Europe Biostimulants Market Size, Share, Trends & Growth Forecast Report, Segmented By Active Ingredients, Application, Crop Type, and By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Biostimulants Market Size

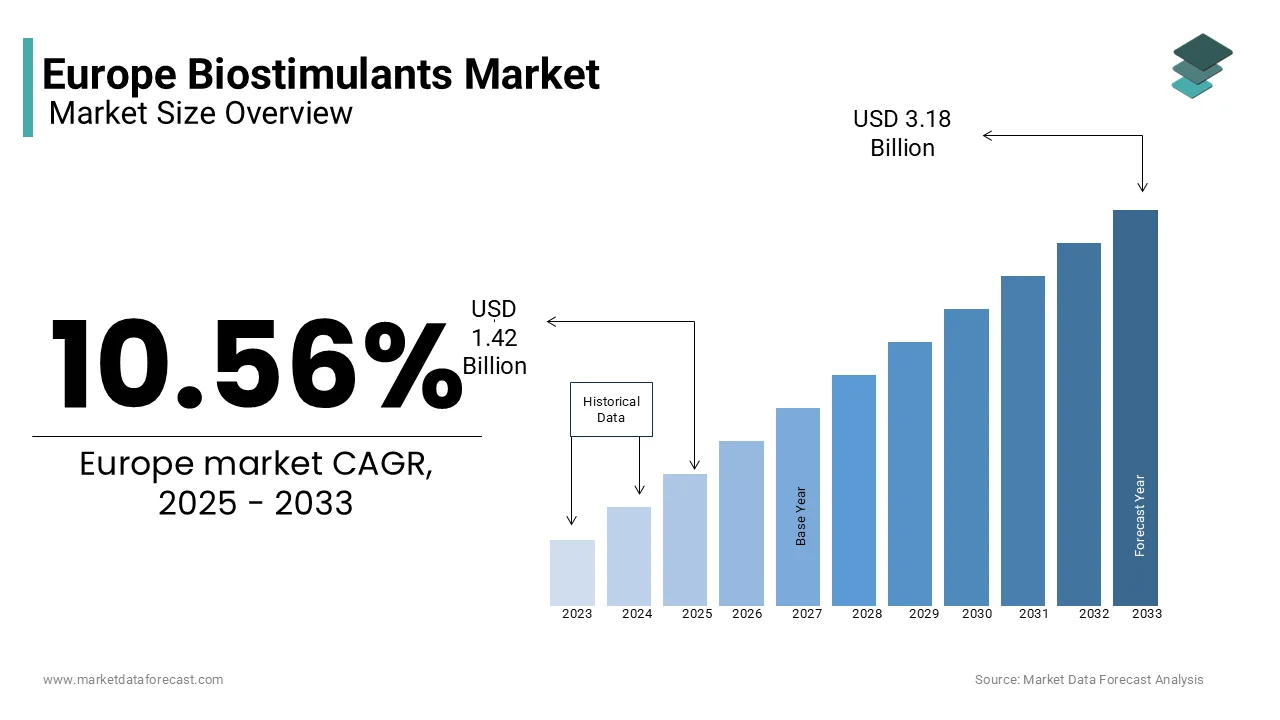

The biostimulants market size in Europe was valued at USD 1.42 billion in 2025 and is anticipated to reach USD 1.57 billion in 2026 from USD 3.50 billion by 2034, growing at a CAGR of 10.56% during the forecast period from 2026 to 2034.

The Biostimulants are plant nutrient efficiency, abiotic stress tolerance, and crop quality without functioning as fertilizers or pesticides. These include seaweed extracts, humic and fulvic acids, amino acids, protein hydrolysate, and beneficial microbes applied via foliar or soil delivery systems. This regulatory clarity has catalyzed innovation in cross-border trade across the European Union.

