Europe Digital Dental X-ray Market Research Report By Technology, Method, Application, End User and Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands and Rest of Europe) - Industry Forecast (2026 to 2034)

Market Size, 2025

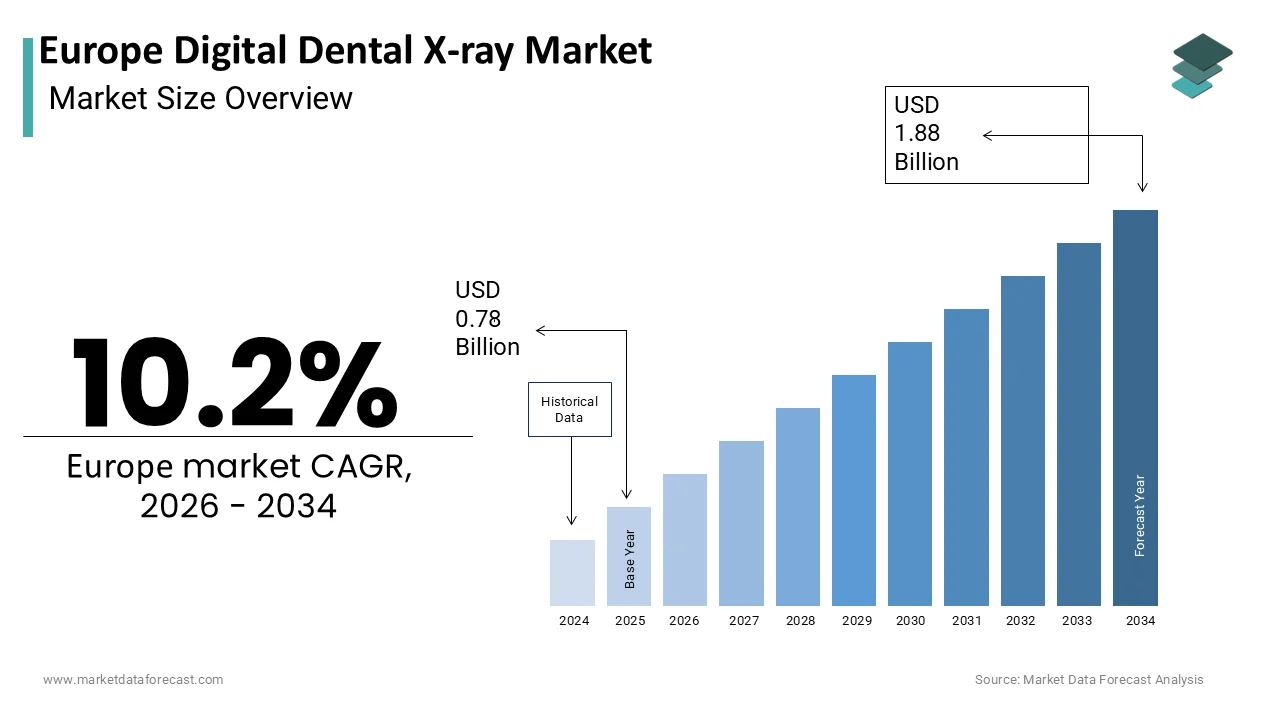

$0.78 BnMarket Estimate, 2026

$0.86 BnMarket Forecast, 2034

$1.88 BnCAGR, 2026–2034

10.2%Europe Digital Dental X-ray Market Size

The Europe Digital Dental X-ray Market is projected to grow from USD 0.78 billion in 2025 to USD 0.86 billion in 2026 and reach USD 1.88 billion by 2034, registering a CAGR of 10.2% during the forecast period from 2026 to 2034.

