Europe Ceiling Fan Market Size, Share, Trends & Growth Forecast Report By Product (Standard, Decorative), Type, Size, Application, Distribution Channel, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Ceiling Fan Market Summary

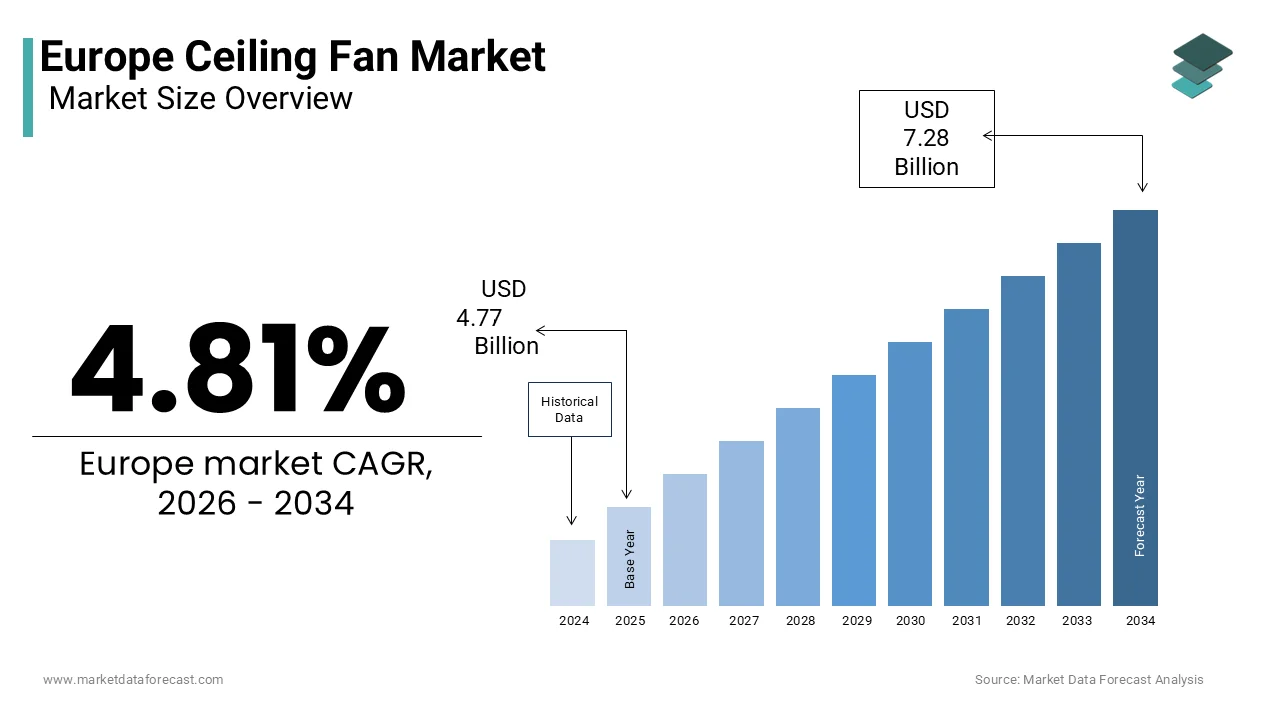

The European ceiling fan market, valued at USD 4.77 billion in 2025, is projected to reach USD 7.28 billion by 2034, growing at a CAGR of 4.81%, driven by rising heat stress, EU energy-efficiency mandates, and adoption of smart, low-carbon cooling solutions.

