Europe Balsa Wood Market Size, Share, Trends & Growth Forecast Report By Form, By Application, and By Country (Germany, France, Italy, United Kingdom & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Balsa Wood Market Report Summary

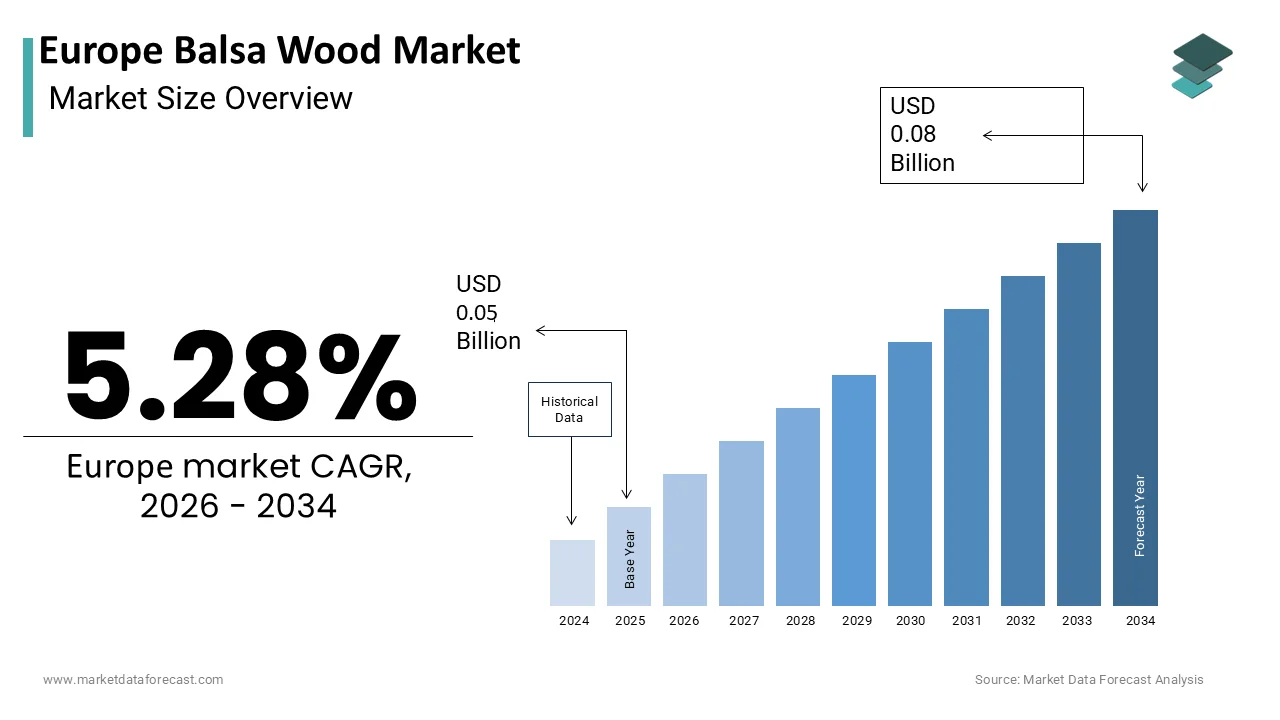

The Europe Balsa Wood Market was valued at USD 0.05 billion in 2025 and is projected to reach USD 0.08 billion by 2034, growing from USD 0.05 billion in 2026 at a CAGR of 5.28% during the forecast period. Growth is driven by expansion of offshore wind energy infrastructure, growing demand for lightweight solutions in marine and transportation sectors, and development of hybrid composite structures. Supply chain concentration in Ecuador and competition from synthetic core materials are shaping market dynamics.

Key Market Trends

- Rising use of balsa-cored blades in offshore wind turbine manufacturing

- Growing adoption of hybrid composites combining balsa with natural fibers like flax and hemp

- Increasing exploration of balsa composites in electric vehicle interior components

- Expansion of balsa wood use in sustainable and modular building construction

- Rising demand for EU Deforestation Regulation-compliant certified sustainable sourcing

Segmental Insights

- Based on form, end grain balsa captured the dominant share in 2025, driven by exceptional compressive strength required for wind turbine blade roots and spar caps.

- Based on application, renewable energy held the leading share in 2025, driven by balsa's critical role as a core material in offshore wind turbine blades.

