Europe Biopharmaceuticals Market Research Report – Segmented By Product Type (Monoclonal Antibodies (mAb), Erythropoietin, Biotech Vaccines, Recombinant Human (RH) Insulin, Granulocyte Colony-stimulating Factor (G-CSF), Interferon, Human Growth Hormones (HGH)), Therapeutic Type & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis From 2025 to 2033

Europe Biopharmaceuticals Market Size

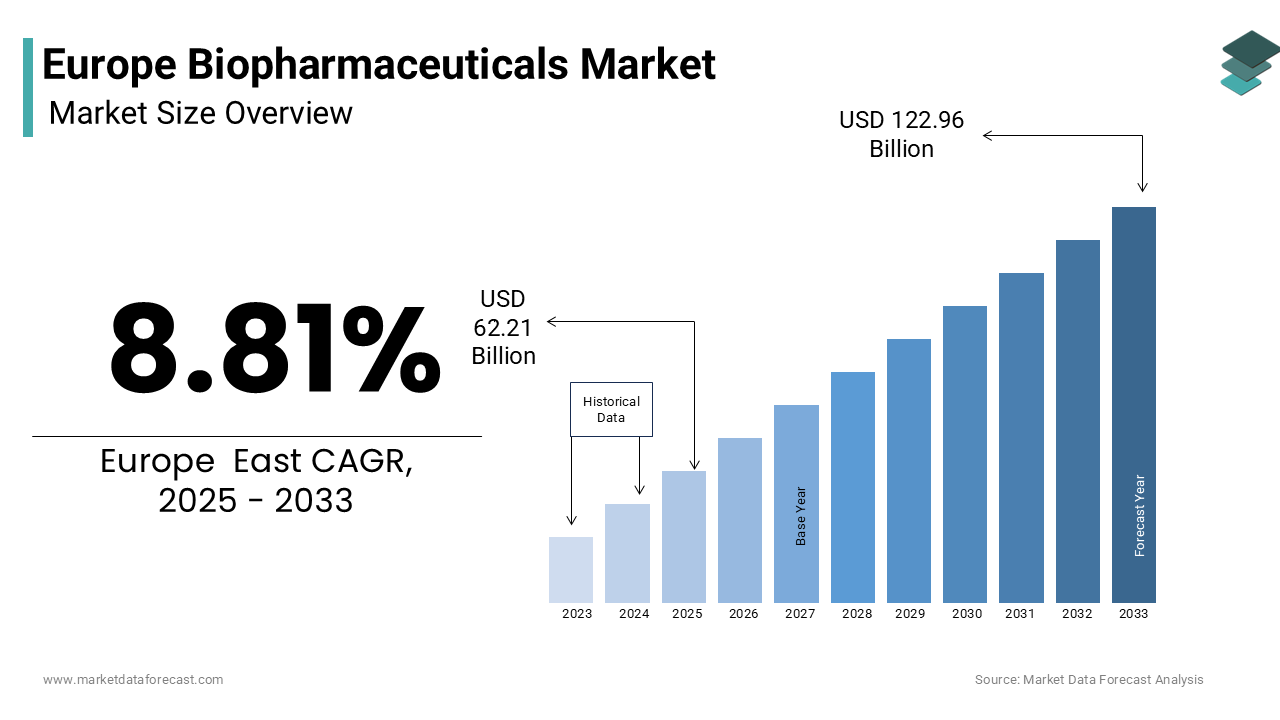

The European Biopharmaceuticals Market was valued at USD 57.13 billion in 2024, is estimated to reach USD 62.21 billion in 2025, and is projected to reach USD 122.96 billion by 2033, growing at a CAGR of 8.89% from 2025 to 2033.

The biopharmaceuticals is a dynamic ecosystem of therapeutic agents derived from biological sources which includes monoclonal antibodies, recombinant proteins, vaccines, and gene and cell therapies. These products are engineered to target complex diseases with high specificity by providing transformative outcomes in oncology, autoimmune disorders, and rare genetic conditions. The European Medical Agency recommended 77 medicines for marketing authorization in 2023 and 39 of these included a new active substance that had not previously been authorized in the EU. As per the European Federation of Pharmaceutical Industries and Associations (EFPIA) more than 1,200 biopharmaceuticals were in clinical development across Europe in 2023.

