Global Cookies Market Size, Share, Trends & Growth Forecast Report Segmented By Ingredient (Chocolate, Chocolate Chip, Oatmeal, Butter, Cream, Ginger, Coconut & Honey), Product, Distribution Channel and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis (2026 to 2034)

Global Cookies Market Report Summary

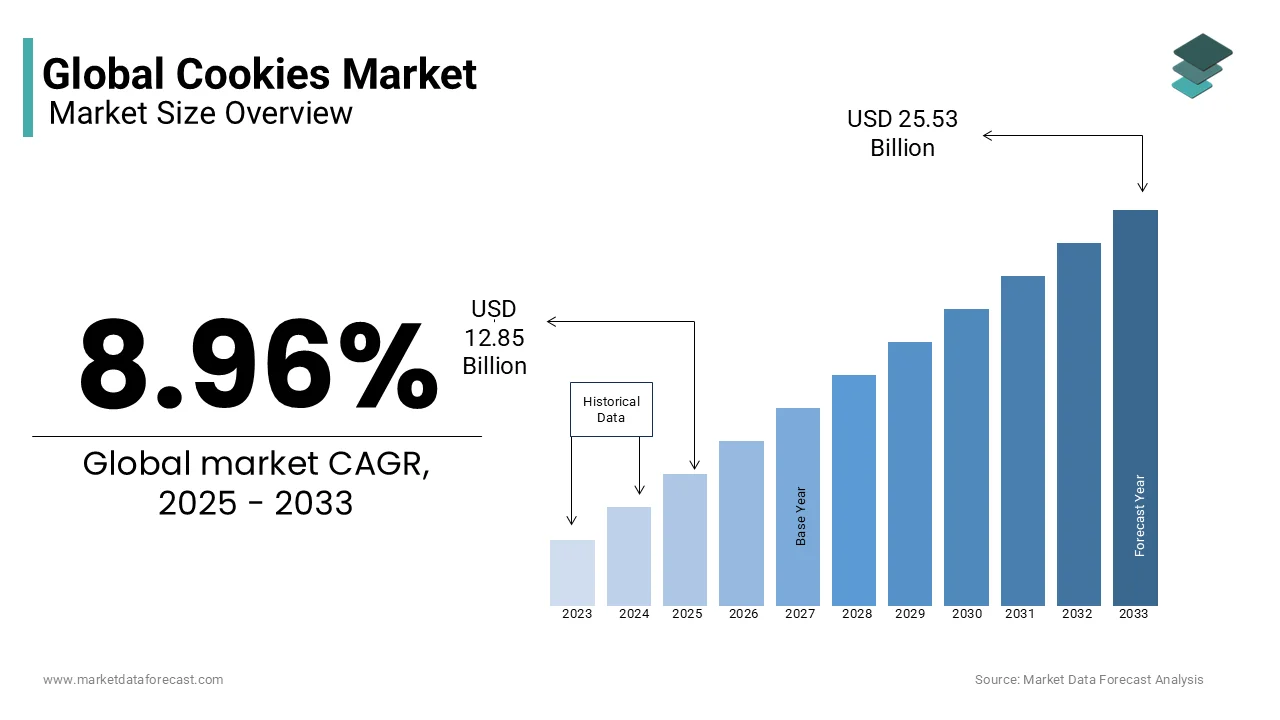

The global cookies market size was valued at USD 12.87 billion in 2025, is projected to reach USD 14.02 billion in 2026, and is expected to surge to USD 27.85 billion by 2034, growing at a strong CAGR of 8.96% during the forecast period. Market growth is driven by rising consumer demand for convenient snacks, increasing product innovation in flavor, texture, and packaging, and the growing popularity of premium, organic, and clean-label cookies. Strong retail expansion, rising disposable incomes, and growing influence of Western snacking habits in developing countries further support market expansion globally.

Key Market Trends

- Increasing demand for convenient, on-the-go snacks across all age groups.

- Rising popularity of premium, artisanal, gluten-free, and organic cookies.

- Growing product diversification including protein cookies, vegan cookies, and limited-edition flavors.

- Expansion of retail networks and strong performance of offline grocery and bakery channels.

- Continued innovation by major brands in packaging, shelf life, and healthier formulations.

- Strong influence of North American cookie culture shaping global market trends.

