Global Sports Drink Market Size, Share, Trends & Growth Forecast Report Segmented By Product (Isotonic, Hypertonic and Hypotonic), Distribution Channel (Retail & Supermarkets and Online Platform), And Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis (2026 to 2034)

Market Size, 2025

$27.5 BnMarket Estimate, 2026

$28.61 BnMarket Forecast, 2034

$39.22 BnCAGR, 2026–2034

4.02%Global Sports Drink Market Size

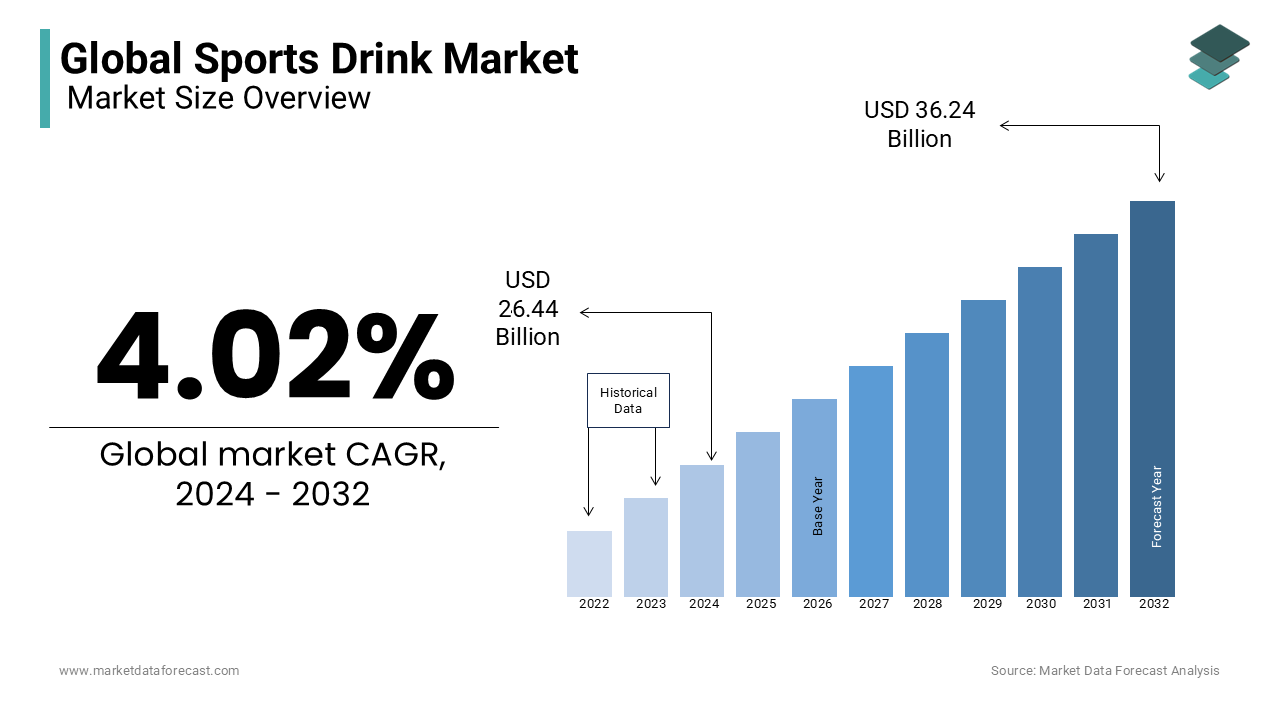

The global sports drink market size was valued at USD 27.50 billion in 2025. The global market size is estimated to grow at a CAGR of 4.02% from 2026 to 2034 and be worth USD 39.22 billion by 2034 from USD 28.61 billion in 2026.

Sports drinks are formulated beverages designed to facilitate rapid hydration, electrolyte replenishment, and energy delivery during or after physical exertion. Unlike standard isotonic or soft drinks, they contain a precise balance of carbohydrates, sodium, potassium, and other electrolytes to support fluid retention and muscle function. These beverages are increasingly consumed not only by athletes but also by active individuals seeking performance optimization or recovery support. According to the American College of Sports Medicine, over 65% of regular exercisers in the U.S. report using sports drinks during workouts lasting more than 60 minutes, reflecting their integration into mainstream fitness routines. The World Health Organization notes that rising urbanization and sedentary lifestyles have paradoxically fueled demand for performance-enhancing hydration, as more individuals engage in structured exercise to counteract inactivity.