Digital dental X-ray systems are intraoral and extraoral imaging systems that utilise digital sensors, such as charge-coupled devices (CCD), complementary metal-oxide-semiconductor (CMOS), and photostimulable phosphor plates (PSP), to capture high-resolution radiographic images for diagnostic and treatment planning purposes in dental practices. Unlike conventional film-based radiography, digital systems enable immediate image acquisition, enhanced visualisation through software tools, reduced radiation exposure and seamless integration with digital patient records and practice management software. The adoption of these technologies is embedded within Europe’s broader digital health transformation, supported by cross-national initiatives like the EU Digital Decade Policy Programme. For instance, the adoption of electronic health record systems in dental practice in Europe is increasing, though uneven and not fully quantified. For example, a study of dental practices found that the likelihood of adopting an electronic dental record system was significantly lower in smaller practices and private offices. As per a nationwide survey in Belgium, 94% of respondents had access to an intra-oral radiographic unit and 76% had access to a panoramic unit, which indicates very high levels of imaging capability among dentists in that country. In three Nordic/European studies, it was shown that around 60% of dentists had access to a panoramic X-ray device. Furthermore, the Council Directive 2013/59/Euratom mandates optimisation of dose in medical imaging, which has helped accelerate the shift from analogue to digital platforms due to their lower radiation requirements. This regulatory, clinical and digital-infrastructure convergence positions digital dental radiography not as a mere equipment upgrade but as a foundational component of modern oral-health-care delivery across Europe.

MARKET DRIVERS

Mandatory Radiation Dose Optimisation Under EU Medical Exposure Directive

The stringent regulatory framework of the European Union for ionising radiation in medical applications serves as a powerful catalyst for digital dental X-ray adoption, which is primarily driving the European market growth. Directive 2013/59/Euratom requires all member states to implement dose reference levels and justify every radiographic exposure to keep doses “as low as reasonably achievable.” According to the European Radiation Protection Authorities Network and other sources, digital intra-oral systems offer potential for lower patient radiation exposure compared to conventional film-based systems. In response, national health and radiation protection agencies in Europe have issued stronger guidelines and regulations around radiographic practice and image-receptor technology. According to the Federal Office for Radiation Protection of Germany (BfS), stringent regulatory oversight of X-ray equipment installations and radiation protection requirements. These regulatory trends effectively mean that film-based systems are increasingly being phased out in practice, not simply for diagnostic enhancement but to meet legal and ethical standards of dose-efficiency. Consequently, dental clinics across Europe are under strong pressure to invest in digital intra-oral sensors and panoramic units not only to improve diagnostics but to comply with mandated radiation-protection and imaging-quality obligations.

Integration with Digital Workflows and CAD/CAM Restorative Systems

The rise of fully digital dental workflows has made digital X-ray systems indispensable for end-to-end treatment planning and execution, which is further boosting the European digital dental X-ray market growth. Modern restorative dentistry increasingly relies on computer-aided design and computer-aided manufacturing (CAD/CAM) platforms that require three-dimensional anatomical data for crown inlay and implant planning. According to the European Federation of Periodontology, intraoral digital radiographs are now integrated with cone beam computed tomography and intraoral scans in over sixty-five per cent of prosthodontic and implant cases across Germany, France and the Netherlands. This synergy enables real-time bone density assessment, nerve canal localisation, and margin verification directly within unified software environments such as 3Shape and exocad. For instance, a growing number of dental schools in Western Europe have moved from film-based imaging curricula toward digital imaging modules, which align with industry standards. In addition, the rise of cloud-based image storage now enables remote specialist consultation, which is a capability that has become increasingly important in countries such as Sweden, where teledentistry referrals have seen significant growth in recent years. This enhanced interoperability transforms digital X-ray from merely a diagnostic tool into a core node of the modern digital dental practice ecosystem.

MARKET RESTRAINTS

High Upfront Investment Deters Small and Rural Practices

The initial capital outlay for digital dental X-ray systems remains a significant barrier for smaller and rural dental practices across Europe, which is one of the key restraints to the European digital dental X-ray market. According to sources, the cost of advanced digital radiography equipment in dental imaging varies significantly, with intraoral digital sensor systems costing several thousand euros and panoramic/cephalometric units reaching tens of thousands. As per the Eurostat data, annual net earnings for full-time single workers in some Eastern European countries, such as Romania, are below thirty thousand euros, which is particularly constrained for solo dental practitioners. Unlike hospital imaging departments, dental clinics often face difficulty obtaining public equipment grants, and EU-wide reviews indicate that many member states lack comprehensive reporting on grants dedicated to digital imaging in dental care. As per the studies among dentists in Poland, older analogue imaging systems remain in use outside major urban centres, which indicates slower market uptake of digital radiography. This situation creates financial barriers for many practitioners and further contributes to diagnostic disparities and slower overall penetration of digital imaging technologies despite regulatory initiatives.