Key Market Highlights

- 2025 Market Size: USD 4.77 billion

- 2026 Market Size: USD 5.00 billion

- 2034 Forecast: USD 7.28 billion

- CAGR (2026–2034): 4.81%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Integration of ceiling fans intothe EU Energy Efficiency Directive and building renovation programs

- Rising urban heat island effects and recurring summer heatwaves

- Low-cost, low-energy alternative to air conditioning in residential buildings

- Adoption of brushless DC motors and smart, sensor-based fan controls

- Public health focuses on passive cooling for the elderly and vulnerable populations

Principal Restraints

- Cultural reliance on natural ventilation over mechanical cooling

- Low perceived necessity of ceiling fans in mild northern climates

- Architectural and heritage preservation constraints in historic buildings

- Installation limitations in rental and multi-tenant housing stock

High-Value Opportunities

- Smart ceiling fans integrated with IoT-enabled energy management systems

- Inclusion of ceiling fans in social housing retrofit programs

- Growth of outdoor ceiling fans for terraces, hospitality, and public spaces

- Development of low-profile, heritage-compatible fan designs

Key Market Challenges

- Absence of a standardized EU energy labeling framework for ceiling fans

- Seasonal demand volatility leading to inventory and margin pressure

- Performance transparency gaps in airflow, noise, and efficiency claims

- Limited installer awareness and inconsistent point-of-sale guidance

Fastest-Growing Segments

- Standard Ceiling Fans — driven by public sector procurement and energy mandates

- Outdoor Ceiling Fans — rapid uptake in Southern Europe and tourism hubs

- Smart & Connected Fans — integration with home automation ecosystems

Regional Leadership & Dynamics

- Germany (25.4%) — the largest market, driven by sustainability policies and homeownership

- Turkey — fastest growth due to urbanization and appliance manufacturing scale

- Spain & Italy — strong demand linked to heat adaptation and building renovations

- Nordic Countries — niche growth tied to environmental regulation compliance

What Wins Commercially

- Verified energy efficiency through DC motor and smart control adoption

- Heritage-friendly, low-profile, silent designs

- Integration with smart home and demand-response platforms

- Partnerships with public housing authorities and renovation programs

- Clear airflow, noise, and lifecycle cost transparency

Top Strategic Ask for Executives

Position ceiling fans as year-round energy efficiency assets by aligning product design with EU renovation policy, smart building integration, and standardized performance disclosure.

Leading Players

Some of the companies that are playing a dominating role in theEuropeane ceiling fan market include

Crompton Greaves Consumer Electricals Limited, Big Ass Fans, Ajanta Electricals, Fanimation, Craftmade, Minka Lighting LLC, Hunter Fan Company, Monte Carlo Fan Company, Mega Home Appliances, and Kichler Lighting LLC.

Europe Ceiling Fan Market Size

The europe ceiling fan market size was valued at USD 4.77 billion in 2025. The europe market size is estimated to be worth USD 7.28 billion by 2034 from USD 5 billion in 2026, growing at a CAGR of 4.81% from 2026 to 2034.

A ceiling fan is an electrically powered rotating fan that is mounted on the ceiling of a room or space to circulate air. Unlike in tropical climates, ceiling fans in Europe are increasingly integrated into holistic indoor climate strategies that prioritize low-carbon operation and architectural harmony. Many European households depend on natural ventilation or fans during summer due to lower air conditioning adoption compared to the United States, where AC is standard, though AC penetration is growing in Europe. The European Environment Agency indicates that cooling requires a portion of EU electricity, with demand expected to rise significantly by mid-century due to warmer temperatures. EU energy policy, specifically the Energy Efficiency Directive, prioritizes reducing total energy consumption, promoting passive cooling, and energy-efficient thermal management to meet sustainability goals. Modern European ceiling fans are increasingly incorporating energy-efficient brushless DC motors and smart technology for automated, occupant-responsive cooling. This convergence of regulatory pressure, climate adaptation, and design sensitivity positions ceiling fans not as retro appliances but as strategic components of sustainable building operation across the continent.

