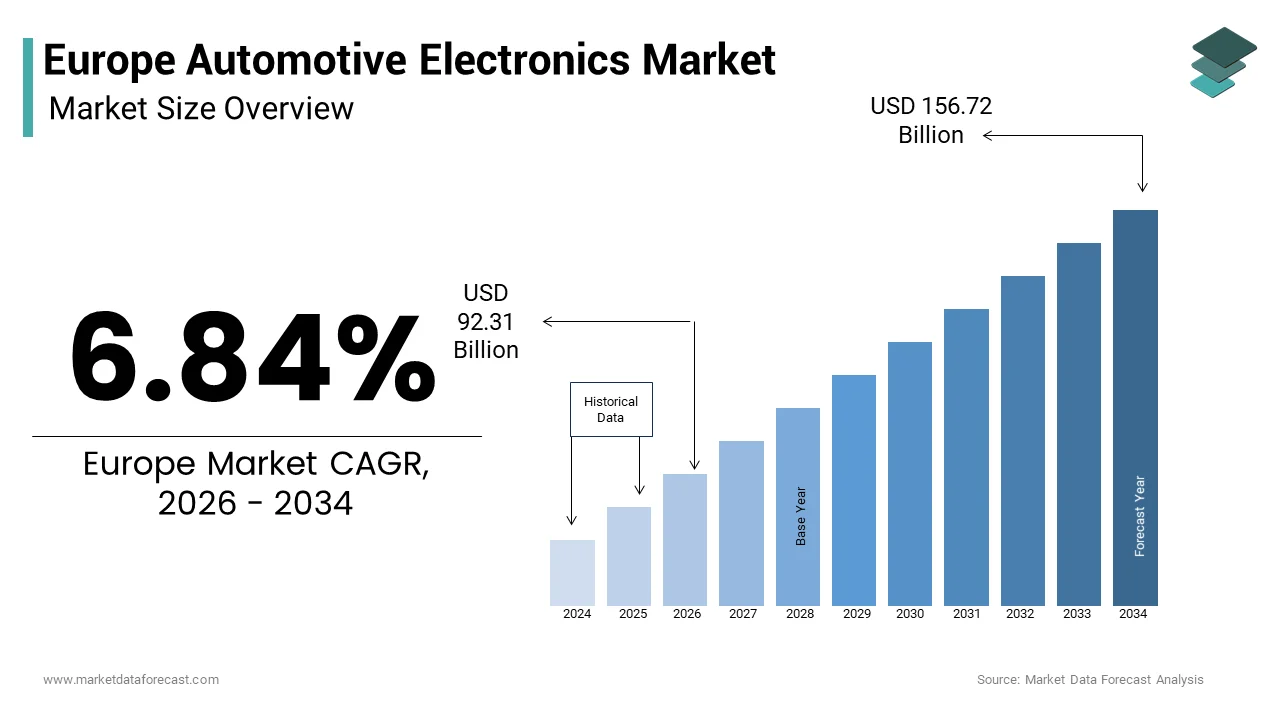

$92.31 BnMarket Estimate, 2026

$98.62 BnMarket Forecast, 2034

$167.44 BnCAGR, 2026–2034

6.84%Europe Automotive Electronics Market

The European automotive electronics market size was valued at USD 92.31 billion in 2025 and is anticipated to reach USD 98.62 billion in 2026 to reach from USD 167.44 billion by 2034, growing at a CAGR of 6.84% during the forecast period from 2026 to 2034.

Introduction to the Europe Automotive Electronics Market

Automotive electronics encompasses the sophisticated array of electronic systems and components that govern vehicle performance, safety, connectivity, and autonomous capabilities within the European region. This sector has transitioned from a supportive function to the central nervous system of modern mobility, driven by the continent's aggressive regulatory framework and technological ambition. The landscape is fundamentally shaped by the European Union's mandate to achieve climate neutrality, which necessitates a complete overhaul of powertrain architectures toward electrification. As per data from the European Environment Agency, transport accounts for a significant portion of total greenhouse gas emissions in Europe, prompting stringent CO2 targets that force original equipment manufacturers to integrate complex battery management systems, and power inverters. Furthermore, the General Safety Regulation enacted by the European Commission mandates advanced driver assistance systems, such as intelligent speed assistance, and lane keeping assist, on all new vehicles, effectively making high-level electronics standard rather than optional. The region also boasts a dense network of research institutions, and semiconductor initiatives, like the European Chips Act, aiming to bolster local supply chain resilience. This convergence of regulatory pressure, safety imperatives, and industrial strategy, creates a unique ecosystem where automotive electronics are not merely features, but essential compliance tools, defining the future of European transportation.

