Europe Dry Beans Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Common Beans, Navy Beans, Kidney Beans, Pinto Beans), Grade, Cultivation Method, And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 To 2034)

Europe Dry Beans Market Report Summary

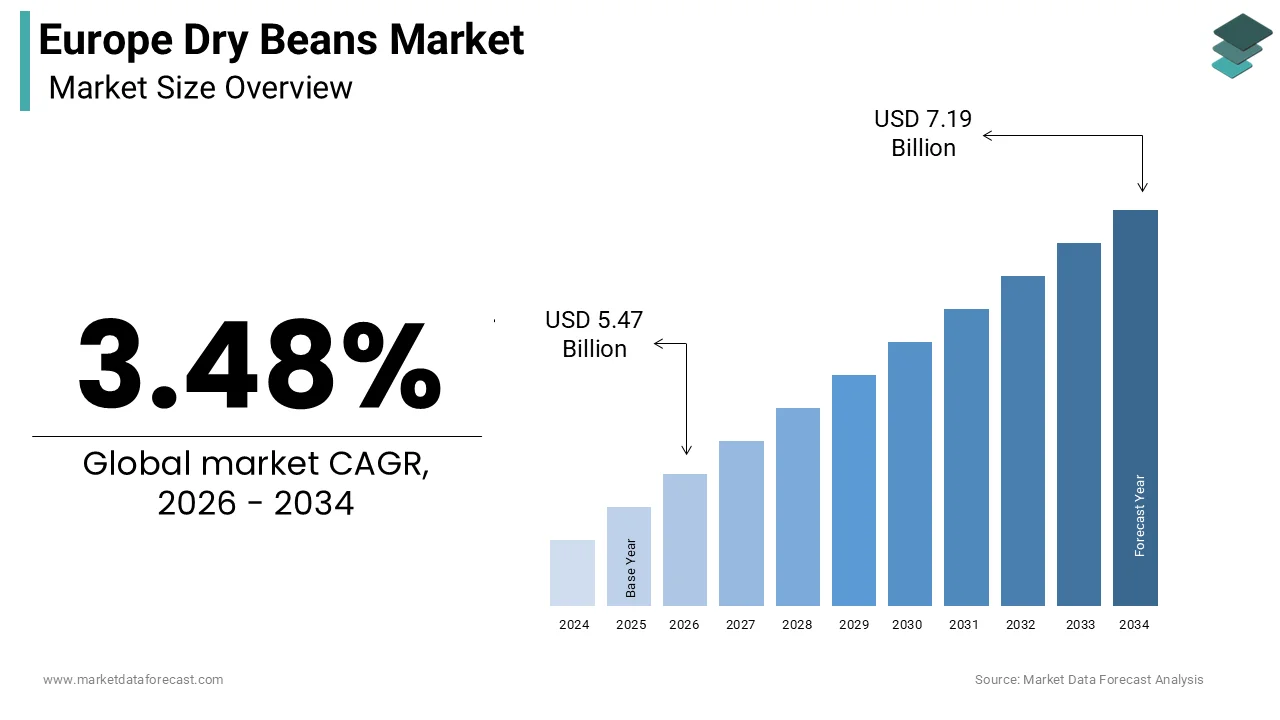

The Europe dry beans market was valued at USD 5.28 billion in 2025 and is projected to reach USD 7.19 billion by 2034, growing from USD 5.47 billion in 2026 at a CAGR of 3.48% during the forecast period. Market growth is driven by increasing consumer preference for plant-based protein, rising health awareness, growing demand for sustainable food products, and expanding adoption of legumes in daily diets. Government initiatives promoting healthy eating and sustainable agriculture, along with increasing demand for protein-rich foods, are further supporting market expansion.

Key Market Trends

- Rising demand for plant-based protein and vegetarian diets.

- Increasing consumption of high-fiber and nutrient-rich legumes.

- Growing popularity of organic and sustainably sourced dry beans.

