Europe Beauty Drinks Market Research Report Segmented By Ingredient Type (Vitamins & Minerals, Protein & Peptides, Antioxidants, Co-Enzymes And Others), Function (Anti-Aging, Detoxication, Radiance, Vitality And Others), Distribution Channel (Supermarket & Hypermarket, Specialty Stores, Online), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Europe Beauty Drinks Market Size

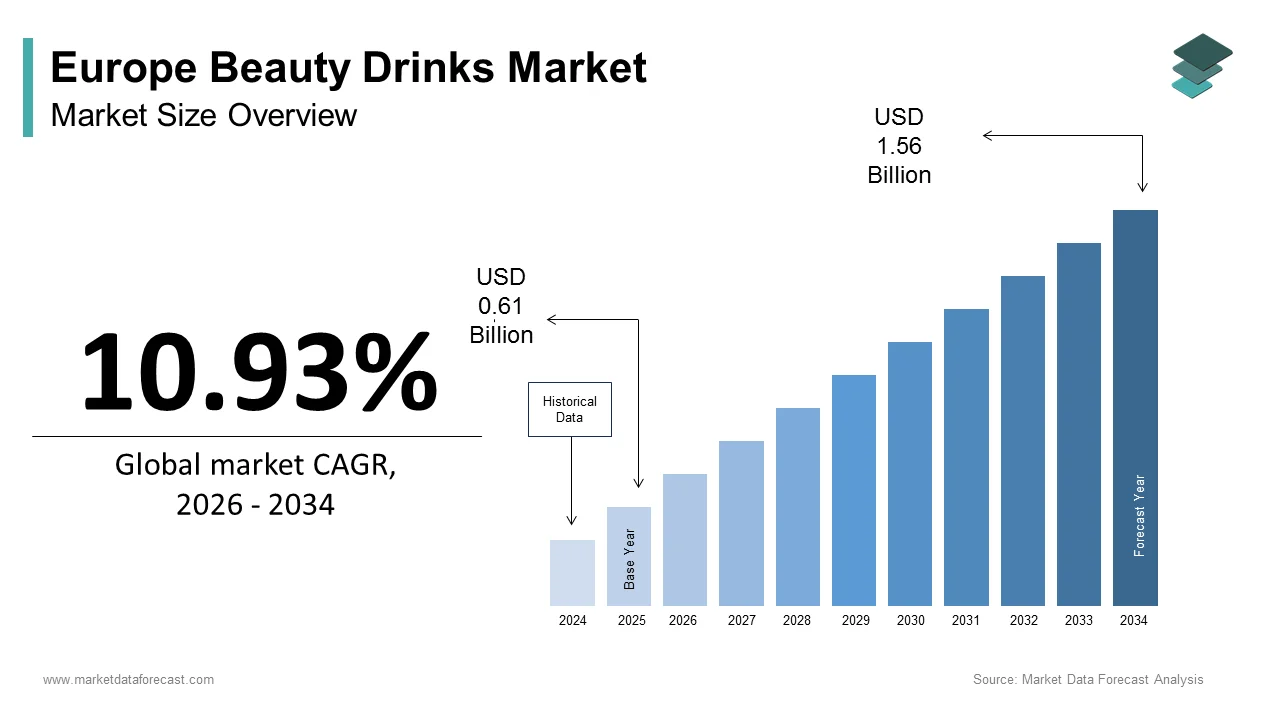

The size of the Europe Beauty Drinks Market was expected to be worth USD 0.61 billion in 2025 and is anticipated to be worth USD 1.56 billion by 2034, from USD 0.68 billion in 2026, growing at a CAGR of 10.93% during the forecast period.