MARKET DRIVERS

Implementation of the EU Fertilising Products Regulation

The EU Fertilising Products Regulation EU 2019 1009, by providing the first legally binding definition of biostimulants at the Union level, is driving the growth of Europeanrope Biostimulants Market. Before this regulation, biostimulants faced fragmented national rules that hindered scalability and investment. This harmonization reduces compliance costs for manufacturers and accelerates time to market across 27 member states. The regulation also mandates rigorous safety and efficacy documentation,n including data on heavy metals, ls microbial contaminants, and agronomic performance, which enhances product credibility among agronomists and farmers. Furthermore, the CE mark facilitates inclusion in national agricultural advisory programs such as France’s Ecophyto Plan, which now lists CE-certified biostimulants as approved inputs for integrated pest management.

Escalating Pressure to Reduce Synthetic Input Dependency

The European agricultural policy is increasingly oriented toward reducing reliance on synthetic agrochemicals, which directly amplifies demand for biostimulants as complementary or alternative solutions. In response, farmers are adopting integrated nutrient management systems where biostimulants enhance nutrient use efficiency, thereby lowering required fertilizer doses. Similarly, the French National Institute for Agricultural Research reported that seaweed extracts improved phosphorus availability in calcareous soils by, 22% reducing the need for phosphate fertilizers. These agronomic benefits align with national sustainability incentives such as Germany’s Fertiliser Ordinance, which penalizes excess nutrient application.

MARKET RESTRAINTS

Absence of Standardized Efficacy Testing Protocols

The EU fertilising products regulation contends with a gap in standardized efficacy evaluation method, which undermines product comparability and farmer t,t is restraining the groofhe f Europeanrope Biostimulants Market. The regulation mandates proof of agronomic benefit but permits diverse trial designs, soil types, and climatic conditions, leading to inconsistent performance claims. Moreover, the lack of uniform metrics for measuring stress tolerance or nutrient efficiency prevents meta-analyses and hinders meta-regulatory decisions.

Limited Awareness and Technical Knowledge Among Farmers

The insufficient agronomic literacy and advisory support among small and medium-scale farmersexpectedally to further degrade the growth of Europeanrope Biostimulants Market. While large commercial farms in Spain and Italy routinely integrate biostimulants into precision agriculture programs, smaller holdings often lack access to trained advisors who can interpret product labels and tailor application protocols. Consequently, many farmers perceive biostimulants as experimental or cost-prohibitive without understanding their role in input optimization.

MARKET OPPORTUNITIES

Integration into Carbon Farming and Soil Health Initiatives

Biostimulants are gaining strategic relevance within Europe’s emerging carbon farming economy due to their role in enhancing soil organic carbon sequestration and microbial activity. The European Commission’s 2023 Carbon Farming Framework recognizes practices that increase soil carbon stocks as eligible for carbon credits, with biostimulants featuring prominently in approved protocols. These policy linkages transform biostimulants from yield enhancers into climate mitigation tools, creating new revenue streams through voluntary and compliance carbon markets.

Expansion into Protected and Vertical Agriculture Systems

The controlled environment agriculture sector in Europe is rapidly adopting biostimulants to optimize resource use and crop resilience in high-value production systems. Vertical farms, greenhouses, and hydroponic facilities across the Netherlands, Belgium, and Germany increasingly integrate microbial and amino acid-based biostimulants to enhance nutrient uptake under soilless conditions. In vertical farming, where energy and input costs dominate economics, biostimulants that improve photosynthetic efficiency or root development directly impact profitability. Furthermore, the EU’s Horizon Europe program allocated 12 million euros in 2023 to projects developing biostimulants tailored for urban agriculture.

MARKET CHALLENGES

Regulatory Ambiguity Surrounding Microbial Biostimulants

Microbial biostimulants face disproportionate regulatory complexity in Europe due to overlapping frameworks governing plant protection biocides and novel foods, which creates uncertainty for developers. While the EU Fertilising Products Regulation includes microorganisms as a product component, these strains may simultaneously fall under the Biocidal Products Regulation if they exhibit antimicrobial properties or under the Novel Food Regulation if derived from non-traditional sources. In 2023, the European Food Safety Authority issued a scientific opinion stating that 40% of microbial biostimulant applications required additional dossiers under parallel legislation as per its cross-sectoral review.

