Europe Cattle Feed Market Size, Share, Trends & Growth Forecast Report – Segmented By Ingredient Type, Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$26.59 BnMarket Estimate, 2026

$27.56 BnMarket Forecast, 2034

$36.71 BnCAGR, 2026–2034

3.65%Europe Cattle Feed Market Report Summary

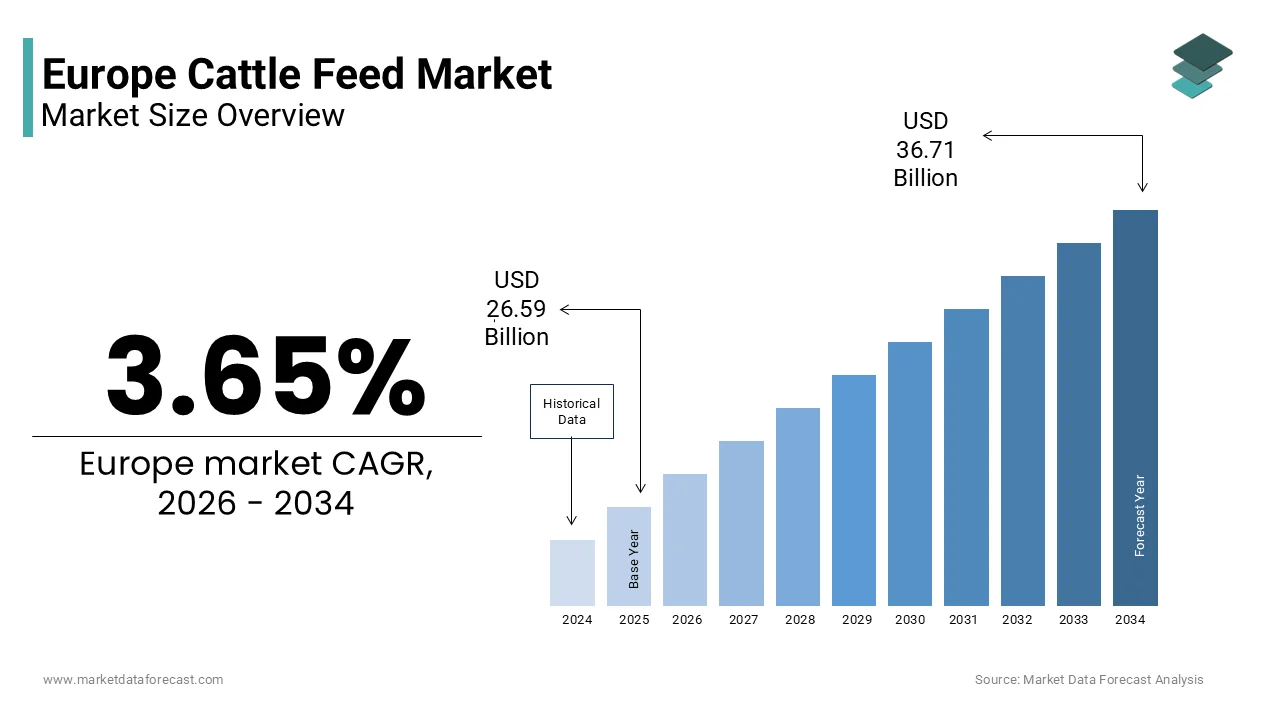

The Europe cattle feed market was valued at USD 26.59 billion in 2025 and is projected to reach USD 36.71 billion by 2034, growing at a CAGR of 3.65% during the forecast period. Market growth is supported by rising demand for high quality dairy and meat products, increasing focus on livestock productivity, and the adoption of scientifically formulated feed solutions to improve animal health and yield. Expanding commercial dairy farming, advancements in feed additives, and growing awareness regarding balanced nutrition for cattle are further contributing to the steady expansion of the Europe cattle feed market.

Key Market Trends

- Growing emphasis on nutritionally balanced feed formulations to enhance milk yield and meat quality.

- Rising adoption of feed additives such as probiotics, enzymes, and vitamins to improve digestion and immunity in cattle.

- Increasing demand for sustainable and organic feed ingredients aligned with European environmental and animal welfare regulations.

- Technological advancements in feed processing and precision livestock farming to optimize feed conversion ratios.