Beauty drinks represent a dynamic intersection of the nutraceutical and beverage industries, focusing on liquid formulations designed to enhance skin health, hair vitality, and nail strength from within. These functional beverages typically contain bioactive ingredients such as hydrolyzed collagen, hyaluronic acid, antioxidants, and specific vitamins that target signs of aging and environmental damage. The cultural shift toward holistic wellness and preventive care has transformed these products from niche supplements into mainstream daily rituals for consumers across the continent. According to Eurostat, the population of the European Union continues to age, reflecting a demographic increasingly concerned with maintaining a youthful appearance and physical vitality. As per the European Food Safety Authority, health claims related to skin protection and hydration are carefully evaluated to ensure that only scientifically substantiated products reach the shelves. National health surveys in countries such as France and Germany highlight a rising prevalence of skin conditions linked to urban pollution and stress, which drives demand for internal solutions rather than topical treatments alone. The convenience factor of ready-to-drink formats appeals to busy urban professionals who seek efficient ways to integrate wellness into their routines without compromising on efficacy. This market thrives on the convergence of scientific innovation and consumer desire for natural, effective, and accessible beauty solutions.

MARKET DRIVERS

Rising Consumer Awareness of Internal Beauty Solutions

The escalating consumer understanding that true radiance originates from internal health serves as a primary catalyst for the expansion of the beauty drinks sector across Europe. Shoppers are increasingly skeptical of topical products that only address surface-level concerns and are turning to ingestible solutions that promise systemic benefits for skin elasticity and hydration. According to the European Consumer Organisation, many consumers in Western Europe actively seek products with proven health benefits beyond basic nutrition, indicating a shift in purchasing behavior. This educational wave is fueled by widespread access to dermatological advice via digital platforms and social media, where influencers and experts emphasize the importance of collagen supplementation and antioxidant intake. The concept of beauty from within has gained traction among millennials and Gen Z demographics who view prevention as superior to correction, leading to earlier adoption of these beverages. As per European scientific journals, oral collagen peptides have been validated for their efficacy in improving skin moisture and reducing wrinkle depth, which further legitimizes the category. Retailers respond by dedicating prominent shelf space to these functional drinks and providing detailed information about ingredient sourcing and clinical results. As the stigma around consuming supplements for aesthetic purposes diminishes, the market expands to include a broader audience seeking holistic self-care routines.

Impact of Urban Pollution and Stress on Skin Health

The deteriorating quality of urban environments and the high stress levels associated with modern European lifestyles create a compelling demand for protective and restorative beauty drinks, which is further boosting the expansion of the European beauty drinks market. Exposure to particulate matter, heavy metals, and ozone in major cities like London, Paris, and Berlin accelerates skin aging and compromises the skin barrier function, necessitating robust internal defense mechanisms. According to the European Environment Agency, air pollution remains a critical health risk in Europe, with citizens exposed to levels exceeding World Health Organization guidelines, which correlates with increased skin sensitivity and inflammation. Chronic stress triggers the release of cortisol, which breaks down collagen and elastin, leading to premature wrinkles and dullness that consumers strive to counteract. Beauty drinks formulated with high levels of antioxidants such as vitamin C, E, and polyphenols offer a convenient way to neutralize free radicals generated by environmental aggressors. The busy pace of life leaves little time for elaborate skincare routines, making ingestible solutions an attractive alternative for maintaining skin health efficiently. Dermatologists increasingly recommend oral supplements as part of a comprehensive strategy to protect against urban damage, reinforcing consumer confidence in these products.

MARKET RESTRAINTS

Stringent Regulatory Frameworks on Health Claims

The rigorous regulatory environment governing health claims in the European Union acts as a significant restraint on the marketing and product development strategies of beauty drink manufacturers. The European Food Safety Authority maintains a strict list of approved health claims and rejects many submissions related to beauty benefits due to insufficient scientific evidence or vague definitions of efficacy. According to the European Commission, only a limited number of specific claims regarding skin protection and hydration have been authorized, which restricts the ability of brands to communicate the full potential of their ingredients to consumers. Companies must invest substantial resources in clinical trials to substantiate their claims, a process that is both time-consuming and expensive, particularly for small and medium-sized enterprises. The prohibition of using terms like anti-aging or rejuvenating without specific approval forces marketers to rely on ambiguous language that may fail to resonate with target audiences. The fragmentation of regulations across different member states regarding novel foods and ingredient approvals further complicates market entry and expansion.