MARKET DRIVERS

Expansion of Fitness Culture and Active Lifestyles

The proliferation of structured fitness regimens from high-intensity interval training to marathon running has significantly amplified the demand for sports drinks as essential recovery tools. As per the International Health, Racquet & Sportsclub Association (IHRSA), over 200 million people were health club members globally in 2023, a 12% increase from pre-pandemic levels, indicating sustained engagement in physical activity. This behavioral shift is particularly pronounced among millennials and Gen Z, who view hydration as integral to performance and recovery. A 2023 survey by the National Strength and Conditioning Association revealed that 73% of gym-goers consume sports drinks post-workout to replenish electrolytes, especially during resistance or endurance training. Brands like Gatorade and Powerade have capitalized on this trend by aligning with fitness influencers, sponsoring marathons, and launching product lines tailored to specific workout types.

Scientific Endorsement and Clinical Validation of Hydration Needs

The robust body of clinical research validating their physiological benefits during prolonged physical activity is additionally levelling up the growth of the wood chips market. According to the American College of Sports Medicine, individuals who lose more than 2% of their body weight in fluid during exercise experience measurable declines in cognitive and physical performance, a threshold easily reached during intense training. Sports drinks, with their optimal sodium-carbohydrate composition, are proven to enhance fluid absorption and delay fatigue. A 2022 meta-analysis published in Medicine & Science in Sports & Exercise concluded that carbohydrate-electrolyte solutions improved endurance performance by an average of 12% compared to water alone.

MARKET RESTRAINTS

High Sugar Content and Associated Health Concerns

The growing scrutiny due to high sugar content, which can contribute to metabolic health risks when consumed outside of intense physical activity is impeding the growth of the wood chips market. According to the Centers for Disease Control and Prevention, the average 20-ounce bottle of a leading sports drink contains 34 grams of sugar exceeding half the daily recommended limit for adults. This has led to public health warnings, particularly regarding youth consumption. The American Academy of Pediatrics advises against routine sports drink use for children under 18 unless engaged in prolonged, vigorous exercise. Additionally, cities like Berkeley and Philadelphia have included sports drinks in sugar-sweetened beverage taxes, signaling regulatory disapproval.

Misalignment with Low-Intensity or Sedentary Lifestyles

The growing disconnect between product functionality and actual consumer activity levels is also enhancing the growth of the sports drink market. As per the National Health and Nutrition Examination Survey (NHANES), only 23% of U.S. adults meet the recommended 150 minutes of moderate-intensity aerobic activity per week, suggesting that the majority of consumers do not engage in exercise intense or long enough to require electrolyte replacement. Yet, marketing and availability often encourage consumption regardless of exertion level. The Harvard T.H. Chan School of Public Health reports that sports drink consumption among inactive individuals rose by 18% between 2015 and 2022, driven by branding that equates these beverages with energy and vitality. Regulatory bodies such as the UK’s National Health Service have issued guidelines cautioning against routine use without physical demand.

MARKET OPPORTUNITIES

Development of Low-Sugar and Functional Sports Drinks for Everyday Use

The emergence of low-sugar, electrolyte-enhanced variants designed for daily hydration rather than just athletic performance is oslely to create new opportunities for the growth of the sports drink market. This shift caters to consumers seeking functional benefits without excessive caloric intake. Brands like Gatorade’s G Zero and Powerade Ultra offer full electrolyte profiles with zero or minimal sugar, aligning with clean-label and metabolic health trends. According to the Nutrition Business Journal, sales of low- and no-sugar sports drinks grew by 15.6% in 2023, outpacing traditional variants. These products are increasingly consumed not during workouts but throughout the day by professionals, students, and shift workers due to claims of sustained energy and mental clarity.

Penetration in Emerging Markets with Rising Sports Participation and Urbanization

The emerging economies in Southeast Asia, Latin America, and Africa present substantial growth potential for sports drinks with rising youth engagement in sports, urbanization, and increasing disposable income is additionally to escalate the growth of the sports drink market. In India, school and collegiate sports participation has grown by 32% since 2018, as reported by the Sports Authority of India, creating a new generation of performance-conscious consumers. Similarly, Brazil’s Ministry of Sports notes that over 12 million adolescents participate in organized athletics, fostering early brand loyalty. Urban populations in cities like Jakarta, Lagos, and Bogotá are adopting gym culture and endurance sports, increasing demand for hydration solutions. A 2023 NielsenIQ report indicates that sports drink sales in Indonesia grew by 13.4% year-on-year, supported by aggressive retail placement and sponsorship of local marathons.

