Europe Automotive Market Size, Share, Trends And Growth Forecasts Research Report, Segmented By Vehicle Type, By Propulsion Type, And Country (The U.K, France, Spain, Germany, and Italy, Russia, Sweden, Denmark, Switzerland, and Nether Land), Industry Analysis (2025 to 2033)

Europe Automotive Market Report Summary

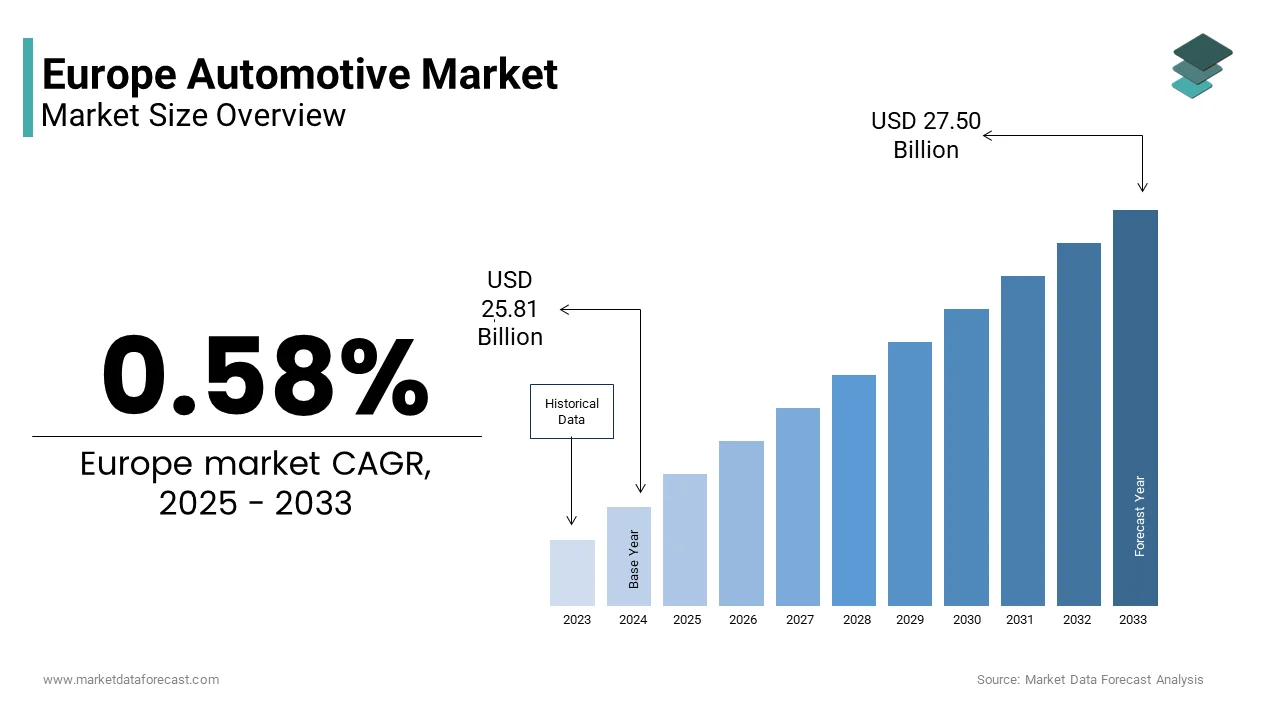

The European automotive market was valued at USD 25.65 billion in 2024, is estimated to reach USD 25.81 billion in 2025, and is projected to reach USD 27.50 billion by 2033, growing at a CAGR of 0.58% from 2025 to 2033. The growth of the European automotive market is driven by ongoing advancements in vehicle technology, a gradual shift toward electrification, and steady demand for passenger vehicles across major economies. However, market growth remains moderate due to regulatory pressures on emissions, supply chain disruptions, and the transition challenges faced by traditional automakers. Nonetheless, the rising adoption of electric vehicles (EVs), connected mobility solutions, and government incentives for clean transportation continue to support long-term market stability.

Key Market Trends

- Growing adoption of electric and hybrid vehicles in response to stringent EU emission norms.