High Cost of Premium Ingredients and Final Products

The elevated cost associated with high-quality bioactive ingredients and the resulting premium pricing of beauty drinks present a formidable barrier to mass market adoption across Europe. Sourcing pharmaceutical-grade collagen, pure hyaluronic acid, and potent botanical extracts involves complex supply chains and rigorous quality control measures that drive up production expenses. According to the European Federation of Cosmetic Ingredients, the prices of key raw materials have fluctuated in recent years due to supply chain disruptions and increasing global demand, which impacts final retail prices. Many beauty drinks are positioned as luxury items with price points that exceed the budget of average consumers, particularly during periods of economic inflation and reduced disposable income. The perception of these products as non-essential indulgences makes them vulnerable to cutbacks when households prioritize spending on fundamental necessities. Smaller brands struggle to compete with established giants who can leverage economies of scale to offer lower prices while maintaining margins. The need for continuous consumption to achieve visible results means that the long-term financial commitment deters potential users who are unwilling to sustain high monthly expenditures.

MARKET OPPORTUNITIES

Expansion into Men's Grooming and Wellness Segments

The emerging interest in grooming and wellness among European men presents a transformative opportunity for the European beauty drinks market. Traditionally viewed as a female-centric category, the perception of male grooming is shifting rapidly as men become more conscious of their appearance and proactive about aging prevention. According to the European Market Research Association, the men's personal care market in Europe has grown steadily, with increasing adoption of supplements and functional beverages targeting skin health and hair loss. Brands that develop formulations specifically tailored to male physiological needs, such as thicker skin structure and different hormonal profiles, can capture significant market share in this nascent segment. Marketing campaigns that normalize the use of beauty drinks for men and highlight benefits like improved energy and stress reduction resonate well with modern male consumers. The rise of male influencers and celebrities endorsing ingestible beauty products further destigmatizes usage and drives acceptance across various age groups. Retailers are beginning to curate dedicated sections for men's wellness products, providing visibility and accessibility that were previously lacking.

Innovation in Plant-Based and Clean Label Formulations

The growing demand for plant-based and clean label products offers a lucrative avenue for innovation within the Europe beauty drinks market as consumers increasingly prioritize sustainability and transparency. Shoppers are scrutinizing ingredient lists for artificial additives, preservatives, and animal-derived components, driving the shift toward vegan collagen alternatives and organic botanical blends. According to the European Plant-Based Foods Association, sales of plant-based products have surged in recent years, reflecting a broader trend that extends into the beauty and wellness categories. Manufacturers are investing in biotechnology to produce bioidentical collagen from yeast or bacteria and extracting active compounds from sustainable sources like algae and fruits. These innovations allow brands to appeal to environmentally conscious consumers who refuse to compromise on ethics for efficacy. The clean label movement also emphasizes minimal processing and recognizable ingredients, which builds trust and loyalty among discerning buyers.

MARKET CHALLENGES

Scientific Skepticism Regarding Bioavailability and Efficacy

The persistent skepticism within the scientific community and among informed consumers regarding the bioavailability and actual efficacy of ingestible beauty ingredients poses a significant challenge to market credibility. Critics argue that many active compounds, such as collagen peptides, are broken down by digestive enzymes before they can reach the skin. According to the European Society for Dermatological Research, while some studies show positive results, there is a lack of large-scale, standardized clinical trials that definitively prove the superiority of oral supplements over placebos for specific beauty outcomes. This ambiguity fuels doubt among potential buyers who are reluctant to invest in products without guaranteed results. The variability in formulation quality and dosage across different brands further complicates the landscape, making it difficult for consumers to distinguish between effective and ineffective products. Negative media coverage highlighting unsubstantiated claims damages the reputation of the entire category and erodes consumer trust.

