Europe Dental Bone Graft Substitutes Market Size, Share, Trends & Growth Forecast Report By Type, Application, Product and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Market Size, 2025

$253 MnMarket Estimate, 2026

$277.04 MnMarket Forecast, 2034

$573 MnCAGR, 2026–2034

9.5%Europe Dental Bone Graft Substitutes Market Report Summary

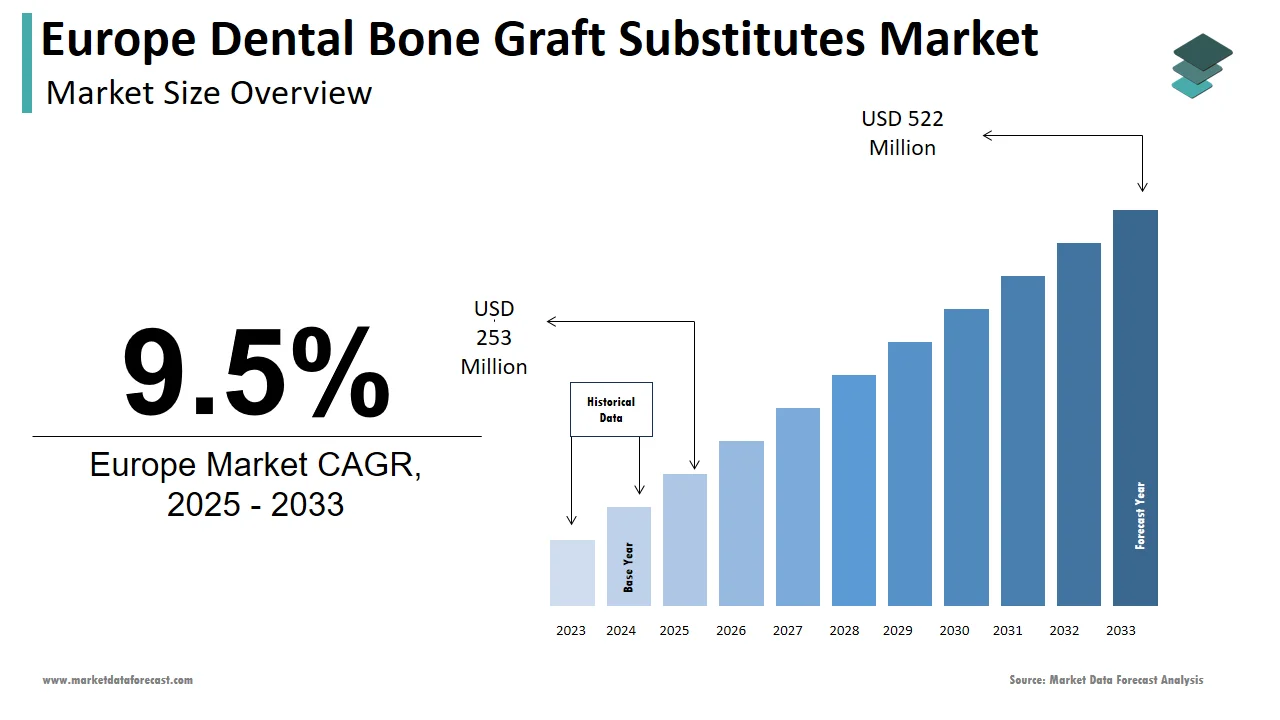

The Europe dental bone graft substitutes market was valued at USD 253 million in 2025, is estimated to reach USD 277.04 million in 2026, and is projected to reach USD 573 million by 2034, growing at a strong CAGR of 9.5% from 2026 to 2034. Market expansion is driven by increasing numbers of dental implant procedures, rising prevalence of periodontal diseases, growing popularity of aesthetic and restorative dentistry, and advancements in synthetic and xenogeneic graft materials. An aging population, improved access to dental care, and growing clinical preference for regenerative biomaterials further support strong market growth across Europe.

Key Market Trends

- Increasing demand for synthetic and bioengineered graft substitutes due to high safety and biocompatibility.

- A growing number of dental implant procedures and socket preservation surgeries post-extraction.

- Advancements in xenograft processing and regenerative materials, enhancing clinical outcomes.

- Rising focus on full-arch rehabilitation driven by aging demographics.

- Growth in dental tourism and improved reimbursement in selected European regions.