MARKET DRIVERS

Mandatory Integration of Advanced Driver Assistance Systems for Safety Compliance

The legislative compulsion for Original Equipment Manufacturers to equip vehicles with sophisticated Advanced Driver Assistance Systems to meet rigorous safety standards is primarily driving the growth of the European automotive electronics market. The European Union has established itself as a global pioneer in vehicular safety regulation, mandating technologies that were previously considered luxury additions. As per the European Commission, the General Safety Regulation requires all new car models introduced from mid-2022, and all new vehicles registered from mid-2024, to include ten specific safety features, including emergency braking, blind spot detection, and driver drowsiness monitoring. This regulatory shift transforms the demand dynamic from consumer driven preference, to manufacturer obligation, ensuring a guaranteed volume uptake for radar sensors, LiDAR units, and high-performance image processing chips. According to the European Transport Safety Council, these systems have the potential to prevent thousands of fatalities annually, providing a strong ethical, and legal, impetus for rapid adoption. Consequently, automotive suppliers are scaling production capacities for electronic control units dedicated to perception and decision-making tasks. The ripple effect extends beyond passenger cars, to commercial fleets, where similar safety mandates are being discussed, to protect vulnerable road users in dense urban environments. This regulatory bedrock ensures sustained investment in sensor fusion technologies, and real time data processing capabilities, securing long term growth for the electronics sector, irrespective of short-term economic fluctuations in vehicle sales volumes.

Accelerated Transition to Electric Powertrains and High Voltage Architectures

The rapid proliferation of electric vehicles across Europe is further boosting the expansion of the European automotive electronics market. Electrification demands a complete reimagining of the vehicle architecture, replacing mechanical systems with complex electronic controls for battery management, thermal regulation, and power conversion. As per the European Automobile Manufacturers Association, sales of fully electric cars in the European Union have surged, representing a growing share of total new car registrations, as charging infrastructure expands. Each electric vehicle requires sophisticated Battery Management Systems to monitor cell health, high voltage inverters to convert direct current to alternating current for the motor, and onboard chargers to manage grid interaction. These components rely heavily on wide bandgap semiconductors, like silicon carbide, to ensure efficiency, and durability, under high stress. The shift also necessitates advanced power distribution units that can handle voltages up to 800 volts in premium segments, driving demand for robust electronic switching devices. Furthermore, the integration of regenerative braking systems, and electric power steering, adds layers of electronic complexity that are absent in traditional drivetrains. This structural transformation ensures that the value of electronics per vehicle increases substantially, creating a robust demand pipeline for specialized semiconductor, and module manufacturers, throughout the European supply chain.

MARKET RESTRAINTS

Critical Shortage of Semiconductor Supply and Geopolitical Vulnerabilities

The persistent vulnerability of the European automotive sector to global semiconductor supply chain disruptions and geopolitical tensions is hampering the European automotive electronics market growth. The regional market relies heavily on imported microchips, with a significant portion sourced from regions prone to logistical bottlenecks, or political instability. As per the International Organization of Motor Vehicle Manufacturers, the global chip shortage resulted in the loss of millions of vehicle production units in Europe, exposing the fragility of just in time manufacturing models. Although the European Chips Act aims to increase local production capacity, building fabrication plants is a capital intensive, and time consuming, process that cannot address immediate deficits. The automotive grade chips required for safety critical applications often utilize mature nodes, which are less prioritized by foundries compared to high margin consumer electronics processors. This allocation imbalance leaves European automakers competing for limited supplies, leading to production halts, and delayed model launches. Furthermore, trade restrictions, and export controls, imposed by major global powers, can abruptly cut off access to essential raw materials, or finished wafers. The lack of diversified sourcing options forces manufacturers to hold larger inventories, increasing working capital requirements, and reducing operational agility. Until a more resilient, and localized supply ecosystem is fully operational, the threat of component scarcity will continue to cap production volumes, and delay the rollout of advanced electronic features.

