Global Beauty Drinks Market Size, Share, Trends, & Growth Forecast Report Segmented By Ingredient Type (Vitamins & Minerals, Protein & Peptides, Antioxidants, Co-Enzymes And Others), Function (Anti-Aging, Detoxication, Radiance, Vitality And Others), Distribution Channel (Supermarket & Hypermarket, Specialty Stores, Online), And Region (North America, Europe, APAC, Latin America, Middle East And Africa) – Industry Analysis From 2026 To 2034

Global Beauty Drinks Market Size

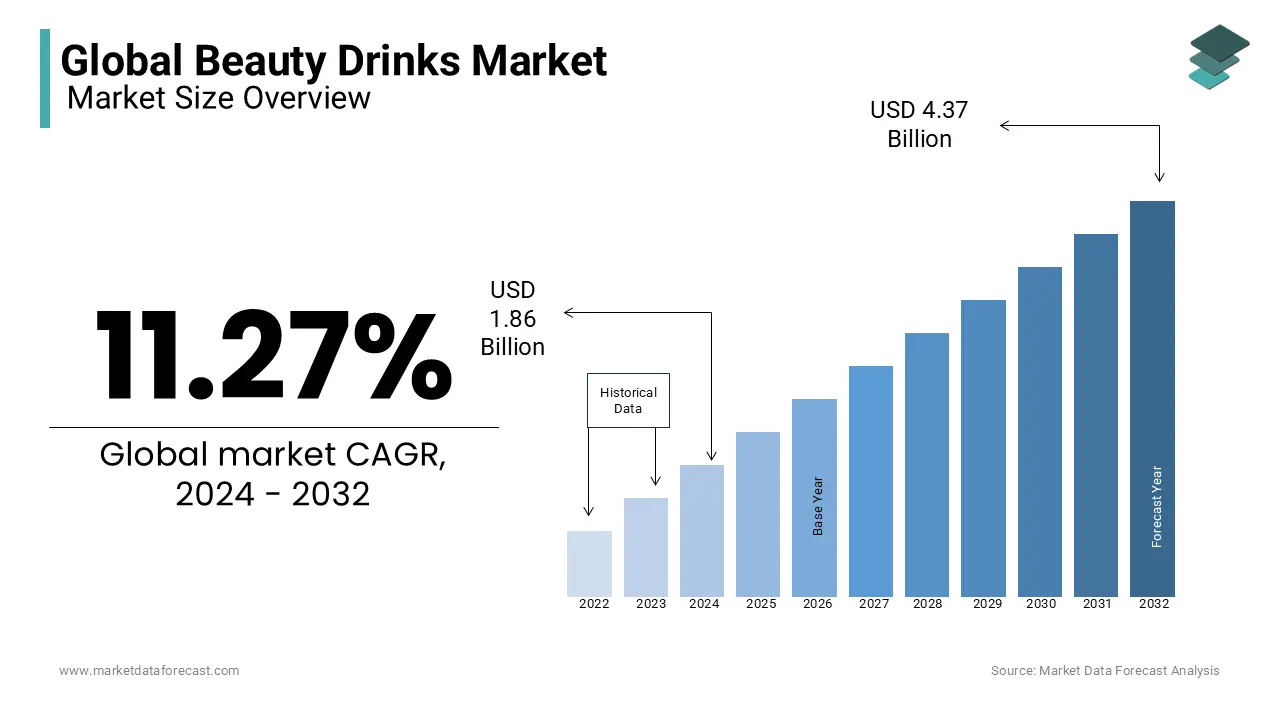

The global beauty drinks market size was valued at USD 2.07 Billion in 2025. The global market is expected to grow at a CAGR of 11.27% from 2026 to 2034 and be valued at USD 5.40 billion by 2034 from USD 2.30 billion in 2026.

Among all the ingestible and topical mix items inside the business, beauty drinks are ending up being an exceptionally agreeable choice, with a developing inclination for these items. Air poisons incorporate polycyclic hydrocarbons that, at last, result in quick aging. Buyers look for reliable alternatives that will inevitably bolster the beauty drinks market around the globe. The significant explanations behind the expanded interest in beauty drinks incorporate expanding commonness of way of life maladies and individuals intentionally taking preventive healthcare measures. Likewise, the market for beauty drinks is overwhelmingly determined by the standard purchaser to move toward preventive skincare, with the expanding maturing populace in developed nations. Moreover, developed markets, similar to the United States and Europe, are finding the undiscovered portion of altered items dependent on health claims.