Segmental Insights

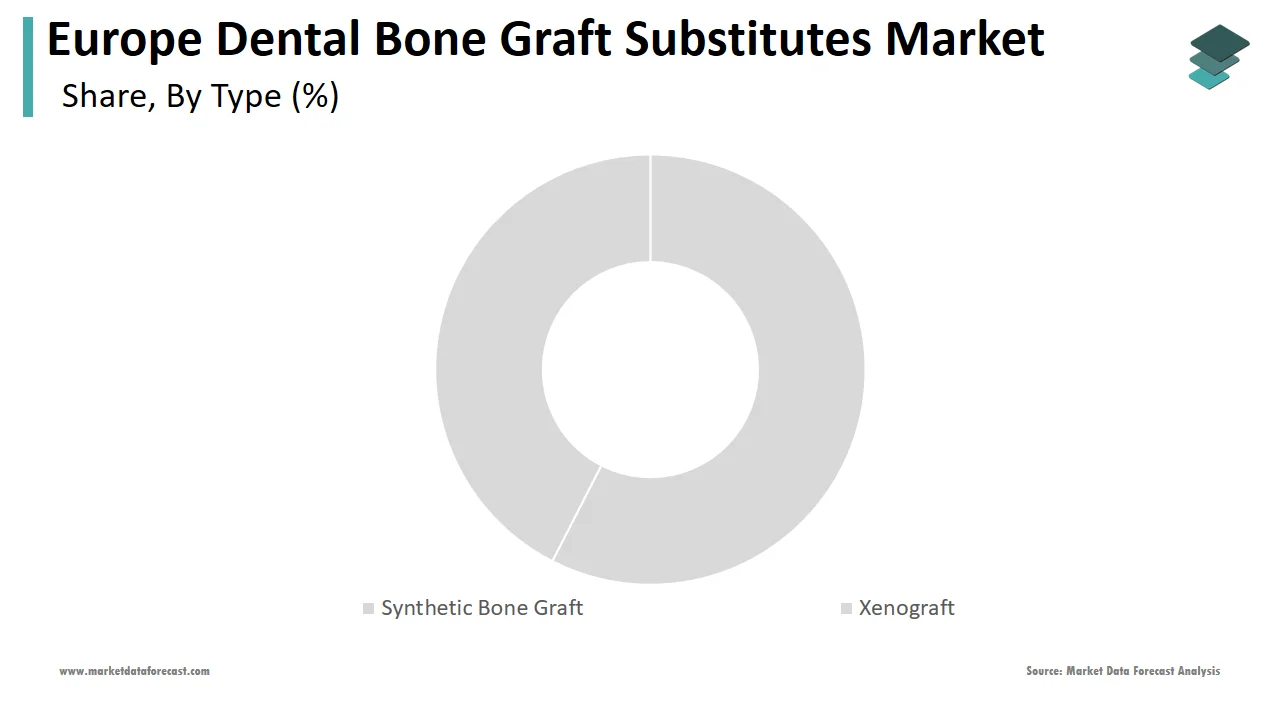

- Based on type, the synthetic bone grafts segment dominated the Europe dental bone graft substitutes market in 2024 with 42.3% share. This segment benefits from strong clinician preference for alloplast materials due to low infection risk, consistent quality, and widespread availability across dental clinics.

- Based on application, the socket preservation segment accounted for 32.2% of the market share in 2024. Rising tooth extraction rates, increased implant planning, and the need to maintain alveolar ridge structure continue to support the dominance of this segment.

- Based on product, the Bio-Oss® (Geistlich Pharma) segment held the largest share in 2024 at 38.2%, supported by its long-standing clinical validation, extensive research backing, and strong adoption across implantology and periodontal regeneration procedures.

Regional Insights

The Europe dental bone graft substitutes market is experiencing strong growth across leading economies, supported by rising implant volumes, increased aesthetic dentistry adoption, and a growing elderly population requiring restorative dental treatments.

- Germany was the top performer, holding 34.2% of the market share in 2024, supported by advanced dental infrastructure, high spending on implantology, and the strong presence of major biomaterial suppliers.

- France ranked second with 18.3% share in 2024, driven by growing dental care investments, broader acceptance of regenerative products, and increasing periodontal disease management.

- Italy is expected to grow at a prominent CAGR due to its large aging population, increasing demand for full-arch rehabilitation, and expanding implant dentistry practices.