Escalating Costs of Raw Materials and Complex Compliance Burdens

The significant headwinds from the rising costs of critical raw materials needed for electronic components and the increasingly burdensome regulatory compliance landscape is further inhibiting the growth of the European automotive electronics market. The production of automotive electronics depends heavily on rare earth elements, copper, and precious metals like gold, and palladium, prices for which have experienced extreme volatility, due to mining constraints, and speculative trading. As per the European Raw Materials Alliance, the dependency on imports for these critical inputs exposes manufacturers to price shocks, that erode profit margins, and force difficult decisions regarding feature prioritization in entry level vehicles. Simultaneously, the regulatory environment in Europe is becoming more complex, with the introduction of the Digital Product Passport, and stricter rules on hazardous substances under the REACH regulation. Compliance with these evolving standards requires extensive testing, documentation, and potential redesign of components, to ensure traceability, and environmental safety. The cost of validating software against functional safety standards, like ISO 26262, also adds substantial overhead to development cycles. Small, and medium sized suppliers, often struggle to absorb these cumulative costs, leading to market consolidation, and reduced innovation diversity. The financial strain of adhering to both material sourcing ethics, and technical safety norms, creates a high barrier to entry, slowing down the pace at which new electronic innovations can be commercialized, and scaled, across the broader vehicle fleet.

MARKET OPPORTUNITIES

Emergence of Software Defined Vehicles and Over the Air Update Capabilities

The paradigm shifts toward Software Defined Vehicles that allows manufacturers to monetize features and enhance performance remotely through Over the Air updates is a significant opportunity in the European automotive electronics market. This evolution turns the automobile into a continuously upgradable platform, opening new revenue streams beyond the initial point of sale. As per the European Association of Automotive Suppliers, the value of software in a new car is projected to increase significantly over the next decade, shifting the competitive advantage from hardware engineering, to software architecture. European automakers are increasingly partnering with technology firms to develop centralized computing platforms, that can host diverse applications ranging from infotainment enhancements, to autonomous driving algorithms. This model enables the activation of premium features, such as enhanced acceleration, or advanced navigation services, via subscription, creating recurring revenue flows that stabilize financial performance. Furthermore, Over the Air capabilities allow for rapid deployment of safety patches, and bug fixes, improving vehicle longevity, and customer satisfaction, without requiring physical workshop visits. The ability to collect anonymized telemetry data also provides valuable insights for refining future electronic designs, and understanding real world usage patterns. By embracing this software centric approach, the European market can leverage its strong engineering heritage to create differentiated products, that offer personalized experiences, thereby capturing greater value in the digital economy.

Development of Vehicle to Grid Integration and Smart Energy Ecosystems

The integration of Vehicle to Grid technology presents a substantial opportunity for the European automotive electronics market. As the continent accelerates its renewable energy transition, electric vehicles equipped with bidirectional charging capabilities can serve as distributed energy storage units, that stabilize the power grid. As per the European Network of Transmission System Operators for Electricity, millions of electric vehicles could provide flexible capacity to balance supply, and demand fluctuations, caused by intermittent wind, and solar generation. This functionality requires sophisticated power electronics, capable of managing two-way energy flow securely, and efficiently, driving demand for advanced inverters, and communication modules. Utilities, and automakers, are beginning to pilot programs where vehicle owners are compensated for feeding energy back into the grid during peak hours. This symbiotic relationship not only enhances the economic viability of electric vehicle ownership, but also positions automotive electronics as critical infrastructure for national energy security. The standardization of communication protocols across Europe further facilitates interoperability, allowing vehicles from different manufacturers to participate in unified smart grid networks. Capitalizing on this synergy allows the automotive electronics market to expand its addressable market beyond transportation, into the broader energy services sector.

MARKET CHALLENGES

Cybersecurity Threats and Vulnerabilities in Connected Vehicle Architectures

The escalating sophistication of cyber threats is a key challenge to the growth of the European automotive electronics market. As cars evolve into data centers on wheels, they become attractive targets for malicious actors seeking to steal personal information, disrupt operations, or even compromise physical safety. As per the European Union Agency for Cybersecurity, the attack surface of modern vehicles has expanded significantly, with the addition of cellular connectivity, Wi-Fi, and Bluetooth interfaces, creating multiple entry points for potential breaches. Ensuring robust cybersecurity requires continuous investment in encryption technologies, intrusion detection systems, and secure boot mechanisms, which adds complexity, and cost, to electronic control unit design. The regulatory landscape is also tightening, with the United Nations Economic Commission for Europe introducing mandatory cybersecurity management systems for vehicle type approval. Compliance demands a lifecycle approach to security, that spans from initial design, to end of life decommissioning, requiring close collaboration between silicon vendors, software developers, and automakers. Any high-profile breach could severely damage consumer trust, and trigger massive recall campaigns, posing existential risks to brands. Balancing the need for seamless connectivity, with impenetrable security, remains a delicate, and resource intensive endeavour, that tests the limits of current engineering capabilities.

