Europe Cookies Market Research Report – Segmented Based on Type, Ingredient, Distribution Channel and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis on Size, Share, Trends, & Growth Forecast (2026 to 2034)

Europe Cookies Market Size

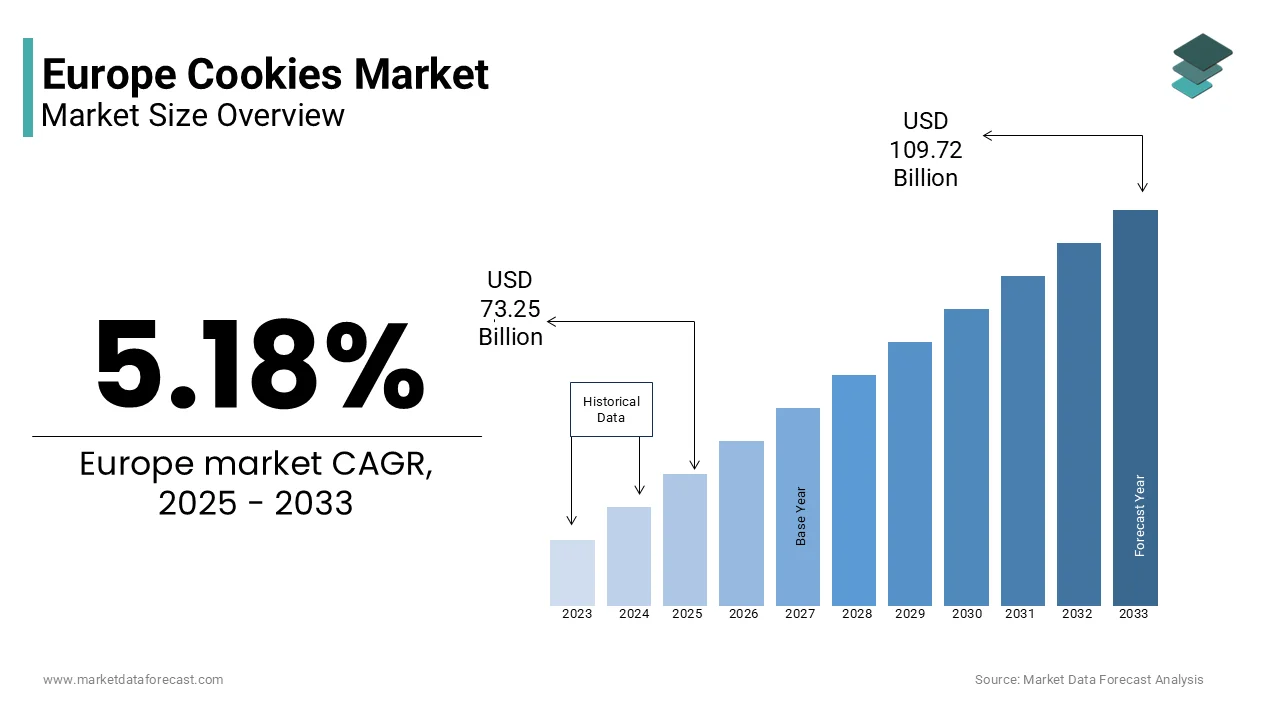

The Europe cookies market size was valued at USD 73.25 billion in 2025, and the market size is expected to reach USD 115.39 billion by 2034 from USD 77.04 billion in 2026. The market is growing at a CAGR of 5.18%.

The cookies are baked sweet and savory confections primarily formulated from flour, sugar, fats, and flavorings, consumed as snacks, desserts, or breakfast accompaniments. These products span traditional butter cookies, chocolate-dipped variants, filled sandwich cookies, and health-oriented functional biscuits. Unlike broader baked goods, cookies in Europe are deeply embedded in cultural rituals—from afternoon tea pairings in the UK to festive Weihnachtsplätzchen in Germany. As of 2024, Europeans consumed an average of 6.8 kilograms of cookies per capita annually, reflecting deeply rooted snacking habits, as per Eurostat’s food consumption survey.