- Edge grain is the fastest-growing form segment, projected at a CAGR of 8.2%, driven by cost-effectiveness in marine decking and automotive interior applications.

Regional Insights

- Germany led the market in 2025, supported by its offshore wind leadership and strong automotive lightweighting initiatives.

- France holds a significant share, driven by its aerospace and luxury yacht manufacturing industries.

- Italy is a prominent market supported by its dominant position in global super yacht production.

- United Kingdom contributes notably due to its aggressive offshore wind capacity targets.

- Marine is the fastest-growing application segment, projected at a CAGR of 9.5%, driven by a resurgence in luxury yacht and recreational boating activity.

Competitive Landscape

The market is highly competitive, with specialized core material manufacturers and diversified composite solution providers competing on product quality, technical expertise, and supply chain reliability. Companies are investing in vertical integration with South American plantations and hybrid core innovation to secure supply and enhance performance.

Prominent players in the market include 3A Composites GmbH, Schweiter Technologies AG, CoreLite Inc., DIAB Group (Ratos AB), The Gill Corporation, SINOKIKO BALSA TRADING CO. LTD., Carbon-Core Corporation, Bcomp Ltd., Core Composites Ltd., Sicomin Epoxy Systems, Pontus Wood Group, and Lianyungang Qiaoyun Balsa Co. Ltd.

Europe Balsa Wood Market Size

The Europe Balsa Wood Market is projected to grow from USD 0.05 billion in 2025 to USD 0.05 billion in 2026 and reach USD 0.08 billion by 2034, registering a CAGR of 5.28% during the forecast period from 2026 to 2034.

Balsa wood is a lightweight hardwood primarily sourced from tropical regions such as Ecuador and Peru for high-performance industrial applications across the continent. This unique material is characterized by an exceptional strength-to-weight ratio, making it indispensable for core materials in composite structures within the wind energy, marine, aerospace, and transportation sectors. In Europe, balsa wood is predominantly processed into sandwich panels that provide structural rigidity while minimizing overall weight, a critical factor in energy-efficient design. According to WindEurope, the European Union reached a total installed wind power capacity of 272 gigawatts by the end of 2025, with offshore projects increasingly relying on balsa-cored blades to withstand harsh marine environments and reduce logistical costs. The material’s natural origin aligns with the European Green Deal objectives, which prioritize sustainable and bio-based materials over synthetic alternatives like polyvinyl chloride foam. As per the European Commission, the construction and industrial sectors are under pressure to reduce carbon footprints, driving manufacturers to seek renewable resources with low embodied energy. Balsa wood serves as a key enabler in this transition, offering a biodegradable and recyclable solution for complex engineering challenges. The market is further supported by stringent safety regulations in the marine and aviation industries, where fire resistance and structural integrity are paramount. With the global push towards decarbonization, the demand for high-performance natural cores in Europe continues to evolve, positioning balsa wood as a strategic material for advanced manufacturing and sustainable infrastructure development.

MARKET DRIVERS

Expansion of Offshore Wind Energy Infrastructure

The rapid expansion of offshore wind energy infrastructure in Europe is majorly fuelling the European balsa wood market growth, as turbine manufacturers increasingly utilize bbalsa-coredcomposite blades to enhance performance and durability. Offshore wind turbines are significantly larger than their onshore counterparts, requiring blades that are both lightweight and rigid to optimize aerodynamic efficiency and reduce load on the tower structure. Balsa wood cores provide the necessary stiffness to prevent blade buckling under high wind loads while keeping the overall weight manageable for installation and maintenance. According to WindEurope, Europe added 3.8 gigawatts of new offshore wind capacity in 2025, with projections indicating a substantial increase to meet the EU’s 2030 renewable energy targets. The harsh marine environment demands materials that can resist moisture ingress and fatigue, properties that engineered balsa panels offer when properly sealed and integrated into fiberglass or carbon fiber laminates. Major turbine manufacturers such as Vestas and Siemens Gamesa have incorporated balsa cores into their latest blade designs to improve energy yield and extend service life. As per industry technical assessments, balsa-cored blades demonstrate superior impact resistance compared to ffoam-coredalternatives, reducing the risk of damage during transport and operation. The European Union’s REPowerEU plan aims to accelerate wind energy deployment to reduce dependence on fossil fuels, creating a sustained demand pipeline for balsa wood.