- Increasing investment in autonomous driving technologies and connected car ecosystems.

- The rising popularity of SUVs and crossovers due to their comfort, versatility, and enhanced safety features.

- Expansion of EV charging infrastructure across major European cities to support sustainable mobility.

- Strengthening the government's focus on carbon neutrality and circular automotive production models.

Segmental Insights

- Based on vehicle type, the SUV segment dominated the European automotive market, holding a 40.8% share in 2024, driven by growing consumer preference for spacious, premium, and safety-oriented vehicles suitable for urban and long-distance travel.

- Based on propulsion, the internal combustion engine (ICE) vehicles segment remained prominent, accounting for 60.6% of the European automotive market share in 2024, as conventional vehicles continue to dominate despite the gradual transition toward electric mobility, supported by strong after-sales networks and affordability in certain markets.

Regional Insights

- The European automotive market exhibits strong regional variation based on manufacturing base, consumer preferences, and policy frameworks.

- Germany outperformed other regions, capturing 25.7% of the market share in 2024, supported by its robust automotive manufacturing ecosystem, technological leadership, and strong exports of luxury and performance vehicles.

- France and Italy demonstrated steady demand growth, fueled by a focus on hybrid and electric vehicle development and domestic production incentives.

- The United Kingdom is witnessing a gradual market recovery post-Brexit, driven by EV adoption and the expansion of smart mobility projects.

- Eastern Europe, including Poland and Hungary, is emerging as a key hub for automotive component manufacturing and EV assembly operations.

Competitive Landscape

- The European automotive market is highly competitive, with global and regional manufacturers focusing on electrification, digitalization, and supply chain resilience to maintain competitiveness.

- Companies are investing in battery technology, AI-driven vehicle systems, and sustainability initiatives to align with the European Green Deal and future mobility trends.

- Prominent players in the European automotive market include Toyota, Tesla, Honda, Hyundai, General Motors, Volkswagen, Stellantis, BYD, Maruti, and Suzuki.

- These companies are emphasizing innovation in EV platforms, expansion of manufacturing capacity, and strategic collaborations to strengthen their market positions and meet Europe’s evolving transportation demands.

Europe Automotive Market Size

The Europe automotive market size was valued at USD 25.65 billion in 2024 and is anticipated to reach USD 25.81 billion in 2025 to USD 27.50 billion by 2033, growing at a CAGR of 0.58% during the forecast period from 2025 to 2033.

Automotive refers to anything related to motor vehicles, especially those designed for transportation on roads. The market covers all companies and activities involved in the design, development, manufacturing, marketing, selling, repairing, and modification of motor vehicles, including passenger cars, light trucks, commercial vehicles, and buses. According to sources, millions of vehicles were registered, with Germany contributing a portion of total sales. SUVs dominate the vehicle landscape, accounting for a share of all registrations, as per studies. The shift toward electric vehicles (EVs) is accelerating, with EV sales surging by 35% annually, fueled by stringent emission regulations and government incentives. Sweden and Norway lead in EV adoption, with over 80% of new car sales being electric or hybrid models. Despite challenges such as supply chain disruptions, the market remains resilient, supported by innovation and growing demand for sustainable mobility solutions.

MARKET DRIVERS

Stringent Emission Regulations

Stringent emission regulations imposed by the European Union are a primary driver of the Europe automotive market. According to the European Commission, automakers face penalties of €95 per gram of CO2 emitted above the limit, compelling manufacturers to accelerate the production of low-emission vehicles. By 2030, new vehicles must emit 55% less CO2 compared to 2021 levels, as mandated by the EU Green Deal. This regulatory push has resulted in an increase in EV production capacity across Europe, according to research. Countries like Germany and France have embraced these policies, investing heavily in EV manufacturing hubs. Apart from these, local governments offer incentives such as tax rebates and reduced road taxes, which further encourage adoption. These measures collectively position regulatory frameworks as a transformative force in driving market expansion.

