Europe Dairy Processing Equipment Market Segmented By Application (Cheese, Yogurt, Processed Milk, Mild Powder, Proteins), Type (Homogenizers, Pasteurizers, Separators, Evaporators, Membrane Filtration), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores and Online Stores), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) – Size, Share, Trends, Growth, Forecast (2026 to 2034)

Market Size, 2025

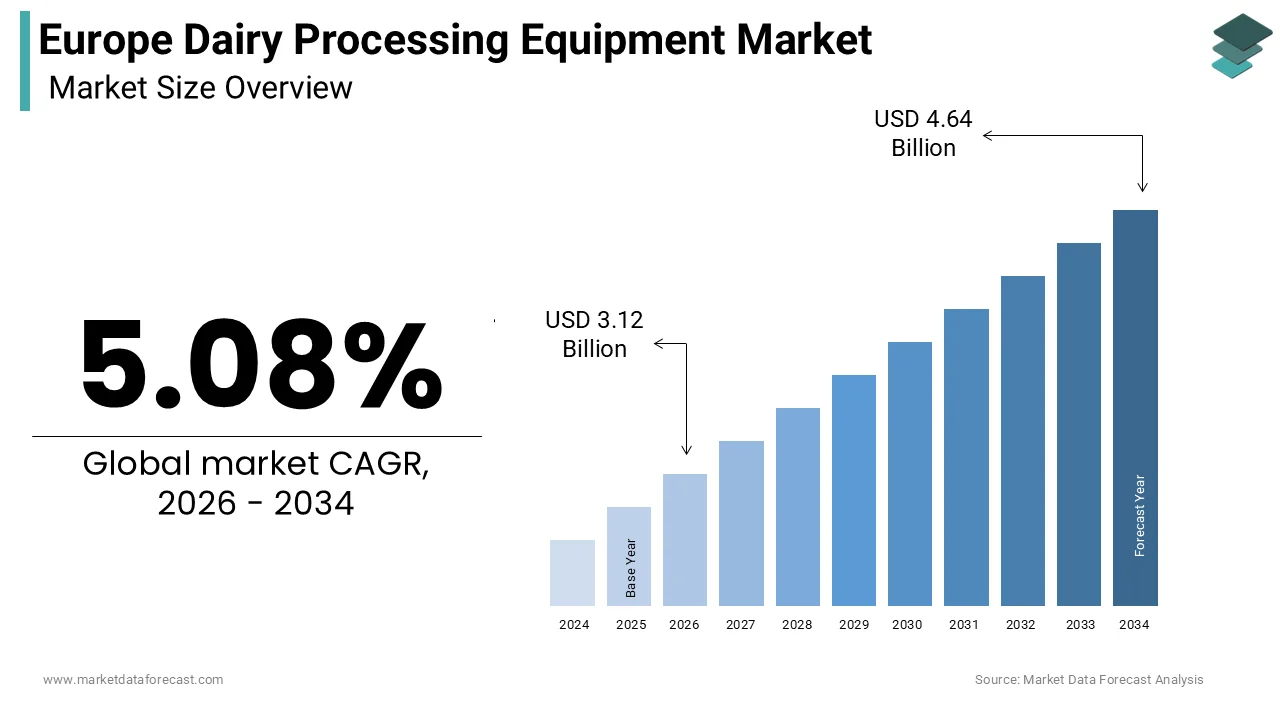

$2.97 BnMarket Estimate, 2026

$3.12 BnMarket Forecast, 2034

$4.64 BnCAGR, 2026–2034

5.08%Executive Summary: Europe Dairy Processing Equipment Market

- Market Scope: European dairy processing equipment market analysis covering machinery types, application sectors, regional leadership frameworks, and adoption metrics.

- Market Valuation: Valued at USD 2.97 billion (2025), estimated at USD 3.12 billion (2026), and projected to reach USD 4.64 billion by 2034, growing at a robust CAGR of 5.08% (2026–2034).