- Expansion of commercial dairy operations across major European economies supporting consistent feed demand.

Segmental Insights

- Based on ingredient type, the cereals and grains segment accounted for 48.2% of the Europe cattle feed market share in 2024. The dominance of this segment is attributed to the high energy content, cost effectiveness, and widespread availability of cereals and grains, making them a primary component in cattle feed formulations.

- Based on application, the dairy cattle segment held 24.3% of the Europe cattle feed market share in 2024. The segment’s leading position is driven by strong dairy production across Europe, increasing milk consumption, and the need for specialized feed to enhance lactation performance and overall herd health.

Regional Insights

- Germany was the largest contributor to the Europe cattle feed market, capturing 21.3% of the market share in 2024. The country’s leadership is supported by its robust dairy and meat production industry, well established feed manufacturing sector, and strong emphasis on livestock productivity and quality standards.

- Other European countries are witnessing stable growth due to expanding dairy farming operations, supportive agricultural policies, and increasing investments in animal nutrition research.

Competitive Landscape

The Europe cattle feed market is highly competitive, with multinational agribusiness companies and regional feed manufacturers focusing on product innovation, nutritional optimization, and sustainable sourcing practices. Companies are investing in research and development to introduce advanced feed additives and improve feed efficiency. Strategic collaborations, acquisitions, and expansion of production facilities are key approaches adopted by market participants to strengthen their regional presence.

Prominent players in the Europe cattle feed market include De Heus Animal Nutrition, United Farmers Cooperative, Farmers Grain, Land O Lakes, Nutreco, Biomin, Kemin Industries, Godrej, Cargill, DSM, Archer Daniels Midland Company, and BASF SE.

Europe Cattle Feed Market Size

The Europe cattle feed market size was valued at USD 26.59 billion in 2025 and is projected to reach USD 36.71 billion by 2034 from USD 27.56 billion in 2026, growing at a CAGR of 3.65%.

The cattle feed is a formulated nutritional product designed to support the health productivity and welfare of dairy and beef cattle. These feeds typically consist of energy sources, such as cereals protein meals like rapeseed or soy derivatives essential minerals vitamins and increasingly functional additives including probiotics enzymes and phytogenics. The composition is strictly governed by EU feed safety regulations under Regulation EC No 767/2009, which mandates traceability labeling and bans on specified risk materials. According to Eurostat, the European Union was home to approximately 87 million head of cattle in 2024 with dairy cows accounting for nearly 23 million animals primarily concentrated in Germany, France, and the Netherlands. As per the European Commission’s Farm to Fork Strategy feed efficiency and methane reduction have become central policy objectives driving reformulation toward low emission diets. This regulatory and biological complexity defines the modern European cattle feed landscape where nutritional science intersects with sustainability mandates and animal welfare standards.

MARKET DRIVERS

Stringent EU Policies Promoting Low Methane Livestock Diets

The European Union’s aggressive climate agenda has positioned cattle feed as a critical lever for reducing agricultural greenhouse gas emissions particularly enteric methane from ruminants. The stringent EU policies promoting low metane livestock diets is major factor propelling the growth of the Europe cattle feed market. As per the European Commission’s 2023 Implementing Decision on Climate Neutrality in Agriculture, livestock accounts for 53% of the sector’s non-CO2 emissions with dairy and beef cattle contributing over 80% of that total. In response, the EU authorized the first methane inhibiting feed additive, 3 nitrooxypropanol in 2022, following extensive review by the European Food Safety Authority which confirmed a 30% average reduction in methane per lactating cow without adverse health effects. By early 2024, over 12000 dairy farms across Germany, Denmark, and the Netherlands had adopted this additive through cooperative feed programs. Additionally, the Horizon Europe funded RUMENET project demonstrated that integrating seaweed derived bromoform into feed at 0.5% inclusion reduced methane by up to 42% in controlled trials. National schemes, such as Ireland’s Agricultural Sustainability Support and Advisory Programme, now provide subsidies for approved methane reducing feed supplements. These policy driven incentives are transforming cattle feed from a commodity input into a climate mitigation tool accelerating adoption across commercial dairies.