Growing Demand for Lightweight Solutions in Marine and Transportation Sectors

The growing demand for lightweight solutions in the marine and transportation sectors is further promoting the regional market expansion, as manufacturers seek to improve fuel efficiency and reduce emissions. In the marine industry, balsa wood is extensively used in the construction of luxury yachts, sailboats, and commercial vessels due to its ability to provide structural rigidity without adding significant weight. According to the International Council of Marine Industry Associations, the European recreational boating market continues to grow, with a strong trend towards larger and more complex vessel designs that require advanced composite materials. Balsa-cored hulls and decks offer superior sound insulation and thermal properties compared to solid fiberglass, enhancing comfort and performance. In the transportation sector, particularly in high-speed rail and automotive applications, weight reduction is critical for achieving energy efficiency goals. The European Automobile Manufacturers Association emphasizes the need to reduce vehicle weight to meet strict carbon dioxide emission standards. Balsa wood composites are being explored for interior panels and structural components in electric vehicles and trains, where every kilogram saved translates to extended range and lower energy consumption. As per engineering studies, balsa-based sandwich structures can reduce weight by up to 40% compared to traditional metal components while maintaining equivalent strength.

MARKET RESTRAINTS

Supply Chain Volatility and Geographic Concentration

Supply chain volatility and geographic concentration pose significant restraints to the Europe balsa wood market, as the majority of global balsa production is confined to specific tropical regions in South America, particularly Ecuador. This geographic dependency creates vulnerability to environmental disruptions, political instability, and logistical bottlenecks that can severely impact availability and pricing. According to market research reports, Ecuador accounts for approximately 75% of the world’s balsa supply, making the global market highly sensitive to local weather events such as El Niño, which can affect crop yields and quality. Recent climate variations have led to fluctuations in harvest volumes, causing intermittent shortages and price spikes for European importers. The long transportation distances from South America to Europe also contribute to higher logistics costs and carbon emissions, contradicting the sustainability goals of many end users. As per shipping industry reports, freight rates and port congestion have increased lead times, complicating inventory management for manufacturers who rely on just-in-time production models. The lack of diversified sourcing options limits the ability of European companies to mitigate these risks, forcing them to absorb cost increases or face production delays.

Competition from Synthetic Core Materials

Competition from synthetic core materials such as polyvinyl chloride foam, polyurethane, and honeycomb structures is further hampering the European balsa wood market expansion, as these alternatives often offer lower costs and easier processing characteristics. Synthetic foams are manufactured through industrial processes that allow for consistent quality, uniform density, and mass production at scales that natural balsa cannot match. According to material science comparisons, PVC foam is widely used in marine and wind energy applications due to its water resistance and ease of thermoforming into complex shapes without the grain direction limitations inherent in wood. While balsa offers superior mechanical properties, the higher initial cost and variability in natural grain structure can deter cost-sensitive projects. The European chemical industry has invested heavily in developing recycled and bbio-basedsynthetic foams that mimic the performance of balsa while offering better supply chain security. As per industry surveys, many composite manufacturers prefer synthetic cores for standard applications because they eliminate the need for extensive quality control checks associated with natural materials. The availability of automated cutting and shaping machinery designed specifically for foams further reduces labor costs and production time.

MARKET OPPORTUNITIES

Development of Hybrid Composite Structures

The development of hybrid composite structures presents a significant opportunity for the Europe balsa wood market, as engineers increasingly combine balsa with other natural fibers and resins to create advanced materials with enhanced properties. By integrating balsa cores with flax, hemp, or recycled carbon fiber skins, manufacturers can produce fully bio-based or partially bio-based sandwich panels that meet high performance standards while maximizing sustainability. According to research from the European Composite Industry Association, the demand for bio composites is growing by 10% annually, driven by regulatory pressures and consumer preference for green products. Hybrid structures allow for the optimization of mechanical performance, where balsa provides compressive strength and stiffness, while natural fibers offer tensile strength and impact resistance. This synergy enables the creation of lightweight components for automotive interiors, furniture, and modular construction elements that align with circular economy principles. As per innovation reports, several European startups are pioneering the use of balsa in combination with bio-based epoxy resins, reducing the overall carbon footprint of composite parts. The automotive sector, in particular, is exploring these hybrids for non-structural panels to meet weight reduction targets without compromising on aesthetics or durability.