CURRENT SCENARIO OF THE BEAUTY DRINKS MARKET

The beauty drinks market is experiencing a swift rise. Today, investment in underground research and development for product innovation has significantly intensified by brands. Lately, beauty and health offerings with unique elements are becoming popular. Especially, for instance, Mashiro Inc., an innovative company, has integrated stem cells and fucoidan into its placenta and collagen. Moreover, in the last few years, consumer understanding of the rise of eco-friendly beauty products and the concept of enhancing health from within is gaining momentum. This has compelled beauty and health companies globally to make new products to satisfy this necessity.

Apart from this, collagen drinks have become a common supplement in the last few years, providing an easy-to-use and relevant item for the target audience focused on overall health, hydration, and skin elasticity.

- According to the researchers from the Shenzhen Porshealth Bioengineering Co., the study of the impacts of an orally managed collagen beverage mixing EP and CP on the skin health of middle and young-aged females under the single-site randomized controlled trial discovered that the group consuming collagen drink exhibited considerable progress i.e. 39.19 per cent rise in skin hydration or moisturization and 33.45 per cent drop in transepidermal water loss against the placebo group.

MARKET TRENDS

The trend is towards the adoption of healthy beverages that are enriched with the extracts of fruits and vegetables to maintain good skin care along with nail and hair growth.

Fruit and vegetable extracts act as a detoxifier that helps brighten the skin along with the reduction of acne, pigmentation, and scars. The presence of essential amino acids, minerals, and vitamins reduces the skin ache and brightens the skin. Rising awareness over the consumption of beauty drinks for healthy skin, hair, and nails is likely to showcase huge growth opportunities for the market during the forecast period.

- A study released in MDPI, the choices of both men and women in consuming citrus fruit juices were the same. 28.1 per cent of men and 28.4 per cent of women were more probably to drink juices 1 to 3 times in a week. The frequency of almost daily or daily juice consumption was higher in men.

MARKET DRIVERS

Rising disposable income, eventually increasing the urban population, is a major factor driving the market share.

- As per Retail Voice, certainly, personal care and beauty continue to be a focus for several as customer spending surged to a projected 11.3 billion pounds in 2023 regardless of external pressures.

The rising prevalence of adopting new products in urban areas to maintain healthy skin will eventually leverage the market growth rate. With the constantly growing demand for the consumption of beauty drinks from emerging countries like China, India, and Japan, the preference to launch high-quality beauty drinks with the latest technological developments is anticipated to escalate the growth rate of the market. Quick adoption of advanced technology in the food and beverages, pharmaceutical, and cosmetics industries is ascribed to fuel the market's growth rate to the extent. Increasing awareness over the use of beauty drinks to reduce skin acne-related problems in a more natural way, such as taking up medications, is greatly influencing the growth rate of the beauty drinks market. The number of people suffering from acne is increasing across the world, which is inclined to show huge positive results for the growth rate of the market.

- According to the latest reports, around 85% of people in America experience any kind of acne at some point in their lives. Also, fifty million people are already suffering from some kind of acne-related problems in the US where out of which 15% of people have severe acne issues. On average, people between 20- and 27-years old face acne, according to a study conducted by the Journal of the American Academy of Dermatology.

This study revealed that more than 96% of people suffering from acne feel depressed due to their condition, which is influencing them to adopt beauty drinks in their regular diet. This attribute is anticipated to fuel the growth rate of the market in the coming years.

Technological advancements in pharmaceutical and personal care are booming, and manufacturers are launching various products in favour of consumer preferences. The trend towards the adoption of organically manufactured drinks is greatly influencing the market growth value. The awareness through social media influencers is rising in every country where the demand for these products is increasing at a random rate that further levels up the market growth rate.

In addition, the rising prevalence of e-commerce platforms where beauty drinks are easily available online and delivered to the doorstep is majorly attracting huge customers that will eventually lavish the growth rate of the global beauty drinks market.

MARKET RESTRAINTS

However, the launch of local brand products at very low cost is a big concern for the top companies.

Local brand products are made with low-quality ingredients that pose negative feedback on the beauty drinks, which further reflects on the branded products. Therefore, the availability of these local brand beauty drinks products is seriously posing a negative impact on the growth rate of the market. Also, government authorities are imposing strict norms over promoting beauty drinks, which is causing serious health issues among a few consumers and is likely to impede the growth rate of the market.

MARKET OPPORTUNITIES

The demand for a unique formulation-based beverage is expected to accelerate the beauty drinks market. Brands are looking for unique ingredients which are not frequently used in beauty drinks, like superfoods (acai, spirulina) or adaptogens (reishi, ashwagandha), providing extra health advantages. Consumers are more inclined towards natural and sugar-free beverages. Modern-day beauty customers are more intelligent than before, progressively looking for beauty items online to discover the most impactful products. So, the demand for edible skincare with collagen-boosting elements, vitamins, and superfoods is projected to escalate.