Rising Demand for High Quality Dairy and Beef Products Linked to Feed Composition

The consumer preference for premium animal protein with verified welfare and nutritional profiles is compelling producers to invest in advanced cattle feed formulations. The rising demand for high quality dairy and beef products is accelerating the growth of Europe cattle feed market. According to the European Consumer Organisation, many EU shoppers consider animal diet a key factor when purchasing milk or meat with grass fed pasture raised and omega-3 enriched labels commanding price premiums of 15 to 35%. This demand is reinforced by retailer commitments, for instance Aldi’s 2023 Sustainable Sourcing Charter requires all private label dairy suppliers to disclose feed composition and limit soy content to certified deforestation free sources. In France, the Label Rouge certification mandates that beef cattle receive forage-based diets supplemented with regionally sourced cereals with a standard met by specialized compound feeds. The German Federal Ministry of Food and Agriculture reported that farms using omega 3 fortified feed saw an increase in milk premiums due to elevated conjugated linoleic acid levels.

MARKET RESTRAINTS

Persistent Volatility in Global Feed Ingredient Prices

The cost instability due to its reliance on imported protein meals and cereals subject to geopolitical and climatic disruptions is limiting the growth of Europe cattle feed market. According to the European Commission’s Short-Term Outlook for Arable, soybean meal prices surged by 38% between January and August 2023, following droughts in Argentina and export restrictions from Brazil. Similarly, the war in Ukraine disrupted sunflower meal supplies which previously accounted for 18% of EU protein feed blends as per Copa Cogeca data. In Spain, over 12000 cattle farms reduced herd sizes in 2023 due to unsustainable feed costs, according to the Ministry of Agriculture. While forward contracting and co-operative pooling offer partial hedging these mechanisms remain inaccessible to small scale producers. This structural vulnerability constrains consistent investment in high performance feed technologies.

Regulatory Restrictions on Conventional Growth Promoters and Antibiotics

The ban on antibiotic growth promoters coupled with tightening rules on zinc and copper usage has limited formulation flexibility for cattle feed producers, which is additionally degrading the growth of Europe cattle feed market. As per Regulation EC No 1831/2003, only feed additives with proven safety and efficacy may be authorized with regular re-evaluations leading to withdrawals. In 2022, the European Medicines Agency recommended phasing out high zinc oxide use in all livestock due to environmental accumulation concerns although this primarily affects swine it heightened scrutiny across species. More critically the European Food Safety Authority’s 2023 guidance emphasized minimizing copper in ruminant feeds to prevent soil contamination with several member states including the Netherlands imposing upper limits of 15 milligrams per kilogram. These constraints force nutritionists to rely on more expensive alternatives such as organic trace minerals yeast derivatives and phytogenic compounds. A 2024 survey by the European Federation of Feed Compounders found that some members reported formulation challenges in maintaining performance parity without conventional tools.

MARKET OPPORTUNITIES

Expansion of Precision Feeding Technologies and Digital Nutrition Platforms

The integration of digital tools and sensor-based monitoring is enabling unprecedented customization in cattle feed delivery creating new value streams for feed companies. The integration of precision feeding technologies and digital nutrition platforms is significantly boosting the growth of Europe cattle feed market. Precision feeding systems that adjust ration composition in real time based on individual cow data are gaining traction across Northern Europe. According to the Dutch Ministry of Agriculture, dairy farms with more than 100 cows now use automated feed pushers linked to milking robots that tailor concentrate allocation based on yield health and stage of lactation. Companies like Lely and DeLaval offer cloud-based nutrition platforms that analyze rumination activity body condition and milk composition to recommend daily feed adjustments. In Germany, the Fraunhofer Institute piloted an AI driven feed optimization model in 2024 that reduced nitrogen excretion, while maintaining milk output by dynamically balancing crude protein levels. These technologies not only enhance efficiency but also generate verifiable sustainability metrics required under emerging carbon credit and eco-labeling schemes thereby transforming feed from a bulk input into a data enabled service.