Integration into Sustainable Building and Modular Construction

The integration of balsa wood into sustainable building and modular construction offers a promising opportunity for market expansion in Europe, as the construction sector seeks to reduce its environmental impact through the use of renewable materials. Balsa wood’s excellent thermal insulation properties and lightweight nature make it suitable for prefabricated wall panels, flooring systems, and roofing structures in energy-efficient buildings. According to Eurostat, the building industry is a significant contributor to total energy consumption and greenhouse gas emissions in the EU, prompting a shift towards low-carbon materials. Balsa-cored panels can significantly improve the thermal performance of building envelopes, reducing heating and cooling demands. The modular construction market is growing rapidly, with a focus on off-site manufacturing to minimize waste and construction time. Balsa wood’s ease of machining and bonding allows for precise fabrication of complex geometric shapes required in modern architectural designs. As per sustainability certifications such as LEED and BREEAM, the use of rapidly renewable materials like balsa contributes to higher rating scores, incentivizing developers to specify these products. Furthermore, the aesthetic appeal of natural wood finishes aligns with biophilic design trends that prioritize human connection to nature.

MARKET CHALLENGES

Quality Variability and Standardization Issues

Quality variability and standardization issues present a major challenge for the Europe balsa wood market, as the natural origin of the material leads to inconsistencies in density, grain structure, and moisture content that can affect performance. Unlike synthetic materials that are produced with tight tolerances, balsa wood exhibits natural variations that require rigorous sorting and grading to ensure suitability for high-precision applications. According to industry standards, balsa must be classified into specific density ranges to match engineering requirements, but achieving consistent batches is difficult due to differences in tree age, growth conditions, and processing methods. This variability necessitates extensive quality control measures, including non-destructive testing and manual inspection, which increase production costs and lead times. As per manufacturing feedback, inconsistent bond lines between balsa blocks and veneers can lead to delamination or structural failures in composite parts, posing safety risks in critical applications like wind turbine blades. The lack of universally accepted international standards for balsa grading further complicates procurement, as different suppliers may use varying criteria. European manufacturers often face challenges in validating material properties for certification purposes, requiring additional testing and documentation.

Environmental and Sustainability Certification Compliance

Navigating complex environmental and sustainability certification compliance poses a significant challenge for the Europe balsa wood market, as buyers increasingly demand proof of responsible sourcing and ethical labor practices. Ensuring that balsa wood is harvested from sustainably managed forests requires adherence to strict certification schemes such as the Forest Stewardship Council or Programme for the Endorsement of Forest Certification. According to the European Union Deforestation Regulation, importers must prove their products are not linked to forest degradation to be placed on the EU market. This regulation requires extensive due diligence and traceability documentation throughout the supply chain, from plantation to final product. Many smallholder farmers in producing countries lack the resources to obtain certification, limiting the pool of compliant suppliers for European companies. As per supply chain audits, verifying the origin of balsa wood is challenging due to fragmented ownership and informal trading practices in source regions. Failure to provide adequate proof of sustainability can result in reputational damage, legal penalties, and loss of market access. Additionally, the carbon footprint associated with long-distance transportation from South America to Europe is scrutinized by environmentally conscious consumers and regulators.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Form, Application, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, Germany, France, Italy, Spain, Netherlands, Belgium, Sweden, Rest of Europe |

| Market Leaders Profiled | 3A Composites GmbH, Schweiter Technologies AG, CoreLite Inc., DIAB Group (Ratos AB), The Gill Corporation, SINOKIKO BALSA TRADING CO., LTD., Carbon-Core Corporation, Bcomp Ltd., Core Composites Ltd., Sicomin Epoxy Systems, Pontus Wood Group, Lianyungang Qiaoyun Balsa Co., Ltd. |

SEGMENTAL ANALYSIS

By Form Insights

The end grain segment captured a dominant share of the European market in 2025 due to its exceptional compressive strength and stiffness, which are critical for high-performance structural applications. In end grain configuration, the wood cells are oriented perpendicular to the face of the panel, allowing the material to withstand significant vertical loads without crushing. This orientation makes it the preferred choice for wind turbine blades and marine hulls where structural integrity under dynamic stress is paramount. For instance, end-grain balsa exhibits compressive strength values up to 10 times higher than edge-grain configurations, making it indispensable for core materials in large-scale structures. The European wind energy sector, which added 3.8 gigawatts of new offshore capacity in 2025 as reported by WindEurope, relies heavily on end grain balsa for blade roots and spar caps where load concentrations are highest. The material’s ability to maintain dimensional stability under thermal and mechanical stress ensures long-term durability in harsh environments. As per technical specifications from leading turbine OEMs, end-grain balsa cores reduce the risk of delamination and fatigue failure, extending the operational life of renewable energy assets.