MARKET DRIVERS

Rising Demand for Indulgent and Premium Snacking Experiences

The European consumers are increasingly prioritizing sensory satisfaction and emotional well-being in their food choices, which is driving the growth of Europe cookies market. The post-pandemic shift toward at-home comfort consumption has elevated the role of indulgent snacks as a form of affordable luxury. Brands like LU (Mondelez), Danone’s LU Biscuits, and German specialty baker Bahlsen have responded with artisanal packaging, single-origin cocoa, and small-batch formulations. The trend is particularly strong among urban millennials and Gen Z consumers, who associate premium cookies with self-reward and mindfulness.

Integration of Functional Ingredients for Cognitive and Emotional Wellness

The growing support for mental well-being and cognitive function with innovation in functional formulations is escalating the growth of Europe cookies market. Ingredients such as magnesium, L-theanine, chamomile, and adaptogenic herbs are being incorporated into cookie matrices to promote relaxation and stress relief. Companies like Eat Your Happy (UK) and SereniTea (France) have launched melatonin-infused and botanical-enriched cookies targeting sleep and anxiety. The European Food Safety Authority has approved several health claims related to magnesium and nervous system function, lending scientific credibility.

MARKET RESTRAINTS

Stringent Nutrient Profiling Regulations Under the EU’s Health Claims Framework

The Europe Union’s tightening regulatory environment the evolving Nutrient Profiling Model under Article 4 of the Nutrition and Health Claims Regulation (EC) No 1924/2006, is restricting the growth of Europe cookies market. National implementations are already underway France’s Nutri-Score system has led to a 27% reduction in shelf space for D- and E-rated sweet snacks since 2020, according to INSEE. The Netherlands’ Hoschedé Table has prompted reformulation delays. These frameworks complicate innovation for products aiming to include functional ingredients while remaining compliant. Manufacturers face rising costs in reformulation and clinical substantiation, which is slowing time-to-market and limiting creative freedom in product development.

Consumer Skepticism Toward Ultra-Processed Ingredients and Artificial Additives

The rejecting products perceived as ultra-processed is hindering the growth of Europe cookies market. As per a 2024 Eurobarometer survey, 63% of EU citizens believe that processed foods negatively impact long-term health, with particular concern over emulsifiers, artificial flavors, and preservatives commonly used in mass-produced cookies. The Nordic Council’s 2022 report on food additives recommended phasing out certain emulsifiers like E471 due to gut microbiome concerns, influencing consumer behavior. Retailers such as Denmark’s Irma and Germany’s Alnatura have delisted conventional cookie lines in favor of organic, short-ingredient alternatives.

MARKET OPPORTUNITIES

Expansion of Plant-Based and Allergen-Free Cookie Variants

The surge in plant-based diets and food allergy awareness is likely to pose new opportunities for theg growth of Europe cookies market. As per the European Federation of Allergy and Airways Diseases Patients’ Associations (EFA), over 22 million Europeans suffer from food allergies, with milk, eggs, and nuts being among the most common triggers. Companies like Pip & Nut (Netherlands) and Biscuiteers (UK) have launched egg-free, dairy-free cookies using oat milk, aquafaba, and pea protein. Supermarkets including Tesco and Carrefour now dedicate shelf space to allergen-free ranges.

Leveraging Regional Culinary Heritage for Export-Oriented Premiumization

The rich tapestry of regional recipes that offer authenticity and differentiation is additionally to elevate the growth of Europe cookies market. Traditional varieties such as Italian amaretti, Austrian linzer, and Danish havregrynskager are increasingly positioned as premium gourmet exports. Countries like Italy and Belgium are branding their cookies as protected gastronomic heritage Parma’s Biscotti di Valtellina received PGI status in 2022 by enhancing market exclusivity. Domestic producers are partnering with luxury retailers such as Harrods and Le Bon Marché to position cookies as gifting items. The European Commission’s “Taste of Europe” campaign has further amplified visibility.