Complexity of Integrating Legacy Systems with Modern Digital Platforms

The significant hurdle in harmonizing decades old legacy electronic architectures with cutting edge digital platforms required for autonomy, and connectivity is further challenging the expansion of the European automotive electronics market. Most existing vehicle designs rely on a distributed network of dozens of independent electronic control units, from various suppliers, each operating on proprietary software stacks, and communication protocols. As per analysis by leading automotive consulting firms, migrating from this fragmented setup, to a centralized high performance computing architecture, involves immense technical debt, and integration risks. The challenge lies in ensuring backward compatibility, while introducing new features that demand high bandwidth, and low latency data exchange. Interoperability issues often arise when integrating third party software solutions, or updating firmware across heterogeneous hardware environments, leading to system instabilities, or performance bottlenecks. Furthermore, the shortage of talent skilled in both automotive engineering, and advanced software development, exacerbates the difficulty of executing these complex transitions. Automakers must manage the coexistence of old, and new systems, during prolonged transformation periods, which increases validation times, and delays time to market. Failure to effectively bridge this architectural divide can result in disjointed user experiences, and compromised safety functions, undermining the potential benefits of digitalization, and slowing the overall adoption of next generation automotive electronics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.40% |

| Segments Covered | By Vehicle Type, Sales Channel, Application, and Region. |

|

Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Delphi Technologies, Continental AG, Bosch Group, Hyundai Mobis, Johnson Control, ZF Friedrichshafen AG, Hitachi Automotive Systems, Denso Corporation, Autoliv, Inc., Samsung Group, Lear Corporation, and Others. |

SEGMENTAL ANALYSIS

By Vehicle Insights

The passenger cars segment led the market by capturing 77.4% of the European automotive electronics market share in 2025. The dominance of passenger cars segment in the European market is driven by the high volume of vehicle production and the intense consumer demand for premium connectivity, and safety features in personal mobility. European buyers increasingly view the vehicle interior as an extension of their digital lives, demanding seamless integration with mobile ecosystems, high resolution touchscreens, and advanced voice recognition systems. As per the European Consumer Organisation, over seventy percent of new car buyers in Western Europe consider the quality of the infotainment system a decisive factor in their purchasing decision, often willing to pay a premium for models equipped with the latest digital interfaces. This trend forces original equipment manufacturers to integrate complex electronic architectures, including multiple display units, high speed data buses, and powerful system on chip processors, into every new model launch. The rise of subscription based services for navigation, streaming media, and remote vehicle control, further incentivizes manufacturers to embed sophisticated telematics units as standard equipment. Unlike commercial fleets, where utility often trumps luxury, the personal vehicle market thrives on differentiation through technology, ensuring that passenger cars remain the primary vessel for deploying cutting edge automotive electronics. The continuous cycle of consumer upgrades, and the short replacement cycle of personal vehicles compared to commercial trucks, sustain a robust, and steady demand for advanced electronic components in this sector.

The commercial vehicles segment is projected to register the highest CAGR of 10.4% over the forecast period in the European market owing to the rising need for fleet optimization, electrification of logistics, mandatory telemetry for heavy duty transport, aggressive regulatory mandates and corporate sustainability goals. As per the European Commission's Fit for 55 packages, there are binding targets to reduce CO2 emissions from heavy duty vehicles by fifteen percent by 2025, and thirty percent by 2030, compelling fleet operators to transition rapidly to electric powertrains. This shift necessitates the installation of specialized high voltage battery management systems, electric drive inverters, and thermal management controllers, that are far more complex than those found in traditional diesel engines. The urban logistics sector, in particular, is seeing a surge in electric van deployments, to comply with emerging zero emission zones in major cities like Paris, London, and Berlin. Each electric commercial vehicle requires a robust electronic architecture to manage range anxiety, charging schedules, and payload efficiency, driving a disproportionate increase in electronics content per unit. Furthermore, government subsidies, and incentives for green freight transport, are accelerating the adoption rate, creating a booming market for power electronics tailored to commercial applications. The sheer scale of the required fleet turnover to meet climate goals ensures that the commercial vehicle segment will experience exponential growth in electronics procurement over the coming decade.