- Primary Growth Drivers: Industrial modernization, stringent food-safety compliance, and rising demand for value-added dairy products (with EU farms producing 160.8 million tonnes of raw milk in 2023 and >40% of new dairy launches featuring functional claims). Key operational metrics include >65% of new equipment installations featuring automated Clean-in-Place systems, membrane filtration reducing water consumption by up to 40%, and mechanical vapor recompression evaporators lowering thermal energy use by up to 80%.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Equipment Type | Separators (held the largest equipment-type share in 2025, with modern units processing up to 40,000 liters per hour and recovering >98% of residual fat) | Membrane filtration (identified as the fastest-growing equipment segment at a 13.1% CAGR driven by advanced fractionation and concentration needs) |

| By Application | Cheese processing (commanded the leading share, supported by average European cheese consumption of 18.5 kg per person annually) | Dairy proteins and functional ingredients (forecast to grow at an 11.7% CAGR driven by nutritional product demand) |

| By Region | Germany (dominated Europe with 22.5% market share in 2025, processing over 33 million tons of milk annually, with >75% of new equipment installations incorporating IoT connectivity and energy recovery) | Germany (identified as the fastest-growing national market driven by advanced smart-factory retrofits and high automation adoption) |

Major Market Players & Market Structure

Market Structure: Highly competitive European dairy processing equipment landscape featuring 10 major market leaders competing on advanced automation, IoT-enabled processing lines, extreme energy and water efficiency, modular systems, membrane filtration innovation, and strict regulatory compliance.

Key Companies: Krones Group, GEA Group, A&B Processing, ISF Industries, Alfa Laval Corp, Tetra Laval International, Feldmeier Equipment, IDMC, SPX Corp, and Agrometal Ltd.

Europe Dairy Processing Equipment Market Size

The Europe Dairy Processing Equipment Market size was calculated to be USD 2.97 billion in 2025 and is anticipated to be worth USD 4.64 billion by 2034, from USD 3.12 billion in 2026, growing at a CAGR of 5.08% during the forecast period.

Dairy processing equipment includes a specialized array of machinery and systems designed for the hygienic and efficient transformation of raw milk into a wide spectrum of value-added products, including cheese, yogurt, butter milk powder, and functional dairy beverages. In Europe, this equipment must comply with stringent food safety standards under Regulation EC 852 2004 and meet the operational demands of both large-scale cooperatives and artisanal producers. According to Eurostat, EU farms produced 160.8 million tonnes of raw milk in 2023, which indicates the scale and economic importance of the sector. The European Commission’s Farm to Fork Strategy drives modernization by mandating a 50% reduction in food waste and 25% organic farmland by 2030, prompting processors to invest in precision separation, energy-efficient pasteurization, and closed-loop cleaning systems. Technological evolution is accelerating with the integration of automation, IoT sensors, and modular skid-mounted units, which enhance traceability, reduce water consumption, and support flexible production of niche products such as lactose-free and plant-dairy hybrids. This convergence of regulatory compliance, sustainability mandates, and consumer diversification defines the contemporary landscape of the Europe dairy processing equipment market.

MARKET DRIVERS

Stringent EU Food Safety and Hygiene Regulations Drive Equipment Modernization

The European Union’s rigorous food safety framework acts as a primary catalyst for continuous investment in advanced dairy processing equipment, which is majorly driving the growth of the Europe dairy processing equipment market. According to Regulation (EC) 852/2004, all dairy facilities must implement Hazard Analysis and Critical Control Points (HACCP) systems and use equipment constructed from food‑grade stainless steel with smooth, non‑porous surfaces to prevent microbial harborage. According to the European Food Safety Authority (EFSA, 2023), more than 1,200 food safety non‑compliance cases in dairy plants were linked to outdated or poorly maintained equipment, prompting intensified inspections. In response, major processors in Germany, France, and the Netherlands have accelerated upgrades, with over 65% of new installations between 2022 and 2025 featuring automated Clean‑in‑Place (CIP) systems that validate sanitation through real‑time conductivity and temperature monitoring. As per the European Commission’s Official Controls Regulation (EU) 2017/625, unannounced audits further incentivize capital expenditure on compliant machinery. As per the EU Organic Regulation (EC) 834/2007, dedicated equipment or validated cleaning protocols are required for organic lines, increasing demand for modular and easily sanitized units. This regulatory pressure transforms compliance from a cost into a strategic driver of equipment renewal across Europe’s dairy landscape.