MARKET DRIVERS

The Advancements and prevalence of chronic and rare diseases is the primary driver enhancing the growth of Europe Biopharmaceuticals Market. In oncology, where biopharmaceuticals dominate treatment paradigms where according to a study published in BMC Cancer in March 2025, citing the GLOBOCAN data has reported 4,471,422 new cancer cases in Europe for the year 2023. Furthermore, with approximately 30 million Europeans affected by rare diseases, of which 72% are of genetic origin, the demand for targeted biologics and advanced therapy medicinal products (ATMPs) continues to surge. This unmet medical need which is coupled with aging demographics has positioned biopharmaceuticals as indispensable in Europe’s evolving healthcare strategy.

The expansion of biosimilars and supportive regulatory frameworks is prompting the growth of Europe Biopharmaceuticals Market. The European Medicines Agency has approved over 80 biosimilars since 2006, fostering competition and improving patient access to high-cost biologic therapies. Countries like Germany and the Netherlands have implemented proactive reimbursement policies, with biosimilar uptake in monoclonal antibody markets exceeding 70% in some therapeutic areas. According to European Union 2023 revision of the pharmaceutical legislation emphasizes incentives for innovation in biologics while escalating the pathways for biosimilar entry. According to data published by Science Direct, 32% of the drugs are new biological entities in European Medicines Agency database in 2023.

MARKET RESTRAINTS

The high costs associated with biopharmaceutical development and commercialization act as primary factor restraining the Europe Biopharmaceuticals Market expansion. The average cost to bring a biologic to market exceeds €2.1 billion, as reported by the EFPIA, with clinical trial expenses alone accounting for nearly 40% of total investment. Unlike small-molecule drugs, biologics require complex manufacturing processes which involves live cell cultures, stringent cold-chain logistics and specialized facilities which escalates the production costs. The financial burdens are particularly challenging for small and mid-sized biotech firms in countries like Spain and Poland.

Stringent regulatory and ethical complexities in advanced therapy development is another factor impeding the growth of Europe Biopharmaceuticals Market. While the EMA has established a Committee for Advanced Therapies (CAT), the approval process for gene and cell therapies remains long lasting with an average review time of 422 days which is significantly longer than the conventional drugs. The ethical concerns particularly around gene editing and germline modifications have prompted strict legislative boundaries in countries such as Germany and France, where constitutional laws limit embryonic stem cell research.

MARKET OPPORTUNITIES

The rapid advancements in precision medicine and genomic integration is ascribed to promote new opportunities for the Europe Biopharmaceutical Market growth. As per the European Commission, more than 600,000 genomes had been sequenced and shared across national biobanks by mid-2023. This data infrastructure enables the development of highly targeted biologics, particularly in oncology and monogenic disorders. For example, the UK’s Genomics England has facilitated the launch of over 40 gene therapy trials since 2020.

Increasing public-private collaborations and innovation hubs are likely to propel the growth of Europe Biopharmaceuticals Market. The Innovative Medicines Initiative (IMI), now succeeded by the Innovative Health Initiative (IHI), has mobilized over €3.5 billion in joint funding from the EU and industry stakeholders since its inception. Regional clusters such as the Basel Area in Switzerland, Medicon Valley in Denmark-Sweden, and Lyonbiopôle in France host over 600 biopharmaceutical firms and research institutions, fostering synergistic R&D. These ecosystems enhance knowledge transfer by reducing the development risks which drives Europe’s competitive edge in biopharmaceutical innovation leading to various opportunities.

MARKET CHALLENGES

The fragmented healthcare systems and unequal access is to pose a challenge for the growth of Europe Biopharmaceuticals Market. Even though, there is high Europe’s scientific growth the disparities in reimbursement and patient access persist across member states which promote challenges in the market growth. As per the European Observatory on Health Systems and Policies, the time lag between EMA approval and national reimbursement ranges from 6 months in Sweden to over 24 months in Hungary and Bulgaria. In 2023, the European Patients’ Forum reported that only 40% of approved orphan drugs were accessible in Eastern European countries, compared to over 90% in Germany and France. These inequities stem from divergent health technology assessment (HTA) methodologies and budget constraints particularly in lower-income nations which challenge the market revenue.