Segmental Insights

- Based on product, the bar cookies segment is predicted to dominate the global cookies market during the forecast period, supported by consumer preference for chewy textures, indulgent flavors, and convenient snack-bar formats.

- Based on distribution channel, offline channels are anticipated to account for the majority of global cookie distribution during the forecast period, driven by supermarkets, hypermarkets, convenience stores, and in-store bakery sections.

Regional Insights

- The North American cookies market outperformed all other regions and accounted for the largest share of the global market in 2024. Growth is fueled by strong consumer affinity for baked snacks, continuous product innovation, and the presence of globally leading cookie brands.

Competitive Landscape

The global cookies market is competitive and dominated by major multinational food manufacturers, supported by strong distribution networks, flavor innovation, and aggressive marketing strategies. Leading companies in the global cookies market include Parle Products Private Limited, Danone S.A., Mondelēz International, Campbell Soup Company, Britannia Industries Ltd, PepsiCo, Nestlé S.A., and The Kellogg Company.

Notably, Nestlé has recently launched edible Funfetti cookie dough brownie batter, adding a new nostalgic flavor experience to its portfolio

Global Cookies Market Size

The global cookies market size was valued at USD 12.87 billion in 2025. The cookies market size is expected to reach USD 27.85 billion by 2034 from USD 14.02 billion in 2026. The market's promising CAGR for the predicted period is 8.96%.

The cookies are baked sweet treats characterized by their flat shape and crisp or chewy texture. The definition extends beyond traditional chocolate chip varieties to include oatmeal shortbread and specialized dietary alternatives. Consumer engagement with this sector remains robust due to the inherent versatility and emotional comfort associated with these confections. Furthermore, as per the International Cocoa Organization, global cocoa consumption reached 4.8 million metric tons in the 2022 to 2023 season reflecting sustained demand for key cookie ingredients. The cultural significance of cookies in European traditions drives consistent purchase behavior regardless of economic fluctuations. Retailers observe that cookies account for a substantial portion of impulse purchases in grocery aisles. Manufacturers focus on texture and ingredient quality to maintain consumer loyalty. The sector benefits from established distribution networks that ensure widespread availability.

MARKET DRIVERS

Rising Preference for Premium and Artisanal Variants

The shift towards premiumization significantly influences purchasing decisions is propelling the growth of the cookies Market. Consumers increasingly seek high quality ingredients such as Belgian chocolate organic flour and natural vanilla extracts. This trend reflects a broader desire for indulgence and authenticity in snack choices. This growth outpaces the overall snack category indicating a strong consumer willingness to pay more for superior products. Artisanal bakeries and specialty brands capitalize on this demand by offering small batch cookies with unique flavor profiles. The emphasis on craftsmanship and local sourcing appeals to discerning buyers who prioritize transparency and ethical production methods. This preference drives manufacturers to reformulate existing products and launch new lines that cater to the gourmet segment. The rise of social media also plays a crucial role as visually appealing premium cookies generate significant online engagement. Influencers and food bloggers often showcase luxurious cookie experiences which further stimulates demand. Retailers respond by dedicating shelf space to high end brands and creating dedicated sections for artisanal treats.

Increasing Demand for Convenient On the Go Snack Options

The modern lifestyles characterized by hectic schedules and limited meal times for convenient snack solutions is escalating the growth of cookies market. Cookies offer an ideal option due to their portability long shelf life and ease of consumption. As per survey, single serve snack packs accounted for 35% of total cookie sales in Western Europe in 2023. This format appeals to students office workers and commuters who require quick energy boosts throughout the day. The convenience factor is further amplified by the widespread availability of vending machines and convenience stores in urban areas. Manufacturers respond by developing resealable packaging and compact sizes that fit easily into bags and pockets. The trend towards smaller household sizes also contributes to this demand as individuals prefer portion-controlled snacks over large family packs. Additionally, the rise of remote work has created new consumption occasions such as mid-morning and afternoon breaks at home.