Rising Demand for Value‑Added and Functional Dairy Products

The European consumer shift toward premium, differentiated, and health‑oriented dairy products is compelling processors to adopt flexible and specialized processing equipment, which is further boosting the expansion of the Europe dairy processing equipment market. According to the European Dairy Association (2023), more than 40% of new dairy launches featured functional claims such as added protein, probiotics, or reduced sugar, driving demand for precision fermentation tanks, membrane filtration systems, and aseptic filling lines. As per the European Food Information Council (EUFIC, 2023), 58% of consumers actively seek high‑protein dairy snacks, with Greek‑style yogurt production alone growing by ~12% annually. This trend necessitates high‑capacity centrifugal separators for whey protein concentration and ultrafiltration units capable of producing milk protein concentrates above 80% purity, as validated by University of Copenhagen trials. According to Eurostat (2023), the lactose‑free dairy market in Europe is valued at €2.8 billion, requiring inline lactase dosing and enzymatic reactors integrated into pasteurization lines. Artisanal cheese makers are also investing in programmable vats with temperature and pH control to replicate terroir‑driven profiles under Protected Designation of Origin (PDO) schemes. This product diversification mandates equipment versatility, precision, and scalability across both industrial and craft segments.

MARKET RESTRAINTS

High Capital Investment and Long ROI Cycles Deter Small Producers

The substantial upfront cost and extended return on investment timeline for advanced dairy processing equipment present significant barriers for small and medium‑sized dairies, which is a significant restraint to the growth of the Europe dairy processing equipment market, particularly in Southern and Eastern Europe. As per the European Commission’s Agricultural Machinery Cost Index, a complete automated cheese production line with integrated cleaning and packaging can exceed €3 million, while a high‑capacity ultrafiltration skid for protein concentration costs more than €800,000. These figures are prohibitive for the ~15,000 small dairies in Europe processing less than 10,000 tons of milk annually (European Milk Board). According to the European Investment Bank (2023), only 28% of dairy SMEs secured equipment financing due to stringent collateral requirements and perceived operational risk. Consequently, many smaller players rely on second‑hand machinery, which often fails to meet current hygiene or energy efficiency standards, increasing non‑compliance risk. National support schemes exist but remain fragmented: as per Italy’s Rural Development Program, only ~40% of eligible modernization costs are covered, with complex application processes. Without coordinated EU‑level financing mechanisms or equipment leasing models, the modernization gap between large cooperatives and small dairies will continue to widen, undermining sector‑wide sustainability and safety goals.

Skilled Labor Shortages in Equipment Operation and Maintenance

The increasing sophistication of dairy processing systems has outpaced the availability of technicians and engineers trained in automation, digital controls, and sanitary engineering across Europe, which is further hindering the Europe dairy processing equipment market growth. According to the European Dairy Association (2023), more than 60% of dairy processors reported critical staffing gaps in maintenance and process engineering, with the most acute shortages in Germany, Poland, and Spain. Modern equipment featuring IoT sensors, variable frequency drives, and CIP automation requires specialized knowledge that traditional vocational programs have not yet fully integrated. As per CEDEFOP (2025), only 11 EU member states offered certified curricula in food processing equipment technology. This deficit leads to extended downtime: according to the European Commission’s Food Processing Observatory, unplanned stoppages averaged 14 days annually per plant due to unresolved technical issues. Manufacturers such as GEA and Tetra Pak now include remote diagnostics and augmented reality support to mitigate this gap, but on‑site expertise remains essential for complex repairs. Until training systems align with technological advancement, equipment performance and food safety will remain compromised in many European dairies.