Development of Alternative Protein Sources from Circular Bioeconomy Streams

The EU’s push for feed protein autonomy is prompting innovation in novel ingredients derived from food waste insect biomass and microbial fermentation is additionally fuelling the growth of Europe cattle feed market. As per the European Commission’s Protein Plan, Europe imports 70% of its feed protein primarily soy creating strategic vulnerability. In response, the EU authorized the use of processed animal protein from cattle feed and pigs in ruminant feed in 2023 under strict segregation protocols opening a potential supply of 1.2 million metric tons annually, according to FEFAC estimates. Simultaneously, insect meal from black soldier fly larvae is emerging as a viable alternative, where Protix’s facility in the Netherlands produces with protein digestibility matching fishmeal. The European Food Safety Authority confirmed in 2024 that single cell protein from hydrogen oxidizing bacteria meets safety standards for cattle feed with trials showing comparable weight gain to soy-based diets. National initiatives such as France’s “Feed Autonomy Pact” provide grants covering capital costs for on farm protein production units. These circular solutions not only reduce import dependency but also align with Farm to Fork objectives by valorizing organic residues and lowering land use pressure.

MARKET CHALLENGES

Fragmented Regulatory Frameworks Across Member States

The harmonization significant disparities in national implementation of feed regulations create operational complexity for cross border feed producers, which is one of the challenges for the growth of Europe cattle feed market. While Regulation EC No 767/2009 establishes baseline requirements member states retain authority over enforcement interpretations and permitted additives. For example, Germany’s Federal Office of Consumer Protection restricts certain mycotoxin binders allowed in France under ANSES approval leading to formulation inconsistencies for multinational feed mills. Such fragmentation increases compliance costs with companies often maintaining multiple product variants for different sectors. A survey by FEFAC revealed that feed compounders spend huge amount annually on regulatory adaptation and documentation. Moreover, delays in mutual recognition of novel feed approvals, such as the 14-month gap between EFSA authorization and national listing in Southern Europe.

Limited Adoption of Advanced Feeds Among Small Scale and Extensive Producers

A substantial portion of Europe’s cattle population is managed by small scale or pasture-based operations that lack the infrastructure or economic incentive to adopt specialized compound feeds. The limited adoption of advanced feeds among small scale and extensive producers is alkso to decline the growth of Europe cattle feed market. These systems prioritize low input extensive management where purchased feed represents a marginal cost rather than a performance driver. The European Environment Agency notes that while such farms contribute to biodiversity and landscape preservation they exhibit minimal engagement with precision nutrition or methane reducing additives due to cost barriers and technical knowledge gaps. In Italy, only few beef farms with under 30 animals use formulated supplements instead on farm cereal leftovers. Extension services remain underfunded; the European Commission reported that only some rural development programs include dedicated feed advisory components. Consequently, innovations in cattle feed are largely confined to intensive dairy clusters leaving a significant segment of the bovine population outside the reach of nutritional advancements despite their collective environmental footprint.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.65% |

| Segments Covered | By Ingredient Type, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | De Heus Animal Nutrition, United Farmers Cooperative, Farmers Grain, Land O Lakes, Nutreco, Biomin, Kemin Industries, Godrej, Cargill, DSM, Archer Daniels Midland Company, and BASF SE |

SEGMENTAL ANALYSIS

By Ingredient Type Insights

The cereals and grains constitute segment was accounted on holding 48.2% of the Europe cattle feed market share in 2024 with their role as primary energy sources in ruminant diets for high yielding dairy cows requiring substantial metabolizable energy to sustain milk production. Barley, wheat, maize, and triticale, are widely used due to their starch content fermentability and regional availability. According to Eurostat, the European Union harvested over 290 million metric tons of cereals in 2023 with nearly 35% allocated to animal feed. Germany alone utilized 18.7 million metric tons of barley and wheat in compound feed production, as per the German Federal Ministry of Food and Agriculture. The Common Agricultural Policy further incentivizes on farm use of homegrown cereals through coupled support schemes reducing reliance on imported protein sources. Additionally, cereals serve as effective carriers for additives and minerals ensuring uniform distribution in total mixed rations. Their established supply chains price stability relative to protein meals and compatibility with existing feeding infrastructure solidify their foundational role in European cattle nutrition strategies.