Competitive Landscape

The Europe dental bone graft substitutes market is dominated by leading global manufacturers specializing in regenerative dental biomaterials and implant dentistry solutions. Companies are focusing on expanding their allograft, xenograft, and synthetic graft portfolios, enhancing product bioactivity, and strengthening collaborations with dental professionals and implant centers. Innovation in composite graft formulations and advanced tissue regeneration technologies is shaping the competitive environment across Europe.

Prominent companies in the Europe dental bone graft substitutes market include Institut Straumann AG, Geistlich, DENTSPLY International, Zimmer Biomet, Medtronic, BioHorizons IPH, Inc., ACE Surgical Supply Company, Inc., RTI Surgical, Inc., LifeNet Health, and Dentium.

Europe Dental Bone Graft Substitutes Market Size

The dental bone graft substitutes market size in Europe was valued at USD 253 million in 2025. The European market is estimated to be worth USD 573 million by 2034 from USD 277.04 million in 2026, growing at a CAGR of 9.5% from 2026 to 2034.

The dental bone graft substitutes are biocompatible materials used to regenerate or replace alveolar bone lost due to periodontal disease, trauma, or tooth extraction ahead of dental implant placement. These substitutes include allografts, xenografts, synthetic ceramics such as hydroxyapatite and beta tricalcium phosphate, and novel composite biomaterials engineered to mimic natural bone architecture. As per the European Federation of Periodontology, over 50% of adults aged 35 to 65 in the European Union suffer from moderate to severe periodontitis, a leading cause of bone resorption requiring grafting intervention. Additionally, the increasing prevalence of edentulism, particularly among aging populations, exacerbates demand. The regulatory landscape is shaped by the EU Medical Device Regulation, which mandates rigorous clinical evidence and post-market surveillance for all bone graft products, reinforcing safety and performance standards across the bloc.

MARKET DRIVERS

Aging Population and Rising Prevalence of Edentulism Drive Clinical Need for Bone Augmentation

The demographic shift toward an older population is a major factor propelling the growth of the Europe dental bone graft substitutes market. According to Eurostat, 21.3% of the European Union’s population was aged 65 or older in 2023, and this proportion is expected to rise to nearly 30% by 2050. Age-related tooth loss remains prevalent, with the World Health Organization reporting that 27% of Europeans over 65 have lost all natural teeth. This anatomical deficiency necessitates grafting before implant placement to ensure osseointegration stability.

Growing Acceptance of Dental Implants as Standard of Care Enhances Graft Utilization

Dental implants have transitioned from elective to mainstream treatment due to superior longevity, patient satisfaction, and cost-effectiveness over conventional dentures. The growing acceptance of dental implants as standard of care enhances graft utilization, which additionally boosts the growth of the Europe dental bone graft substitutes market. Clinical guidelines from the European Society of Endodontology now recommend implant-supported prostheses as first-line therapy for single and multiple tooth replacement where bone quality permits. This procedural dependency creates consistent demand for graft substitutes. Furthermore, public healthcare systems in countries like France and Sweden have expanded partial reimbursement for implant procedures under specific clinical criteria, encouraging wider access. Private dental insurance penetration is also rising, with Allianz and AXA offering enhanced implant coverage in Germany and the Netherlands.

MARKET RESTRAINTS

Stringent Regulatory Requirements Under EU MDR Increase Time to Market and Development Costs

The European Union Medical Device Regulation, implemented in 2021, has significantly heightened compliance burdens for bone graft substitute manufacturers. Stringent regulatory requirements under EU MDR are hampering the growth of the Europe dental bone graft substitutes market. As per the European Commission, all Class III and implantable Class IIb devices, including most synthetic and biological grafts, must undergo rigorous clinical evaluation and obtain approval from notified bodies before market entry. Many small and medium enterprises lack the resources to conduct large scale post market clinical follow up studies now mandated for high-risk devices. Moreover, the requirement for unique device identification and enhanced traceability systems has forced companies to overhaul their supply chain IT infrastructure.