MARKET OPPORTUNITIES

Integration of Energy Efficient and Water Recycling Technologies

The European Green Deal and national decarbonization targets are creating a strategic opportunity for the Europe dairy processing equipment market. As per the European Environment Agency, the dairy sector accounts for 2.1% of the EU’s industrial energy consumption, with pasteurization and evaporation being the most energy‑intensive steps. In response, equipment providers have introduced mechanical vapor recompression evaporators that reduce thermal energy use by up to 80% and heat recovery units that capture waste heat from cooling systems. According to the Netherlands Enterprise Agency, Dutch dairies adopting these technologies cut energy costs by €250,000 annually per facility. Additionally, closed‑loop water recycling systems now recover and purify over 90% of process water through membrane bioreactors and ultrafiltration, as demonstrated in Arla’s pilot plant in Denmark. As per the European Commission’s Eco‑Innovation Program, €75 million was allocated in 2023 to support the adoption of such systems through the Dairy 2030 Initiative. With the EU Carbon Border Adjustment Mechanism potentially affecting food exports, these green technologies position European dairies for both regulatory compliance and global competitiveness.

Expansion of Modular and Skid‑Mounted Processing Units

The growing demand for localized production, flexible product runs, and rapid capacity scaling is driving adoption of modular and skid‑mounted dairy processing systems across Europe, which is another promising opportunity for the Europe dairy processing equipment market. These prefabricated units integrate homogenizers, separators, pasteurizers, and filling lines into compact mobile or containerized formats that can be deployed within weeks rather than years. As per the European Federation of Food Science and Technology, more than 120 modular dairy units were installed in 2023, primarily by startups and cooperatives producing plant‑dairy hybrids, specialty cheeses, and regional yogurts. According to the European Commission’s Smart Villages Initiative, modular processing hubs in rural areas are being funded to reduce raw milk transport and support local economies. Companies such as SPX Flow and IDMC now offer skid‑based lactose‑free milk lines that process 2,000 liters per hour with full CIP automation, enabling small dairies to enter high‑value segments without major infrastructure. Furthermore, these units comply with EU hygiene standards through seamless welded surfaces and integrated validation protocols. This plug‑and‑play approach democratizes access to advanced technology and aligns with Europe’s circular and decentralized food system vision.

MARKET CHALLENGES

Fragmented Equipment Standards Across Member States

Despite EU‑level food safety regulations, technical standards for dairy processing equipment installation and validation remain inconsistent across member states, which is creating compliance complexity and market entry barriers and is one of the major challenges to the Europe dairy processing equipment market. According to the European Committee for Standardization, national interpretations of EN 1672:2009 for food machinery hygiene vary significantly, with Germany requiring additional third‑party certification from TÜV while France accepts manufacturer self‑declarations. This divergence increases costs for equipment suppliers who must adapt control panels, documentation, and material certifications for each market. As per the European Dairy Association, 45% of equipment delays in 2023 were due to conflicting national requirements for pressure equipment or electrical safety under the Machinery Directive. Additionally, validation protocols for Clean‑in‑Place systems differ, with Nordic countries mandating weekly ATP swabbing while Southern Europe relies on visual inspection. These inconsistencies hinder the free movement of standardized equipment and delay modernization, particularly for multi‑country operators. Without harmonized technical annexes under a unified EU dairy equipment code, investment efficiency and food safety outcomes will remain suboptimal across the single market.