MARKET RESTRAINTS

Stringent Government Regulations on Sugar Content and Labeling

The health concerns related to excessive sugar consumption have prompted governments to implement stricter regulations on food products is declining the growth of cookies market. These measures directly limit the amount of sugar that can be used in formulations. For instance, the United Kingdom introduced a soft drinks industry levy which has inspired similar discussions for solid foods including cookies. According to the World Health Organization, European Region recommended daily sugar intake should not exceed 50 grams yet many cookie products surpass this limit in just a few servings. Compliance with new labeling laws such as the Nutri Score system requires manufacturers to reformulate recipes to achieve better nutritional ratings. This process involves significant research and development expenses as well as potential changes in supply chains for alternative sweeteners. Furthermore, negative public perception of high sugar products discourages consumption among health conscious people. This scrutiny forces brands to invest heavily in marketing low sugar variants which may not always match the taste profile of traditional cookies. The regulatory landscape thus creates a challenging environment where manufacturers must balance taste appeal with legal and health standards. Failure to adapt can result in reduced shelf space and declining sales as retailers prioritize healthier options.

Volatility in Raw Material Prices for Key Ingredients

The fluctuating costs of essential ingredients, such as wheat cocoa butter and milk powder is also degrading the growth of cookies market. These commodities are subject to global supply chain disruptions weather events and geopolitical tensions, which lead to unpredictable price swings. Cocoa prices specifically reached historic highs in early 2024 due to poor harvests in West Africa, which supplies 70% of the world's cocoa. This surge forces manufacturers to either absorb the costs resulting in lower margins or pass them on to consumers through higher retail prices. Both options carry risks as price hikes can reduce demand while margin compression affects profitability. Data from the International Grains Council shows that wheat prices remained volatile throughout 2023 with monthly fluctuations averaging 8%. Dairy prices also exhibit instability due to varying feed costs and production levels in major exporting countries. These financial uncertainties complicate long term planning and budgeting for cookie manufacturers. Small and medium sized enterprises are particularly vulnerable as they lack the bargaining power to secure favorable contracts.

MARKET OPPORTUNITIES

Expansion into Plant Based and Allergen Free Segments

The rising prevalence of food allergies and the growing adoption of plant-based diets for innovation is solely to create new opportunities for the growth of cookies market. Consumers increasingly seek products free from gluten dairy eggs and nuts due to health concerns or ethical choices. According to the European Academy of Allergy and Clinical Immunology, approximately 17 million people in Europe suffer from food allergies driving demand for safe alternative snacks. Manufacturers respond by developing specialized formulations using ingredients such as almond flour oat milk and chickpea protein. Cookies labeled as vegan or gluten free often command higher prices and attract loyal customer bases. Retailers are expanding their free from sections to accommodate this trend providing greater visibility for niche products. Additionally, the clean label movement encourages the use of natural ingredients and avoidance of artificial additives. This preference aligns well with plant based cookies which often emphasize whole food ingredients. Brands that successfully communicate the health and ethical benefits of their products can capture a growing segment of conscientious consumers. Innovation in texture and flavor remains critical to ensuring that these alternatives meet the sensory expectations of traditional cookie lovers.

Integration of Sustainable Packaging and Eco Friendly Practices

The environmental sustainability in consumer purchasing behavior prompting cookie manufacturers to adopt greener practices is additionally leveraging the growth of cookies market. The use of recyclable biodegradable or compostable packaging materials helps reduce plastic waste and aligns with circular economy principles. According to research, only 32% of plastic packaging waste in the European Union was recycled in 2022 with the urgent need for improvement. Companies are responding by transitioning to paper-based wrappers and mono material films that are easier to recycle. As per study, 65% of European consumers consider packaging sustainability when making buying decisions. This shift not only reduces environmental impact but also strengthens brand loyalty among eco aware demographics. Furthermore, manufacturers are investing in energy efficient production facilities and sourcing ingredients from sustainable farms. Certifications such as Rainforest Alliance for cocoa and Fairtrade for sugar enhance credibility and appeal to ethically minded shoppers. Retailers increasingly favor suppliers with strong environmental credentials providing competitive advantage to sustainable brands. The transition to green practices also mitigates regulatory risks as governments impose stricter rules on single use plastics. By prioritizing sustainability cookie producers can differentiate themselves in a crowded market and contribute to broader environmental goals. This strategic focus ensures long term viability and resonates with the values of modern consumers.