- Expansion of convenience food products featuring dry beans.

- Increasing investments in sustainable agriculture and pulse production.

Segmental Insights

- Based on Type, the common beans segment dominated the Europe dry beans market in 2025 by accounting for the largest market share. The segment's growth is attributed to its versatility, affordability, nutritional value, and widespread use in traditional European cuisines.

- Based on Grade, the US No. 1 grade segment held the largest share of the market in 2025 due to its superior quality, uniformity, and strong preference among commercial food processors, retailers, and exporters.

- Based on Cultivation Method, the conventional cultivation segment dominated the Europe dry beans market in 2025, owing to its cost-effectiveness, high production capacity, and ability to meet large-scale commercial demand across the region.

Regional Insights

- Spain dominated the Europe dry beans market in 2025, supported by extensive bean cultivation, favorable climatic conditions, strong domestic consumption, and a well-established processing industry.

- France is expected to maintain a significant market position during the forecast period due to continued government support for domestic pulse production, increasing plant-based food consumption, and sustainable agriculture initiatives.

- Italy is anticipated to witness steady market growth, driven by its long-standing culinary tradition, consistent demand for premium legumes, and increasing consumer preference for healthy, protein-rich foods.

- Germany is projected to experience sustained growth in the dry beans market due to rising health consciousness, expanding vegan and vegetarian populations, and increasing demand for plant-based protein sources.

- The United Kingdom is expected to witness continued market expansion, supported by growing adoption of plant-based diets, increasing demand for sustainable food products, and rising awareness of the nutritional benefits of dry beans.

Competitive Landscape

The Europe dry beans market is highly competitive, with companies focusing on product quality, sustainable sourcing, organic product offerings, and value-added packaged bean products. Market participants are investing in product innovation, strategic partnerships, and expanding distribution networks to strengthen their competitive positions.

Key players operating in the Europe dry beans market include Bonduelle Group, Princes Group, Conserve Italia, Cirio, Hodmedod's, Lupa Foods, Brusco Food Group, CIACAM, Forest Whole Foods, Merchant Gourmet, Bioitalia, D'aucy, Pedon S.p.A., Napolina, and Valfrutta.

Europe Dry Beans Market Size

The Europe dry beans market size was calculated at USD 5.28 billion in 2025 and is anticipated to reach USD 7.19 billion by 2034, from USD 5.47 billion in 2026, growing at a CAGR of 3.48% during the forecast period.

Dry beans are legumes such as kidney beans, navy beans, and pinto beans that are harvested in a dried state for long-term storage and culinary use. These pulses serve as a vital source of plant-based protein and dietary fiber, aligning with the continent’s shifting nutritional priorities. According to Eurostat data, the European Union produced approximately 1.2 million tonnes of dry pulses, including beans and lentils, in 2022, which reflects the region’s growing emphasis on crop diversification. As per industry observations, consumer awareness regarding sustainable diets has surged, with plant-based food sales increasing by 15% across major European markets in recent years. Dry beans offer a low-carbon-footprint alternative to animal proteins, requiring significantly less water and land for cultivation. The Farm to Fork Strategy aims to reduce pesticide use by 50% and increase organic farming area to 25% by 2030, creating a favorable environment for pulse cultivation. Despite this potential, Europe remains a net importer of dry beans, relying on supplies from North America and Africa to meet domestic demand. The versatility of dry beans in traditional and modern cuisines supports their steady integration into daily diets. As health consciousness rises and environmental concerns mount, dry beans are positioned as a cornerstone of sustainable food systems across the continent.