Supply Chain Vulnerabilities for Critical Components

The dairy processing equipment sector in Europe faces growing exposure to global supply chain disruptions, particularly for high‑precision components such as variable frequency drives, sensors, and food‑grade pumps, which further challenge the expansion of the Europe dairy processing equipment market. As per the European Commission’s Industrial Raw Materials Scoreboard, more than 65% of high‑end pressure transducers and 50% of stainless‑steel sanitary valves are sourced from outside the EU, primarily from the United States and Japan. According to the German Engineering Federation, the 2022 semiconductor shortage delayed delivery of automated control systems by up to nine months. Geopolitical tensions and export controls further amplify risk, with recent restrictions on high‑purity nickel alloys affecting the production of aseptic fillers. European manufacturers such as Alfa Laval and Krones have responded by qualifying alternative suppliers and increasing local inventory, but lead times for critical spares remain volatile. As per the European Central Bank’s 2023 supply chain risk assessment, 30% of dairy equipment projects experienced cost overruns due to component scarcity. Until strategic stockpiling and nearshoring of key subassemblies are implemented, the resilience of Europe’s dairy processing infrastructure will remain contingent on fragile global logistics networks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.08% |

| Segments Covered | By Equipment Type, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Krones Group, GEA Group, A&B Processing, ISF Industries, Alfa Laval Corp, Tetra Laval International, Feldmeier Equipment, IDMC, SPX Corp, and Agrometal Ltd |

SEGMENTAL ANALYSIS

By Equipment Type Insights

The separators segment held the largest share in the Europe dairy processing equipment market in 2025. The dominance of the separators segment in this regional market is majorly due to their indispensable role in standardizing milk fat content, producing skim milk and cream, and recovering fat from whey across all dairy applications. As per the European Dairy Association, more than 230 million tons of raw milk processed annually in the EU require separation as the first critical step before further processing. Modern high‑capacity disc stack separators can process up to 40,000 liters per hour with fat accuracy within 0.01%, enabling precise formulation for yogurt, cheese, and infant formula. According to the European Commission’s milk quality directive, fat standardization is mandated for all commercial dairy products, reinforcing universal adoption. Additionally, separators are essential in whey valorization, with advanced models recovering over 98% of residual fat for butter oil production, as validated by trials at the University of Hohenheim. Leading manufacturers such as Alfa Laval and GEA dominate the segment with units featuring automated bowl cleaning and IoT‑enabled performance monitoring to minimize downtime. This foundational function across every dairy stream ensures separators remain the most widely deployed equipment type in Europe.

The membrane filtration segment is the fastest-growing equipment segment in the Europe dairy processing equipment market and is anticipated to register a CAGR of 13.1% over the forecast period, owing to the rising need for precision protein concentration, lactose reduction, and water recovery in response to consumer and regulatory pressures. As per the European Food Safety Authority, more than 70% of new high‑protein dairy products launched in 2023 required ultrafiltration or microfiltration to achieve target protein levels without additives. According to the European Environment Agency, membrane systems reduce water consumption by up to 40% through permeate recycling, aligning with the EU’s water efficiency targets. Furthermore, the ban on palm oil in infant formula has increased demand for microfiltration to produce native milk fat globule membranes as clean‑label emulsifiers. Companies such as Tetra Pak and IDMC have introduced skid‑mounted nanofiltration units that concentrate minerals for functional beverages while retaining flavor. As per the EU’s Farm to Fork Strategy, resource efficiency and clean‑label formulations are prioritized, making membrane filtration a strategic investment across both industrial and artisanal dairies.

By Application Insights

The cheese processing segment commanded the leading share of the Europe dairy processing equipment market in 2025. The growth of the cheese processing segment in this regional market is driven by Europe’s deep‑rooted cheesemaking heritage, high per capita consumption, and expanding artisanal and protected designation of origin production. As per the European Dairy Association, Europeans consume an average of 18.5 kilograms of cheese per person annually, with France, Germany, and Italy alone accounting for over 40% of EU cheese output. According to the European Commission’s Protected Designation of Origin registry, more than 250 cheese varieties require specialized equipment such as programmable curd cutters, temperature‑controlled vats, and aging chambers with precise humidity management. Industrial‑scale producers are also investing in high‑capacity automated lines to meet rising demand for sliced, shredded, and ready‑to‑eat formats, with Eurostat reporting a 9% annual increase in processed cheese sales between 2021 and 2023. Furthermore, according to the European Green Deal framework, whey valorization is incentivized with equipment for ultrafiltration and spray drying integrated into cheese plants to convert byproducts into protein concentrates. This fusion of cultural tradition, regulatory specificity, and industrial innovation ensures that cheese remains the dominant application for dairy processing equipment across Europe.