Rising Urbanization and Mobility Needs

The rapid pace of urbanization and evolving mobility needs are also a major accelerator of the expansion of the Europe automotive market. According to Eurostat, urban populations in Europe account for a portion of the total population, creating robust demand for compact and fuel-efficient vehicles. Cities like London, Paris, and Berlin have witnessed a surge in shared mobility services, with a large number of users opting for ride-hailing and car-sharing platforms, as sources. This trend has amplified the need for small, versatile vehicles such as hatchbacks and compact SUVs, particularly among millennials and Gen Z consumers who prioritize affordability and convenience. According to sources, urbanization contributes to an annual increase in vehicle sales by emphasizing its vital role in market growth.

MARKET RESTRAINTS

Supply Chain Disruptions and Chip Shortages

Supply chain disruptions and semiconductor shortages pose a barrier to the growth of the Europe automotive market. According to the European Automobile Manufacturers' Association, global chip shortages caused a significant impact on vehicle production in 2023 and also impacted profit margins for manufacturers. This issue is particularly pronounced for electric vehicles (EVs), which rely heavily on advanced electronics for battery management and connectivity systems. In addition, geopolitical tensions have exacerbated delays in shipping and logistics, further complicating procurement. As per a study published by the European Central Bank, these disruptions have slowed production cycles, hindering market growth and limiting accessibility to affordable vehicles.

High Costs of Electric Vehicle Adoption

The high costs associated with transitioning to electric vehicles (EVs) restrain the growth of the Europe automotive market. According to the European Consumer Organisation, premium EVs can cost up to €50,000, making them inaccessible for lower-income households. Even with government subsidies, out-of-pocket expenses deter many individuals from adopting these technologies. This financial burden is further compounded by the rising costs of lithium-ion batteries, which account for a portion of an EV’s total cost, as per sources. In countries like Italy and Spain, where subsidies are limited, adoption rates lag behind Western Europe. These factors hinder the broader adoption of EVs despite growing consumer demand for sustainable mobility solutions.

MARKET OPPORTUNITIES

Growing Demand for Connected and Autonomous Vehicles

The increasing demand for connected and autonomous vehicles offers new opportunities for the growth of the Europe automotive market. According to studies, a portion of vehicles sold feature advanced driver-assistance systems (ADAS), which reflects consumer interest in smart mobility solutions. Germany and Sweden have positioned themselves as leaders in this space, with startups developing AI-driven navigation systems tailored to urban environments. As per a study by the European Innovation Council, connected vehicles reduce traffic accidents, which appeals to both consumers and corporate clients. These innovations position connected and autonomous vehicles as a transformative force in the market, which ensures sustained growth and innovation.

Advancements in Battery Technology

Advancements in battery technology are setting up new opportunities for the expansion of the Europe automotive market. According to sources, next-generation solid-state batteries are projected to increase energy density, which reduces charging times and extends driving ranges. Sweden and Germany have positioned themselves as leaders in this space, with research institutions collaborating with manufacturers to develop scalable solutions. Besides, the integration of renewable energy sources into battery production ensures sustainability, aligning with EU environmental goals. These factors collectively position battery innovation as a key growth driver in the market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 0.58% |

| Segments Covered | By Vehicle Type, Propulsion Type, And Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | Toyota, Tesla, Honda, Hyundai, General Motors, Volkswagen, Stellantis, BYD, Maruti, Suzuki |

SEGMENTAL ANALYSIS

By Vehicle Insights

The SUV segment dominated the Europe automotive market and held a share of 40.8% in 2024. Their versatility offers spacious interiors and superior performance, which appeal to both urban and rural consumers has mainly contributed to the growth of the SUV segment. SUV sales grew annually in recent years, which reflects their important role in meeting diverse mobility needs, as per sources. Germany leads in SUV adoption, leveraging advanced manufacturing techniques to enhance product quality. These vehicles are also associated with lower long-term ownership expenses compared to other car segments. Furthermore, government incentives for low-emission models ensure compliance with environmental standards, appealing to eco-conscious consumers.