MARKET DRIVERS

Rising Consumer Preference for Plant-Based Protein Sources

The escalating demand for plant-based protein is one of the major factors propelling the expansion of the European dry beans market as consumers actively seek alternatives to meat and dairy products. Health concerns related to red meat consumption, including cardiovascular diseases and obesity, have prompted a dietary shift toward legumes. According to the European Commission, the average European consumes 16 kilograms of pulses per year, but this figure is expected to rise as national dietary guidelines increasingly recommend higher pulse intake. In Germany, for instance, public health campaigns have encouraged citizens to replace one meat meal per week with a plant-based option, which is leading to a 10% increase in pulse purchases. Dry beans are rich in essential amino acids, fiber, and micronutrients, making them an ideal component of balanced vegetarian and vegan diets. According to market surveys, the number of vegans in Europe has doubled in the last five years, reaching approximately 3.5 million individuals. This demographic expansion directly correlates with increased retail sales of dry beans in supermarkets and specialty stores. Furthermore, the affordability of dry beans compared to processed meat substitutes makes them accessible to a broader socioeconomic spectrum. Retailers are responding by expanding shelf space for various bean varieties and offering bulk options. The cultural acceptance of beans in Mediterranean cuisines further supports their adoption in Northern European countries, where consumption was historically lower. This widespread dietary transition ensures sustained demand growth for dry beans across the region.

Government Initiatives Promoting Sustainable Agriculture and Crop Rotation

Strategic government policies aimed at enhancing soil health and reducing agricultural emissions are significantly boosting the cultivation and consumption of dry beans in Europe, which is another major market driver. Legumes like dry beans have the unique ability to fix atmospheric nitrogen into the soil, reducing the need for synthetic fertilizers. The European Union’s Common Agricultural Policy provides direct payments to farmers who adopt crop rotation practices that include legumes. According to the French Ministry of Agriculture, the national protein plan aims to double the production of plant proteins by 2030 to reduce dependence on imported soybeans for animal feed, leading to a 20% increase in the area dedicated to pulse crops, including dry beans, over the past three years. Additionally, the Green Deal targets a 20% reduction in fertilizer use by 2030, making nitrogen-fixing crops economically attractive for farmers. Subsidies for organic farming also favor dry bean production as these crops thrive without chemical inputs. According to regional agricultural data, Spain has seen a 15% rise in dry bean acreage due to regional incentives supporting sustainable water use and soil conservation. These policy frameworks not only encourage production but also promote the environmental benefits of pulses to consumers. By aligning agricultural subsidies with ecological goals, governments are creating a robust supply chain for dry beans. This regulatory support ensures that dry beans remain a key component of Europe’s sustainable agriculture strategy.

MARKET RESTRAINTS

Competition from Imported Pulses and Price Volatility

The Europe dry beans market faces significant restraint from the influx of cheaper imported pulses, which often undercut local producers on price. Countries such as Canada and Argentina are major exporters of dry beans to Europe due to their large-scale mechanized farming and lower production costs. According to trade data from the International Trade Centre, Europe imported over 600,000 tonnes of dry beans primarily from North America in 2022. This reliance on imports creates price volatility that disadvantages European farmers who operate under stricter environmental and labor regulations. The cost of production in Europe is approximately 30% higher than in major exporting nations due to compliance with EU standards. Fluctuations in global currency exchange rates further exacerbate price instability, making it difficult for local producers to compete consistently. During periods of high global supply, European prices drop, forcing some domestic farmers to switch to more profitable crops like cereals. The lack of sufficient storage infrastructure for pulses in certain European regions also leads to post-harvest losses and reduced market availability. Consumers often prioritize price over origin, leading to a preference for cheaper imported varieties in budget-conscious segments. This competitive pressure limits the growth potential of the local dry bean industry. Without protective measures or premium branding strategies, European producers struggle to maintain market share against global giants.