The presence of workforce shortages in biomanufacturing and bioinformatics threaten the scalability challenging the Europe Biopharmaceuticals Market growth. A 2023 study by the European Association for Biindustries (EuropaBio) revealed a deficit of approximately 150,000 skilled professionals in bioprocessing, quality control, and computational biology across the EU. This gap is particularly acute in emerging fields such as gene therapy manufacturing, where specialized training programs remain limited. Germany’s BioRegions initiative estimates that 30% of biomanufacturing positions went unfilled in 2023 due to a lack of qualified candidates. The European Centre for the Development of Vocational Training (Cedefop) projects a shortfall of 50,000 data scientists in life sciences by 2027.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Therapeutic Type, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic, |

| Market Leader Profiled | Merck & Co., Inc., F. Hoffmann-La Roche AG, Eli Lilly and Company, Inc., Sanofi, Amgen Inc., AbbVie Inc., Biogen Idec, Bayer AG, Johnson & Johnson Services, Pfizer, Inc. and Novartis AG. |

SEGMENTAL ANALYSIS

By Product Type Insights

The monoclonal antibodies (mAbs) segment dominated the Europe Biopharmaceuticals Market with largest share of 42.1% in 2024. The widespread application in treating high-burden diseases such as cancer, autoimmune disorders, and inflammatory conditions is propelling the market. The therapeutic efficacy of mAbs is rooted in their ability to precisely target disease-specific antigens by minimizing off-target effects. The enhancement in the mAb is the escalation in regulatory endorsement and clinical integration of biosimilars which have significantly broadened patient access is primarily driving the segment growth. The affordability has enabled national health systems to expand treatment coverage particularly in chronic conditions like rheumatoid arthritis where mAb use has increased by 18.3% annually across Scandinavia as noted by Nordics Health.

The biotech vaccines segment is predicted to witness the highest CAGR of 10.8% in Europe Biopharmaceuticals Market from 2025 to 2033. The structural transformation in vaccine development post-pandemic, with mRNA and viral vector platforms now central to Europe’s public health strategy is primarily driving the segment growth. The success of Pfizer-BioNTech and Moderna’s mRNA vaccines both developed with significant European R&D contributions demonstrated the scalability and rapid adaptability of biotech vaccine platforms which drives the segment growth.

By Therapeutic Type Insights

The Oncology segment led the Europe Biopharmaceuticals Market by capturing 48.4% of share in 2024. The rising cancer burden and the increasing reliance on biologic and advanced therapy medicinal products (ATMPs) for disease management is fueling the segment expansion. Monoclonal antibodies, immune checkpoint inhibitors, and CAR-T therapies have become standard of care particularly in non-small cell lung cancer, melanoma, and diffuse large B-cell lymphoma. The major driver to oncology’s market growth is the integration of targeted biologics into national cancer control plans. As per the EMA’s 2023 therapeutic trends report, the EMA approved 11 oncology biologics in 2023 which includes the bispecific antibody mosunetuzumab by reflecting a regulatory environment that prioritizes cancer innovation.

The neurology segment is estimated to register a CAGR of 12.4% in Europe Biopharmaceuticals Market from 2025 to 2033. This is driven by the increasing prevalence of neurodegenerative and neuroimmunological disorders, coupled with recent breakthroughs in biologic therapies for previously untreatable conditions. The treatment options were largely symptomatic but the advent of disease-modifying biologics has transformed clinical outcomes. Another prominent factor is the growing investment in gene therapies for monogenic neurological disorders is enhancing the segment growth.

REGIONAL ANALYSIS

Germany was the top performer in the European Biopharmaceutical Market by accounting for 22.4% of the share in 2024 due to its largest national economy and a hub for industrial innovation where Germany combines advanced healthcare infrastructure with a dense network of biotech firms and research institutions which fuels the market expansion. This ecosystem is further strengthened by 12 designated biotechnology clusters which includes BioRegio Ruhr and Munich BioCenter where these host over 400 biopharmaceutical enterprises leading to nationwide market expansion. Statutory health insurance covers 90% of the population and routinely reimburses high-cost biologics, including innovative cancer and autoimmune therapies fueling the market.

France was ranked second by occupying 16.2% of the Europe Biopharmaceuticals Market share in 2024. The nation’s prominence arises from its robust public research infrastructure, strong government support for life sciences and strategic geographic which is positioning within Western Europe. France hosts over 700 biotech companies including global players like Sanofi and Servier and has emerged as a leader in vaccine and rare disease therapeutics. Sanofi committed €2.5 billion and later announced an additional €1 billion+ investment, to boost French manufacturing capacity. The government collaborates with Sanofi.