The protein segment is the fastest-growing application segment in the Europe dairy processing equipment market and is estimated to record a CAGR of 11.7% over the forecast period, owing to the escalating consumer demand for high‑protein dairy snacks, functional beverages, and sports nutrition products. As per the European Food Information Council, 62% of European consumers actively seek added protein in their diets, with Greek‑style yogurt and whey protein drinks leading new product launches. This trend necessitates advanced membrane filtration systems capable of producing milk protein concentrates above 85% purity and diafiltration units for lactose reduction. According to the European Dairy Association, more than 200 new protein enrichment projects were initiated in 2023 across Germany, the Netherlands, and Denmark, with average investment exceeding €2 million per facility. Additionally, as per the EU’s Protein Plan, domestic production of dairy‑based proteins is prioritized to reduce reliance on imported soy, creating policy tailwinds. Equipment manufacturers such as SPX Flow and GEA have responded with modular skid‑mounted ultrafiltration systems that enable small dairies to enter this high‑margin segment. This convergence of health trends, policy support, and technological accessibility drives rapid expansion in protein‑focused dairy processing.

REGIONAL ANALYSIS

Germany Dairy Processing Equipment Market Analysis

Germany dominated the Europe dairy processing equipment market in 2025 by holding 22.5% of the regional market share. The dominance of Germany in the European market is majorly driven by its position as Europe’s largest milk producer, with over 33 million tons collected annually, and its dense network of cooperatives and industrial dairies. German processors lead in automation, with over 75% of new equipment installations between 2022 and 2025 featuring IoT connectivity and energy recovery systems, according to the German Engineering Federation. The National Energy Efficiency Act mandates a 20% energy reduction in food processing by 2027, accelerating the adoption of mechanical vapor recompression evaporators and heat pump dryers. Additionally, Germany hosts global equipment leaders like GEA and Krones, whose R&D centers in Stuttgart and Berlin pioneer next‑generation hygienic design. The Milk 2030 initiative, funded by the Federal Ministry, supports SMEs in upgrading to compliant and efficient systems.

France Dairy Processing Equipment Market Analysis

France plays a pivotal role in the European dairy equipment market. The growth of France in this regional market is anchored in its world‑renowned cheese diversity, with over 400 varieties requiring specialized vats, cutters, and aging infrastructure. The National Interprofessional Dairy Organization reports that over 150 artisanal dairies modernized their facilities in 2023 with modular units to meet EU hygiene standards while preserving traditional methods. Industrial players such as Lactalis and Savencia have invested heavily in automated protein concentration lines to expand into functional dairy beverages. Furthermore, France’s Energy Climate Law requires all food processors to conduct energy audits every four years, driving upgrades to pasteurizers and separators with heat recovery. The government’s France 2030 investment plan allocated €180 million to support digital and green transitions in dairy processing.

Netherlands Dairy Processing Equipment Market Analysis

The Netherlands exerts a strong influence as Europe’s dairy export hub, processing over 12 million tons of milk annually into butter, cheese, and milk powder. Dutch processors prioritize sustainability, with over 90% of large dairies using membrane filtration for water recycling and mechanical vapor recompression for evaporation, according to Wageningen University. FrieslandCampina’s Route 2030 strategy mandates carbon‑neutral processing by 2030, spurring investment in ammonia heat pumps and solar thermal integration. The Netherlands also leads in dairy equipment innovation, with companies such as SPX Flow and IDMC developing compact skid‑mounted units for emerging dairy startups. The Top Sector AgriFood program funded €50 million in 2023 for pilot projects on resource‑efficient processing.