MARKET DRIVERS

Integration with EU Energy Efficiency and Building Renovation Mandates

The European Union’s binding energy performance standards for buildings serve as a primary driver for theEuropeane ceiling fans market. This trend is occurring across both residential and public sectors. Policy frameworks increasingly mandate higher energy performance for new buildings and deep retrofits for existing public structures to reduce energy demand. Ceiling fans are recognized as a tool to support energy initiatives by allowing for higher indoor temperature setpoints, which helps reduce cooling energy consumption. Standards indicate that operating ceiling fans at moderate speeds can lower the perceived temperature, potentially lessening the load on active cooling systems. Governmental subsidy programs are broadening their scope to include and incentivize the installation of energy-efficient ceiling fans as part of building renovation efforts. Public funding and renovation initiatives are increasingly incorporating passive cooling technologies, such as ceiling fans, into housing retrofits due to their low installation and operational costs. This policy-driven integration transforms fans from discretionary purchases into compliance tools within Europe’s decarbonization architecture.

Rising Urban Heat Island Effects and Summer Temperature Extremes

Escalating urban heat stress across European cities is accelerating demand for low-impact cooling solutions like ceiling fans as traditional infrastructure proves inadequate, which further propels the expansion of the European ceiling fans market. Extreme summer temperatures are increasingly exceeding historical norms across Europe, leading to sustained periods of high heat that challenge existing infrastructure. Dense urban environments frequently experience significantly higher temperatures than neighboring rural areas because heat-retaining building materials and limited vegetation create localized thermal concentrations. Municipal planning is moving toward passive cooling methods, such as the use of high-albedo materials, improved natural ventilation, and shaded public spaces, to manage indoor and outdoor temperatures. New public health initiatives are increasingly focused on retrofitting housing and care facilities for the elderly, specifically targeting those most susceptible to heat-related risks. There is a growing pattern of using low-tech, energy-efficient tools like ceiling fans and enhanced building insulation as primary measures to provide immediate thermal relief while minimizing further environmental impact. Ceiling fans offer an immediate, low-impact means of safeguarding public health as the frequency of extreme temperature events continues to rise globally.

MARKET RESTRAINTS

Low Penetration of Air Conditioning and Cultural Resistance to Mechanical Cooling

The historically limited adoption of air conditioning in European households acts as a significant restraint on the European ceiling fans market expansion. This is despite rising temperatures. Throughout the European Union, the adoption of residential cooling systems is significantly lower than in other major global regions, though it is currently experiencing a period of rapid growth due to more frequent extreme heat events. This stems from cultural preferences for natural ventilation, concerns about energy consumption, and stringent building codes that discourage high-power HVAC retrofits in historic structures. Consequently, many consumers perceive ceiling fans as unnecessary or redundant, particularly in regions with mild summers. Many households in certain European regions tend to view fans primarily as seasonal or decorative items rather than as functional, year-round climate tools. Rental market conditions can inhibit the installation of permanent fixtures, as property owners may hesitate to invest in upgrades without clear, immediate returns. The market for these products often faces constraints due to gaps in consumer perception and a general resistance to changing established habits. Increased awareness regarding the year-round benefits of these products, such as their utility in heat distribution during colder months, could help address these behavioral and perceptual limitations.

Architectural and Heritage Preservation Constraints in Historic Urban Cores

Stringent building conservation regulations in the region’s historic city centers impede ceiling fan installation due to structural and aesthetic limitations, which limit the growth of the European ceiling fans market. Many older structures across Europe feature interior elements, such as ceilings and fixtures, that are subject to strict preservation regulations. Local building codes in numerous historic European cities frequently restrict modifications to original structural or decorative components, making conventional ceiling fan installation difficult. Architecturally sensitive districts often have guidelines that limit the addition of visible mechanical fixtures to maintain the visual consistency of the area. Renovation projects in designated zones sometimes forgo the installation of fans due to lengthy approval processes. Standard fan fixtures may conflict with the aesthetic of historic interiors, while specialized, compliant options can incur significantly higher costs. The lack of formal recognition for adaptive retrofits (e.g., surface-mounted magnetic or tension-based systems) in conservation guidelines persists as a regulatory barrier, inhibiting market growth in culturally significant yet thermally vulnerable urban areas.