The United Kingdom Biopharmaceuticals Market is lucratively to grow in the coming years. The UK’s enduring influence stems from its world-class academic institutions, concentrated biotech clusters in Cambridge, London, and Oxford, and a historically strong pipeline in oncology and immunology. The significant factor is the UK’s advanced genomics and precision medicine infrastructure. Genomics England has sequenced over 1 million whole genomes as of 2023 by enabling the development of targeted biopharmaceuticals through initiatives like the Newborn Genomes Programme.

Italy Biopharmaceuticals Market is expected to grow in the next coming years. The country’s market is characterized by a growing emphasis on biosimilars, a rising burden of chronic diseases, and expanding participation in pan-European research consortia. Italy hosts over 800 biopharmaceutical firms, with clusters in Milan, Padua, and Naples driving innovation in monoclonal antibodies and cell therapies. A significant driver is the nationwide biosimilar substitution policy and cost-containment strategy. Italy participates in 41 Horizon Europe health projects, including the BEAT-CML consortium developing next-generation tyrosine kinase inhibitors ensuring sustained R&D momentum.

COMPETITIVE LANDSCAPE

The competitive landscape of the Europe Biopharmaceuticals Market is characterized by a blend of established pharmaceutical players and agile biotech innovators escalating for dominance in high-growth therapeutic areas. While multinational corporations like Roche, Novartis, and Sanofi lead in R&D investment and commercial scale the surge in specialized biotech firms particularly in gene therapy, oncology, and autoimmune diseases is reshaping market dynamics. Intense competition is visible in the race to develop next-generation modalities such as bispecific antibodies, ADCs and in vivo gene editing therapies. Regulatory differentiation, speed to market, and real-world evidence generation are becoming prominent competitive levers. Moreover, national disparities in reimbursement and market access create fragmented battlegrounds which prompts companies to adopt region-specific commercial strategies.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe space tourism market include

- Merck & Co., Inc.

- F. Hoffmann-La Roche AG

- Eli Lilly and Company, Inc.

- Sanofi

- Amgen Inc.

- AbbVie Inc.

- Biogen Idec

- Bayer AG

- Johnson & Johnson Services

- Pfizer, Inc.

- Novartis AG

Top Players in the Europe Biopharmaceuticals Market

Roche plays prominent role in Europe’s Biopharmaceutical innovation which is headquartered in Switzerland where it mainly works for oncology, immunology, and neuroscience. The company has pioneered monoclonal antibody therapies such as trastuzumab and rituximab which remain standard-of-care treatments across European healthcare systems. In recent years, Roche has intensified its focus on personalized medicine along with integration of companion diagnostics with biologic therapies to enhance treatment precision. Roche has also expanded its digital pathology partnerships with NHS England and invested in AI-driven drug discovery through its collaboration with UK-based Sensyne Health which is enhnacing its prominence in data-integrated biopharmaceutical development.

Novartis plays a transformative role in the European biopharmaceutical landscape due to its advanced therapies and cardiovascular innovation. The company’s gene therapy Zolgensma, approved for spinal muscular atrophy, has been adopted in 24 European countries which is significantly improving outcomes for pediatric patients. The company launched its Europe-focused Biologics Innovation Hub in Basel dedicated to accelerating ADC and bispecific antibody development.

Sanofi is one of the major players in Europe’s biopharmaceutical sector especially in immunology, rare diseases, and vaccine development. The company’s Dupixent, a fully human monoclonal antibody for atopic dermatitis and asthma has become one of the most prescribed biologics across European dermatology and respiratory clinics. It also strengthened its mRNA vaccine capabilities through a joint venture with BioNTech for pandemic preparedness. Its collaboration with the European Medicines Agency on real-world evidence studies for biologics further enhance its role in shaping regulatory and clinical standards.