Moreover, in the coming years, the union of hydro stretch therapy and bio-remodelling is anticipated to transform the treatments for anti-ageing, as a result, the market is expected to thrive in the coming years.

MARKET CHALLENGES

The soaring prices of beauty drinks due to the fluctuations in the supply chain is a key challenging factor for the market players.

High-quality beauty drinks cost a lot as the availability of the raw materials used in manufacturing these drinks is slowly degrading. Nutricosmetic products are too expensive where, and common people cannot afford those products. The cost of manufacturing high-quality beauty drinks requires many research and development activities with huge investments and is inclined to show a negative growth rate in the global beauty drinks market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.27% |

| Segments Covered | By Ingredient Type, Function, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | SAPPE Public Company Limited, Shiseido Co. Ltd, Vital Proteins LLC, Kinohimitsu, Lacka Foods Limited, Gelita AG, Big Quark, Hangzhou Nutrition and Others. |

SEGMENTAL ANALYSIS

Global Beauty Drinks Market Analysis By Ingredient Type

The antioxidants are presumed to account for a prominent share of the worldwide beauty drinks market due to the increasing demand for such products among consumers across the globe. The vitamins & Minerals segment is gaining much traction over the growth rate of the market with the growing prominence to spend huge amounts on health and wellness programs.

Global Beauty Drinks Market Analysis By Function

The anti-aging segment is leading with the highest share of the market with the growing aging population across the world. The number of people aged above 30 is increasing globally, and the demand to maintain an excellent skincare routine among these people is growing with the help of beauty drinks, which is ascribed to propel the growth rate for the anti-aging beauty drinks market.

Global Beauty Drinks Market Analysis By Distribution Channel

The online segment is growing at a faster rate during the forecast period. The increasing availability of products in online shopping stores through the launch of various applications in smartphones is inclined to fuel the market growth rate. Nowadays, the number of people using smartphones is gradually increasing, even in remote areas. With the extension of internet connectivity devices worldwide, the demand for online shopping is eventually increasing, which is further fuelling the growth rate of the online beauty drinks market share. The specialty stores segment is next in leading the dominant market share. In developed countries, people are more inclined to purchase beauty drinks from specialty stores to avail themselves of the best and highest-quality products at varying costs, increasing the prominence of the specialty stores' market value.

REGIONAL ANALYSIS

North America to Drive the Global Beauty Drinks Market.

North America's beauty drinks market is leading with the dominant share of the market. Health is becoming a lower priority among Americans because of the development of a tumultuous work-life plan for the United States. This prompts a requirement for nutricosmetic items, similar to beauty drinks. Organizations are primarily focusing on purchasers who are 30 years or older, as they seem, by all accounts, to be increasingly concerned with respect to health and aging. The offer of beauty drinks in the nations of North America, particularly the United States, is foreseen to increase colossally because of the expanding frequency of skin issues, hair fall issues, and the impact of the style business. To catch this chance, the beauty drink organizations that are overwhelming the area are progressing in the direction of augmenting the number of brands and expanding their arrangements.

Following North America, Europe is next in leading the significant share of the market. High per capita income is one of the primary factors that will help the market grow in the European region. European people focus more on beauty products, where the prominence of maintaining a good skincare routine through beauty drinks is quite common and is increasing the market share. Government support to prevent skin ache diseases is increasing eventually, and the need to launch beauty products at affordable costs is surging the growth rate of the market. The number of people suffering skin-related diseases is very high in Europe, where the government authorities are promoting beauty drinks to lower the risks and prevent ache issues. Support from government authorities is likely to increase the growth rate of the beauty drink market in European countries. Spain, Italy, Germany, France, and the UK are the major countries contributing the highest share of the market. High expenditure on nutricosmetics in these countries is the major attribute accelerating the growth rate of the market.

Asia Pacific is likely to hit the highest CAGR by the end of 2029. Growing research and development activities to launch quality cosmetics and pharmaceutical products in favor of the users will eventually escalate the growth rate of the Asia Pacific beauty drinks market. Promoting the benefits of beauty drinks that contain essential vitamins helps rejuvenate the skin in various ways through social media and other channels to reach target customers in a more effective way. The companies are gaining much traction over the share of the market. Also, people's interest in health and wellness, especially in emerging countries like India, China, Japan, and others, is outraging the market size. In addition, the rising prominence for the adoption of organically manufactured beauty drinks that have huge health benefits is conquered in gearing up the market share. Apart from these, the market is also expected to grow in Australia and New Zealand because of the motivational and sociodemographic factors that drive customers of the hospitality industry to willingly pay premium costs for healthy drinks.