Italy Dairy Processing Equipment Market Analysis

Italy remains a significant contributor to the European dairy equipment market, driven by its vast artisanal cheese sector with over 500 traditional varieties, including Parmigiano Reggiano and Mozzarella di Bufala, requiring precise temperature‑controlled vats and brining systems. The Italian National Association of Dairy Producers notes that over 200 small dairies upgraded to automated curd handling and CIP systems in 2023 to comply with EU hygiene audits. Industrial players such as Granarolo have expanded protein production lines to meet demand for high‑protein yogurt and beverages. Italy’s National Recovery and Resilience Plan allocated €120 million to support energy‑efficient equipment in agri‑food SMEs, with 40% subsidies for heat‑recovery pasteurizers and membrane filters. Southern regions are also adopting modular units to reduce raw milk transport and support local economies.

Denmark Dairy Processing Equipment Market Analysis

Denmark plays an outsized role in the European dairy equipment market owing to its cooperative dairy model, where over 90% of milk is processed by Arla Foods, which is a company that sets global benchmarks in sustainability and automation. Arla’s Dairy Chain 2030 strategy mandates zero waste and 50% lower emissions, driving investment in closed‑loop water systems and CO₂ heat pumps across its twelve European plants. The Danish Environmental Protection Agency requires all dairies to report energy and water use annually, incentivizing upgrades to high‑efficiency separators and evaporators. Denmark is also a pioneer in dairy protein innovation, with pilot plants in Aarhus using nanofiltration to produce mineral‑enriched milk for clinical nutrition. The government’s Green Tripartite Agreement provides low‑interest loans for green processing equipment, with over 85% uptake among SMEs.

COMPETITION OVERVIEW

Competition in the Europe Dairy Processing Equipment Market is defined by technological sophistication, regulatory compliance, and sustainability integration among a few global engineering leaders and specialized regional manufacturers. The landscape is dominated by GEA Tetra Pak and SPX FLOW, which offer comprehensive portfolios backed by decades of dairy process expertise. Rivalry centers on energy efficiency, automation hygiene validation, and total cost of ownership rather than initial price alone. Unlike generic machinery markets value is determined by integration capability, service support, and alignment with EU food safety and environmental directives. Emerging players face high barriers due to the need for CE certification, hygienic design certification, and long-term service networks. Innovation cycles are accelerating with digital twins, AI optimization, and circular water systems becoming differentiators. National dairy structures also influence competition as cooperative models in the Netherlands and Denmark favor integrated turnkey solutions, while artisanal sectors in France and Italy drive demand for flexible modular units. Success requires a deep understanding of both engineering rigor and Europe’s diverse dairy culture.

KEY MARKET PLAYERS

A few major players of the Europe dairy processing equipment market include

- Krones Group

- GEA Group

- A&B Processing

- ISF Industries

- Alfa Laval Corp

- Tetra Laval International

- Feldmeier Equipment

- IDMC

- SPX Corp

- Agrometal Ltd

Top Strategies Used by the Key Market Participants

Key players in the Europe Dairy Processing Equipment Market focus on four core strategies to maintain leadership. First, they embed energy and water efficiency into equipment design to align with EU Green Deal mandates and reduce operational costs for dairies. Second, they develop modular and skid-mounted systems to enable rapid deployment and accessibility for small and medium producers. Third, they integrate digital technologies such as IoT sensors, remote diagnostics, and AI-driven process control to enhance uptime, food safety, and traceability. Fourth, they align product innovation with consumer trends like high protein lactose free andclean-labell dairy through advanced membrane filtration and precision separation. Additionally, companies collaborate with major dairy cooperatives and research institutions to validate performance under real European production conditions. These strategies collectively address regulatory, economic and technological imperatives shaping Europe’s dairy processing future.

Leading Players in the Europe Dairy Processing Equipment Market

- GEA Group is a global leader in process engineering with deep roots in the Europe Dairy Processing Equipment Market, offering end-to-end solutions for cheese, yogurt, milk powder, and protein production. The company’s equipment portfolio integrates hygienic design, energy recovery, and digital process control to meet stringent EU food safety and sustainability standards. In 202,4 GEA launched its next-generation Eco separator series featuring real-time fat monitoring and 20% lower energy consumption, validated in trials with German and Dutch dairies. It also expanded its digital service platform GEA Smart Farm to provide remote diagnostics and predictive maintenance for dairy processors across Southern Europe. Through continuous innovation in resource efficiency and automation, GEA reinforces its position as a trusted engineering partner in Europe’s evolving dairy landscape.