Limited Reimbursement and High Out-of-Pocket Costs Constrain Patient Accessibility

The dental procedures remain largely self-funded across most European countries, restricting the growth of the Europe dental graft substitutes market. According to the European Health Insurance Observatory, public reimbursement for bone grafts is available in only four EU member states, and even then, it is limited to specific indications such as trauma or oncology-related reconstruction. A 2023 survey by the European Confederation of Dental Hygienists, 63% of patients declined recommended grafting due to cost concerns, leading to compromised implant outcomes or alternative treatments. Private insurance coverage is fragmented, with major providers like Bupa and Sanitas excluding graft materials from standard dental plans. This financial barrier is particularly acute in Southern and Eastern Europe, where average monthly disposable income is below 1,500 euros as per Eurostat. Clinicians often resort to autografts, which avoid material costs but increase surgical time and morbidity.

MARKET OPPORTUNITIES

Advancements in Bioactive and Resorbable Synthetic Grafts Enable Predictable Clinical Outcomes

Innovations in biomaterial science are transforming synthetic bone grafts into intelligent osteoconductive scaffolds that actively support regeneration, which is creating new opportunities for the growth of the Europe dental bone graft substitutes market. New formulations combining beta tricalcium phosphate with bioactive glass or collagen matrices mimic natural bone mineral composition and degrade at controlled rates, matching new bone formation. Companies like Geistlich and Straumann have launched next-generation synthetics with surface functionalization that enhances mesenchymal stem cell attachment and vascular ingrowth. As per the Technical University of Munich, these smart materials reduce healing time and eliminate disease transmission risks associated with biological grafts.

Expansion of Dental Tourism in Eastern and Southern Europe Creates New Demand Channels

Countries such as Hungary, Croatia, and Turkey have emerged as leading destinations for affordable high-quality dental care, attracting over 1.2 million medical tourists annually, according to reports. The expansion of dental tourism across countries is ascribed to bolstering the growth of the Europe dental bone graft substitutes market. These patients often seek complex implant rehabilitation requiring extensive bone grafting, yet face cost barriers in their home countries like the UK, Germany, and Scandinavian nations. Clinics in these hubs invest heavily in premium graft materials from EU-certified suppliers to ensure outcomes meet Western standards. This cross-border demand stimulates local consumption of advanced substitutes while encouraging global manufacturers to establish distribution partnerships in these regions.

MARKET CHALLENGES

Clinical Variability in Graft Performance and Lack of Standardized Outcome Metrics

The significant heterogeneity persists in the clinical performance of bone graft substitutes due to differences in composition, particle size, porosity, and surgical technique, which poses a new challenge for the growth of the Europe dental bone graft substitutes market. According to a 2023 systematic review in the European Journal of Oral Implantology, success rates for the same graft type varied across studies, reflecting inconsistent protocols and follow-up durations. The absence of universally accepted radiographic or histological benchmarks for bone regeneration complicates comparative assessments. Clinical trials on grafts use objective volumetric analysis via cone beam computed tomography. This evidentiary gap fuels clinician skepticism and preference for autografts despite their morbidity. Moreover, long-term data beyond 24 months remains scarce for newer synthetics, limiting confidence in durability.

Supply Chain Fragility for Biological Grafts and Ethical Sourcing Concerns

The xenografts and allografts face growing scrutiny over traceability, animal welfare, and disease safety despite stringent processing, which is additionally hampering the growth of the Europe dental bone graft substitutes market. Bovine-derived hydroxyapatite constitutes, yet originates primarily from non-EU countries with divergent agricultural regulations. According to the European Centre for Disease Prevention and Control, while no cases of prion transmission from dental grafts have been recorded the theoretical risk remains a regulatory concern. In 2023, Germany’s Federal Institute for Drugs and Medical Devices issued two safety alerts regarding unverified bovine graft imports lacking proper certification. Coupled with geopolitical disruptions affecting collagen and bone powder supply from key regions like Brazil and the United States, biological grafts face reputational and logistical vulnerabilities that synthetic solutions are increasingly positioned to address.

SEGMENTAL ANALYSIS

By Type Insights

The synthetic bone grafts segment held 42.3% of the Europe dental bone graft substitutes market share in 2024 due to their consistent quality, predictable resorption rates, and absence of disease transmission risks. Unlike biological alternatives, synthetics such as beta tricalcium phosphate and hydroxyapatite are manufactured under sterile controlled conditions, ensuring batch-to-batch reliability. Periodontists in Western Europe now prefer synthetic grafts for routine socket preservation and ridge augmentation owing to their osteoconductive properties and regulatory simplicity under the EU Medical Device Regulation. The European Commission classifies most synthetics as Class IIb devices requiring less extensive clinical data than allografts or xenografts, which are often Class III. Additionally, synthetics align with growing patient demand for animal-free and ethically neutral materials.