The pick-ups and light trucks segment is estimated to register the fastest CAGR of 12.8% from 2025 to 2033. This rapid expansion of the pick-ups and light trucks segment is fueled by their increasing use in commercial applications, such as logistics and construction, which require durable and versatile vehicles. According to sources, pickup trucks have achieved strong market success in rural regions across Europe by appealing to businesses seeking cost-effective solutions. Sweden and Denmark have embraced this trend, with startups developing lightweight and fuel-efficient models tailored to specific industries. As per research, these vehicles help lower operational expenses, which makes them attractive for both commercial and personal use. These factors position pick-ups and light trucks as the most dynamic segment in the market.

By Propulsion Insights

In 2024, the internal combustion engine (ICE) vehicles segment remained prominent in the Europe automotive market by accounting for 60.6% share in 2024. The dominance of the internal combustion engine (ICE) vehicle segment is ensured by its widespread adoption and affordability, making it the preferred choice for budget-conscious consumers. According to the European Automobile Manufacturers' Association, ICE vehicles account for a portion of rural vehicle sales, which reflects their vital role in regions with limited EV infrastructure. Germany leads in ICE production, leveraging advanced manufacturing techniques to enhance fuel efficiency and reduce emissions. Apart from these, government subsidies for low-emission ICE models ensure broader accessibility, appealing to consumers seeking cost-effective mobility solutions.

The electric vehicles (EVs) segment is anticipated to witness the fastest CAGR of 18.5% during the forecast period, owing to stringent emission regulations and rising consumer awareness about sustainable mobility. According to the International Energy Agency, EV sales surged annually in recent years, driven by features such as zero emissions and reduced operating costs. Sweden and Norway have embraced this trend, with governments offering substantial incentives such as tax exemptions and free parking. These factors position EVs as the most dynamic propulsion type in the market.

COUNTRY ANALYSIS

Germany Automotive Market Analysis

Germany outperformed other regions in the Europe automotive market by capturing 25.7% of the regional market in 2024. The domination of Germany is largely because of the country’s robust manufacturing base, advanced technological infrastructure, and strong policy support for innovation. According to research, millions of vehicles were produced nationwide, supported by investments in electric and autonomous vehicle technologies. Berlin and Munich lead in EV deployment by leveraging partnerships between automakers and local governments to promote clean transportation. Collaborations between academia and industry foster innovation, with startups developing next-generation batteries tailored to long-distance travel.

France Automotive Market Analysis

France was the second-largest region in the Europe automotive market and occupied a 15.5% share in 2024. The growth of France is driven by its focus on sustainable mobility and consumer-friendly policies, which include subsidies and tax rebates for low-emission vehicles. According to sources, EV sales grew annually in urban areas by reflecting their widespread adoption among environmentally conscious consumers. Paris leads in EV infrastructure development, with public charging points ensuring seamless refueling. Besides, the government’s focus on renewable energy integration has encouraged manufacturers to adopt greener practices, ensuring compliance with EU environmental standards. France's smaller scale compared to Germany is offset by its strategic emphasis on sustainability, which positions it as a key player in the regional market.

COMPETITIVE LANDSCAPE

The Europe automotive market is characterized by intense competition, driven by the presence of established players and emerging innovators. The market is moderately consolidated, with Volkswagen Group, Stellantis, and BMW Group dominating the landscape. These companies compete based on technological superiority, product scalability, and strategic collaborations. Smaller firms, however, are gaining ground by focusing on niche segments, such as compact EVs and connected vehicles. The competitive dynamics are further shaped by regulatory requirements, which mandate rigorous testing and compliance, creating barriers to entry for new entrants. Pricing burdens also influence competition, as companies strive to offer cost-effective solutions without compromising quality. Despite these challenges, the market’s growth potential remains robust, fueled by increasing demand for sustainable mobility and advancements in automotive technologies.

KEY MARKET PLAYERS

A few of the market players in the Europe automotive market include

- Toyota

- Tesla,

- Honda

- Hyundai

- General Motors

- Volkswagen

- Stellantis

- BYD

- Maruti

- Suzuki

Top Players In The Market

The Europe automotive market is led by three key players: Volkswagen Group, Stellantis, and BMW Group. These companies collectively account for over 40% of the global market share, leveraging their extensive product portfolios and innovative technologies. Volkswagen dominates with its flagship brands such as Audi and Porsche, which are widely regarded as benchmarks for performance and sustainability. According to sources, the company’s strong revenue performance in Europe highlights its dominant position in the automotive sector. Stellantis continues to compete effectively through accessible and innovative electric models that appeal to a broad customer base. The company is also expanding its electric vehicle production capabilities to support steady growth and wider market adoption, as per research. BMW rounds out the top three, with a strong presence in luxury and high-performance vehicles. Its commitment to sustainability ensures eco-friendly designs, supporting its global standing.