By Sales Channel Insights

The original equipment manufacturer (OEM) channel held the overwhelming majority of the market share of the European market in 2025. The leading position of the OEM segment in the European market is attributed to the increasing complexity of vehicle architectures that require factory integrated electronic systems for safety, performance, and connectivity. The extreme technical complexity of modern automotive electronics that requires precise factory integration, and calibration, that cannot be replicated in the aftermarket is further boosting the expansion of the OEM channel segment in the European market. Contemporary vehicles feature deeply embedded networks, where electronic control units communicate via high-speed protocols like Ethernet and CAN FD, which is requiring seamless software harmonization with the vehicle's central operating system. As per engineering guidelines from the Society of Automotive Engineers, the calibration of sensors for advanced driver assistance systems, such as radar, and LiDAR, must be performed in controlled manufacturing environments, using specialized robotic equipment, to ensure millimeters level accuracy. Any deviation in alignment, or software configuration, can lead to system failures, or safety hazards, making post production installation virtually impossible for critical components. Furthermore, the trend toward zonal architectures, and centralized computing, means that electronics are no longer standalone modules, but integral parts of the vehicle's structural design. Manufacturers embed wiring harnesses, and cooling systems, specifically tailored to these electronic loads, during the assembly line process. This level of integration ensures that the vast majority of electronics, from engine management units, to infotainment heads, are installed before the vehicle leaves the factory, securing the OEM channel's dominant position in the value chain.

The aftermarket segment is anticipated to witness the fastest CAGR of 8.12% over the forecast period in the European market owing to the aging vehicle parc, the rising popularity of retrofitted connectivity solutions, and the need to upgrade older fleets with modern safety technologies. As per the European Automobile Manufacturers Association, the average age of passenger cars in the European Union has reached an all-time high of over twelve years, creating a vast installed base of vehicles lacking contemporary electronic features. Many owners of these older vehicles seek to enhance safety, and resale value, by installing aftermarket solutions, such as backup cameras, blind spot monitoring systems, and upgraded infotainment units with Apple CarPlay, or Android Auto. The European Union's push to extend advanced safety requirements to existing fleets, through periodic technical inspections, encourages the adoption of retrofittable electronic aids. Specialized workshops, and accessory retailers, are responding with plug and play kits that allow for relatively easy installation, without voiding warranties. This trend is particularly strong in Southern, and Eastern Europe, where vehicle replacement cycles are longer, due to economic factors. The ability to breathe new life into older vehicles through electronic upgrades provides a cost-effective alternative to buying new cars, which is fuelling a robust demand for aftermarket electronics, that grows in tandem with the aging fleet.

By Application Insights

The power train electronics segment led the market by holding 31.3% of the European market share in 2025. The growth of the power train electronics segment in the European market can be credited to the massive structural shift toward electrification, and the stringent efficiency requirements for both electric, and internal combustion powertrains. As per production data from the European Battery Alliance, the ramp up of gigafactories across Europe is directly correlated with the increased output of electric vehicles, each requiring at least one main traction inverter, and multiple voltage conversion units. These components are responsible for converting direct current from the battery into alternating current for the motor, and stepping down voltage for low voltage accessories, functions that are critical for vehicle operation. The transition to 800 volt architectures in premium electric vehicles further amplifies the value, and complexity, of these electronic systems, necessitating the use of advanced silicon carbide semiconductors. Unlike other applications, where electronics serve auxiliary functions, power train electronics are the core enablers of propulsion in the new era of mobility. The sheer volume of electric vehicle production targets set by European governments ensures a consistent, and high volume demand for these specific electronic components. Furthermore, hybrid vehicles also require sophisticated power control units to manage the interplay between electric motors, and combustion engines, broadening the addressable market beyond pure battery electrics, and solidifying the segment's dominance.

The advanced driver assistance systems (ADAS) segment is poised to grow at a CAGR of 15.5% over the forecast period in the European market owing to the mandatory safety legislation, the pursuit of autonomous driving capabilities, and the increasing affordability of sensor technologies. As per the General Safety Regulation enforced by the European Commission, technologies such as intelligent speed assistance, emergency lane keeping, and advanced emergency braking, became mandatory for new type approvals in 2022 and for all new registrations in 2024. This regulatory cliff edge has triggered a massive surge in the deployment of cameras, radars, ultrasonic sensors, and the associated electronic control units needed to process their data. Automakers have had to rapidly retool their supply chains, and software stacks, to comply, resulting in an unprecedented uptake of ADAS electronics across all vehicle segments, from entry level, to luxury. The regulation does not merely suggest these features, but makes them a prerequisite for market entry, creating an inelastic demand curve that guarantees growth, regardless of economic conditions. Furthermore, the scope of these regulations is expected to expand in future revisions, to include more advanced functionalities like driver monitoring, and intersection assistance, promising a long runway for continued expansion. This legal imperative transforms ADAS from a competitive differentiator, into a compliance necessity, driving the segment's rapid ascent.