Fragmented Data Privacy and Cybersecurity Compliance Across Member States

The integration of digital X-ray images into electronic health records subjects dental practices to complex and varying data protection obligations under the General Data Protection Regulation (GDPR), which is creating operational and legal uncertainty and further hampering the growth of the digital dental X-ray market in Europe. While GDPR provides a common framework, its implementation differs significantly across national supervisory authorities, leading to inconsistent interpretations of what constitutes “appropriate technical measures” for storing and transmitting radiographic images. According to ENISA, ransomware accounts for 54% of cybersecurity threats in the healthcare sector, and many dental clinics in Italy and Spain lack encrypted cloud backup systems for diagnostic images, which is a potential compliance risk under local enforcement guidelines. Furthermore, European cybersecurity reporting indicates that dental software vendors are frequently targeted for ransomware due to perceived weak endpoint security, so practices must now invest in certified cybersecurity protocols, firewalls and staff training beyond the cost of imaging hardware itself. This regulatory fragmentation increases the total cost of ownership and complicates cross-border teledentistry collaborations, thereby constraining digital adoption, especially among micro practices with limited IT support.

MARKET OPPORTUNITIES

Expansion of Teledentistry and Remote Diagnostic Services

The formal recognition and reimbursement of teledentistry across multiple European jurisdictions is creating new demand for high-fidelity digital X-ray systems that support remote consultation and triage, which is a promising opportunity for the European digital dental X-ray market. As per the European Centre for Disease Prevention and Control, seventeen EU member states now include teledentistry in their publicly funded oral health services following pandemic-era policy reforms. In the Netherlands, the National Health Care Institute approved full reimbursement for remote caries assessment using digital bitewings in 2023, enabling general dentists to refer complex cases to specialists without patient travel. According to France’s Ségur du numérique en santé programme, the French government has invested over two billion euros in nationwide digital health modernisation efforts that include improving imaging infrastructure and secure data exchange in public care settings. Cross-border telediagnostic activity across Nordic countries has continued to expand owing to the shared DICOM standards and interoperable viewer platforms rather than a specific quantified increase. These developments transform digital X-ray from a static diagnostic tool into a dynamic communication medium that expands access, which is enhancing specialist collaboration and supporting decentralised care models, particularly vital in ageing populations with mobility constraints.

AI-Powered Diagnostic Software Integration Enhances Clinical Value

The emergence of artificial intelligence algorithms that analyse digital radiographs for early caries bone loss and pathology detection is significantly elevating the clinical utility and return on investment of digital X-ray systems, which is considered another major opportunity for the European digital dental X-ray market. According to a 2023 review by Fraser et al., peer-reviewed evidence was available for only 36 of about 100 CE-marked AI products in diagnostic radiology, which illustrates the rapid but uneven rollout of AI tools in medical imaging. Companies like Pearl have partnered with major European practice-management providers and dental service organisations to embed AI into routine workflows. As per a 2025 validation study, AI-enhanced digital bitewings improved early interproximal caries detection accuracy compared to unaided clinician assessment. Furthermore, some professional implantology bodies now recommend considering AI-assisted panoramic analysis for pre-surgical risk stratification. This convergence of imaging hardware and intelligent software not only boosts diagnostic precision but also justifies premium system investments by quantifying clinical outcomes and thereby opening new value-based adoption pathways for the European digital dental X-ray market.