Inconsistent National Interpretation of EU Harmonized Rules

Despite the EU Fertilising Products Regulation’s intent to create a single market for biostimulants, divergent national interpretations of conformity assessment and post-market surveillance continue to fragment commercialization. A 2023 survey by the European Biostimulants Industry Council found that 61% of companies encountered unexpected national requirements after obtaining CE certification, leading to shipment delays and inventory write-offs. This unpredictability discourages small enterprises from pursuing pan-European distribution and favors large multinationals with regulatory affairs capacity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.56% |

| Segments Covered | By Active Ingredients, Application, Crop Type, and Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Balkans & Rest of Europe |

| Market Leaders Profiled | BASF SE, Biostadt India Limited, Valagro SpA, Novozymes A/S, Biolchim SpA, Isagro SpA, and Koppert B.V. |

SEGMENT ANALYSIS

By Active Ingredients Insights

The seaweed extracts segment held 31.2% ofEuropeanurope biostimulants Market share in 2025 due to their multifunctional bioactive compounds, including alginates, laminarin, and betaines that enhance plant growth, stress tolerance, and nutrient uptake. Seaweed-based products are particularly effective in Mediterranean climates where water scarcity and salinity challenge crop productivity. Furthermore, over 80 CE-marked biostimulants containing seaweed extracts are listed in the EU Fertilising Products Register according to the European Biostimulants Industry Council, reflecting strong industry adoption.

The protein hydrolysates segment is likely to grow with an expected CAGR of 12.8% during the forecast period. Derived from plant or animal sources through enzymatic hydrolysis, these mixtures of peptides and free amino acids act as chelating agents and signaling molecules that stimulate root development and photosynthetic activity. The EU Fertilising Products Regulation classifies them under Component Material Category 6, enabling streamlined CE certification with over 45 protehydrolysate-based products approved as of 2024 according to the European Commission’s register.

By Application Insights

The foliar application segment was the largest and held 48.3% of Europeanrope biostimulants Market share in 2024, with a focus on high-value horticulture where precision and rapid effect are significant. In Southern Europe, foliar biostimulants are routinely used during flowering and fruit set to improve pollination and reduce flower drop under heat stress. National advisory services in Spain and Italy actively promote foliar biostimulant use in integrated production protocols, with over 60% of extension bulletins referencing them for stress mitigation. This combination of agronomic immediacy,cy equipment reading, and institutional endorsement sustains foliar application as the dominant delivery method.

The seed treatment segment is likely to grow with an anticipated CAGR of 11.5% during the forecast period, with the rise of precision planting and early-season stress resilience strategies. Coating seeds with humic substances or microbial consortia primes germination vigor and root establishment under suboptimal conditions, such as cold soils or drought. This trend is amplified by the EU’s Sustainable Use of Pesticides Regulation,n which encourages non-chemical seed treatments to reduce fungicide dependency.

By Crop Insights

The fruits and vegetables segment accounted in holding 42.3% of Europeanrope biostimulants Market share in 2024 due to their high economic value, sensitivity to environmental stress, and stringent quality standards that favor biological inputs. Growers of tomatoes, grapes, strawberries, and leafy greens routinely use biostimulants to enhance color uniformity, shelf life, and sugar content while reducing physiological disorders.

The cereals and oilseeds segment is expected to register a CAGR of 10.9% during the forecastperiodf with the policy mandates to reduce synthetic input use in staple crops. The EU’s Farm to Fork Strategy targets a 20% reduction in fertilizer use by 2030, which has prompted large-scale cereal farmers to adopt biostimulants for nitrogen and phosphorus use efficiency. Similarly, in France, the Ecophyto Plan II encourages biostimulant use in oilseed rape to improve establishment under variable autumn conditions, with over 300000 hectares treated in 2023 according to FranceAgriMer. The economic viability of biostimulants in extensive crops has improved due to bulk formulation and compatibility with existing spraying equipment. Additionally, the EU’s Common Agricultural Policy now links direct payments to sustainable practice, including biological input use, which incentivizes adoption among subsidy-dependent cereal growers.