MARKET OPPORTUNITIES

Smart Home Integration and IoT-Enabled Energy Management

The convergence of ceiling fans with smart building ecosystems offers a major opportunity to reposition them as intelligent climate nodes rather than standalone appliances, which is expected to fuel the expansion of the European ceiling fans market. Leading manufacturers have introduced models compatible with Matter Zigbee and Thread protocols, enabling seamless integration with Apple Home,e Google Nest, st and Amazon Alexa. These systems allow automated operation based on occupancy temperature and humidity data, optimizing energy use without user intervention. Ambient sensors paired with ceiling fans enable automated, real-time adjustments based on environmental conditions. Automated fan systems can yield higher efficiency in energy usage compared to manual operation. Energy providers are exploring incentive programs to encourage the adoption of smart fan technology. Smart fan technologies linked to grid-responsive platforms can facilitate reduced usage during peak demand periods. This digital transformation elevates fans from passive devices to active participants in demand side management and personalized comfort, unlocking new revenue streams and consumer engagement models.

Retrofit Programs in Social and Public Housing Stock

Large-scale public housing renovation initiatives offer a structured channel for ceiling fan deployment across economically diverse populations, which is anticipated to boost the growth of the European ceiling fans market. The European Commission is pushing to significantly increase the rate of energy renovations for buildings, with a particular focus on upgrading social housing to reduce energy poverty and meet sustainability goals. Ceiling fans are increasingly included in these retrofits as cost-effective measures to improve summer comfort without increasing grid load. Publicly funded programs in Spain are increasingly prioritizing passive cooling solutions, such as energy-efficient, smart-controlled ceiling fans, as a cost-effective measure to improve comfort in municipal housing. Similarly, French housing agencies are incorporating modern, low-energy cooling technologies into their renovation packages to assist lower-income households with rising summer temperatures. The European Anti-Poverty Network emphasizes that such interventions reduce heat-related health risks among elderly and chronically ill residents who cannot afford air conditioning. A large portion of the European social housing stock requires extensive thermal improvements, driving a long-term demand for skilled labor and consistent, high-volume investment in green building technologies.

MARKET CHALLENGES

Inconsistent Energy Labeling and Performance Transparency

The absence of a standardized EU energy labeling framework specifically for ceiling fans creates consumer confusion and undermines trust in efficiency claims, which holds back the expansion of the European ceiling fans market. Unlike refrigerators or lighting, ceiling fans are not covered under the EU Energy Labeling Regulation, allowing manufacturers to use disparate metrics such as airflow per watt, cubic feet per minute, or subjective “eco mode” descriptions. Many tested fan models have shown discrepancies between their advertised airflow performance and their actual power consumption. The variance in performance data makes it difficult for consumers aiming for energy efficiency to accurately compare product options. This inconsistency in technical specifications may deter environmentally conscious buyers from making informed purchasing decisions. Studies have recognized this performance gap, leading to considerations for including these products in future regulatory frameworks. The absence of standardized verification allows these market inconsistencies to continue. Retailers further complicate choices by grouping fans with decorative lighting rather than climate appliances, obscuring functional attributes. The market will struggle to reward true innovation and penalize greenwashing until harmonized testing protocols and mandatory disclosure of performance metrics (CFM, wattage, noise) are enacted.