- Tetra Pak plays a pivotal role in the Europe Dairy Processing Equipment Market by providing integrated processing and packaging lines with a strong focus on food safety, circularity, and digitalization. The company’s dairy systems are widely used for liquid milk, yogurt, and whey processing across both large cooperatives and mid-sized dairies. In early 2025, Tetra Pak introduced a modular membrane filtration skid for on-site protein concentration, enabling small producers to enter the high-protein dairy segment without major infrastructure. It also partnered with Arla Foods to deployAI-drivenn pasteurization controls that reduce energy use by 15% while maintaining safety. By aligning its technology with Europe’s Farm to Fork and Green Deal objectives, Tetra Pak strengthens its relevance across the continent’s sustainable dairy transformation.

- SPX FLOW exerts significant influence in the Europe Dairy Processing Equipment Market through its specialized solutions in separation, evaporation, and homogenization for both traditional and functional dairy applications. The company’s Anhydro and APV brands are recognized for robust performance in cheese whey and milk powder production across Northern and Central Europe. In 202,4 SPX FLOW unveiled a compact skid-mounted ultrafiltration system designed for lactose-free and high protein yogurt production with full Clean in Place automation. It also enhanced its digital offering with the FlowConnect platform, enabling real-time performance tracking and compliance reporting for EU hygiene audits. Through modular design and digital integration,n SPX FLOW supports European dairies in achieving flexibility, efficiency, and regulatory compliance in a competitive market.

MARKET SEGMENTATION

This research report on the Europe dairy processing equipment market has been segmented and sub-segmented based on equipment type, application, and region.

By Equipment Type

- Homogenizers

- Pasteurizers

- Separators

- Evaporators

- Membrane Filtration

By Application

- Cheese

- Yogurt

- Processed Milk

- Mild Powder

- Proteins

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe Dairy Processing Equipment Market?

Growth is driven by increasing dairy consumption, rising demand for processed dairy products, technological advancements in automation, and stringent food safety regulations across Europe.

2. Which type of equipment holds the largest market share?

Pasteurizers, homogenizers, separators, evaporators, and filling & packaging equipment account for a significant share of the market owing to their essential role in dairy processing.

3. Which application segment dominates the market?

Milk processing remains the largest application segment, followed by cheese, yogurt, butter, and milk powder production.

4. How is automation influencing the dairy processing equipment market?

Automation improves production efficiency, reduces labor costs, enhances product consistency, minimizes waste, and supports real-time process monitoring.

5. What role does food safety play in market growth?

Strict European food safety and hygiene standards encourage dairy manufacturers to invest in advanced processing equipment that ensures product quality and regulatory compliance.

6. What challenges does the Europe Dairy Processing Equipment Market face?

High initial investment costs, equipment maintenance expenses, fluctuating milk production, and rising energy costs are key market challenges.

7. How are technological advancements shaping the market?

Innovations such as IoT-enabled monitoring, AI-driven process optimization, robotics, and predictive maintenance are improving operational efficiency and product quality.

8. Which end users are the primary buyers of dairy processing equipment?

Large dairy processing companies, cooperative dairies, medium-sized dairy manufacturers, and specialty dairy product producers are the primary end users.

9. What opportunities exist in the Europe Dairy Processing Equipment Market?

Growing demand for value-added dairy products, expansion of premium dairy brands, modernization of dairy plants, and increasing exports create significant growth opportunities.

10. What is the future outlook for the Europe Dairy Processing Equipment Market?

The market is expected to witness steady growth over the forecast period, supported by automation, digitalization, sustainability initiatives, and increasing demand for high-quality processed dairy products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com