The demineralized bone matrix allografts segment is likely to grow at the fastest CAGR of 11.2% during the forecast period, owing to their inherent osteoinductive capacity, due to preserved growth factors such as bone morphogenetic proteins. While traditional allografts only provide structural support, demineralized variants actively stimulate stem cell differentiation, enhancing regeneration in complex defects. The European Tissue and Cells Directives have strengthened donor screening and viral inactivation protocols, increasing clinician confidence in safety. Moreover, processing innovations such as freeze drying and particle size standardization have improved handling and shelf life. Companies like Medtronic and Zimmer Biomet have launched putty and gel formulations that integrate easily with surgical workflows.

By Application Insights

The socket preservation segment accounted in holding 32.2% of the Europe dental bone graft substitute market share in 2024, with routinely performed immediately after tooth extraction to prevent alveolar ridge collapse and facilitate future implant placement. According to the European Federation of Periodontology, over 18 million teeth are extracted annually in the European Union, with 60 to 70% of these sites deemed at high risk for significant bone loss. Clinical guidelines from the European Association for Osseointegration strongly recommend grafting in extraction sockets with thin buccal plates or in the aesthetic zone to maintain ridge contour. The procedure’s predictability, short healing time, and integration into standard extraction workflows make it a high-volume low low-complexity indication. This preventive approach not only improves prosthetic outcomes but also reduces the need for more invasive ridge augmentation later, enhancing overall treatment efficiency and patient satisfaction.

The sinus lift procedure segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2034 due to the rising demand for posterior maxillary implants, where bone height is often insufficient. The aging population exacerbates this need as prolonged tooth loss leads to pneumatization of the maxillary sinus, reducing available bone to less than 5 millimeters in many cases. Advances in lateral and transalveolar techniques have improved safety and reduced morbidity, making the procedure more accessible to general dentists. Furthermore, the use of collagen-stabilized grafts and platelet-rich fibrin has enhanced graft retention and vascularization.

By Product Insights

The Bio OSS manufactured by the Geistlich Pharma segment was the largest and held 38.2% of the Europe dental bone graft substitutes market share in 2024, with decades of clinical validation, strong brand recognition, and extensive scientific backing. Derived from bovine cancellous bone, the product closely mimics human bone architecture and has been used in over 10 million procedures globally. Its natural porous structure supports rapid vascular ingrowth and maintains volume stability during remodeling for aesthetic and functional outcomes. Geistlich’s investment in education, including over 200 annual hands-on workshops across Europe, has cemented clinician loyalty. The product is CE certified under the stringent EU Medical Device Regulation with full traceability from donor herd to final packaging.

The Grafton demineralized allograft by Medtronic segment is anticipated to witness the fastest CAGR of 11.2% from 2026 to 2034 due to its osteoinductive properties and expanding indications in complex regeneration. The product is processed under the American Association of Tissue Banks standards and distributed in Europe with full compliance with the EU Tissues and Cells Directives, ensuring donor traceability and viral safety. Medtronic’s recent launch of Grafton Putty and Flex formats has improved handling and adaptability in irregular defects, increasing adoption among oral surgeons.

COUNTRY LEVEL ANALYSIS

Germany Dental Bone Graft Substitutes Market Analysis

Germany was the top performer of the Europe dental bone graft substitutes market by holding 34.2% of share in 2024, with the presence of the largest dental care provider and innovation hub. The country performs over 1.2 million dental implant procedures annually, with bone grafting involved in nearly 70% of cases. Leading manufacturers, including Heraeus Kulzer and Straumann, maintain R&D centers in Germany, driving local innovation in synthetic ceramics. Additionally, the country hosts Europe’s largest dental trade fair, IDS in Cologne, which serves as a key launchpad for new graft technologies. The presence of a dense network of 45,000 dental specialists and strong private insurance coverage ensures consistent clinical adoption of advanced substitutes.