MARKET CHALLENGES

Intense Competition from Private Label Brands

The private label cookies, as retailers improve quality and expand variety, while maintaining lower prices is a challenge for the growth of cookies market. This trend poses a serious challenge to national and international brands that rely on brand equity to justify premium pricing. According to the Private Label Manufacturers Association, private label products account for 38% of total supermarket sales in several European countries. Retailers invest heavily in product development and marketing to enhance the appeal of their own brands. The private label cookie sales grew by 9% in 2023, outpacing branded counterparts. Consumers perceive these products as offering better value for money especially during periods of economic uncertainty. The quality gap between private label and branded cookies has narrowed significantly with many store brands using similar ingredients and production methods. This parity makes it difficult for established brands to differentiate themselves solely on taste or texture. Additionally, retailers prioritize shelf space for their own labels reducing visibility for competitor products. This behavior increases price sensitivity and reduces brand loyalty. Established manufacturers must therefore innovate continuously and invest in marketing to maintain relevance. However, the cost of such efforts can strain resources and impact profitability. The dominance of private labels thus represents a persistent challenge that requires strategic adaptation to sustain market position.

Supply Chain Disruptions and Logistical constraints

The ongoing challenges from supply chain instabilities caused by geopolitical conflicts labor shortages and transportation delays is additionally to limit the growth of cookies market. These disruptions affect the timely delivery of raw materials and finished goods leading to stockouts and increased inventory costs. According to the study, supply chain constraints contributed to a 15% increase in logistics costs for food manufacturers in 2023. The reliance on global sourcing for ingredients such as cocoa and vanilla exposes producers to international trade barriers and customs delays. Labor shortages in the transportation sector further exacerbate these issues with a deficit of 400000 truck drivers, across the European Union. This shortage limits the capacity to distribute products efficiently particularly during peak demand seasons. Additionally, energy price volatility affects production schedules and cold storage operations for perishable ingredients. These factors combine to create an unpredictable operating environment where manufacturers struggle to maintain consistent supply. Stockouts not only result in lost sales but also damage brand reputation as consumers switch to available alternatives. Companies must therefore invest in diversified supply chains and advanced logistics technologies to mitigate risks. However, these adaptations require substantial capital investment and operational restructuring posing a significant challenge for the industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.96% |

| Segments Covered | By Ingredient, Product Type, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Parle Products Private Limited, Danone S.A., Mondelēz International, The Campbell Soup Company, Britannia Industries Ltd, PepsiCo, Nestlé S.A., and The Kellogg Company |

SEGMENTAL ANALYSIS

By Ingredient Insights

The chocolate and chocolate chip cookies segment was the largest by holding 35.3% of global cookies market share in 2025. The growth of segment is driven by the deep-rooted psychological association between cocoa and comfort. According to the International Cocoa Organization, global demand for cocoa beans reached record levels in 2023 with consumption exceeding 4.9 million metric tons. The versatility of chocolate allows it to pair effectively with various textures including chewy centers and crisp edges. Manufacturers leverage this preference by introducing premium dark chocolate options which appeal to health conscious consumers seeking antioxidants. Furthermore, the widespread availability of high quality cocoa derivatives enables consistent product quality across mass market brands. Retailers prioritize shelf space for chocolate varieties due to their high turnover rates. Marketing campaigns often emphasize the richness and decadence of chocolate which resonates strongly with impulse buyers. The emotional reward associated with consuming chocolate drives habitual purchasing behavior making it a staple in household pantries.

The coconut and honey segment is anticipated to register a fastest CAGR of 6.8% during the forecast period owing to the shifting consumer preference towards natural and functional ingredients. Honey is perceived as a healthier alternative to refined sugar offering additional health benefits such as antimicrobial properties. Coconut adds a tropical flair and provides healthy fats which align with ketogenic and paleo dietary trends. The combination of honey and coconut creates a unique flavor profile that appeals to adventurous eaters. Manufacturers are launching gluten free and vegan cookies using these ingredients to cater to specific dietary needs. A survey found that 45% of consumers actively seek products with clean labels and recognizable ingredients. Retailers are expanding their health food aisles to accommodate these innovative products. Social media influencers often promote coconut and honey cookies as guilt free treats further stimulating demand.