- According to the study published in the National Center for Biotechnology Information, beverages represent more than 40 per cent of revenue in the hospitality industry. It also stated that hospitality companies have opportunities to provide more functional foods, like drinks having less sugar and extra probiotics and vitamins, as an effective tactic to lure the “health dollar”.

Also, the growing population is another factor anticipated to leverage the growth rate of the beauty drinks market. The rapid adoption of advanced technologies in the food and beverage industry shall contribute to huge growth opportunities for the beauty drinks market in Asia Pacific. In addition, the growing number of working women populations who are mostly beauty conscious and have less time to eat only healthy foods prefer to have high nutritional value beauty drinks for healthy skin.

- For instance, in China, around 43.2 percent of the population are working women, which means the contribution of beauty products is merely high in this country.

RECENT HAPPENINGS IN THE MARKET

- In January 2025, Pretty Tasty introduced a new beverage range, “Pretty Tasty Collagen Tea”, created with collagen peptides to enhance the health of nails, joints, and hair. This tea comes in two flavours, including raspberry and peach. Moreover, the range has natural elements like black currants and carrots for colour and is minimally sweetened with the help of stevia leaf extract. It is created with 10 grams of protein and no synthetic colours are added. The line is without any important allergens, involving nuts, lactose, gluten, and soy.

KEY PLAYERS IN THE GLOBAL BEAUTY DRINKS MARKET

Companies playing a notable role in the global beauty drinks market include SAPPE Public Company Limited, Shiseido Co. Ltd, Vital Proteins LLC, Kinohimitsu, Lacka Foods Limited, Gelita AG, Big Quark, and Hangzhou Nutrition Biotechnology Co. Ltd. Around the world, Shiseido Company Limites accounted for the protruding portion of the beauty drinks business, followed by other players like SAPPE Public Company Limited and Vital Proteins Ltd. New products like Verisol by Gelita AG are improving the metabolism of skin with the addition of bioactive collagen peptides. In addition, several known firms in the beauty drinks market, like Big Quark, Kinohimitsu, Hangzhou Nutrition Biotechnology Co. Ltd, etc., are engaging in more product launches, partnerships, expansions, and innovations to increase their overall share in the global market.

DETAILED SEGMENTATION OF THE GLOBAL BEAUTY DRINKS MARKET INCLUDED IN THIS REPORT

This research report on the global beauty drinks market has been segmented and sub-segmented based on the following categories.

By Ingredient Type

- Vitamins & minerals

- Protein & peptides

- Antioxidants

- Co-enzymes

By Function

- Anti-aging

- Detoxication

- Radiance

- Vitality

By Distribution Channel

- Supermarket & hypermarket

- Specialty stores

- Online

By Region

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What are the key drivers driving the growth of the specialty food ingredients market?

Several factors contribute to the growth of this market, including increasing consumer demand for natural and clean-label products, rising awareness about health and wellness, the popularity of ethnic and gourmet cuisines, and advancements in food processing technologies.

2. What are the challenges faced by the specialty food ingredients market?

Challenges include the high cost of some specialty ingredients, regulatory complexities related to labeling and claims, sourcing sustainable and ethically produced ingredients, and addressing consumer concerns about allergens and food safety.

3. What are some emerging trends in the specialty food ingredients market?

Emerging trends include using alternative proteins such as insect proteins or lab-grown meats, developing plant-based alternatives for traditional dairy and meat products, innovations in natural food preservation techniques, and integrating digital technologies for traceability and quality assurance.

4. Which ingredient segment dominates the Beauty Drinks Market?

Collagen-based beauty drinks dominate the market as they support skin elasticity, firmness, and youthful appearance.

5. What are the major functions of beauty drinks?

Major functional benefits include anti-aging, detoxification, skin hydration, radiance enhancement, and vitality improvement.

6. Why are millennials adopting beauty drinks?

Millennials are increasingly adopting beauty drinks due to growing concerns about premature aging and preference for convenient wellness solutions.

7. What are the main distribution channels for beauty drinks?

Beauty drinks are mainly distributed through specialty stores, supermarkets, online platforms, and e-commerce websites

8. Which functional segment holds the largest market share?

The anti-aging segment holds the largest market share due to increasing consumer demand for wrinkle reduction and youthful skin maintenance.

9. What role do antioxidants play in beauty drinks?

Antioxidants help protect skin cells from environmental damage and promote healthy skin regeneration.

10. How are clean-label trends impacting the Beauty Drinks Market?

Consumers are increasingly preferring natural, organic, and chemical-free formulations, encouraging manufacturers to develop clean-label beauty drinks.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com