On the other side, the edge grain segment is projected to register the highest CAGR of 8.2% over the forecast period in the European market owing to its cost-effectiveness and versatility in non-structural and semi-structural applications. In edge-grain configuration, the wood cells are oriented parallel to the face of the panel, resulting in lower compressive strength but greater flexibility and ease of forming into curved shapes. This makes it ideal for applications such as marine decking, interior automotive panels, and architectural cladding where extreme load-bearing is not required. For instance, the demand for lightweight aesthetic materials in the luxury yacht and automotive sectors is increasing, with the European boating industry continuing to see strong revenue streams. Edge-grain balsa offers a natural wood finish that appeals to high-end consumers while providing thermal and acoustic insulation benefits. For instance, automotive manufacturers are exploring edge-grain balsa for interior trim components to reduce vehicle weight and enhance sustainability credentials. The lower cost of edge-grain balsa compared to end-grain makes it accessible for broader applications, expanding the total addressable market. Its ability to be easily machined and bonded to various substrates further enhances its appeal for custom fabrication projects.

By Application Insights

The renewable energy segment accounted for the leading share of the European market in 2025 due to the critical role balsa plays in the manufacturing of wind turbine blades. Balsa wood is used as a core material in sandwich composites to provide stiffness and prevent buckling in large blades, which can exceed 100 meters in length. According to WindEurope, the European Union reached a total installed wind capacity of 272 gigawatts by the end of 2025, with a significant portion coming from offshore projects that require robust and lightweight blade structures. The unique strength-to-weight ratio of balsa wood allows for the construction of larger blades that capture more energy without imposing excessive loads on the turbine tower. As per technical assessments by major turbine manufacturers, bbalsa-coredblades demonstrate superior fatigue resistance and impact tolerance compared to ffoam-coredalternatives, ensuring longer service life in harsh marine environments. The European Green Deal’s target of achieving climate neutrality by 2050 drives continuous investment in wind energy infrastructure, sustaining high demand for balsa wood. The shift towards larger offshore turbines further increases the volume of balsa required per unit, reinforcing the segment’s dominance.

On the other hand, the marine segment is projected to register the highest CAGR of 9.5% over the forecast period in the European market owing to the resurgence in luxury yacht and recreational boating activities. Balsa wood is extensively used in the construction of high-performance sailboats and motor yachts due to its ability to provide structural rigidity while minimizing weight. According to the International Council of Marine Industry Associations, the European boating market is showing sustained strength, with a strong trend towards larger and more sophisticated vessels. Balsa-cored hulls and decks offer superior strength and stiffness compared to solid fiberglass, allowing for thinner laminates and improved hydrodynamic performance. As per market surveys, affluent consumers are increasingly prioritizing sustainability and natural materials in their purchasing decisions, favoring balsa over synthetic foams. The aesthetic appeal of balsa wood, particularly when used in visible interior components, adds value to luxury vessels. The growth of charter tourism and marine leisure activities in Mediterranean countries further boosts demand for new boat construction and refurbishment. This renewed interest in high-end marine craftsmanship drives the rapid adoption of balsa wood in the sector.

COUNTRY LEVEL ANALYSIS

Germany Balsa Wood Analysis

Germany dominated the market in 2025 and is expected to maintain steady growth in its demand for balsa wood over the next few years as it continues to expand its offshore wind capacity and high-end manufacturing. Germany holds a prominent position in the Europe balsa wood market, driven by its advanced manufacturing sector and strong commitment to renewable energy. The country is a global leader in wind turbine technology, with major manufacturers such as Siemens Gamesa headquartered there. According to the German Wind Energy Association, Germany installed significant offshore wind capacity in recent years, creating substantial demand for balsa-cored blades. The automotive industry, another key consumer of lightweight materials, is exploring balsa composites for electric vehicle components to extend range. As per federal economic strategies, Germany’s industrial policy prioritizes sustainable materials, supporting the adoption of bio-based cores. The presence of specialized composite processing facilities and research institutions fosters innovation in balsa applications. High engineering standards and strict quality control requirements ensure that only premium-grade balsa is used in critical applications.