MARKET CHALLENGES

Ingredient Sourcing and Supply Chain Vulnerability for Electrolytes and Additives

The production of sports drinks relies on consistent access to key functional ingredients such as sodium citrate, potassium chloride, and carbohydrates like dextrose, many of which are subject to supply chain volatility. The 2022 sanctions on Belarusian potash exports led to a 22% spike in potassium chloride prices, as reported by IHS Markit. Additionally, sugar and corn-derived dextrose are sensitive to climate fluctuations; the Food and Agriculture Organization noted that droughts in the U.S. Midwest reduced corn yields by 10% in 2023, impacting raw material availability. These supply constraints increase formulation costs and complicate pricing strategies for premium or clean-label variants.

Regulatory and Labeling Disparities Across Global Markets

Sports drink manufacturers face a fragmented regulatory landscape, where definitions, health claims, and permissible additives vary significantly across regions, complicating global product standardization. In the European Union, Regulation (EC) No 1924/2006 restricts claims like “boosts energy” unless supported by specific scientific dossiers, while the U.S. FDA permits broader usage with less stringent validation. Moreover, countries like Thailand and South Africa have introduced sugar taxes that include sports drinks if sugar content exceeds thresholds, forcing reformulation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.02% |

| Segments Covered | By Product, Distribution Channel and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | PepsiCo Inc, Coca-Cola Company, AJE Group, BodyArmor, Arizona Beverage Company, Gatorade Company, J Donohoe Beverages Ltd, BA Sports Nutrition, LLC, GU Energy Labs, BE Innovations, CytoSport, Inc and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The isotonic segment was the largest and held a prominent share of the sports drink market in 2025. These beverages, which match the body’s natural fluid concentration (osmolality of ~280–300 mOsm/kg), are scientifically optimized for rapid hydration and energy delivery during moderate to intense physical activity. Their dominance is rooted in widespread acceptance among athletes, fitness enthusiasts, and sports organizations. According to the American College of Sports Medicine, isotonic drinks are recommended for activities lasting longer than 60 minutes, a guideline adopted by schools, professional teams, and military training programs globally.

The hypotonic segment is likely to witness a CAGR of 9.4% from 2026 to 2034. These beverages, with osmolality below 280 mOsm/kg, are designed for rapid fluid absorption, making them ideal for quick rehydration during short-duration or high-sweat activities. Their accelerated growth is fueled by rising demand for low-calorie hydration solutions that prioritize fluid replenishment over energy supply. As per the International Society of Sports Nutrition, hypotonic drinks are preferred in hot climates and endurance events where fluid loss exceeds 2% of body weight, a scenario increasingly common due to global temperature rise.

By Distribution Channel Insights

The retail and supermarket segment was accounted in holding a significant share of the sports drink market in 2025 with the impulse-driven nature of beverage purchases and the strategic placement of sports drinks near checkout counters, gyms, and refrigerated sections in high-traffic stores. According to the Food Marketing Institute, over 60% of bottled beverage purchases in the U.S. occur in supermarkets and mass merchandisers, where visibility and promotional displays significantly influence consumer decisions. The integration of sports drinks into daily shopping baskets is reinforced by co-merchandising with fitness products, energy bars, and protein supplements.

The online platforms segment is esteemed to witness a CAGR of 12.8% during the forecast period with the shifting consumer behavior toward digital commerce, subscription models, and direct-to-consumer (DTC) brand engagement. As per the U.S. Department of Commerce, e-commerce accounted for 15.6% of total retail sales in 2023, with beverages showing the highest growth rate in online basket penetration. Consumers increasingly purchase sports drinks in bulk through Amazon, Instacart, and brand-owned websites, attracted by convenience, competitive pricing, and home delivery.

REGIONAL ANALYSIS

North America Sports Drink Market Insights

North America was the top performer of the global sports drink market by accounting for 46.4% of share in 2025 with a deeply ingrained fitness culture, widespread sports participation, and strong brand presence. The National Federation of State High School Associations confirms that over 7.9 million students participated in high school sports in 2023, creating early brand loyalty. Major leagues such as the NFL, NBA, and NCAA have long-standing sponsorship deals with Gatorade, reinforcing product visibility. Additionally, the U.S. Department of Health and Human Services reports that more than 50% of adults engage in regular physical activity, increasing demand for performance hydration.