By Product Insights

The drop cookies segment held 40.3% of the global cookies market share in 2025 with the simplicity of the manufacturing process, which involves dropping spoonfuls of dough onto baking sheets. This method allows for high volume production and consistent quality control. According to the American Bakers Association, drop cookies account for the majority of commercial bakery output due to their efficiency. The versatility of drop cookies enables manufacturers to experiment with various ingredients such as nuts fruits and chocolates. The familiar texture and appearance resonate with consumers across all age groups. Retailers favor drop cookies because they have a long shelf life and are less prone to breakage during transportation. The cost effectiveness of production allows for competitive pricing which drives volume sales. Additionally, the homemade aesthetic of drop cookies appeals to consumers seeking comfort foods. Marketing campaigns often evoke nostalgia associating drop cookies with family gatherings and holidays. This emotional connection strengthens brand loyalty. Manufacturers continuously introduce new variations such as double chocolate or white chocolate macadamia to maintain consumer interest.

The sandwich cookies segment is swiftly emerging at an anticipated CAGR of 7.2% from 2026 to 2034 with the demand for indulgent snacks that offer a dual texture experience. The combination of two crisp cookies with a creamy filling provides a satisfying mouthfeel that appeals to modern consumers. According to study, sales of sandwich cookies increased by 10% globally in 2023 driven by new flavor launches. The versatility of fillings allows for endless innovation including fruit jams marshmallows and flavored creams. These consumers seek experiential snacking options that are Instagram worthy. Social media platforms are flooded with images of colorful and creative sandwich cookies which stimulates demand. Manufacturers are responding by introducing limited edition collaborations with popular candy brands. Retailers are expanding their confectionery aisles to include premium sandwich cookie brands. The perception of sandwich cookies as a treat rather than a staple allows for higher price points. Additionally, the rise of single serve packaging aligns with portion control trends.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest by accounting for 55.3% of the global cookie market share in 2025 with the extensive shelf space allocated to snack foods and the convenience of one stop shopping. The visibility of cookies in high traffic aisles encourages impulse purchases. Retailers use strategic placement such as end caps and checkout counters to maximize exposure. The wide variety of brands and flavors available in supermarkets caters to diverse consumer preferences. Bulk buying options appeal to families and large households looking for value. The established logistics networks of supermarket chains ensure consistent product availability. Private label cookies in supermarkets offer competitive pricing which attracts budget conscious shoppers. The trust consumers place in major retail chains enhances brand credibility. Loyalty programs and digital coupons further incentivize purchases. Supermarkets also facilitate the launch of new products through sampling events and featured placements. This comprehensive approach ensures that supermarkets remain the primary destination for cookie purchases. The integration of online grocery services with physical stores further strengthens this channel.

The online sales segment is likely to witness a fastest CAGR of 9.5% from 2026 to 2034 owing to the expansion of e-commerce platforms and the rise of direct to consumer models. Consumers appreciate the convenience of home delivery and the ability to compare prices easily. The pandemic accelerated the adoption of online grocery shopping a trend that has persisted. Specialty cookie brands benefit from online channels by reaching niche audiences without the need for physical retail presence. Subscription services offer regular deliveries of fresh cookies enhancing customer loyalty. The ability to customize orders and access exclusive online flavors drives engagement. Retailers are investing in faster delivery options such as same day shipping to meet consumer expectations. The wide assortment available online surpasses physical store limitations. Consumers can access international brands and artisanal products that are not locally available.

REGIONAL ANALYSIS

North America Cookies Market Analysis

North America was the largest contributor of the global cookies market by capturing 35.4% of share in 2025 with the high per capita consumption and the presence of major multinational corporations. According to the study, the United States alone consumes over 2 billion pounds of cookies annually. Innovation in health focused products, such as gluten free and low sugar options drives growth. The well-developed retail infrastructure ensures widespread availability. E commerce penetration is high facilitating direct to consumer sales. The trend towards premiumization is strong with consumers willing to pay for high quality ingredients. Seasonal promotions during holidays such as Halloween and Christmas boost sales significantly. The region also leads in the adoption of sustainable packaging practices. Regulatory support for food safety and labeling enhances consumer trust. The diverse population drives demand for varied flavors and types. The robust economic environment supports discretionary spending on snacks. North America remains the benchmark for global cookie trends and innovations.