COUNTRY LEVEL ANALYSIS

Germany Automotive Electronics Market Analysis

Germany held the dominant position in the European automotive electronics market in 2025 by commanding 26.9% of the regional market share. The dominance of Germany in the European market is driven by its status as the continent's largest vehicle producer, and the home base for global original equipment manufacturers, and tier one suppliers. The German market is characterized by an unparalleled ecosystem of engineering excellence, where companies like Bosch, Continental, and Infineon Technologies drive innovation in semiconductor, and sensor technologies. As per data from the German Association of the Automotive Industry, the country accounts for nearly one third of all passenger car production in Europe, with a heavy skew toward premium vehicles that incorporate the highest density of electronic content. The German government's strategic support for the semiconductor industry, through the European Chips Act implementation, further strengthens local supply chains for automotive grade microchips. The nation's strong focus on Industry 4.0 principles has led to highly automated manufacturing facilities, capable of integrating complex electronic systems with precision. Furthermore, the robust research, and development infrastructure, including collaborations between universities, and automotive giants, fosters rapid prototyping, and deployment of next generation electronics. The domestic demand for high performance vehicles, with advanced driver assistance, and connectivity features, also fuels local consumption. This combination of manufacturing scale, technological leadership, and supportive policy framework, cements Germany's position as the primary engine of the European automotive electronics sector.

France Automotive Electronics Market Analysis

France secured the second largest position in the European automotive electronics market in 2025. The growth of France in the European market can be credited to its strong automotive manufacturing heritage, and aggressive national strategies for electric mobility, and digital sovereignty. The French market is distinguished by the presence of major automakers like Stellantis, and Renault, who are rapidly transitioning their fleets to electric platforms, that require extensive electronic architectures. As per the French Ministry of Economy and Finance, the government has committed billions of euros to support the electrification of the automotive supply chain, including specific grants for battery, and power electronics production. France is also becoming a hub for software defined vehicle development, with significant investments in startups focused on autonomous driving algorithms, and connected car services. The country's emphasis on sovereign technology has led to partnerships aimed at reducing dependency on non-European chip suppliers, fostering a resilient local ecosystem for automotive semiconductors. Additionally, the French consumer market shows a high adoption rate for electric vehicles, driven by generous purchase bonuses, and strict low emission zone regulations in cities like Paris. This policy driven demand stimulates the integration of advanced powertrain, and telematics electronics. The synergy between industrial policy, manufacturing capacity, and consumer incentives, ensures France remains a critical pillar of the regional automotive electronics landscape.

United Kingdom Automotive Electronics Market Analysis

The United Kingdom is anticipated to account for a notable share of the European automotive electronics market during the forecast period due to its world leading research in autonomous systems, a strong niche in premium automotive manufacturing, and a vibrant tech startup scene. Although vehicle production volumes have fluctuated in recent years, the UK maintains a disproportionate influence on the high value end of the automotive electronics spectrum. As per the Society of Motor Manufacturers and Traders, the UK is a global center for the development of autonomous driving technologies, hosting numerous testbeds, and innovation centers, supported by government funding. The presence of luxury brands like Jaguar Land Rover, and Bentley, drives demand for bespoke, high complexity electronic systems, including advanced infotainment, bespoke driver assistance, and luxury comfort controls. The UK's strength in artificial intelligence, and software engineering, complements its hardware capabilities, enabling the development of sophisticated software stacks for next generation vehicles. Furthermore, the government's commitment to banning the sale of new petrol, and diesel cars by 2030, has accelerated investment in electric powertrain electronics, and charging infrastructure. The collaboration between academic institutions, and industry players, fosters a culture of innovation that keeps the UK at the forefront of automotive digitalization. This focus on high tech, high value electronics, ensures the UK remains a key player, despite broader manufacturing challenges.