MARKET CHALLENGES

Volatility in Key Raw Material Supply Chains, Particularly Palm Oil and Cocoa

The instability in the supply of ingredients like palm oil and cocoa, both of which are subject to geopolitical, climatic, and regulatory disruptions is hindering the growth of Europe cookies market. In 2022, Indonesia’s temporary palm oil export ban caused prices to spike by over 40% within three weeks, severely impacting production margins. Similarly, cocoa prices reached a 47-year high in early 2025 due to crop failures in West Africa, where Côte d’Ivoire and Ghana produce 60% of global supply, according to the International Cocoa Organization.

Balancing Sustainability Commitments with Packaging Performance

The manufacturers are under increasing pressure to eliminate plastic-based packaging in preserving freshness and preventing breakage with eco-friendly alternatives, which is likely to limit the growth of Europe cookies market. As per the European Environment Agency, flexible plastic packaging accounts for 39% of all plastic waste in the EU, prompting legislation like the Packaging and Packaging Waste Regulation (PPWR) mandating 65% recyclability by 2030. Brands like McVitie’s and Kelsen have delayed rollouts of sustainable packaging due to quality concerns. This tension between environmental goals and product integrity forces companies into costly R&D cycles, which is slowing progress despite strong consumer demand for greener solutions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.18% |

| Segments Covered | By Type, Ingredient, Distribution Channel and Region |

| Various Analyses Covered | Global, Regional, and country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

| Market Leaders Profiled | Mondelez International, Kellogg Co., Campbell Soup Co., Nestle SA, United Biscuits, PepsiCo, M. Dias Branco, Britannia Industries, Barilla G. e R. Fratelli, and Arcor U.S.A., Kraft Foods, Thomas Tunnock Limited, Nutrexpa, Paterson Arran Limited |

SEGMENTAL ANALYSIS

By Type Insights

The sandwich cookies segment was accounted in holding 28.3% of the Europe cookies market share in 2025 with their versatility, portability, and strong appeal across age groups, particularly children and young adults. The emotional and nostalgic association with well-established brands is escalating the growth of Europe cookies market. Mondelez’s Oreo, for instance, reported a 12% year-on-year sales increase in Western Europe in 2024, driven by limited-edition flavors and seasonal packaging, as noted in the company’s regional performance review. Additionally, the rise of premium sandwich cookies with fillings like salted caramel and matcha has expanded their appeal beyond traditional consumers.

The no-bake cookies segment is projected to grow with an expected CAGR of 9.7% during the forecast period with the shifting consumer preferences toward convenience, clean-label ingredients, and home-based experiential cooking. As per a 2024 Eurobarometer survey, 68% of European parents with children under 12 prefer no-bake or minimal-cook recipes for weekend family activities, reflecting a cultural shift toward interactive, low-effort food preparation. The alignment of no-bake cookies with clean-label and plant-based trends is amplifying the growth of segment.

By Ingredient Insights

The chocolate ingredient segment was accounted in holding 35.4% of the Europe cookies market share in 2025 with the chocolate’s universal appeal, sensory richness, and deep integration into European confectionery culture. From dark chocolate-dipped digestives in the UK to filled Schokoladenkekse in Germany, chocolate remains the most preferred flavor enhancer in cookie formulations. The psychological association between chocolate and mood enhancement is escalating the growth of Europe cookies market. Chocolate contains compounds such as theobromine and phenylethylamine, which are linked to serotonin release.

The oatmeal ingredient segment is swiftly emerging with a CAGR of 8.9% from 2026 to 2034 with the rising emphasis on whole grains, digestive health, and sustained energy release. Oatmeal cookies are increasingly perceived not as mere snacks but as functional foods that support balanced diets. The recognition of beta-glucan, a soluble fiber in oats, for its cholesterol-lowering effects. This scientific backing has elevated oatmeal cookies from traditional home baking to mainstream health positioning. Brands like Alpro and Oatly have extended into baked snacks, which is launching oat-based cookies with added plant protein and no added sugar by appealing to fitness-conscious and diabetic consumers.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held a dominant share of the Europe cookies market in 2025. These channels remain the primary destination for cookie purchases due to their wide product assortment, competitive pricing, and integration into weekly grocery routines. The format allows consumers to access everything from mass-market brands like McVitie’s and LU to premium and organic variants under one roof. Retailers use data-driven planograms to maximize visibility and impulse buying.