Intense Competition from Traditional Skincare and Supplements

The beauty drinks market in Europe faces fierce competition from established topical skincare lines and traditional pill-based supplements, which dominate the personal care landscape and enjoy higher consumer loyalty. Topical products offer immediate sensory feedback and visible results that liquids often cannot match in the short term. According to the European Cosmetic Toiletry and Perfumery Association, the skincare sector remains the largest segment of the beauty industry, supported by decades of brand equity and extensive distribution networks. Pill supplements are perceived as more concentrated and convenient by some users who dislike the taste or volume of liquid formulations. The shelf space in pharmacies and supermarkets is limited, forcing beauty drinks to compete directly with these entrenched categories for visibility and consumer attention. Marketing budgets of major skincare giants far exceed those of emerging beauty drink brands, allowing them to saturate media channels and influence consumer preferences effectively.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.93% |

| Segments Covered | By Ingredient Type, Function, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | The Coca-Cola Company, SIPA Spa, Asterism Healthcare Plus, Inc., Big Quark LLC, DyDo Drin Co., Inc.c, Beatific-Beauty lab, Hangzhou Nutrition, Nestlé SA, Vemma Nutrition, Juice Generation, AMC, Sappe Public Company Limited, and Zoppas Industries Group |

SEGMENTAL ANALYSIS

By Ingredient Type Insights

The vitamins and minerals segment dominated the market by commanding the highest share of the Europe beauty drinks market in 2025 due to the foundational role these micronutrients play in maintaining skin integrity and overall physiological function. This dominance is primarily driven by the widespread consumer recognition of vitamins such as C, E, and the B complex as essential elements for collagen synthesis and cellular protection. According to the European Food Safety Authority, health claims regarding the contribution of vitamin C to collagen formation and the protection of cells from oxidative damage are officially authorized, which boosts consumer confidence and regulatory compliance for manufacturers. The familiarity of these ingredients allows brands to market products with clear and understandable benefits, effectively reducing the educational barrier for new adopters. Furthermore, the inclusion of minerals like zinc and selenium addresses common dietary deficiencies in modern European lifestyles caused by processed food consumption, making these drinks an attractive supplementary solution. National health campaigns in countries such as Germany and France emphasize the importance of adequate micronutrient intake for preventing premature aging, reinforcing sustained demand for fortified beverages.

The protein and peptides segment is projected to be the fastest CAGR of 10.5% over the forecast period in the European beauty drinks market. The surging popularity of hydrolyzed collagen peptides, increasingly recognized for their ability to improve skin elasticity and reduce wrinkle depth when consumed orally, and the shifting consumer perception that ingestible collagen offers systemic benefits compared to topical applications, a view supported by emerging clinical research, are propelling the growth of the proteins and peptides segment in the European market. According to the International Society of Aesthetic Plastic Surgery, studies indicate that oral supplementation with specific collagen peptides can improve skin hydration and density within weeks of daily use, providing tangible evidence that drives repeat purchases. Manufacturers are innovating with marine and plant-based peptide sources to cater to vegan and sustainable demographics prevalent in Northern Europe. The ability of peptides to target multiple concerns, such as skin firmness and joint health, simultaneously adds significant value to the product proposition.

By Function Insights

The anti-aging segment led the market and held a major share of the European beauty drinks market in 2025. The growth of the anti-aging segment in the European market is attributed to the continent's aging demographic and cultural focus on maintaining a youthful appearance. This dominance stems from the high prevalence of age-related skin concerns such as loss of elasticity, fine lines, and pigmentation. According to Eurostat, the European Union population includes a substantial proportion of individuals aged 65 or older, creating a large consumer base actively seeking solutions to slow down visible signs of aging. Cultural norms in countries such as France and Italy place a high value on aesthetic preservation, encouraging lifelong adoption of beauty rituals, including ingestible supplements. Scientific advancements in understanding cellular aging have led to more effective formulations containing retinol alternatives and potent antioxidants that appeal to informed consumers.