Seasonal Demand Volatility and Inventory Management Pressures

The highly seasonal nature of ceiling fan sales in the region, peaking between May and August, constrains the growth of theEuropeane ceiling fans market. This creates significant operational challenges for distributors and retailers. Fan shipments tend to concentrate within a specific, short timeframe, creating a cycle of high-volume demand followed by extended periods of inactivity. This pattern requires supply chains to manage significant inventory fluctuations, transitioning quickly from peak activity to dormancy, which can result in overstocking during lower demand or severe shortages during unexpected heatwaves. Manufacturers respond by limiting model variety and favoring generic designs that minimize SKU complexity, stifling aesthetic and technological differentiation. Additionally, unsold inventory from mild summers is often discounted heavily in autumn, eroding margins and discouraging premium product development. The European Retail Round Table notes that seasonal volatility also deters small electricians from stocking fans, reducing point of sale advice and installation support. Absent active demand management, such as seasonal marketing or utility-driven off-season incentives, the industry remains locked in a boom-and-bust procurement cycle that stifles long-term growth and innovation investment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Type, Size, Application, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Crompton Greaves Consumer Electricals Limited, Big Ass Fans, Ajanta Electricals, Fanimation, Craftmade, Minka Lighting LLC, Hunter Fan Company, Monte Carlo Fan Company, Mega Home Appliances, Kichler Lighting LLC, and others. |

SEGMENT ANALYSIS

By Product Insights

The decorative ceiling fans segment held the majority share of 58.6% of the European ceiling fans market in 2025. The supremacy of the decorative ceiling fans segment is driven by strong consumer preference for integrated lighting and aesthetic design in residential interiors. Ceiling fans with integrated lighting are increasingly chosen, reflecting a trend toward versatile, multi-functional fixtures. Decorative models with detailed, handcrafted finishes are frequently featured in upscale retail offerings within certain markets. Ceiling fans are increasingly incorporated into urban interior design plans as coordinated elements rather than standalone appliances. Additionally, heritage-sensitive markets like the UK and the Netherlands favor low-profile decorative fans that blend with period architecture without compromising ceiling integrity. Retailers such as Leroy Merlin and Bauhaus allocate dedicated showroom space to designer fan collections, often collaborating with architects to showcase them in lifestyle vignettes. This fusion of form and function has repositioned ceiling fans from utilitarian appliances to curated home accessories, sustaining the dominance of the decorative segment across high-income and design-conscious demographics.

The standard ceiling fans segment is predicted to witness the highest CAGR of 6.9% from 2026 to 2034 due to large-scale public sector procurement and energy efficiency mandates. Unlike decorative variants, standard models prioritize performance, uniformity,y low noise,se and minimal maintenance, attributes critical for institutional applications. Policies in Spain have introduced requirements for specific energy-efficient ceiling fans, focusing on brushless DC motor technology and performance standards for new social housing projects. Germany’s public financing initiatives have facilitated the installation of standard fans in municipal buildings to improve climate resilience. The European Committee for Standardization has established updated requirements for fans in public procurement, setting benchmarks for motor longevity and ingress protection. These new standards and initiatives in both countries often favor industrial designs that meet the updated performance criteria. Furthermore, utility companies like Enel and EDF are bundling standard fans with heat pump retrofits as part of demand response initiatives, leveraging their predictable power draw for grid stability. This institutional pull, combined with lower unit costs and simplified logistics, positions the standard segment as the fastest growing despite its utilitarian positioning.

By Type Insights

The indoor ceiling fans segment was the largest segment in tEuropeanope ceiling fans market by capturing a substantial share in 2025. The leading position of the indoor ceiling fans segment is attributed to climatic usage patterns and building typologies across the region. The vast majority of residential interior space in Europe is designed to be climate-controlled, focusing on indoor comfort rather than outdoor living. Regional climate factors in Northern and Central Europe make the use of outdoor fans impractical for significant portions of the year due to temperature and precipitation. Indoor ceiling fan models are favored in both new building projects and renovations. Installations of ceiling fans are concentrated in residential living areas, such as bedrooms and hallways, where quiet operation is prioritized. Regulatory standards for fan performance are designed to meet indoor noise requirements. Retail inventory in the region strongly favors indoor-rated fan models over those designed for outdoor use, even in warmer climates. This structural alignment between climate behavior and product availability ensures the indoor segment remains overwhelmingly dominant.