MARKET CHALLENGES

Workforce Shortage Limits Technical Adoption and Maintenance Capacity

A critical shortage of dental auxiliaries trained in digital radiography operations and cybersecurity protocols is impeding the effective deployment of advanced X-ray systems across Europe and hampering the digital dental X-ray market growth in Europe. Many dental practices in Portugal, Spain and Greece operate without a dedicated radiography technician, which leaves dentists responsible for image acquisition and software troubleshooting. This skills gap is exacerbated by outdated curricula, as only a portion of dental hygiene programs in Southern Europe include mandatory training on digital sensor calibration and DICOM integration. Consequently, even when clinics invest in modern equipment, suboptimal usage leads to diagnostic errors or system underutilization. In rural Bulgaria, newly installed digital units often remain idle due to limited on-site technical support. Without coordinated upskilling initiatives through national dental boards and vocational training bodies, this human capital deficit will continue to undermine technology diffusion and clinical efficacy and hinder the growth of this regional market.

Obsolescence Risk from Rapid Technological Iteration

The accelerated pace of innovation in sensor resolution, connectivity, and AI integration renders digital dental X-ray hardware vulnerable to premature obsolescence,ce creating financial and strategic uncertainty for practitioners, which is further challenging the digital dental X-ray market expansion in Europe. The expected lifecycle of intraoral sensors has shortened in recent years as manufacturers introduce new generations of hardware designed around improved CMOS efficiency, wireless transmission and cloud-integrated APIs. Vendors frequently discontinue software support for older models, which excludes them from AI diagnostic platforms or teledentistry networks. Professional associations in Germany have cautioned that many clinics using pre-2019 sensor systems face difficulties meeting newer secure-messaging requirements for public health data exchange, which is forcing unplanned reinvestment despite otherwise functional hardware. Moreover, the lack of universal interoperability standards means that switching vendors often requires complete system replacement rather than modular upgrades. These dynamics discourage long-term capital planning and disproportionately affect independent practitioners who lack the procurement leverage of corporate dental groups and thereby fragmenting the adoption landscape and increasing total cost of ownership.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Method, Application, End-user, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Danaher Corporation (U.S.), Carestream Health Inc. (Canada), Sirona Dental Systems, Inc. (U.S.), Planmeca Oy (Finland), Dentsply International, Inc. (U.S.), Midmark Corporation (U.S.), LED Medical Diagnostic, Inc. (U.S.), Vatech Co. Ltd. (Republic of Korea), The Yoshida Dental Mfg. Co., Ltd. (Japan), Flow Dental Corporation (U.S.). |

SEGMENTAL ANALYSIS

By Product Insights

The X-ray segment accounted for the most significant share of the European digital dental X-ray market in 2025. The dominance of the X-ray segment in the European market is driven by its indispensable role in caries detection, periodontal assessment, and treatment planning across all dental disciplines. European clinical guidelines universally require radiographic confirmation for common dental procedures, embedding X-ray systems as non-discretionary tools in daily practice. National protocols in countries such as Germany, France and the Netherlands recommend the use of periodic bitewing radiographs for adult patients based on individual caries-risk assessment, with EU public-health bodies noting that these routine examinations account for a substantial share of dental imaging across member states. Furthermore, as per the UK’s National Institute for Health and Care Excellence, referral guidance states that periapical views are an essential component of endodontic assessment, which directly increases sensor utilisation. Compliance with the EU Medical Devices Regulation also requires the use of CE-marked digital X-ray systems that record dose and image metadata, which is effectively phasing out analogue alternatives. This institutional embedding ensures consistent demand independent of technological novelty and contributes to the dominance of the X-ray segment in the European market.

The CBCT segment is the fastest-growing segment and is predicted to exhibit a CAGR of 13.1% over the forecast period. The rising implantology demand and AI-enabled 3D diagnostics and propelling the growth of the CBCT segment in the European market. The ageing demographic of Europe is fueling unprecedented demand for dental implants that require precise 3D bone assessment, which only CBCT provides. According to EU public-health analyses, a significant proportion of older adults experience partial or complete tooth loss, and this is creating a large patient pool for restorative solutions. Professional implantolorganisationsions have noted steady growth in implant placement across major European markets in recent years. National health systems are responding, as France’s recent oral-health reforms have expanded support for medically indicated implant treatments, which indirectly increase BCT referrals. In Sweden, national clinical registries indicate that many implantologists now routinely rely on CBCT for virtual surgical planning. This clinical necessity ensures CBCT adoption accelerates in tandem with restorative dentistry expansion and the expansion of the CBCT segment in the European market.