The additives segment is projected to grow at a CAGR of 7.2% from 2025 to 2033 with the expanding ingredient category in the European cattle feed market. The growth of the segment is driven by the regulatory pressure to reduce antibiotic use and methane emissions alongside rising demand for performance enhancing and welfare focused solutions. As per the European Food Safety Authority, over 120 feed additives were authorized for ruminants in 2024, including probiotics enzymes phytogenics and methane inhibitors. Additionally, the European Commission’s Farm to Fork Strategy mandates a 50% reduction in antimicrobial sales for livestock by 2030 spurring investment in alternatives, such as yeast cell wall derivatives, which trials show improve gut health and reduce pathogen colonization. In France, the National Institute for Agricultural Research reported a 28% increase in additive inclusion rates in commercial dairy rations between 2022 and 2024. These functional ingredients not only address compliance but also enable premium product claims linked to animal welfare and environmental stewardship.

By Application Insights

The dairy cattle segment was the largest by holding 24.3% of the Europe cattle feed market share in 2024 by the intensive nutritional demands of high yielding herds. The average EU dairy cow produces over 8500 kilograms of milk annually according to the European Commission requiring precise energy protein and mineral balance to maintain productivity and health. Germany with 4.2 million dairy cows and the Netherlands with 1.6 million operate some of the world’s most productive systems where total mixed rations are standard practice. As per the European Dairy Association, over 90% of commercial dairies utilize compound feed supplements to bridge nutrient gaps left by forage alone. Furthermore, EU quality schemes such as Protected Designation of Origin for cheeses often mandate specific feeding protocols that influence concentrate composition. This combination of biological necessity economic pressure and regulatory linkage ensures sustained dominance of dairy cattle in feed consumption patterns across the continent.

The calves segment is lucratively growing at a fastest CAGR of 6.8% throughout the forecast period with the early life nutrition to improve lifetime productivity and reduce antimicrobial dependency. Scientific consensus now affirms that the first eight weeks of life critically determine mammary development immune competence and feed efficiency in adulthood. As per the European Federation of Animal Science, trials demonstrate that calves receiving optimized starter feeds with digestible protein and bioactive additives achieve higher first lactation yields. The European Medicines Agency’s 2023 guidelines restrict prophylactic antibiotic use in youngstock prompting widespread adoption of prebiotics organic acids and immunoglobulin enriched feeds. In Denmark, the CalfCare national program reported a slight decline in neonatal diarrhea after mandating high quality milk replacers and textured starter grains on all registered farms. Similarly, the UK’s Agriculture and Horticulture Development Board launched a calf nutrition benchmarking initiative in 2024 linking feed quality to subsidy eligibility. These science-based welfare policies and long term economic incentives are transforming calf feeding from a cost center into a strategic investment driving rapid segment growth.

REGIONAL ANALYSIS

Germany Cattle Feed Market Analysis

Germany was the largest contributor of the European cattle feed market by capturing 21.3% of share in 2024 with its position as the continent’s top dairy producer and home to advanced feed manufacturing infrastructure. The German Feed Industry Association reports that over 24 million metric tons of compound feed were produced in 2023 with cattle formulations representing 42% of the total. Stringent national standards under the German Feed Ordinance require full traceability and batch testing for mycotoxins and contaminants reinforcing demand for high quality ingredients. Additionally, Germany leads in methane reducing feed adoption with the “Climate Smart Dairy” initiative co-funded by the Ministry of Agriculture. The presence of global feed additive companies like EW Nutrition and Dr Eckel further strengthens innovation capacity. This blend of scale regulation and technological readiness cements Germany’s leadership in the European cattle feed landscape.

France Cattle Feed Market Analysis

France cattle feed market was ranked second by occupying 16.8% of share in 2024 with its diverse cattle systems ranging from intensive dairy in Brittany to extensive beef in the Massif Central. The French feed industry produced 18.3 million metric tons of compound feed in 2023 with significant regional variation in formulation based on local crop availability. The government’s “Protein Plan” actively promotes rapeseed sunflower and legume integration to reduce soy dependency aligning with EU protein autonomy goals. In 2024, the National Institute for Agricultural Research launched the RumiFeed project demonstrating that regionally sourced pea and faba bean blends can replace imported soy without compromising weight gain in Charolais calves. France’s Label Rouge certification requires strict feeding protocols that drive demand for premium non-GMO feeds. This dual focus on self-sufficiency and quality differentiation positions France as a pivotal and multifaceted player in the European feed market.