Italy Automotive Electronics Market Analysis

Italy represents a significant force in the European automotive electronics market. The specialization in high performance sports cars, luxury vehicles and a robust component manufacturing sector that supplies the wider European market are propelling the Italian market expansion. The Italian automotive electronics landscape is heavily influenced by the requirements of iconic brands like Ferrari, Lamborghini, and Maserati, which demand cutting edge electronics for performance management, active aerodynamics, and exclusive infotainment experiences. As per Confindustria ANFIA, the Italian automotive supply chain includes hundreds of specialized SMEs that produce high precision electronic components, sensors, and wiring harnesses, for export to other European assembly plants. The country's strong design culture extends to the user interface, and digital experience of vehicles, driving innovation in human machine interaction systems. Italy is also seeing growth in the commercial vehicle sector, particularly in luxury motorhomes, and specialized transport, which incorporate advanced electronics for comfort, and safety. The government's incentives for industrial digitization, and green transition, are encouraging local suppliers to upgrade their capabilities in electric drive systems, and connected technologies. The unique blend of artisanal craftsmanship, and high-tech engineering that allow Italy to occupy a lucrative niche in the premium, and super premium segments of the automotive electronics market.

The Czech Republic is anticipated to account for a notable share of the European automotive electronics market during the forecast period. Czech Republic is serving as a crucial manufacturing hub for Central Europe, and a key production base for major international automotive groups, including Skoda Auto, and Hyundai. The country's market status is defined by its high volume of vehicle production relative to its population, making it a dense cluster for automotive electronics assembly, and integration. As per the Czech Automotive Industry Association, the sector is the largest contributor to the national industrial output, with a significant portion of production destined for export to Western European markets. The Czech Republic has attracted substantial foreign direct investment in electronics manufacturing, with several tier one suppliers establishing plants to produce control units, sensors, and infotainment systems locally. The availability of a skilled engineering workforce, and competitive operational costs, makes it an attractive location for high volume production of standardized electronic modules. The government's support for research, and development in electromobility, is fostering the gradual shift toward electric vehicle component manufacturing. The strategic location within the European supply chain allows for efficient logistics, and just in time delivery, to neighbouring German, and Slovakian plants. This role as a high efficiency manufacturing backbone ensures the Czech Republic remains a vital component of the European automotive electronics value chain.

COMPETITIVE LANDSCAPE

The competition in the Europe automotive electronics market is intensely dynamic and characterized by a fierce rivalry between established tier one suppliers and emerging technology entrants vying for dominance in the software defined vehicle era. Traditional giants leverage their decades of engineering expertise and deep relationships with automakers to maintain leadership in safety critical hardware and integrated systems. However, new players specializing in artificial intelligence, cloud connectivity, and semiconductor design are disrupting the status quo by offering agile and innovative solutions that challenge conventional architectures. The shift toward centralized computing has intensified battles for control over the vehicle operating system and data ecosystem, turning software capabilities into a primary competitive differentiator. Price pressure remains significant as automakers seek to reduce costs while demanding higher performance and faster development cycles. Regulatory compliance regarding cybersecurity and functional safety adds another layer of complexity, favoring companies with robust quality management systems. The race to secure semiconductor supply chains further exacerbates competitive tensions, forcing participants to make substantial capital investments to guarantee component availability. This volatile environment demands constant adaptation and strategic agility to sustain market relevance and profitability.

KEY MARKET PLAYERS

These are some of the major key market players involved in the European automotive electronics market.

- Delphi Technologies

- Continental AG

- Robert Bosch GmbH

- Bosch Group

- Infineon Technologies AG

- Hyundai Mobis

- Johnson Control

- ZF Friedrichshafen AG

- Hitachi Automotive Systems

- Denso Corporation

- Autoliv, Inc.

- Samsung Group

- Lear Corporation

Top Players In The Market

- Robert Bosch GmbH stands as a preeminent force in the Europe automotive electronics landscape, leveraging its vast engineering heritage to supply critical components globally. The company plays a pivotal role in advancing electrification and autonomous driving technologies through its comprehensive portfolio of sensors, control units, and software solutions. Recently Bosch has intensified its investment in semiconductor manufacturing by partnering with foundries to secure supply chains for power chips essential for electric vehicles. The firm actively collaborates with European automakers to develop centralized vehicle computer architectures that simplify wiring and enhance software update capabilities. Their commitment to sustainability drives the creation of energy efficient electronic systems that reduce overall vehicle carbon footprints. By establishing new research centers focused on artificial intelligence and neural networks, Bosch ensures its technologies remain at the forefront of innovation. These strategic moves reinforce its position as a trusted partner for original equipment manufacturers seeking reliable and cutting-edge electronic solutions for the future of mobility.