The online sales channel is projected to grow at a CAGR of 12.4% during the forecast period with the changing consumer behavior, digital accessibility, and the rise of specialty and direct-to-consumer (DTC) brand. Cookies, particularly artisanal, limited-edition, and subscription-based varieties, are well-suited for online fulfillment due to their shelf-stable nature and gifting appeal. The proliferation of niche brands leveraging digital platforms to bypass traditional retail gatekeepers is additionally to elevate the growth of Europe cookies market.

REGIONAL ANALYSIS

Germany Cookies Market Analysis

Germany was the top performer and held 18.3% of the Europe cookies market share in 2025. Germans consume an average of 7.3 kilograms of cookies annually, the highest in Western Europe, as reported by the German Nutrition Society. This cultural habit drives consistent demand, with cookies consumed daily in homes, workplaces, and cafés. The Federal Ministry of Food and Agriculture notes that over 60% of packaged cookies sold in Germany are purchased for home consumption, often as part of weekly grocery hauls. Major players like Bahlsen, Hero, and Nestlé maintain strong domestic production by ensuring freshness and supply chain control. In recent years, Germany has also emerged as a testbed for innovation, with brands launching sugar-reduced, fiber-enriched, and allergen-free variants in response to tightening nutritional guidelines.

United Kingdom Cookies Market Analysis

The UK was positioned second by capturing 12.3% of the Europe cookies market share in 2025. It is distinguished by its concentration of globally recognized brands and a highly competitive retail landscape. The brand’s dominance is reinforced by nostalgic branding, consistent quality, and strategic innovation, such as the launch of chocolate-coated and light versions.British consumers exhibit strong brand loyalty but are also receptive to premium and health-oriented variants. As per a 2024 YouGov survey, 52% of UK adults consume biscuits daily, with afternoon tea being a key consumption occasion.

France Cookies Market Analysis

France cookies market growth is likely to be driven by the premiumization and artisanal production. The country’s biscuiteries régionales, such as those in Alsace and Brittany, produce high-margin, heritage-based cookies that command price premiums both domestically and internationally. As per the French Federation of Baking Industries, over 220 artisanal cookie producers operate in France, many with protected geographical indications. This preference supports niche brands like LU, which has revitalized its image with organic and limited-edition lines.

Italy Cookies Market Analysis

Italy cookies market growth is likely to grow with the unique role due to its culinary heritage and export strength. Italian cookies are often linked to protected designations, such as Amaretti di Saronno (IGP), which enhances authenticity and pricing power. Retailers like Conad and Esselunga promote regional varieties, supporting local producers. Additionally, Italy is a leader in gluten-free innovation, with rice- and almond-based cookies catering to celiac populations.

Spain Cookies Market Analysis

Spain represents 9% of the Europe cookies market in 2024, according to Spain’s National Statistics Institute (INE), and is emerging as a high-potential market due to shifting consumption habits and urbanization. Traditionally, churros and pastries dominated the sweet snack space, but packaged cookies are gaining ground, especially among younger, urban consumers. As per a 2024 study by the Spanish Nutrition Foundation, cookie consumption among adults aged 18–35 increased by 17% between 2020 and 2024.

COMPETITIVE LANDSCAPE

The competition in the Europe cookies market is characterized by a dynamic interplay between multinational corporations, regional artisans, and emerging direct-to-consumer brands. Established players like Mondelez and Nestlé dominate through brand equity, distribution scale, and R&D capabilities, while local producers leverage heritage and authenticity to capture niche segments. The rise of health-consciousness, sustainability demands, and digital shopping has intensified rivalry, forcing companies to innovate beyond taste into functionality and ethics.

KEY MARKET PLAYERS

A few of the notable players in the Europe cookies market include

- Mondelez International

- Kellogg Co.

- Campbell Soup Co.

- Nestle SA

- United Biscuits

- PepsiCo

- M. Dias Branco

- Britannia Industries

- Barilla G. e R. Fratelli

- Arcor U.S.A.