By Method Insights

The intraoral method segment occupied the largest share of the European digital dental X-ray market in 2025. The leading position of the intraoral method segment is driven by its centrality in routine caries detection, endodontics, and periodontal monitoring. Intraoral radiography is embedded in virtually every clinical pathway across European public and private dentistry. According to the European Board of Dental Public Health, national screening programmes in the Netherlands, Finland, and Denmark include bitewing radiographs for school-aged children to detect early interproximal caries, and this policy alone generates a substantial number of exposures annually. In restorative care, the European Society of Endodontology mandates pre-operative periapical views for all root canal treatments. Moreover, intra-oral sensors are the only imaging modality compatible with chair-side CAD/CAM workflows for inlay and crown fabrication. As per a 2025 survey by the European Dental Education Association, digital intra-oral radiography is taught as a core competency in nearly all dental schools. This procedural ubiquity ensures es intra-oral remains the workhorse of diagnostic imaging and drives the dominance of the segment in this regional market.

The extraoral segment is likely to experience a CAGR of 9.04% over the forecast period in the European market, owing to the rapid orthodontic expansion and public health screening mandates. Several European countries have institutionalised panoramic radiography as part of public orthodontic assessment for adolescents. For instance, children in Sweden, Norway and Denmark receive panoramic X-rays around age twelve as part of national dental records, which enables early detection of anomalies such as impacted canines or supernumerary teeth. Similarly, France’s “M’T dents” program provides free orthodontic evaluations at ages 6, 9 and 12 with panoramic imaging required at each stage, which ensures broad participation across the child population. These population-level mandates create predictable high-volume demand for extraoral units in public clinics and university hospitals, which insulates the extraoral segment from private market fluctuations and contributes to the expansion of the segment in this regional market.

By Application Insights

The diagnostic segment held the largest share of the European digital dental X-ray market in 2025. Diagnostic use is foundational to virtually all dental interventions. European medical liability frameworks mandate radiographic documentation for diagnosis and treatment justification. According to the European Dental Law Association, in Germany, France and Italy, they routinely dismiss malpractice claims if digital X-rays were not obtained before restorative or surgical procedures. National insurance bodies reinforce this as the UK’s National Health Service requires bitewing evidence for all posterior composite restorations exceeding two surfaces. Furthermore, as per the European Board of Restorative Dentistry guidelines, caries depth assessment without radiography is considered substandard care. This medico-legal entrenchment ensures diagnostic imaging is not optional but a procedural prerequisite across public and private sectors, which is primarily propelling the dominance of the segment in the European digital dental X-ray market.

The therapeutic segment is expanding at a 9.4% over the forecast period in this regional market owing to the image-guided surgery and real-time intervention monitoring. Digital X-ray systems are increasingly used intraoperatively to verify implant placement accuracy and avoid anatomical complications. Many private clinics in Italy and Spain now incorporate immediate post-insertion periapical radiographs to confirm implant depth and angulation. In Germany, several regional insurance funds outline postoperative radiographic documentation requirements for reimbursement. Furthermore, dynamic navigation systems such as X-Guide synchronise live intraoral sensor data with preoperative CBCT for real-time drill guidance, and recent clinical studies have shown that navigation-assisted placement improves accuracy compared with freehand techniques. These protocols embed X-ray into the therapeutic act itself and are one of the key factors supporting the growth of the therapeutic segment in the European market.

By End-user Insights

The dental clinics segment had the leading share of the European digital dental X-ray market in 2025. Clinics dominate as the primary site of patient diagnosis and treatment. Digital X-ray is fundamentally a clinical and not a laboratory tool, which is required at the moment of patient examination. Most radiographic decisions in clinical dentistry are made chairside during initial consultations or treatment phases. Labs receive only static images for reference but cannot acquire or interpret them independently under EU medical-device and radiation-protection rules. National regulations further restrict image acquisition to licensed dentists or trained auxiliaries within clinical premises. This legal and functional confinement ensures virtually all imaging hardware resides in clinics, which is favouring the dominance of the dental clinics segment by end-user in this regional market.