The radiance segment is emerging as the fastest growing segment in the Europe beauty drinks market and is estimated to witness a CAGR of 11.6% over the forecast period, owing to the evolving desire for a healthy, glowing complexion rather than just wrinkle reduction. This acceleration is attributed to the influence of social media and digital culture, where luminous skin is celebrated as a sign of health and vitality among younger demographics. According to the Global Wellness Institute, the wellness economy in Europe has shifted toward holistic beauty solutions that address dullness caused by chronic stress and urban pollution. Urban dwellers in major cities such as London and Berlin are increasingly exposed to environmental aggressors that strip the skin of its natural radiance, creating demand for internal repair mechanisms. Brands are launching glow-specific formulations that promise hydration and brightness, appealing to those seeking quick yet visible results. The trend of minimal makeup routines further boosts demand for drinks that make bare skin look flawless and healthy.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held the leading share of the European beauty drinks market in 2025. The dominance of supermarkets and hypermarket segments in the European market can be credited to their extensive reach, high foot traffic, and the convenience they offer for routine grocery shopping. This dominance is driven by impulse buying behavior associated with these retail environments, where beauty drinks are often strategically placed near checkout counters or in health food aisles alongside other wellness products. According to Eurostat, supermarkets and hypermarkets remain the primary channel for food and beverage purchases for European households, ensuring visibility and accessibility for functional drinks. The ability of these large-format stores to stock a wide variety of brands and price points caters to diverse consumer segments ranging from budget-conscious shoppers to premium seekers. Promotional activities such as buy one get one free offers and loyalty program discounts frequently drive volume sales and encourage trial among new customers. The trust consumers place in established retail chains regarding product quality and safety reinforces their preference for purchasing beauty beverages from these outlets. Furthermore, the integration of private label ranges by major supermarket chains provides affordable alternatives that expand the consumer base. The physical presence of these stores allows for immediate product acquisition without waiting for delivery, which is crucial for consumers seeking instant gratification or urgent replenishment of their wellness routines.

The online distribution channel segment is witnessing the fastest growth in the Europe beauty drinks market and is predicted to grow at a CAGR of 13.2% over the forecast period, owing to the rapid digital transformation of retail and changing consumer habits. This surge is driven by the increasing preference for e-commerce platforms that offer product variety, detailed informational content, and the convenience of home delivery. According to the European E-commerce Report, online sales of health and beauty products have risen as consumers become more comfortable purchasing supplements and functional beverages via digital channels. The ability of online retailers to provide educational content, authentic customer reviews, and flexible subscription models fosters deeper engagement and loyalty among users. Direct-to-consumer brands leverage social media marketing and influencer partnerships to drive traffic to their websites, bypassing traditional retail barriers and reaching niche audiences. The pandemic accelerated the adoption of online shopping for wellness products, a trend that has persisted as consumers appreciate the time-saving aspects of digital procurement. Advanced logistics networks ensure rapid delivery even for temperature-sensitive items, removing previous hurdles for online beauty drink sales. The data analytics capabilities of online platforms allow brands to personalize offerings and recommendations, enhancing the shopping experience and driving repeat purchases.