Netherlands Cattle Feed Market Analysis

The Netherlands cattle feed market growth is likely to be driven by its ultra intensive dairy sector and world class feed innovation ecosystem. Dutch feed mills produce over 9 million metric tons of compound feed yearly with cattle formulations emphasizing precision nutrition and methane mitigation. The Dutch Dairy Association mandates that all participating farms use feed additives proven to reduce enteric methane with a policy accelerating adoption of 3 nitrooxypropanol and seaweed derivatives. Wageningen University collaborates with companies like Nutreco and ForFarmers on next generation feeds incorporating insect protein and single cell biomass. Additionally, the Netherlands serves as a logistics hub importing raw materials via Rotterdam and exporting specialized feed premixes, across Europe. This emergence of scientific excellence regulatory foresight and trade infrastructure makes the Netherlands a disproportionate influencer in shaping future feed standards.

United Kingdom Cattle Feed Market Analysis

The United Kingdom cattle feed market growth is steadily growing with the enhance feed self-reliance and animal health resilience. The Agriculture Act 2020 introduced the Sustainable Farming Incentive which rewards farmers for using feed that reduces ammonia and methane emissions. In 2024, over 3200 farms enrolled in the scheme adopted low crude protein rations supplemented with protected amino acids and tannin rich forages. The UK also leads in calf nutrition research with the Royal Veterinary College demonstrating that early life feeding protocols can reduce lifetime antibiotic use by up to 40%. Feed producers, such as ABN and Wynnstay have launched carbon footprint labeled products enabling traceability from field to trough. These policy driven innovations position the UK as a testbed for outcome-based feed systems aligned with net zero agriculture ambitions.

Italy Cattle Feed Market Analysis

Italy cattle feed market growth is significantly to have prominent opportunities with its dual focus on high value dairy for cheese production and extensive beef grazing in southern regions. The country’s 3.8 million dairy cows primarily located in Lombardy and Emilia Romagna produce milk for Parmigiano Reggiano and Grana Padano, which require strict feeding protocols prohibiting silage and limiting soy. Meanwhile, southern beef systems are gradually adopting supplementary concentrates to improve carcass quality under the National Rural Development Program. Italy’s unique blend of tradition driven formulation and modern safety investments creates a resilient and segmented feed demand structure that balances heritage with innovation.

COMPETITIVE LANDSCAPE

The Europe cattle feed market features a competitive landscape dominated by large integrated nutrition companies alongside regional cooperatives and specialized premix producers. Competition is increasingly defined by technical expertise sustainability credentials and digital capabilities rather than price alone. Major players leverage extensive R&D networks to develop methane reducing additives gut health solutions and low emission formulations that align with EU regulatory mandates. Regional cooperatives maintain strong farmer relationships and local grain sourcing advantages particularly in France Germany and the Nordic countries. Regulatory complexity under REACH and feed hygiene regulations creates high entry barriers favoring established firms with robust compliance systems. Innovation in alternative proteins and circular feed ingredients is intensifying as companies seek to address soy dependency and land use concerns. Customer loyalty is reinforced through advisory services precision feeding tools and outcome based contracts linking feed performance to milk yield or health metrics.

KEY MARKET PLAYERS

Some of the notable key players in the Europe cattle feed market are

- De Heus Animal Nutrition

- United Farmers Cooperative

- Farmers Grain

- Land O Lakes

- Nutreco

- Biomin

- Kemin Industries

- Godrej

- Cargill

- DSM

- Archer Daniels Midland Company

- BASF SE

Top Players in the Market

- For Farmers Group is a leading European animal nutrition company headquartered in the Netherlands with extensive operations across Germany, Belgium, France, and the United Kingdom. The company supplies tailored cattle feed solutions to both dairy and beef producers emphasizing sustainability traceability and performance optimization. For Farmers actively integrates circular economy principles by utilizing co products from food and biofuel industries such as brewers grains and rapeseed meal. The company launched its “FeedPrint” digital platform which calculates the carbon footprint of each ration enabling farmers to align feeding practices with EU climate targets. It also expanded its methane reducing feed portfolio following regulatory approval of novel additives in key markets reinforcing its commitment to science based nutritional innovation.