- Continental AG operates as a leading technology company shaping the future of mobility with a strong emphasis on intelligent vehicle architectures and connectivity solutions across Europe and the world. The corporation contributes significantly to the global market by providing advanced driver assistance systems, high performance computers, and digital ecosystem services that redefine the driving experience. Recent actions include the strategic spinoff of its powertrain division to focus resources on electronics and software development for autonomous and electric vehicles. Continental has forged key partnerships with major chipmakers to co-develop next generation zone controllers that streamline vehicle electrical systems. The company also invests heavily in cybersecurity measures to protect connected vehicles from emerging digital threats. Their expansion of software engineering teams across European hubs enables rapid deployment of over the air update platforms. By prioritizing sustainable production methods and circular economy principles for electronic components, Continental strengthens its reputation as an innovator dedicated to safe, efficient, and environmentally responsible automotive technologies.

- Infineon Technologies AG serves as a cornerstone of the European automotive electronics sector by delivering superior semiconductor solutions that power everything from electric drivetrains to advanced safety systems globally. The company specializes in power semiconductors, microcontrollers, and sensors that are indispensable for modern vehicle functionality and efficiency. Infineon recently accelerated its capacity expansion for silicon carbide chips which are critical for high voltage electric vehicle applications and fast charging infrastructure. The firm has secured long term supply agreements with leading European car manufacturers to ensure stable availability of essential electronic components amidst global shortages. Their continuous investment in research and development focuses on integrating artificial intelligence into microcontrollers for smarter real time decision making in autonomous driving scenarios. Infineon also leads initiatives to standardize cybersecurity protocols for automotive chips to safeguard vehicle integrity. By fostering deep collaborations with technology startups and academic institutions, Infineon maintains its technological edge and drives the industry toward a more electrified and automated future.

Top Strategies Used By Key Market Participants

Key players in the Europe automotive electronics market primarily employ vertical integration strategies to secure critical semiconductor supplies and reduce dependency on external foundries. Companies are increasingly investing in internal chip design and manufacturing capabilities to mitigate supply chain risks and ensure consistent production volumes. Strategic partnerships and joint ventures with technology firms and startups serve as another vital approach to accelerate innovation in software defined vehicles and autonomous driving algorithms. Major participants focus heavily on research and development expenditures to pioneer next generation sensors and high performance computing platforms that meet evolving safety standards. Acquisitions of specialized software companies allow traditional hardware manufacturers to expand their digital service offerings and capture recurring revenue streams. Furthermore, firms are adopting sustainable manufacturing practices and circular economy principles to comply with stringent European environmental regulations and appeal to eco conscious consumers. These multifaceted strategies enable market leaders to maintain competitiveness and drive growth in a rapidly transforming industry landscape.

MARKET SEGMENTATION

This market research report on the European automotive electronics market is segmented and sub-segmented into the following categories.

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Sales Channel

- OEM

- Aftermarket

By Application

- Advanced Driver Assistance System (ADAS)

- Power Trains

- Security Systems

- Entertainment

- Body Electronics

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What role do electronic systems play in modern European vehicles?

They control safety, power management, connectivity, and driver assistance functions.

Which vehicle features rely heavily on automotive electronics today?

Navigation systems, advanced driver assistance, infotainment, and battery management depend on electronic components.

What factors are accelerating the use of electronics in European cars?

Electric mobility, stricter safety standards, and demand for connected vehicle features.

Which components form the core of automotive electronic architecture?

Sensors, control units, semiconductors, and communication modules manage vehicle operations.

What makes electronics essential for electric vehicle performance?

They regulate battery charging, energy distribution, and motor control systems.

Which safety technologies depend on advanced automotive electronics?

Features like automatic emergency braking and lane assistance rely on sensor-based electronics.

What challenges affect automotive electronics development in Europe?

Complex integration of hardware and software requires rigorous testing and validation.

Which industries support the production of automotive electronic components?

Semiconductor manufacturing, software engineering, and electronics assembly play key roles.

What advantages do digital dashboards offer drivers?

They provide real-time vehicle data and customizable driving information displays.

Which technologies are improving vehicle connectivity across Europe?

5G communication modules and cloud-based services enable smarter vehicle interaction.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com