REGIONAL ANALYSIS

Germany Beauty Drinks Market Analysis

Germany stood as the leading market for beauty drinks in Europe and commanded for 23.2% of the regional market share in 2025. The dominating position of Germany in the European market can be credited to its highly developed health and wellness culture. The country's position is reinforced by a strong tradition of naturopathy and a high level of consumer awareness regarding the benefits of nutritional supplements for skin health. According to the German Federal Ministry of Food and Agriculture, the nation records some of the highest expenditures on dietary supplements in Europe, reflecting a deep belief in preventive health measures. The robust pharmacy network in Germany serves as a trusted distribution channel where pharmacists actively recommend beauty drinks to customers seeking professional advice. German consumers are known for their rigorous scrutiny of ingredient lists and scientific backing, forcing manufacturers to maintain high standards of quality and transparency. The aging population creates sustained demand for anti-aging solutions while younger demographics drive growth in radiance and vitality segments. Major domestic players invest heavily in research and development to create innovative formulations that meet strict regulatory requirements. The strong economy ensures that consumers have the disposable income to invest in premium beauty beverages.

France Europe Beauty Drinks Market Analysis

France secured the second largest market share in the Europe beauty drinks market in 2025. The growth of France in the European market is driven by a sophisticated consumer base that blends skincare rituals with ingestible beauty solutions. According to the French Federation of Cosmetic Products, the country has a long history of embracing “beauty from within” concepts, with many cosmetic brands expanding portfolios to include functional beverages. The strong emphasis on natural and organic ingredients aligns with clean label trends dominating the category. French consumers prioritize efficacy and sensory experience, demanding products that taste good while delivering visible results. The dense network of perfumeries and pharmacies provides excellent visibility and accessibility for premium beauty drinks. Government support for the cosmetic industry fosters innovation and collaboration between food scientists and dermatologists. The cultural importance of maintaining an elegant appearance at any age drives consistent demand across demographics. Tourism also plays a role as visitors seek out French beauty secrets and take them back to their home countries.

United Kingdom Europe Beauty Drinks Market Analysis

The United Kingdom is expected to account for a prominent share of the European beauty drinks market during the forecast period. The vibrant digital landscape, early adoption of global wellness trends, and the rapid rise of direct-to-consumer brands that leverage social media and influencer marketing to reach young audiences are driving the UK beauty drinks market growth. According to the British Retail Consortium, online sales of health and beauty products have grown significantly, with beauty drinks being a key beneficiary. British consumers are receptive to new ingredients and functional claims, particularly those related to veganism and sustainability. The diverse multicultural population introduces a wide range of beauty needs and preferences, encouraging brands to innovate with inclusive formulations. The presence of major retail chains like Boots and Superdrug provides strong offline distribution, while independent health stores cater to niche markets. The post Brexit regulatory environment allows for potential flexibility in approving novel ingredients, fostering innovation. The strong fitness and wellness community in the UK drives demand for beauty drinks that also support vitality and recovery.

Italy Europe Beauty Drinks Market Analysis.

Italy represents a crucial market within the Europe beauty drinks market. The deep appreciation for natural beauty and healthy living, and the Mediterranean diet culture that emphasizes fresh ingredients and holistic health, is creating fertile ground for natural beauty drinks and propelling the Italian market growth. According to the Italian National Institute of Statistics, demand for organic and natural products has risen in recent years, benefiting beauty drink formulations based on fruits, vegetables, and herbal extracts. Italian consumers value authenticity and heritage, preferring brands that highlight traditional ingredients with modern scientific validation. The strong pharmaceutical sector supports distribution through pharmacies where trust in product efficacy is high. The aging population drives demand for anti-aging solutions while fashion-conscious youth seek radiance and glow-enhancing products. Regional differences in tastes and preferences require brands to tailor offerings to local palates. The tourism industry exposes the market to international trends while promoting Italian beauty secrets globally.

Spain Europe Beauty Drinks Market Analysis.