COUNTRY ANALYSIS

Spain Biostimulants Market Analysis

Spain was the top performer of Europeanrope Biostimulants Market with 24.2% of share in 2024, with its extensive horticultural sector water scarcity challenges and early adoption of sustainable intensification practices. Over 70% of Spain’s biostimulant use occurs in fruit and vegetable production, particularly in the Murcia and Almería regions, where intensive greenhouse farming dominates. Consequently, seaweed extracts and amino acids are routinely applied to maintain yields under heat and salinity stress. Spain also hosts several major biostimulant manufacturers, including Bioiberica, which supplies products across the EU.

France Biostimulants Market Analysis

France held 19.2% of Europeanrope biostimulants Market share in 2024. The national Ecophyto Plan, which aims to halve pesticide use, has expanded to include biostimulants as approved inputs for integrated crop management, with over 45 products listed in the official registry as confirmed by the French Agency for Food, Environmental and Occupational Health and Safety. Public research institutions such as INRAE have published over 60 peer-reviewed studies on biostimulant efficacy since 2020, validating their role in nutrient efficiency and stress tolerance. Adoption is widespread in viticulture and arable farming, with 38% of cereal farmers using biostimulants in 20,23, according to FranceAgriMer.

Italy Biostimulants Market Analysis

Italy's biostimulants market growth is likely to have a significant CAGR during the forecast period, with its premium fruit and wine sectors that prioritize quality and sustainability. The Italian National Research Council has demonstrated that foliar amino acids improve polyphenol content in Sangiovese grapes by 18% by enhancing wine typicity. Italy also hosts a vibrant domestic biostimulant industry with companies like Valagro and Italpollina exporting globally.

Germany Biostimulants Market Analysis

Germany's Biostimulants Market growth is likely to grow with its focus on cereals, oilseed, and scientific rigor in product evaluation. The Julius Kühn Institute maintains a national biostimulant efficacy database evaluating over 90 products annually, with results disseminated through the official agricultural advisory network. Germany also leads in regulatory compliance, with all major biostimulant suppliers obtaining CE marking under the EU Fertilising Products Regulation.

COMPETITIVE LANDSCAPE

European biostimulants Market features a competitive landscape shaped by scientific credibility, regulatory agility, and agronomic relevance rather than price alone. It includes multinational agrochemical firms leveraging existing distribution networks alongside specialized European biostimulant companies with deep regional expertise. Competition is intensifying as boundaries blur between biostimulants, ts biocontrol, and traditional inputs, prompting cross-segment innovation. Differentiation hinges on robust field validation under local conditions, transparent sourcing, and seamless integration into farm management systems. The harmonized EU regulatory framework has lowered entry barriers but raised evidence standards, favoring companies with strong R and D capabilities.

KEY MARKET PLAYERS

A few of the market players in Europeanrope biostimulants market include

- BASF SE

- Biostadt India Limited

- Valagro SpA

- Novozymes A/S

- Biolchim SpA

- Isagro SpA

- Koppert B.V.

Top Players In The Market

- BASF SE is a global leader in agricultural solutions with a robust biostimulants portfolio anchored in its Plant Science division. The company offers seaweed-based and amino acid formulations tailored for European crops under brands like Nova and Lormax. BASF has invested heavily in field validation across diverse agroclimatic zones, collaborating with research institutions in France and Spain to generate localized efficacy data. In 2023, it expanded its biostimulant production capacity at its Ludwigshafen facility to meet rising EU demand and integrated its products into digital farming platforms like Xarvioo for precision application.

- Valagro SpA, headquartered in Italy, is a pioneer in biostimulant innovation with a legacy of over four decades in developing protein hydrolysates and seaweed extracts. The company operates a state of the art R and D center in Atessa and maintains a strong presence across Southern and Central Europe. Valagro actively contributed to the development of the EU Fertilising Products Regulation by participating in industry working groups.