The outdoor ceiling fans segment is estimated to register the fastest CAGR of 9.3 % during the forecast period, owing to the rise of all-season terraces and climate-resilient urban design. Municipalities across Southern Europe are incentivizing covered outdoor spaces to combat heat stress. Spanish municipalities are facilitating the adoption of durable, weather-resistant outdoor cooling units through incentive programs for residential and commercial areas. Growing demand for these solutions in high-humidity environments is driving technical advancements in moisture-resistant motor components and corrosion-resistant materials. The trend shows a shift toward incorporating robust and energy-efficient cooling technology in outdoor urban spaces. Manufacturers like Fanzart and Casablanca have introduced marine-grade aluminum and UV-stabilized ABS composite models specifically for coastal zones. Additionally, the EU’s Green Cities Framework encourages shaded public seating with passive cooling, creating municipal procurement opportunities. This convergence of public health policy, tourism economics, and climate adaptation makes outdoor fans the highest growth niche despite their smaller base.

By Distribution Channel Insights

The offline distribution segment led theEuropeane ceiling fans market by occupying a significant share in 2025. The prominence of the offline distribution segment is credited to the high importance of tactile evaluation, professional installation, and in-person advisory services. Consumers often seek expert advice regarding installation and design for complex or illuminated ceiling fans before finalizing a purchase. Retailers commonly provide in-store demonstrations to allow customers to experience fan performance, such as airflow and noise levels, firsthand. In specific regions with strict electrical regulations for heavy fixtures, consumers tend to favor authorized dealers who can ensure compliant installation. Trade professionals frequently purchase products directly from physical wholesalers to verify technical support and warranty coverage. Seasonal promotions during spring home improvement fairs further drive foot traffic, with bundled offers including downrods and remote controls. This reliance on trust, expertise, and post-sale service sustains the offline channel’s dominance despite digital advances.

The online distribution segment is anticipated to witness the fastest CAGR of 12.4% from 2026 to 2034. The rapid expansion of the online distribution segment is propelled by enhanced digital visualization tools, augmented reality previews,s and streamlined logistics for lightweight DC motor models. Platforms like Amazon EU and ManoMano now offer 3D room simulators, allowing users to preview fan size, blade pitch,h and light output in their actual ceiling dimensions. The rise of direct-to-consumer brands such as Fanzart and Big Ass Fans Europe has further disrupted traditional retail by offering premium features at lower prices through digital native marketing. Additionally, younger homeowners increasingly research products via YouTube reviews and Pinterest inspiration boards before ordering, bypassing physical showrooms entirely. Improved last-mile logistics and more efficient return processes are enabling online channels to secure a larger share of both first-time and replacement purchases.

COUNTRY LEVEL ANALYSIS

Germany Ceiling Fan Market Analysis

Germany was the top performer in the Europe ceiling fan market with an estimated share of 25.4% in 2025. The growth of the segment is due to the country’s robust manufacturing base and high homeownership rates. Germany’s emphasis on sustainability, which aligns with EU regulations, is drivingthe adoption of eco-friendly models. For instance, as per Eurostat, over 70% of households in Germany own private homes, which is creating a robust demand for efficient cooling solutions. Additionally, government incentives for recycling have increased the use of eco-friendly fans.

Turkey Ceiling Fan Market Analysis

Turkey is expected to grow with the fastest CAGR of 9.8% in the coming years, owing to the rapid urbanization, increasing consumer spending, and rising exports of home appliances. Turkey’s ceiling fan market has grown by 30% since 2020, with investments in modern manufacturing facilities. Additionally, government-led initiatives promoting sustainable construction practices have accelerated adoption, positioning Turkey as a key growth driver in the region.

Countries like France, Italy, and Spain are expected to witness steady growth due to their strong construction industries and export-oriented economies. Eastern European nations like Poland and Romania face challenges such as limited infrastructure, but show potential due to ongoing reforms. The Czech Ministry of Trade predicts a 15% increase in ceiling fan investments by 2025. Meanwhile, Nordic countries benefit from stringent environmental regulations by ensuring equitable access to sustainable solutions.