Top Strategies Used by Key Market Participants

Key players in the Europe Biopharmaceuticals Market are implementing a range of strategic initiatives to consolidate their growth and accelerate innovation. Major strategies include vertical integration of biomanufacturing to ensure supply chain resilience which is seen in Sanofi’s expansion of mAb facilities. Companies are increasingly engaging in cross-border public-private partnerships such as Roche’s collaboration with academic hospitals on real-world evidence generation. Mergers and acquisitions are being leveraged to access novel platforms, such as Novartis’s acquisition of biotech firms specializing in gene editing. Strategic licensing agreements with mid-sized biotechs enable rapid pipeline expansion while the digital health integrations such as AI-driven target discovery and patient monitoring platforms are enhancing R&D efficiency. The firms are investing in biosimilar portfolios to maintain market presence post-patent expiry ensuring sustained patient access and revenue continuity across therapeutic areas.

RECENT MARKET DEVELOPMENTS

- In January 2023, Roche launched its AI-powered drug discovery center in Munich, Germany, integrating machine learning with high-throughput screening to accelerate the development of novel monoclonal antibodies and bispecifics by enhancing its innovation pipeline across oncology and immunology.

- In May 2023, Novartis acquired Chinook Therapeutics for $3.5 billion is gaining rights to atrasentan and Zigakibart, a targeted biologic for IgA nephropathy is significantly expanding its presence in the renal disease biologics market across Europe.

- In September 2023, Sanofi inaugurated a €1.3 billion in insulin manufacturing facility in Frankfurt, Germany is boosting its in-house biologics production capacity and reducing dependency on external suppliers for key products like Dupixent.

- In June 2024, Bayer announced plans to establish the Berlin Center for Gene and Cell Therapies in partnership with Charité – Universitätsmedizin Berlin. The new center will be substantially financed and supported by Germany's federal government and the state of Berlin with Bayer AG as a minority partner.

MARKET SEGMENTATION

This research report on the European Biopharmaceuticals Market has been segmented and sub-segmented into the following categories.

By Product Type

- Monoclonal Antibodies (mAb)

- Erythropoietin

- Biotech Vaccines

- Recombinant Human (RH) Insulin

- Granulocyte Colony-stimulating Factor (G-CSF)

- Interferon

- Human Growth Hormones (HGH)

By Therapeutic Type

- Neurology

- Infectious Diseases

- Diabetes

- Oncology

- Cardiovascular

- Other Therapeutic Areas

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Biopharmaceuticals Market?

The Europe Biopharmaceuticals Market encompasses the research, development, production, and commercialization of biological drugs derived from living organisms, including monoclonal antibodies, vaccines, recombinant proteins, and gene therapies.

What factors are driving the growth of the Europe Biopharmaceuticals Market?

Growth is fueled by rising chronic disease prevalence, advancements in biotechnology, strong government support for R&D, and increasing demand for targeted and personalized therapies.

Which product segment dominates the European biopharmaceuticals market?

Monoclonal antibodies dominate the market due to their widespread use in treating cancers, autoimmune diseases, and infectious disorders, followed by vaccines and recombinant proteins.

What therapeutic areas drive demand for biopharmaceuticals in Europe?

Key therapeutic areas include oncology, autoimmune diseases, cardiovascular disorders, metabolic conditions, and infectious diseases, with oncology showing the fastest growth.

How does the aging population impact the biopharmaceuticals market?

Europe’s aging population contributes to higher demand for chronic disease treatments, regenerative medicines, and biologic-based therapies, supporting sustained market expansion.

Which countries lead the Europe Biopharmaceuticals Market?

Germany, France, the United Kingdom, Italy, Spain, and Switzerland are key contributors, supported by advanced biotech infrastructure and strong pharmaceutical manufacturing bases.

What challenges are restraining market growth?

Key challenges include high production costs, complex manufacturing processes, stringent regulatory requirements, and limited cold-chain logistics for biologics storage and transport.

How is the regulatory environment influencing market growth?

The European Medicines Agency (EMA) plays a vital role in defining regulatory pathways for biologics and biosimilars, ensuring stringent safety, efficacy, and quality compliance across member states.

What technological advancements are shaping biopharmaceutical production?

Key advancements include single-use bioreactors, continuous manufacturing, automation, and AI-driven quality control, improving scalability and cost efficiency in biologics production.

What is the long-term outlook for the Europe Biopharmaceuticals Market?

The market is poised for steady growth driven by technological innovation, expanding biologics pipelines, favorable government policies, and increased healthcare spending, positioning Europe as a global hub for biopharmaceutical innovation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com