- Nutreco NV a Dutch multinational specializing in animal and aquafeed operates under the Trouw Nutrition brand in the ruminant sector delivering advanced cattle feed premixes and specialty ingredients globally. The company leverages its R&D centers in Spain and the Netherlands to develop gut health solutions probiotics and methane mitigation technologies. Nutreco has prioritized antimicrobial reduction through its “Feed for Health” initiative which promotes alternatives like organic acids and phytogenics. Nutreco partnered with major dairy cooperatives in Germany and Denmark to deploy precision feeding systems that adjust nutrient delivery based on real time cow data thereby enhancing efficiency and reducing environmental impact across commercial herds.

- Cargill Animal Nutrition Europe provides comprehensive cattle feed formulations and advisory services across the continent with strong presence in the UK, France, Italy, and Eastern Europe. The company combines global ingredient sourcing with localized nutritional expertise to address regional challenges such as mycotoxin contamination and protein shortages. Cargill has invested heavily in digital tools including its “DairyBeef Advisor” platform which offers herd specific feed recommendations using machine learning. The company inaugurated a new innovation center in Belgium focused on alternative proteins and low emission diets supporting EU Farm to Fork objectives.

Top Strategies Used by the Key Market Participants

Key players in the Europe cattle feed market pursue strategies centered on sustainability compliance digital integration and ingredient innovation. Companies are reformulating feeds to reduce methane and ammonia emissions in alignment with EU climate policies while maintaining animal performance. Investment in digital nutrition platforms enables precision feeding and carbon footprint tracking meeting both regulatory and consumer demands. Vertical integration with secure sourcing of alternative proteins such as insect meal and microbial biomass reduces dependency on imported soy. Strategic partnerships with dairy cooperatives and veterinary networks facilitate rapid adoption of antimicrobial free solutions. Additionally, firms are enhancing traceability through blockchain and batch level monitoring to comply with stringent EU feed safety regulations. These approaches collectively strengthen competitive positioning by transforming feed from a commodity into a value-added service linked to environmental and animal welfare outcomes.

MARKET SEGMENTATION

This research report on the European cattle feed market has been segmented and sub-segmented based on categories.

By Ingredient Type

- Protein Meals or Cakes

- Cereals and Grains

- Brans

- Additives

- Others

By Application

- Beef Cattle

- Dairy Cattle

- Calves

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is cattle feed?

Cattle feed refers to formulated nutritional products designed to meet the dietary requirements of dairy and beef cattle. It typically includes forage, concentrates, protein meals, vitamins, minerals, and feed additives to support growth, milk production, and overall health.

2. What factors are driving the growth of the Europe Cattle Feed Market?

Growth is driven by rising demand for dairy and beef products, increasing livestock productivity requirements, advancements in feed formulation technology, and growing focus on animal health and nutrition efficiency.

3. Which countries are leading in the Europe Cattle Feed Market?

Germany, France, the Netherlands, Spain, and the United Kingdom are major contributors due to strong dairy industries, advanced livestock farming practices, and established feed manufacturing infrastructure.

4. What are the main types of cattle feed available in Europe?

The market includes forage feed, concentrates, compound feed, silage, and specialty feed blends. Concentrates and compound feed are widely used to enhance milk yield and meat production efficiency.

5. What are the key ingredients used in cattle feed?

Common ingredients include corn, barley, wheat, soybean meal, rapeseed meal, molasses, vitamins, minerals, amino acids, and feed additives such as probiotics and enzymes.

6. How does feed quality impact dairy and beef production?

High quality feed improves milk yield, enhances weight gain, supports reproductive performance, strengthens immunity, and reduces disease incidence, thereby improving overall farm profitability.

7. What role do feed additives play in the Europe Cattle Feed Market?

Feed additives such as enzymes, probiotics, antioxidants, and rumen modifiers improve digestion efficiency, enhance nutrient absorption, and support animal health while reducing methane emissions.

8. How are sustainability trends influencing the market?

Sustainability trends are promoting the use of alternative protein sources, reduced carbon footprint feed formulations, locally sourced raw materials, and precision feeding strategies to minimize environmental impact.

9. What challenges affect the Europe Cattle Feed Market?

Major challenges include volatile raw material prices, supply chain disruptions, stringent EU regulations, animal welfare standards, and environmental compliance requirements.

10. What opportunities exist in the Europe Cattle Feed Market?

Opportunities include development of organic feed products, functional feed formulations, digital feed management systems, and innovations aimed at improving feed conversion ratios and reducing emissions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com