Europe Sports Drink Market Insights

Europe was accounted in holding 25.4% of the global sports drink market in 2025. European consumers increasingly favor functional, low-sugar formulations, driven by regulatory pressure and health awareness. According to the European Federation of Bottled Waters, sports drink sales in Western Europe grew by 6.3% in 2023, with isotonic and hypotonic variants gaining traction among endurance athletes. The Tour de France, UEFA Champions League, and major marathons serve as high-visibility platforms for brand activation. Additionally, the European Environment Agency reports that rising summer temperatures have increased heat-related hydration demand, particularly in Southern Europe.

Asia Pacific Sports Drink Market Insights

Asia Pacific sports drink market growth is likely to grow with rapid expansion driven by urbanization, youth engagement in sports, and rising disposable incomes. China, India, and Japan are key contributors, with China alone representing over 40% of regional sales, as reported by the Asia Pacific Sports Nutrition Association. In India, the Khelo India initiative has increased youth sports participation by 35% since 2018, fostering a new generation of performance-conscious consumers. Japan’s aging population is adopting sports drinks for hydration support, with the Ministry of Health recommending electrolyte intake for elderly individuals during heatwaves.

Latin America Sports Drink Market Insights

Latin America sports drink market growth is likely to grow with Brazil and Mexico serving as primary growth engines. The region’s market is fueled by passion for football, rising gym culture, and government-led health initiatives. As per the Brazilian Institute of Geography and Statistics, over 38 million Brazilians engage in regular physical activity, creating a robust consumer base. Football clubs like Flamengo and América México have sponsorship deals with major brands, enhancing visibility.

Mexico Sports Drink Market Insights

Mexico’s sugar tax, implemented in 2014, has redirected consumers toward lower-sugar alternatives, including reformulated sports drinks. The Mexican Institute of Social Security reports that sales of non-sugary functional beverages increased by 19% between 2015 and 2023. Retail chains like Soriana and Extra have expanded chilled beverage sections, while digital platforms such as Mercado Libre report rising online sales.

Middle East & Africa Sports Drink Market Insights

The Middle East and Africa sports drink market growth is likely to grow steadily throughput the forecast period. The UAE’s Ministry of Health recommends hydration with electrolytes during outdoor activities is aligning with public health campaigns. Dubai Fitness Challenge, a 30-day citywide initiative, has boosted sports drink visibility since its 2017 launch. In Saudi Arabia, Vision 2030 includes a national sports strategy aiming to increase physical activity participation to 40% of the population by 2030, up from 13% in 2018. South Africa dominates the African segment, with sports drink sales growing by 9.1% in 2023, according to Statista Africa.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies that play a significant role in the global sports drink market include PepsiCo Inc, Coca-Cola Company, AJE Group, BodyArmor, Arizona Beverage Company, Gatorade Company, J Donohoe Beverages Ltd, BA Sports Nutrition, LLC, GU Energy Labs, BE Innovations, CytoSport, Inc and Others.

The sports drink market is marked by intense rivalry among multinational corporations, regional brands, and emerging functional beverage startups. Dominant players like Gatorade and Powerade leverage scientific credibility, global sponsorships, and extensive distribution networks to maintain prominent position. However, regional competitors such as Aquarius and Burn are gaining ground through localized flavors and climate-specific marketing. The rise of health-conscious consumers is driving demand for low-sugar, electrolyte-enhanced alternatives, prompting innovation across formulations. Digital platforms and e-commerce are reshaping accessibility, while sustainability pressures are forcing packaging overhauls. Regulatory scrutiny on sugar content and health claims adds complexity, particularly in Europe and Asia.

TOP PLAYERS IN THE MARKET

PepsiCo (Powerade)

PepsiCo has significantly expanded Powerade’s footprint across the Asia Pacific region through localized product development and high-impact sports partnerships. In 2023, the company launched Powerade Ultra, a zero-sugar isotonic variant, in Japan, South Korea, and Australia, aligning with regional demand for low-calorie hydration. The brand has strengthened its presence by sponsoring national cricket teams in India and Australia, leveraging the sport’s massive viewership to enhance visibility. PepsiCo also introduced region-specific packaging with local languages and cultural motifs to improve consumer resonance. In collaboration with convenience retailers like 7-Eleven and FamilyMart, Powerade has optimized chilled distribution in urban centers. Additionally, the company launched digital campaigns featuring regional athletes on platforms like TikTok and WeChat, targeting younger demographics.