France Dental Bone Graft Substitutes Market Analysis

France was ranked second by holding 18.3% of the Europe dental bone graft substitutes market share in 2024, driven by high patient demand for aesthetic dentistry and robust specialist infrastructure. The French Health Authority has issued clear clinical guidelines endorsing bone grafting for ridge preservation and sinus augmentation, which are widely followed in both private and university clinics. Public hospitals in Paris, Lyon, and Marseille serve as centers of excellence for maxillofacial reconstruction using advanced allografts and synthetics. Companies like Bioteck and Septodont have strong domestic manufacturing and distribution networks. France’s emphasis on evidence-based practice and high density of periodontists ensures sustained demand for clinically validated graft substitutes.

Italy Dental Bone Graft Substitutes Market Analysis

Italy dental bone graft substitutes market growth is expected to have a prominent CAGR during the forecast period, with its large aging population and growing focus on full arch rehabilitation. According to, 24% of Italians are over 65, with edentulism affecting 31% of this cohort, driving extensive bone reconstruction needs. Southern regions like Sicily and Campania have seen a surge in dental tourism, with clinics in Naples and Palermo offering comprehensive grafting and implant packages at 40% lower costs than Northern Europe. Domestic manufacturers such as OsteoBiol and Tecnoss supply high-quality bovine and synthetic grafts widely used across the country.

United Kingdom Dental Bone Graft Substitutes Market Analysis

The United Kingdom dental bone graft substitutes market growth is likely to grow with the sophisticated private dental sector and increasing patient investment in long-term oral health. Over 720,000 dental implants were placed in 2023, with bone grafting performed in 68% of cases, as per some reports. The National Institute for Health and Care Excellence provides clear guidance on bone preservation techniques, which are widely adopted in specialist practices. Companies like Nobel Biocare and Dentsply Sirona have extensive training academies in London and Manchester, promoting advanced grafting protocols. The rise of digital implant planning using cone beam CT has also increased precision in graft volume estimation, enhancing clinical outcomes and material utilization efficiency.

Spain Dental Bone Graft Substitutes Market Analysis

Spain dental bone graft substitute market growth is driven by the high dental tourism volumes and expanding specialist networks in major cities. Clinics in Barcelona, Madrid, and Valencia offer bundled grafting and implant packages at 50 to 60% lower costs than Northern Europe without compromising on material quality.

COMPETITIVE LANDSCAPE

The competition in the Europe dental bone graft substitutes market is defined by a blend of established multinational innovators and specialized biomaterial firms operating within a rigorous regulatory and clinical environment. Leadership is not solely determined by scale but by depth of scientific validation, brand trust, and integration into clinical workflows. Companies compete on product performance, safety, traceability, and educational support rather than price alone. The EU Medical Device Regulation has raised entry barriers favoring incumbents with resources to meet stringent clinical evaluation and post-market surveillance requirements. Synthetic graft manufacturers are gaining ground due to ethical preferences and regulatory simplicity, while biological graft providers counter with superior osteoinductive data. Competition is also intensifying in niche applications such as sinus lift and ridge augmentation, where outcomes are highly technique and material-sensitive. Differentiation increasingly hinges on digital integration, training ecosystems, and compatibility with implant systems.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe dental bone graft substitutes market include

- Institut Straumann AG

- Geistlich

- DENTSPLY International

- Zimmer Biomet

- Medtronic

- BioHorizons IPH, Inc.

- ACE Surgical Supply Company, Inc.

- RTI Surgical, Inc.

- LifeNet Health

- Dentium

TOP PLAYERS IN THE MARKET

- Geistlich Pharma is a Swiss innovator and global leader in regenerative dental and orthopedic biomaterials headquartered in Wolhusen. The company’s flagship product, Bio OSS, derived from bovine bone, has become the clinical gold standard for socket preservation and sinus lift procedures across Europe. Geistlich contributes significantly to global scientific advancement through its extensive research partnerships with universities and dental societies. In recent years, the company has reinforced its position by achieving full compliance with the EU Medical Device Regulation and enhancing traceability across its supply chain. It has also expanded its educational initiatives, launching over 200 hands-on surgical training workshops annually throughout Europe to support evidence-based clinical adoption.

- Medtronic is a global healthcare technology company with a strong presence in the European dental bone graft market through its Grafton line of demineralized allografts. Leveraging its expertise in biologics processing, Medtronic offers osteoinductive grafts that actively stimulate bone formation in complex periodontal and implant cases. The company has strengthened its European footprint by aligning Grafton’s manufacturing and donor screening protocols with the EU Tissues and Cells Directive, ensuring the highest safety standards. Recent actions include the launch of new putty and flex formulations tailored to European surgical workflows and expanded distribution agreements with specialty dental networks in the UK, Germany, and the Nordics. Medtronic’s integration of grafting solutions into its broader craniofacial portfolio enhances clinical relevance and accessibility.