Spain is anticipated to record a healthy CAGR in the European beauty drinks market during the forecast period, owing to a growing focus on self-care and wellness integration into daily lifestyles. The Spanish market reflects a transition from occasional supplement use to regular consumption of functional beverages as part of a holistic health regimen. According to the Spanish Agency for Food Safety and Nutrition, awareness of the link between nutrition and skin health is rising, particularly among urban populations exposed to sun and pollution. The warm climate and outdoor lifestyle create specific skin concerns such as sun damage and dehydration, which beauty drinks aim to address with hydrating and protective ingredients. The expansion of modern retail formats and the increasing penetration of e-commerce facilitate easier access to a wider range of products. Spanish consumers are becoming more open to trying new formats and flavors, encouraging innovation with refreshing formulations. The influence of Latin American beauty trends also shapes consumer preferences and product development. Government initiatives promoting healthy eating and active living support the wellness ecosystem. As the Spanish economy continues to recover and disposable incomes rise, the adoption of premium beauty drinks is expected to accelerate.

COMPETITION OVERVIEW

The competition in the Europe beauty drinks market is intense and characterized by a mix of global beverage giants, specialized nutraceutical companies, and emerging direct-to-consumer brands. Major corporations leverage their extensive distribution networks and marketing budgets to dominate shelf space and consumer attention. Smaller niche players differentiate themselves through unique ingredient profiles, organic certifications, and targeted messaging that resonates with specific demographic groups. The landscape is rapidly evolving as companies race to innovate with new functional ingredients like marine collagen and adaptogens to meet shifting consumer preferences. Price competition remains fierce, particularly in the mass market segment where private label offerings from retailers gain traction. Regulatory compliance regarding health claims serves as a key battleground where providers compete to validate their efficacy scientifically. Strategic partnerships between ingredient suppliers and beverage manufacturers are becoming essential to secure high-quality raw materials and drive cost efficiencies. This dynamic environment fosters continuous product development and marketing creativity as firms strive to establish loyalty in a category driven by trends and perceived results.

Top Strategies Used by Key Market Participants

Key players in the Europe beauty drinks market primarily focus on product innovation to develop formulations with clinically proven benefits and clean labels. Companies frequently pursue strategic acquisitions of niche brands to gain access to proprietary ingredients and specialized technologies. Investment in sustainable sourcing and eco-friendly packaging helps firms meet growing consumer demand for environmental responsibility. Expanding distribution networks through online platforms and specialty stores ensures greater product accessibility and visibility. Collaborations with influencers and dermatologists drive brand awareness and credibility among target demographics. Firms also prioritize scientific research to substantiate health claims and comply with strict regulatory standards. These strategies collectively enable market participants to differentiate their offerings and capture growth opportunities in a competitive landscape.

KEY MARKET PLAYERS

A few major players of the Europe beauty drinks market include

- The Coca-Cola Company

- SIPA Spa

- Asterism Healthcare Plus, Inc

- Big Quark LLC

- DyDo Drin Co., Inc.c

- Beatific-Beauty lab

- Hangzhou Nutrition

- Nestlé SA

- Vemma Nutrition

- Juice Generation

- AMC

- Sappe Public Company Limited

- Zoppas Industries Group

Leading Players in the Market

- The Coca-Cola Company stands as a dominant force in the Europe beauty drinks market by leveraging its massive distribution network to introduce functional beverages with beauty benefits. The company contributes significantly to the global market through brands like AdeS and various vitamin-enriched waters that target skin health and hydration. Recent actions include the expansion of its portfolio to include drinks fortified with collagen and antioxidants specifically designed for European consumers seeking internal beauty solutions. The firm actively invests in research to develop clean-label formulations that align with strict regional regulations and consumer preferences for natural ingredients. Strategic partnerships with local suppliers ensure sustainable sourcing of key components while maintaining high-quality standards. By utilizing its unparalleled logistics capabilities, The Coca-Cola Company ensures widespread availability of these niche products across diverse retail channels. This approach solidifies its position as a key player capable of scaling innovative beauty concepts from niche trends to mainstream consumption throughout the continent and beyond.