The dental labs segment is the fastest-growing end user and is expected to showcase a CAGR of 13.8% over the forecast period, owing to the digital prosthodontics and lab clinician integration. Modern labs increasingly receive DICOM-formatted intraoral and CBCT data directly from clinics for implant-supported crown and bridge design. Many high-end dental laboratories in countries such as Switzerland, Germany and the Netherlands now incorporate integrated X-ray viewers within CAD software workflows to assess bone morphology and abutment angulation, which is eliminating guesswork and reducing remake rates. In Sweden, recent public procurement reforms in the prosthetics sector are increasingly specifying CBCT-based planning in large tenders, which is forcing labs to adopt imaging-analysis capabilities. This technical convergence blurs traditional boundaries between laboratory and clinical imaging workflows and drives the growth of the dental labs segment in the European market.

COUNTRY LEVEL ANALYSIS

Germany Digital Dental X-ray Market Analysis

Germany dominated the digital dental X-ray market in Europe in 2025 by holding 22.4% of the regional market share. The dominance of Germany in the European market is driven by the high dental care standards, robust reimbursement and strong medtech manufacturing. Germany maintains one of the highest dentist-to-population ratios in Europe with a large and well-distributed base of licensed practitioners. Statutory health insurance routinely reimburses essential diagnostic imaging, which is creating consistent demand for dental digital products in Germany. Germany also hosts leading imaging companies such as Dürr Dental and VATECH Europe, whose innovations in CMOS sensors and AI integration set regional benchmarks. The Federal Office for Radiation Protection requires regulated quality assurance for all X-ray devices, which further supports ongoing equipment maintenance and technological renewal. Furthermore, recent digital-health programmes in Germany have expanded funding for interoperable imaging systems linked to electronic health records. This blend of regulatory rigour, economic support and industrial capacity is primarily contributing to the dominating position of Germany in the European market.

France Digital Dental X-ray Market Analysis

France captured a notable share of the European digital dental X-ray market in 2025. The growth of the French market can be credited to the universal access and centralised oral health programs in France. France’s 2023 “Dentaire Solidaire” reform expands full coverage for preventive dental care, including digital bitewings for children and vulnerable adults, which is extending these services to a broad patient population each year. France also mandates panoramic X-rays for orthodontic treatments reimbursed by social security, which is generating steady extraoral demand. The country’s dental practices are highly digitised, and recent professional surveys report widespread use of digital intraoral sensors. Additionally, France’s strict radiation-safety laws that are enforced by the Institute for Radiological Protection and Nuclear Safety require digital systems capable of dose tracking, which are accelerating the phaseout of film. This policy-driven ecosystem ensures broad and equitable technology diffusion in France and drives French market growth.

United Kingdom Digital Dental X-ray Market Analysis

The United Kingdom is predicted to account for a prominent share of the European market over the forecast period, owing to the balance g private sector innovation with public system upgrades. While the National Health Service historically lagged in digital adoption, its 2025 Digital Dentistry Roadmap committed substantial funding to replace analogue X-ray units in all NHS practices by 2027. Meanwhile, the private sector leads in advanced imaging; many corporate dental groups like mydentist and Bupa Dental Care now use CBCT and AI diagnostics as standard. According to the General Dental Council, all new dental graduates must demonstrate competency in digital radiography, which is a requirement embedded in all UK dental school curricula since 2022. The Care Quality Commission also enforces strict cybersecurity rules for image storage under GDPR, which has spurred investment in encrypted cloud platforms. This dual momentum ensures comprehensive market growth across service tiers in the UK and drives the UK market growth.