COMPETITIVE LANDSCAPE

TheEuropeane ceiling fans market features a diverse mix of global brands, niche designers,s and local manufacturers competing across price,ce performance, and aesthetics. Competition is intensified by low entry barriers for decorative models, yet tempered by technical requirements for energy efficiency,y noise control, and electrical safety compliance. Global players leverage scale and smart technology integration while regional artisans differentiate through bespoke craftsmanship and heritage alignment. The absence of mandatory EU energy labeling creates information asymmetry, allowing unsubstantiated efficiency claims to persist. Retail channels exert significant influence, with large DIY chains favoring standardized SKUs while independent showrooms curate premium collections. Consumer awareness remains uneven—high in Southern Europe due to heavy exposure,e but limited in Nordic regions where fans are perceived as unnecessary. Innovation focuses on silent operation, compact profile,s and reversible winter modes to justify year-round value. As climate adaptation policies evolve, competition is gradually shifting from decorative appeal to verifiable thermal comfort contribution within broader building energy strategies.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe ceiling fan market include

- Crompton Greaves Consumer Electricals Limited

- Big Ass Fans

- Ajanta Electricals

- Fanimation

- Craftmade

- Minka Lighting LLC

- Hunter Fan Company

- Monte Carlo Fan Company

- Mega Home Appliances

- Kichler Lighting LLC

TOP LEADING PLAYERS IN THE MARKET

- Fanzart has established a strong presence in the European ceiling fans market through its premium designer fans that blend high airflow performance with architectural aesthetics. The company specializes in ultra-quiet brushless DC motor technology and offers models with integrated smart controls compatible with European home automation systems. Recently, Fanzart expanded its distribution network across Germany, France, and Italy by partnering with high-end interior design studios and lighting showrooms. It also launched a dedicated EU compliance team to ensure all products meet CE, RoC, and Ecodesign Directive requirements. The brand’s emphasis on customizable finishes and energy efficiency has resonated with urban renovators and boutique hospitality projects seeking sustainable luxury solutions without compromising on style or silence.

- Hunter Fan Company maintains significant influence in Europeanrope ceiling fans market by leveraging its heritage brand recognition and extensive product portfolio spanning traditional to contemporary designs. The company has localized its offerings to meet European voltage standards and acoustic regulations while integrating with popular smart home platforms like Apple HomeKit and Google Assistant. In recent years,s Hunter strengthened its position by collaborating with major DIY retailers such as Leroy Merlin and Kingfisher to enhance in-store visibility and installation support. It also introduced a line of low-profile fans specifically engineered for older European apartments with limited ceiling height. These adaptations demonstrate Hunter’s commitment to addressing regional structural and aesthetic preferences while maintaining global quality benchmarks.

- Big Ass Fans Europe serves the commercial and high-performance residential segments with industrial-grade ceiling fans optimized for large-volume spaces and energy-conscious operation. The company supplies schools, warehouses,s and public buildings across Northern and Western Europe with fans that deliver superior air movement at minimal wattage. Recently, it enhanced its digital offering by launching an online airflow simulator that helps architects specify optimal fan size and placement based on room dimensions and occupancy patterns. Big Ass Fans also works closely with EU energy agencies to include its products in public building retrofit guidelines. Its focus on verifiable performance data third-partyy certifications, and lifecycle cost analysis differentiates it in technically driven procurement environments where efficiency and durability outweigh decorative appeal.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in theEuropeane ceiling fans market prioritize integration with smart home ecosystems to enhance user convenience and energy management capabilities. They invest in brushless DC motor technology to comply with stringent EU ecodesign and noise regulations while reducing operational costs. Companies collaborate with interior designers and electricians to embed fans into holistic renovation projects rather than treating them as standalone appliances. Strategic partnerships with large-format DIY retailers ensure prominent in-store placement and access to certified installation services. Additionally, they emphasize winter destratification functionality to promoteyear-roundd usage and counter seasonal demand volatility. Marketing campaigns increasingly highlight health and comfort benefits beyond cooling, including improved air circulation and reduced mold risk in humid climates. These strategies collectively reinforce product relevance in a market historically dominated by passive ventilation and cultural resistance to mechanical air movement.