Coca-Cola Company (Gatorade)

The Coca-Cola Company has prominent Gatorade’s dominance in the Asia Pacific sports drink market through strategic localization, scientific innovation, and deep integration with athletic ecosystems. The company has also introduced regionally inspired flavors such as lychee, green tea, and yuzu to cater to local palates. Gatorade has partnered with elite sports academies in India, Australia, and Thailand to provide hydration education and branded products. Its presence in marathons, university leagues, and esports tournaments enhances cross-generational appeal. In 2023, Coca-Cola expanded Gatorade’s ready-to-drink and powder formats through e-commerce platforms like Tmall and Flipkart, improving accessibility.

Asahi Group Holdings (Aquarius)

Asahi Group Holdings has established Aquarius as a leading sports drink brand in Asia through decades of regional focus, scientific formulation, and climate-responsive marketing. Originating in Japan, Aquarius has become a household name in countries like Thailand, Indonesia, and Malaysia, where high humidity and temperatures amplify hydration needs. In 2023, Asahi introduced Aquarius Water Boost, a hypotonic variant with reduced sugar and added B-vitamins, across Southeast Asia, targeting health-conscious urban professionals. The brand is widely distributed through vending machines, convenience stores, and transportation hubs, ensuring high availability. Asahi has also partnered with national sports federations in Thailand and Vietnam to support youth athletics and promote proper hydration practices. Its sponsorship of the Tokyo Marathon and digital campaigns featuring local influencers reinforce brand credibility.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the sports drink market are deploying product innovation, strategic sponsorships, regional customization, digital engagement, and sustainable packaging to consolidate their positions. Companies are reformulating products to include lower sugar, added electrolytes, and clean labels to meet health demands. Partnerships with sports leagues, fitness events, and athletes enhance brand credibility and visibility. Localization of flavors and packaging improves cultural relevance in diverse markets. E-commerce expansion and direct-to-consumer models increase accessibility and customer retention. Investment in recyclable materials and lightweight bottles addresses environmental concerns.

RECENT HAPPENINGS IN THE MARKET

- In July 2023, PepsiCo launched Powerade Ultra, a zero-sugar isotonic drink, in Australia and South Korea, which is expanding its low-calorie portfolio and enhancing shelf presence in modern retail and gym outlets.

- In March 2025, The Coca-Cola Company introduced Gatorade’s Gx BCAA variant in India, targeting fitness enthusiasts with branched-chain amino acids for muscle recovery with influencer campaigns on Instagram and YouTube.

- In October 2023, Asahi Group Holdings expanded Aquarius distribution to 50,000 convenience stores in Indonesia through a partnership with Alfamart by boosting regional availability and brand visibility.

- In January 2025, Monster Beverage launched its new sports hydration line, Reignite, in Japan with three hypotonic variants by leveraging its existing energy drink distribution network for rapid market penetration.

MARKET SEGMENTATION

This research report on the global sports drink market has been segmented and sub-segmented based on product, distribution channel and region.

By Product

- Isotonic

- Hypertonic

- Hypotonic

By Distribution Channel

- Retail and Supermarkets

- Online Platforms

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the sports drink market?

The sports drink market includes beverages designed to rehydrate, replenish electrolytes, and provide energy during or after physical activities.

2. What is driving the growth of the sports drink market?

Rising fitness trends, increasing participation in sports, and growing awareness of hydration and performance needs are key drivers.

3. Which regions dominate the sports drink market?

North America leads the market, while Asia-Pacific shows the fastest growth due to urbanization and rising health-conscious consumers.

4. Who are the leading players in the sports drink market?

Major players include PepsiCo (Gatorade), Coca-Cola (Powerade), BodyArmor, Lucozade, and Danone.

5. What challenges does the sports drink market face?

High sugar content concerns, competition from functional water and energy drinks, and regulatory restrictions are major challenges.

6. How do sports drinks differ from energy drinks?

Sports drinks focus on hydration and electrolyte balance, while energy drinks are designed to boost mental alertness with caffeine and stimulants.

7. How is innovation influencing the sports drink market?

Companies are introducing plant-based electrolytes (like coconut water), sugar-free formulas, and eco-friendly packaging to attract health-conscious buyers.

8. What is the future outlook for the sports drink market?

The market is expected to grow steadily with rising sports participation, fitness culture, and demand for functional, healthier hydration options.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com