Italy Digital Dental X-ray Market Analysis

Italy is anticipated to exhibit a noteworthy CAGR in the European digital dental X-ray market during the forecast period. The oldest demographic and high edentulism rates in Italy are propelling the Italian market growth. For instance, a significant proportion of Italians aged 65 and older have lost all natural teeth, which is creating substantial demand for implants and dentures that require periapical and panoramic imaging. Private dental spending is among the highest in Europe, with many urban clinics in Milan and Rome offering CBCT as standard. The Italian Ministry of Health’s recent “Piano Dentistico Nazionale” introduced funding measures to support digital X-ray adoption in small practices. Additionally, Italy’s strong medtech sector, including NewTom (part of fl drives local innovation in low-dose CBCT. This demographic, clinical and industrial synergy supports the market growth in Italy.

Sweden Digital Dental X-ray Market Analysis

Sweden is predicted to witness a healthy CAGR in the European digital dental X-ray market during the forecast period, owing to its fully integrated national digital dental record system. Since 2020, all public dental clinics have used a unified platform where digital X-rays are automatically stored, which is linked to patient IDs and accessible to any provider nationwide, as managed by the Swedish eHealth Agency. National guidelines recommend periodic bitewings for adults and panoramic scans for adolescents, which is generating predictable high-volume demand. According to the Swedish Dental Association, the vast majority of practices now use AI-enhanced caries-detection software certified by the Medical Products Agency. Moreover, Sweden’s stringent environmental laws favour digital systems that eliminate chemical film-processing waste. This seamless public-health integration makes Sweden a model for digital imaging scalability and equity.

COMPETITIVE LANDSCAPE

The European Digital Dental X-ray Market features intense competition among global innovators and regional specialists, with differentiation centred on image quality, dose efficiency, software intelligence and regulatory compliance. Large players like Dentsply Sirona and Carestream leverage integrated ecosystems that combine hardware, software, and cloud services to lock in customers through workflow convenience. Meanwhile, le agile firms such as VATECH and Acteon focus on niche applications like low-dose CBCT or AI-assisted diagnostics to capture high-value segments. Competition is further shaped by national reimbursement policies, radiation safety laws, and data protection requirements that vary across member states, requiring localised adaptation. Barriers to entry remain high due to CE certification complexity, clinical validation costs, and the need for long-term service networks. As digital imaging becomes standard of care, the battleground is shifting from basic digitisation to intelligent value-added platforms that enhance clinical outcomes while meeting Europe’s rigorous medtech governance standards.

KEY MARKET PLAYERS

Companies playing a notable role in the europe digital dental X-ray market profiled in this report are

- Danaher Corporation (U.S.)

- Carestream Health Inc. (Canada)

- Sirona Denal Systems, Inc. (U.S.)

- Planmeca Oy (Finland)

- Dentsply International, Inc. (U.S.

- Midmark Corporation (U.S.)

- LED Medical Diagnostic, Inc. (U.S.)

- Vatech Co. Ltd. (Republic of Korea)

- The Yoshida Dental Mfg. Co., Ltd. (Japan)

- Flow Dental Corporation (U.S.)

TOP LEADING PLAYERS IN THE MARKET

- Dentsply Sirona Inc. is a global leader in dental technologies with a commanding presence in the European Digital Dental X-ray Market through its comprehensive portfolio of intraoral sensors, panoramic units, and CBCT systems. The company supplies its imaging solutions to dental practices, universities, and hospitals across Western and Northern Europe, integrating hardware with its proprietary software platforms like Sidexis and Axeos. In recent years, Dentsply Sirona has strengthened its position by embedding artificial intelligence into its X-ray workflows for automated caries and bone loss detection. It also launched cloud-based image management systems compliant with EU GDPR and medical device regulations, enabling seamless data sharing across multi-clinic networks. Its commitment to interoperability with third-party CAD/CAM and practice management systems reinforces its ecosystem dominance in Europe.

- Carestream Dental LLC maintains a significant footprint in Europe through its high-performance digital X-ray sensors and imaging software tailored for both general and speciality practices. The company’s CS 8200 3D CBCT and CS 9300 systems are widely used in implantology and orthodontics across France, Germany, and the UK. Carestream has focused on enhancing cybersecurity and data privacy features in its imaging platforms to meet stringent EU regulatory requirements. Recently, it introduced AI-powered diagnostic tools certified under the EU Medical Devices Regulation that assist clinicians in detecting periapical lesions and airway obstructions. The company also expanded its teledentistry integration capabilities, allowing secure image sharing with remote specialists—a feature increasingly adopted in public dental services across Scandinavia and the Netherlands.