France Balsa Wood Analysis

France is poised to see increased balsa wood adoption as it aligns its aerospace and marine sectors with more stringent sustainable manufacturing standards in the coming years. France occupies a significant share of the Europe balsa wood market, characterized by its robust aerospace and marine industries. The country is home to major aerospace manufacturers that utilize balsa wood in satellite structures and aircraft interiors for weight reduction. According to the French Aerospace Industry Association, the sector is increasingly adopting sustainable materials to meet environmental targets. The luxury yacht building industry in regions like Brittany and the Mediterranean also drives demand for high-quality balsa cores. As per national ministerial policies, France supports the development of green technologies, including renewable energy and sustainable transport. The integration of balsa wood in high-speed train components further expands its application base. Strong regulatory frameworks for environmental protection encourage the substitution of synthetic foams with natural alternatives.

Italy Balsa Wood Analysis

Italy is likely to strengthen its status as a top consumer of balsa wood for luxury marine applications throughout the next few years. Italy is a key player in the Europe balsa wood market, primarily driven by its prestigious luxury yacht and super yacht manufacturing sector. The country accounts for a large portion of global super yacht production, with shipyards in regions like Tuscany and Liguria relying on balsa wood for hull and deck construction. According to industry reports, the Italian nautical industry generates billions of euros in export revenue, with a strong emphasis on craftsmanship and quality. Balsa wood is valued for its aesthetic appeal and structural performance in high-end vessels. The automotive sector, particularly luxury sports car manufacturers, also utilizes balsa composites for lightweight body panels. As per recent market data, the demand for sustainable luxury goods is rising, favoring natural materials like balsa. The presence of skilled artisans and advanced composite workshops supports the efficient use of balsa wood.

United Kingdom Balsa Wood Analysis

The United Kingdom is projected to maintain a high reliance on balsa wood as it accelerates its offshore wind targets and invests in sustainable infrastructure over the next few years. The United Kingdom maintains a steady presence in the Europe balsa wood market, influenced by its ambitious offshore wind energy targets and strong marine heritage. The UK government has set aggressive goals for offshore wind capacity, driving investment in large-scale turbine projects that require balsa-cored blades. According to the Department for Energy Security and Net Zero, the UK is a global leader in offshore wind installation, creating consistent demand for core materials. The recreational boating sector, particularly in coastal regions, also contributes to balsa consumption for yacht repairs and new builds. As per national data, the UK’s focus on net zero emissions supports the adoption of sustainable materials in construction and transport. The presence of research centers specializing in composite materials fosters innovation in balsa applications.

Spain Balsa Wood Analysis

Spain is expected to see a significant boost in balsa wood consumption as its renewable energy and marine tourism sectors continue to scale up in the coming years. Spain is an important market in the Europe balsa wood sector, driven by its growing renewable energy sector and vibrant marine tourism industry. The country has invested heavily in wind power, both onshore and offshore, creating demand for balsa-cored turbine components. According to the Spanish Wind Energy Association, Spain is one of the leading wind energy producers in Europe, with continuous expansion plans. The yacht building and repair industry in regions like the Balearic Islands and the Costa del Sol also drives demand for balsa wood. As per ministerial ecological transition reports, Spain is committed to increasing its renewable energy share, supporting long-term market growth. The tourism sector’s reliance on marine leisure activities sustains demand for new and refurbished vessels. The combination of energy infrastructure development and marine tourism makes Spain a dynamic market for balsa wood suppliers.

COMPETITIVE LANDSCAPE

The competition in the Europe balsa wood market is characterized by a mix of specialized core material manufacturers and diversified composite solution providers. Leading players compete on product quality, technical expertise, and supply chain reliability rather than price alone due to the critical nature of balsain in high-performance applications. The market is moderately consolidated with a few key players dominating the supply to major wind turbine and marine manufacturers. Competition is intense in terms of innovation, with companies striving to develop lighter, stronger, a nd more sustainable core solutions. Entry barriers are high due to the need for established relationships with raw material suppliers and stringent certification requirements from end users. Regional players often differentiate themselves through specialized services and faster response times for niche applications. The shift towards sustainability drives competition in eco-friendly processing and certified sourcing practices. Collaborative partnerships between suppliers and OEMs are common, fostering long-term loyalty and reducing switching costs. This dynamic landscape encourages continuous improvement and adaptation to changing regulatory and market demands.