Europe Cookies Market Analysis

Europe cookies market was positioned second by holding 28.4% of the global cookies market share in 2025 with a strong tradition of baking and high quality standards. According to research, the European Union produces over 6 million tons of bakery products annually. Consumer preference for artisanal and organic cookies is prominent. Strict regulations on sugar and additives drive innovation in healthier formulations. The rise of private label brands offers competitive alternatives to national brands. Retailers focus on sustainability and ethical sourcing which resonates with European consumers. The diverse culinary landscape supports a wide variety of cookie types from shortbread to biscotti. Economic stability in Western Europe supports consistent demand. Eastern Europe is experiencing growth due to rising disposable incomes. The influence of health trends is significant with consumers seeking clean label products. Digital transformation in retail enhances online sales channels. Cross border trade within the EU facilitates market expansion.

Asia Pacific Cookies Market Analysis

Asia Pacific cookies market growth is esteemed to grow at a fastest CAGR in coming years with the rapid urbanization and rising disposable incomes. According to the survey, middle class consumption in the region is expected to double by 2030. Changing lifestyles lead to increased demand for convenient snacks. Western influence introduces new cookie varieties to traditional markets. Local manufacturers are adapting global recipes to suit regional tastes. The popularity of e commerce facilitates access to diverse products. Young consumers are the primary drivers of demand seeking trendy and innovative snacks. Health consciousness is rising leading to demand for fortified and low sugar options. Retail expansion in tier two and three cities opens new markets. Government initiatives to support food processing industries boost production. The region benefits from a large population base ensuring volume growth. Cultural festivals and gifting traditions drive seasonal sales. International brands are entering the market through joint ventures and acquisitions.

Latin America Cookies Market Analysis

Latin America cookies market growth is propelled with the strong culture of sweet consumption and family oriented snacking. According to the study, food and beverage consumption in the region is resilient despite economic fluctuations. Affordability is a key factor influencing purchasing decisions. Local brands dominate the market with competitive pricing. International brands are present but face competition from established local players. The rise of modern retail formats, such as supermarkets enhances distribution. Economic volatility poses challenges but also drives demand for value packs. Innovation in flavors such as dulce de leche and tropical fruits appeals to local tastes. Health trends are emerging but price sensitivity remains high.

Middle East and Africa Cookies Market Analysis

The Middle East and Africa cookies market growth is driven by urbanization and the influence of Western dietary habits. Ramadan and other religious festivals drive significant seasonal demand. Local production is increasing to reduce reliance on imports. Health awareness is rising leading to demand for healthier options. International brands are expanding their presence through partnerships. Retail infrastructure is improving with the growth of supermarkets. E-commerce is nascent but growing rapidly. Price sensitivity varies across the region with affluent consumers seeking premium products. Supply chain challenges persist in some African countries. Government initiatives to support local agriculture benefit ingredient sourcing. The young population demographic supports long term growth potential. Manufacturers are adapting products to local tastes and preferences.

COMPETITIVE LANDSCAPE

The Cookies Market features intense competition characterized by the presence of established multinational corporations and numerous regional players. Major companies leverage strong brand recognition and extensive distribution networks to maintain dominance while smaller entities focus on niche segments such as organic or artisanal products. Innovation serves as a critical differentiator with firms continuously introducing new flavors and healthier alternatives to capture consumer interest. Price competition remains significant particularly in the mass market segment where private label brands offer affordable options. Strategic mergers and acquisitions are common as companies seek to consolidate market power and expand their geographic reach. Sustainability has emerged as a key competitive factor with brands emphasizing ethical sourcing and eco friendly packaging to appeal to environmentally conscious buyers. Digital marketing and e commerce capabilities are increasingly vital for engaging consumers and driving sales.

KEY MARKET PLAYERS

Some of the notable key players in the global cookies market are

- Parle Products Private Limited

- Danone S.A.

- Mondelēz International

- Campbell Soup Company

- Britannia Industries Ltd

- PepsiCo

- Nestlé S.A.

- The Kellogg Company

Top Players in the Market

- Mondelez International stands as a dominant force in the global cookies sector through its iconic brands such as Oreo and Chips Ahoy. The company leverages extensive distribution networks to ensure widespread availability across diverse markets. Recent strategic initiatives focus on digital transformation and direct to consumer engagement to enhance brand loyalty. Mondelez invests heavily in sustainable sourcing practices particularly for cocoa which strengthens its supply chain resilience. The corporation actively innovates product portfolios by introducing reduced sugar and plant-based variants to align with evolving health trends. Its robust marketing campaigns utilize social media platforms to connect with younger demographics effectively. The company also emphasizes packaging sustainability to meet regulatory requirements and consumer expectations for environmental responsibility.