- Straumann Group is a Swiss-based global leader in tooth replacement and orthodontics with a vertically integrated approach to bone regeneration. The company offers a comprehensive range of synthetic and collagen-based grafting materials under its Botiss and Geistlich partnerships, complementing its implant systems. Straumann actively invests in digital dentistry and tissue regeneration R&D through its Innovation Center in Basel. To bolster its position in the European bone graft market, the company has expanded its Emdogain enamel matrix derivative portfolio and integrated grafting protocols into its implant planning software. It also conducts extensive clinician training via its global education network with over 30 learning centers across Europe. These initiatives ensure seamless adoption of bone preservation strategies within Straumann’s ecosystem of restorative solutions.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe dental bone graft substitutes market employ a cohesive set of strategies centered on regulatory compliance, clinical education, and product innovation. Companies prioritize full alignment with the EU Medical Device Regulation by investing in robust quality management systems and clinical evidence generation. Strategic collaboration with academic institutions and professional societies enhances scientific credibility and drives guideline adoption. Extensive hands-on training programs and digital surgical planning tools are deployed to improve clinician proficiency and procedural standardization. Vertical integration with implant systems allows for bundled solutions that streamline treatment workflows. Companies also strengthen supply chain resilience through localized manufacturing and enhanced donor traceability, especially for biological grafts. Active engagement in dental tourism hubs through certified distribution channels captures cross-border demand. These multifaceted approaches ensure sustained relevance in a highly specialized and evidence-driven market.

EUROPE DENTAL BONE GRAFT SUBSTITUTES MARKET NEWS

- In March 2024, Geistlich Pharma completed its EU MDR recertification for Bio OSS and launched an updated digital traceability platfor,m enhancing transparency and reinforcing its leadership in the Europe Dental Bone Graft Substitutes Market.

MARKET SEGMENTATION

This Europe dental bone graft substitutes market research report is segmented and sub-segmented into the following categories.

By Type

- Synthetic Bone Graft

- Xenograft

- Allograft

- Demineralized Allograft

By Application

- Socket Preservation

- Ridge Augmentation

- Periodontal Defect Regeneration

- Implant Bone Regeneration

- Sinus Lift

By Product

- Bio OSS

- Osteograf

- Grafton

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which countries dominate the europe dental bone graft substitutes market?

Germany and the UK lead the europe dental bone graft substitutes market due to advanced healthcare infrastructure and strong governmental support

2. What are key growth drivers of the europe dental bone graft substitutes market?

Growth drivers include rising dental implant procedures, aging population, increased oral disease awareness, and technological advances in graft materials

3. What types of dental bone graft substitutes are popular in europe?

Synthetic and allograft bone substitutes are widely used in the europe dental bone graft substitutes market due to safety, affordability, and availability

4. What challenges does the europe dental bone graft substitutes market face?

Challenges include high procedure costs, reimbursement issues, regulatory hurdles, limited dental care access in some regions, and skilled professional shortage

5. How important is technology in the europe dental bone graft substitutes market?

Technological advancements enhance graft quality, reduce complications, and improve patient outcomes, boosting the europe dental bone graft substitutes market

6. What role do regulatory policies play in the europe dental bone graft substitutes market?

Stringent regulatory frameworks ensure safety and efficacy, influencing product approvals and adoption within the europe dental bone graft substitutes market

7. How does the aging population affect the europe dental bone graft substitutes market?

An increasing elderly population with dental issues drives demand for bone graft solutions in the europe dental bone graft substitutes market

8. Are synthetic bone graft substitutes popular in europe?

Yes, synthetic substitutes dominate the europe dental bone graft substitutes market due to longer shelf life and low infection risk

9. Which companies are prominent in the europe dental bone graft substitutes market?

Key players include Geistlich, Botiss Biomaterials, Zimmer Biomet, Straumann, and Dentsply Sirona in the europe dental bone graft substitutes market

10. How does dental implant volume influence the europe dental bone graft substitutes market?

Higher dental implant surgeries increase demand for graft substitutes, expanding the europe dental bone graft substitutes market significantly

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com