KEY MARKET PLAYERS

Some of the companies that are playing a dominant role in the Europe Balsa Wood Market include

- 3A Composites GmbH

- Schweiter Technologies AG

- CoreLite Inc.

- DIAB Group (Ratos AB)

- The Gill Corporation

- SINOKIKO BALSA TRADING CO., LTD.

- Carbon-Core Corporation

- Bcomp Ltd.

- Core Composites Ltd.

- Sicomin Epoxy Systems

- Pontus Wood Group

- Lianyungang Qiaoyun Balsa Co., Ltd.

TOP LEADING PLAYERS IN THE MARKET

- 3A Composites Core Materials AG is a leading supplier of high-performance core materials, including balsa wood for the European composite industry. The company provides specialized end grain and edge grain balsa products tailored for wind energy, marine,ine and transportation applications. Recent actions include the expansion of its production capabilities in Europe to ensure reliable supply chains for major turbine manufacturers. The company focuses on sustainable sourcing practices and has implemented advanced quality control systems to meet stringent industry standards. By investing in research and development, 3A Composites enhances the mechanical properties of its base cores, ensuring superior performance in demanding environments. Their strategic partnerships with key OEMs strengthen their position as a preferred supplier for critical infrastructure projects across the continent.

- Diab Group is a global provider of composite components and core materials with a strong presence in the European balsa wood market. The company offers a wide ranbalsa-based based sandwich solutions that cater to the wind energy, marine,e and industrial sectors. Diab has recently invested in upgrading its manufacturing facilities to improve efficiency and reduce environmental impact. The company emphasizes innovation by developing hybrid core structures that combine balsa with other sustainable materials. Through continuous improvement in processing technologies, es Diab ensures consistent quality and performance for its customers. Their commitment to sustainability and customer collaboration drives their growth and reinforces their reputation as a trusted partner in the European composite market.

- Gurit Holding AG is a prominent player in the Europe balsa wood market, ket specializing in advanced composite materials and structural cores. The company supplies high-quality balsa wood products for wind turbine blades, aerospace components, and marine vessels. Gurit has strengthened its market position by expanding its service network and technical support capabilities across Europe. Recent initiatives include the development of customized balsa solutions that optimize weight and stiffness for specific client requirements. The company focuses on operational excellence and sustainable manufacturing practices to meet evolving regulatory demands. By leveraging its technical expertise and global reach, ch Gurit continues to deliver value to customers and maintain a competitive edge in the dynamic European market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe balsa wood market primarily employ vertical integration and sustainable sourcing strategies to secure raw material supply and ensure product quality. Companies invest in long-term partnerships with plantation owners in South America to guarantee consistent availability of high-grade balsam logs. Product innovation is another major strategy, with firms developing hybrid cores and improved processing techniques to enhance mechanical performance and ease of manufacturing. Expansion of local processing facilities in Europe helps reduce lead times and logistics costs while meeting regional content requirements. Strategic collaborations with original equipment manufacturers allow suppliers to co-develop customized solutions for specific applications such as offshore wind turbines. Emphasis on certification and compliance with environmental regulations strengthens brand reputation and access to green markets. Digitalization of supply chain management improves transparency and traceability, addressing sustainability concerns. These strategies collectively help companies mitigate risks and capitalize on growing demand for lightweight sustainable materials.

MARKET SEGMENTATION

This research report on the europe balsa wood market is segmented and sub-segmented into the following categories.

By Form

- End Grain

- Edge Grain

By Application

- Renewable Energy

- Marine

By Country

- Germany

- France

- Italy

- United Kingdom

- Spain

- Rest of Europe

Frequently Asked Questions

1. Which grade leads the market?

Grade A balsa is the largest and fastest‑growing segment, favored for high‑performance applications that require consistent density and strength.

2. Which industries are most important?

Key end‑use industries include wind energy, aerospace, marine, and specialty applications such as model aircraft and crafts.

3. Which countries are key markets?

Germany and the UK are the largest European markets, with significant activity also in France, Spain, and other Western European countries involved in wind and aerospace manufacturing.

4. Where does Europe source its balsa?

Most balsa is imported from tropical growing regions (mainly Latin America), then processed and distributed to European composite and OEM manufacturers

5. What is the market outlook?

The outlook is positive, with continued demand expected from wind‑energy and aerospace sectors, supported by balsa’s sustainability profile and performance in high‑value composite applications.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com