- Nestlé S.A. maintains a strong presence in the cookies market with popular brands like Toll House and Foxs Crystal Clear. The company focuses on nutritional enhancement by reformulating products to reduce sodium and sugar content. Nestlé integrates advanced manufacturing technologies to improve production efficiency and product consistency. Recent efforts include expanding its portfolio of organic and gluten free options to cater to health conscious consumers. The corporation emphasizes ethical sourcing and community development programs to build brand trust and credibility. Nestlé utilizes data analytics to understand consumer preferences and drive targeted marketing strategies. Its global reach allows for rapid deployment of innovative products across multiple regions. The company also invests in sustainable packaging solutions to minimize environmental impact.

- Ferrero Group has significantly expanded its footprint in the cookies segment through strategic acquisitions and organic growth. The company owns renowned brands such as Keebler and Famous Amos which contribute to its diverse portfolio. Ferrero focuses on premiumization by offering high quality ingredients and unique flavor profiles. Recent actions include investing in state of the art production facilities to enhance capacity and efficiency. The group emphasizes sustainability by committing to responsible sourcing of palm oil and cocoa. Ferrero leverages its strong brand equity to launch limited edition products that generate consumer excitement. The company also enhances its digital capabilities to improve customer engagement and e commerce performance.

Top Strategies Used by the Key Market Participants

Key players in the Cookies Market primarily employ product innovation and diversification to maintain competitive advantage. Companies frequently launch new flavors and textures to attract discerning consumers seeking novel experiences. Strategic acquisitions enable firms to expand their portfolios and enter new geographic regions efficiently. Investment in sustainable sourcing and eco friendly packaging addresses growing environmental concerns among shoppers. Digital transformation initiatives enhance direct to consumer channels and personalize marketing efforts. Manufacturers also focus on health oriented formulations by reducing sugar and incorporating functional ingredients. Partnerships with retailers ensure optimal shelf placement and visibility for flagship brands. Cost optimization through automated production processes improves margins and operational efficiency.

MARKET SEGMENTATION

This research report on the global cookies market has been segmented and sub-segmented based on the product type, distribution channel, and region.

By Product

- Molded

- Rolled

- Bar

- Drop

By Ingredients

- Chocolate

- Chocolate chip

- Oatmeal

- Butter

- Cream

- Ginger

- Coconut

- Honey

By Distribution Channel

- Offline

- Online

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the cookies market?

The cookies market includes the global production, distribution, and sale of various cookie products such as chocolate chip, buttery, cream-filled, and specialty cookies.

2. What factors are driving the growth of the cookies market?

Growing demand for convenient snacks, product innovation, rising disposable incomes, and the popularity of indulgent and premium cookies are major growth drivers.

3. Which region dominates the global cookies market?

North America holds a significant share due to high consumption and widespread product availability.

4. What are the key types of cookies available in the market?

Common types include bar cookies, drop cookies, molded cookies, sandwich cookies, and specialty health-focused cookies.

5. Who are the major players in the cookies market?

Leading companies include Parle Products Private Limited, Danone S.A., Mondelēz International, Campbell Soup Company, Britannia Industries Ltd, PepsiCo, Nestlé S.A., and The Kellogg Company.

6. How is consumer preference evolving in the cookies market?

Consumers increasingly prefer healthier, low-sugar, gluten-free, and organic cookie variants.

7. What innovations are shaping the cookies market?

Innovations include plant-based cookies, protein-packed cookies, premium gourmet ingredients, and sustainable packaging.

8. How has e-commerce impacted cookie sales?

Online retail has boosted cookie sales by making a wide variety of brands and flavors more accessible to consumers.

9. What ingredients are commonly used in cookie production?

Key ingredients include flour, sugar, butter or oil, chocolate, nuts, flavorings, and preservatives.

10. What challenges does the cookies market face?

Challenges include fluctuating raw material costs, rising health concerns over sugar content, and growing competition from healthier snack alternatives.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com