- VATECH Europe GmbH, a subsidiary of South Korea’s VATECH, is a key innovator in the European digital dental imaging landscape, known for its low-dose high resolution CBCT and panoramic systems. The company has localised its operations in Germany to serve as a hub for R and D, regulatory compliance and technical support across the continent. VATECH Europe has strengthened its market position by developing eco-conscious imaging devices with reduced power consumption and lead-free components, aligning with EU Green Deal objectives. Its EZImplant software, which combines CBCT data with surgical planning tools, has gained traction among implantologists in Italy and Spain. The company also partners with European dental schools to integrate its imaging platforms into curricula, ensuring early adoption among new practitioners.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Digital Dental X-ray Market pursue several strategic imperatives to sustain competitiveness. They embed artificial intelligence into imaging software to enhance diagnostic accuracy and automate analysis in compliance with the EU Medical Devices Regulation. They ensure full interoperability with electronic health records, hird-party/D/CADM systems through standardised DICOM and HL7 protocols. They invest in cybersecurity measures, including end-to-end encryption and GDPR compliant cloud storage, to protect patient radiographic data. They localise technical support and training programs to address workforce skill gaps in digital radiography across diverse member states. They also design low radiation, low energy hardware to align with both EU radiation safety directives and sustainability mandates.

MARKET SEGMENTATION

This research report on the europe digital dental X-ray market has been segmented and sub-segmented into the following categories.

By Product

- X-ray

- BCT

- Intraoral Camera

- Optical Imaging

By Method

- Extraoral

- Intraoral

By Application

- Diagnostic

- Therapeutic

- Cosmetic

- Forensic

By End-user

- Dental Clinic

- Dental Labs

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers behind the growth of the Europe Digital Dental X-ray Market?

Factors include the rising incidence of dental diseases, increased awareness about oral health, technological innovations, and the growing adoption of advanced imaging devices across dental practices in Europe.

2. Which countries in Europe are leading in the adoption of digital dental X-ray systems?

Germany, the UK, and France are major markets due to their advanced healthcare infrastructure, increasing dental care expenditure, and high adoption of new dental technologies

3. What are the major challenges faced by the Europe Digital Dental X-ray Market?

High costs of digital X-ray systems, lack of reimbursement policies, and the need for continuous technological upgrades pose significant barriers to market growth.

4. What types of digital X-ray systems are most common in Europe?

Intraoral and extraoral X-ray systems dominate, with cone-beam computed tomography (CBCT) gaining traction for 3D imaging and enhanced diagnostic accuracy.

5. What technological innovations are shaping the Europe Digital Dental X-ray Market?

Integration with practice management software, AI-powered diagnostics, portable systems, and higher-resolution imaging are major innovations propelling market growth.

6. What role does patient awareness play in the Europe Digital Dental X-ray Market?

Growing patient awareness about the benefits of digital imaging—such as lower radiation exposure and faster results—drives demand, especially among young and elderly populations.

7. Which companies are key players in the European digital dental X-ray industry?

Major players include Danaher Corporation, Carestream Health, Dentsply Sirona, Planmeca, and Vatech, all investing heavily in innovative products and strategic partnerships.

8. How does the demographic profile influence the Europe Digital Dental X-ray Market?

An aging population with higher susceptibility to oral diseases and rising dental concerns among youth contribute significantly to increased demand for advanced imaging solutions in Europe.

9. What are the advantages of digital X-ray systems over traditional film-based systems?

Digital systems offer quicker image processing, lower radiation doses, enhanced image quality, and easier sharing and storage, which improve diagnostic precision and patient outcomes.

10. What factors could limit the growth of the Europe Digital Dental X-ray Market?

High costs, lack of insurance coverage, and low awareness in certain regions could slow down market penetration and hinder widespread adoption.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com