- Danone S.A. plays a pivotal role in the Europe beauty drinks market through its specialized nutrition division, which focuses on health and wellness-oriented beverages. The company leverages its expertise in fermentation and plant-based sciences to create products that support skin vitality and overall well-being. Recent initiatives involve the launch of new probiotic and prebiotic drink lines that claim to improve skin clarity and reduce inflammation from within. Danone has strengthened its market position by acquiring innovative startups focused on functional ingredients and sustainable packaging solutions. The firm prioritizes transparency and scientific validation to build trust with health-conscious European consumers who demand evidence-based benefits. Collaborations with dermatologists and nutritionists help refine product formulations to meet specific regional needs. By integrating beauty benefits into its core medical nutrition and early life nutrition portfolios, Danone creates a holistic approach to wellness. These strategic moves enhance its reputation as a leader in science-backed functional beverages that bridge the gap between food, medicine, and beauty.

- Nestlé S.A. maintains a significant presence in the Europe beauty drinks market by offering a diverse range of nutritional beverages under its health science and confectionery divisions. The company contributes to the global market by developing advanced delivery systems for bioactive compounds like collagen peptides and vitamins. Recent actions include the reformulation of existing product lines to include higher concentrations of beauty-enhancing ingredients while reducing sugar content. Nestlé has invested heavily in biotechnology to produce sustainable and effective protein sources for its beauty drink portfolio. The firm actively engages in consumer education campaigns to highlight the benefits of ingestible beauty solutions compared to topical treatments. Strategic alliances with research institutions drive innovation in taste masking and nutrient stability. By leveraging its strong brand equity and extensive retail relationships, Nestlé ensures its beauty drinks reach a broad audience across supermarkets and pharmacies. This commitment to innovation and quality reinforces its status as a major contributor to the evolving landscape of functional beauty beverages worldwide.

MARKET SEGMENTATION

This research report on the Europe beauty drinks market has been segmented and sub-segmented based on ingredient type, function, distribution channel & region.

By Ingredient Type

- Antioxidants

- Collagen

- Vitamins

- Bioactive Ingredients

- Minerals

By Function

- Detox

- Anti-Aging

- Vitality

- Radiance

By Distribution Channel

- Non-Store-Based

- Online Retailing

- Store-Based

- Supermarkets

- Specialty Stores

- Hypermarkets

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the Europe Beauty Drinks Market?

Growing awareness about skin health, rising disposable income, clean-label trends, and increasing preference for preventive healthcare are major drivers.

2. What are the key ingredients used in beauty drinks?

Common ingredients include collagen peptides, biotin, hyaluronic acid, vitamin C, vitamin E, zinc, and plant-based extracts.

3. What are the major product types in the market?

The market includes collagen drinks, vitamin-infused beverages, antioxidant drinks, herbal beauty beverages, and protein-based beauty drinks.

4. Which distribution channels are prominent in Europe?

Supermarkets and hypermarkets, specialty health stores, pharmacies, and online retail channels dominate distribution.

5. Which countries lead the Europe Beauty Drinks Market?

Germany, the UK, France, Italy, and Spain are among the key markets due to high consumer awareness and developed retail infrastructure.

6. Who are the key market players in the Europe Beauty Drinks Market?

Major companies include Nestlé S.A., Shiseido Company Limited, Kinohimitsu, Amway Corporation, and Herbalife Nutrition Ltd.

7. What are the major challenges in the market?

High product pricing, regulatory scrutiny on health claims, and intense competition from dietary supplements are key challenges.

8. What role does e-commerce play in market growth?

Online platforms significantly contribute to sales growth by offering product variety, subscription models, and influencer-driven marketing.

9. What opportunities exist in the Europe Beauty Drinks Market?

Product innovation, personalized nutrition, vegan collagen alternatives, and expansion into Eastern Europe present strong growth opportunities.

10. How is the competitive landscape evolving?

The market is becoming highly competitive with new product launches, collaborations, influencer marketing, and premium positioning strategies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com