- Kraft Foods

- Thomas Tunnock Limited

- Nutrexpa

- Paterson Arran Limited

TOP PLAYERS IN THE MARKET

- Mondelez International is a dominant force in the Europe cookies market, which is leveraging iconic brands such as Oreo, LU, and Cadbury to shape consumer preferences across the continent. The company has consistently invested in product innovation, introducing region-specific flavors like Oreo Red Velvet in Germany and LU Petit Écolier in France. In 2024, Mondelez expanded its sustainability-driven "Cocoa Life" program across European supply chains, ensuring ethically sourced ingredients while reducing environmental impact. It also enhanced its digital engagement through augmented reality packaging and e-commerce partnerships with Amazon and Picnic. Additionally, Mondelez strengthened its manufacturing footprint by upgrading its biscuit facility in Warsaw, Poland, to increase output efficiency and support export demand.

- Nestlé prioritized health-oriented innovation, reformulating several cookie lines to reduce sugar by up to 30% without compromising taste, in alignment with WHO recommendations and national sugar reduction strategies. It has also deepened retail integration through smart shelf technology in partnership with Carrefour, enabling real-time inventory tracking and personalized promotions. Nestlé’s investment in AI-driven consumer insights has accelerated product development cycles, allowing rapid response to flavor trends and dietary shifts.

- Bahlsen is a German-origin biscuit manufacturer, which remains a cornerstone of the Europe cookies market with heritage brands like Leibniz, Choco Leibniz, and Jaffa Cakes. The company has maintained strong regional loyalty while expanding its presence through strategic innovation and sustainability initiatives. It also launched a line of protein-enriched cookies in collaboration with fitness nutrition platforms, targeting active consumers in Scandinavia and Benelux. Bahlsen has enhanced its digital footprint by partnering with online grocery platforms like Edeka.de and REWE.to, optimizing direct-to-consumer delivery.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the Europe cookies market are deploying multifaceted strategies to maintain competitiveness amid evolving consumer demands and regulatory pressures. Major approaches include product innovation focused on health enhancement, such as sugar reduction, fiber enrichment, and allergen-free formulations. Companies are investing in clean-label transparency, sourcing non-GMO, organic, and ethically produced ingredients. Sustainability is a central pillar, with brands transitioning to recyclable packaging and carbon-neutral production. Digital engagement through e-commerce optimization, direct-to-consumer models, and AI-driven personalization is accelerating customer retention.

MARKET SEGMENTATION

This research report on the Europe cookies market has been segmented and sub-segmented into the following categories.

By Type

- Bar

- Sandwich

- Drop

- Rolled

- Molded

- Refrigerator

- No-Bake

- Fried

By Ingredient

- Chocolate

- Chocolate Chip

- Oatmeal

- Butter

- Cream

- Ginger

- Coconut

- Honey

- Others

By Distribution Channel

- Supermarkets and Hypermarkets

- Independent Retailers

- Convenience Stores

- Online Sales

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe cookies market?

The Europe cookies market refers to the production, distribution, and consumption of cookies across European countries, including both traditional and innovative cookie varieties.

2. What is driving the growth of the Europe cookies market?

Rising demand for convenient snacks, premiumization, and healthier alternatives like gluten-free and organic cookies are major growth drivers.

3. Which countries lead the Europe cookies market?

The United Kingdom, Germany, France, and Italy are among the leading markets in Europe due to high consumer demand and established bakery industries.

4. What are the main product types in the Europe cookies market?

Popular categories include chocolate chip cookies, cream-filled cookies, butter cookies, oatmeal cookies, and specialty cookies.

5. What distribution channels dominate the Europe cookies market?

Supermarkets, hypermarkets, convenience stores, online retail, and specialty bakeries are the primary sales channels.

6. Who are the major players in the Europe cookies market?

Leading companies include Mondelez International, Nestlé, Kellogg’s, United Biscuits, Barilla, and Britannia Industries.

7. What challenges does the Europe cookies market face?

Increasing health awareness, sugar reduction regulations, and strong competition from alternative snacks are key challenges.

8. What is the future outlook for the Europe cookies market?

The market is expected to grow steadily, driven by innovation in flavors, health-focused cookies, and digital retail expansion.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com