- Koppert Biological System, based in the Netherlands, has strategically expanded from biocontrol into biostimulants through its Trianum and Natupol lines, enhanced with microbial synergists. The company leverages its extensive greenhouse grower network to deploy integrated biological solutions combining biostimulants with beneficial microbes. Koppert collaborates closely with Wageningen University on soil health trials and has developed proprietary formulations for protected cultivation systems prevalent in the Benelux and Germany. In 2023, it introduced a fulvic acid-based root stimulant specifically designed for hydroponic lettuce production, which is now used by over 120 vertical farms across Europe.

Top Strategies Used By The Key Market Participants

Key players in the European biostimulants Market prioritize regulatory compliance by securing CE marking under the EU Fertilising Products Regulation to ensure pan-European market access. They invest in localized field trials across diverse agroclimatic zones to generate credible efficacy data for agronomists and farmers. Strategic partnerships with seed companies, equipment manufacturers, and digital farming platforms enable integrated product delivery. Companies also expand production capacity within the EU to reduce supply chain risks and meet sustainability criteria.

RECENT MARKET NEWS

- In March 2023, BASF SE launched a line of seaweed-based biostimulants, designed to cater to the growing demand for organic farming solutions.

- In June 2023, Valagro SpA partnered with agricultural cooperatives to promote its microbial biostimulants, achieving a 15% increase in sales.

- In January 2024, Adama Agricultural Solutions Ltd. acquired a startup specializing in crop-specific biostimulants, aiming to expand its precision agriculture portfolio.

- In September 2023, Biolchim collaborated with research institutions to integrate biostimulants into regenerative farming practices, enhancing efficiency.

- In November 2023, Koppert Biological Systems invested €300 million in expanding its microbial biostimulant production facilities, focusing on sustainable agriculture.

MARKET SEGMENTATION

This research report on Europeanrope biostimulants market is segmented and sub-segmented into the following categories.

By Active Ingredients

- Fulvic Acid

- Protein Hydrolysates

- Seaweed Extracts

- Amino Acid

- Humic Acid

- Others

By Application

- Seed

- Foliar

- Soil

By Crop Type

- Fruits & Vegetables

- Cereals & Oilseeds

- Turfs & Ornaments

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of the Europe biostimulants market?

Increasing demand for organic farming, sustainable agriculture practices, and government support for eco-friendly products.

Which countries lead the biostimulants market in Europe?

Major markets include Spain, Italy, France, Germany, and the UK, driven by advanced agricultural practices.

What are the main types of biostimulants used in Europe?

Key types include humic substances, seaweed extracts, microbial biostimulants, amino acids, and protein hydrolysates.

Which sectors benefit the most from biostimulants?

Crop production (fruits, vegetables, cereals), horticulture, and turf management see the highest adoption rates.

What challenges does the European biostimulants market face?

Regulatory complexities, lack of standardization, and limited farmer awareness remain significant barriers to growth.

What are biostimulants, and why are they gaining traction in Europe?

Biostimulants are substances or microorganisms that enhance plant growth, nutrient uptake, and stress tolerance—without directly providing nutrients. Their adoption is surging in Europe due to the EU’s Farm to Fork Strategy, which promotes reduced chemical inputs and sustainable farming.

Which types of biostimulants dominate the European market?

Seaweed extracts, humic and fulvic acids, amino acids, and microbial biostimulants (e.g., mycorrhizal fungi, rhizobacteria) lead the market, valued for improving soil health and crop resilience under organic and conventional systems.

How does EU regulation affect biostimulant classification and sales?

Since 2022, the EU Fertilising Products Regulation (EU 2019/1009) has created a harmonized framework, allowing CE-marked biostimulants to move freely across member states—accelerating innovation and market access for compliant products.

Are organic and conventional farmers both using biostimulants?

Yes—organic growers rely on them as approved inputs, while conventional farmers use them to reduce synthetic fertilizer dependency and meet sustainability KPIs demanded by food retailers and policymakers.

Which countries are leading in biostimulant adoption in Europe?

Spain, Italy, France, the Netherlands, and Germany lead due to intensive horticulture, vineyards, and strong agri-tech ecosystems, supported by national subsidies for sustainable inputs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com