Top Strategies Used By Key Market Participants

Key players in the Europe automotive market employ a variety of strategies to strengthen their positions. Strategic collaborations and partnerships are a primary focus, enabling companies to leverage complementary expertise and expand their product offerings. For instance, Volkswagen has partnered with Northvolt to develop next-generation batteries tailored to long-distance travel. Mergers and acquisitions are another important strategy, allowing firms to consolidate their market presence. Stellantis, for example, acquired a startup specializing in autonomous driving technologies, enhancing its capabilities in smart mobility solutions. Furthermore, these companies prioritize geographic expansion, targeting underserved regions to increase accessibility. BMW has invested heavily in establishing EV production facilities across Eastern Europe, ensuring broader market penetration. Product innovation remains central to their strategies, with substantial R&D investments driving the development of advanced solutions tailored to evolving consumer needs.

MARKET SEGMENTATION

This research report on the Europe automotive market is segmented and sub-segmented into the following categories.

By Vehicle Type

- Hatchback

- Sedan

- SUV

- MPV

- Vans

- Pick-Ups/Light Trucks

By Propulsion Type

- ICE

- Hybrid & Electric

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What defines the current state of the European automotive market?

The market is undergoing a historic transformation—shifting from internal combustion engines (ICE) to electric mobility—amid tightening emissions regulations, supply chain recalibration, and evolving consumer preferences toward sustainability and digital features.

Which countries lead vehicle production and sales in Europe?

Germany, France, Italy, Spain, and the UK are the largest automotive markets by volume, with Germany remaining the production powerhouse, home to premium OEMs like Volkswagen, BMW, and Mercedes-Benz.

How is the EU’s 2035 ICE ban impacting the industry?

The phaseout of new CO₂-emitting cars by 2035 is accelerating EV investments, with nearly all major automakers committing to full electrification—though concerns remain over charging infrastructure, raw material access, and affordability.

Are electric vehicles (EVs) gaining significant market share?

Yes—EVs accounted for over 15% of new car registrations in 2024, driven by EU CO₂ targets, national subsidies (e.g., in Germany and France), and expanding model lineups, though growth slowed slightly in 2025 due to subsidy rollbacks and economic headwinds.

What role do Chinese EVs play in the European market?

Chinese brands like BYD, MG (SAIC), and NIO are rapidly gaining share with competitively priced, tech-rich EVs—prompting the EU to launch anti-subsidy investigations and consider tariffs to protect domestic manufacturers.

Who are the key automotive players in Europe?

Leading OEMs include Volkswagen Group, Stellantis, BMW Group, Mercedes-Benz, and Renault Group, while major suppliers like Bosch, Continental, and ZF are pivoting toward e-mobility, software, and autonomous systems.

How is digitalization reshaping the European car experience?

Over-the-air (OTA) updates, connected services, advanced driver-assistance systems (ADAS), and in-car infotainment are now key purchase drivers—pushing automakers to partner with tech firms and develop in-house software stacks.

What challenges is the industry facing today?

High energy costs, skilled labor shortages, slow public charging rollout, geopolitical trade tensions, and consumer affordability concerns are creating headwinds despite strong policy support for green transition.

Is the used car market growing in response to new EV costs?

Yes—soaring new car prices and extended EV waiting times have boosted demand for quality used ICE and hybrid vehicles, especially among cost-conscious buyers in Southern and Eastern Europe.

What’s the market outlook for 2025–2030?

Europe’s automotive sector will remain in transition—EV adoption will continue rising, but at a moderated pace, while software-defined vehicles, circular economy practices, and regional supply chain resilience become strategic priorities for long-term competitiveness.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com