EUROPE CEILING FAN MARKET NEWS

- In April 2023, Hunter Fan launched a new line of AI-driven smart ceiling fans in Germany by reducing energy consumption by 25% while maintaining performance.

- In June 2023, Minka-Aire partnered with Italian interior designers to develop custom decorative fans by enhancing brand differentiation and market penetration.

- In September 2023, Big Ass Fans acquired a leading ceiling fan manufacturer in Turkey by strengthening its position in the fast-growing Middle Eastern market.

- In November 2023, Casablanca Fan Company introduced a cloud-based platform in Switzerland by streamlining the customization of fan designs based on consumer preferences.

- In February 2025, Fanimation collaborated with tech firms in France to develop solar-powered fans by positioning itself as a leader in eco-friendly solutions.

MARKET SEGMENTATION

This research report on the europe ceiling fan market is segmented and sub-segmented into the following categories.

By Product

- Standard

- Decorative

By Type

- Indoor

- Outdoor

By Distribution Channel

- Online

- Offline

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which countries lead the Europe Ceiling Fan Market?

Germany dominates the Europe Ceiling Fan Market with high consumer awareness, energy efficiency focus, and strong construction activity. France and Italy follow, supported by homeownership rates and preferences for modern, sustainable cooling in residential spaces.

2. What types dominate the Europe Ceiling Fan Market?

Medium-sized fans lead the Europe Ceiling Fan Market for their balance of affordability, performance, and features like smart controls. Standard fans hold significant share due to versatility in homes and offices, with growing interest in decorative and rustic designs.

3. How do energy regulations impact the Europe Ceiling Fan Market?

EU energy regulations drive the Europe Ceiling Fan Market by incentivizing low-power, eco-friendly models that consume far less electricity than AC units. This shift appeals to environmentally conscious consumers seeking sustainable cooling options in cities.

4. What role do smart features play in the Europe Ceiling Fan Market?

Smart ceiling fans are emerging in the Europe Ceiling Fan Market, integrated with home automation for remote control and efficiency. Adoption rises in Western Europe, where over 40% of households use connected devices, supported by subsidies for green tech.

5. What are main distribution channels in the Europe Ceiling Fan Market?

Offline channels dominate the Europe Ceiling Fan Market as consumers prefer physical inspection, immediate purchase, and after-sales support in retail stores. Online growth occurs but lags due to the tactile buying preference for fans.

6. Why prefer ceiling fans in the Europe Ceiling Fan Market?

Ceiling fans in the Europe Ceiling Fan Market offer cost-effective cooling, using 80% less energy than air conditioners, ideal for rising bills. They suit varied climates, especially southern Europe, and pair with AC for enhanced comfort.

7. What trends shape the Europe Ceiling Fan Market?

Trends in the Europe Ceiling Fan Market include aesthetic designs, smart integration, and premium decorative fans like contemporary or black models. Sustainability pushes low-energy motors and materials, aligning with green building codes.

8. How does urbanization affect the Europe Ceiling Fan Market?

Urbanization fuels the Europe Ceiling Fan Market through new apartments, renovations, and dense housing needing efficient cooling. Cities prioritize space-saving, stylish fans that fit modern interiors while cutting energy use.

9. What opportunities exist in the Europe Ceiling Fan Market?

Opportunities in the Europe Ceiling Fan Market lie in smart home tech, eco-incentives, and hospitality expansions. Demand grows for connected, recyclable fans in commercial projects and sustainable residential upgrades.

10. Which fan sizes are popular in the Europe Ceiling Fan Market?

Medium sizes prevail in the Europe Ceiling Fan Market for optimal airflow in typical rooms, offering energy savings and modern aesthetics. They suit diverse applications from homes to offices effectively.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com