Consumer Perception and Culinary Preparation Barriers

Despite their nutritional benefits, dry beans face resistance from consumers who perceive them as time-consuming and difficult to prepare, which is further hampering the regional market expansion. The long soaking and cooking times required for dry beans deter busy urban populations who prefer convenience foods. According to consumer studies, 40% of European consumers avoid cooking dry beans due to the perceived effort involved compared to canned or pre-cooked alternatives. This preference for convenience limits the market potential for raw dry beans, particularly among younger demographics. The lack of culinary knowledge on how to properly prepare and season beans also contributes to low consumption rates in Northern Europe, where beans are not traditionally staple foods. In countries like Sweden and Denmark, pulse consumption remains below the European average due to limited familiarity with diverse bean recipes. Educational gaps in schools and households mean that many consumers do not know how to incorporate dry beans into daily meals effectively. While canned beans offer a solution, they often contain added sodium and preservatives, which health-conscious buyers seek to avoid. The gap between the intention to eat healthy and actual cooking behavior remains a significant barrier. Retailers and manufacturers have struggled to bridge this gap through simple packaging instructions alone. Until preparation becomes easier or consumer habits shift significantly, the growth of the dry bean segment will remain constrained by these behavioral factors.

MARKET OPPORTUNITIES

Expansion of Value-Added and Convenience Bean Products

The development of value-added and convenience-oriented dry bean products presents a substantial opportunity for market growth in Europe. Manufacturers are introducing pre-soaked quick-cook beans and seasoned bean mixes that reduce preparation time while retaining the nutritional benefits of whole pulses. According to industry reports, the global convenience food market is growing at a rate of 5% annually, and this trend is evident in the pulse sector. Companies are launching ready-to-cook kits that include dry beans with spices and recipe cards, appealing to novice cooks. In the United Kingdom, sales of convenience pulse products increased by 12% in 2023 as retailers focused on easy meal solutions. Innovations in packaging, such as vacuum-sealed bags with clear cooking instructions, enhance shelf appeal and user experience. The rise of meal kit delivery services also incorporates dry beans as a key ingredient, exposing new consumers to their versatility. For instance, these services reported a 20% increase in plant-based meal selections featuring legumes. By addressing the convenience barrier, manufacturers can tap into the large segment of time-poor consumers who wish to eat healthily. Furthermore, the introduction of flavored dry bean blends caters to diverse palates, encouraging experimentation. This product evolution transforms dry beans from a basic commodity into a convenient culinary ingredient. Such innovations align with modern lifestyle demands and drive higher value sales in the retail sector.

Integration into Alternative Protein and Food Tech Innovations

The integration of dry beans into alternative protein formulations and food technology innovations offers a lucrative opportunity for the European market. Food scientists are utilizing bean flours and isolates to create plant-based meats, cheeses, and snacks due to their functional properties and neutral taste. According to market projections, the European alternative protein market is expected to reach 10 billion euros by 2030, driven by demand for sustainable food sources. Dry beans provide a locally sourced ingredient for these products, reducing reliance on imported soy and pea protein. Startups in Germany and the Netherlands are developing bean-based pasta and bread that offer higher protein content than traditional wheat products. These innovations appeal to health-conscious consumers seeking gluten-free or high-fiber options. The technical ability of bean flour to improve texture and moisture retention in baked goods expands its application scope. Major food manufacturers are investing in research to optimize bean extraction processes for better yield and quality. Collaborations between agricultural cooperatives and food tech companies facilitate the supply of high-quality bean raw materials. This industrial demand creates a new revenue stream for dry bean producers beyond traditional retail. As consumer acceptance of plant-based alternatives grows, the demand for bean-derived ingredients will surge. This shift positions dry beans as a critical raw material in the future food landscape.

MARKET CHALLENGES

Climate Change Impact on Yield Stability and Quality

Climate change poses a significant challenge to the Europe dry beans market by causing unpredictable weather patterns that affect crop yields and quality. Dry beans are sensitive to temperature fluctuations and water stress during the flowering and pod-filling stages. According to agricultural assessments, extreme heatwaves in Southern Europe reduced bean yields by up to 25% in affected regions in 2022. Drought conditions in Spain and Italy have forced farmers to irrigate more frequently, increasing production costs and straining water resources. Conversely, excessive rainfall in Northern Europe leads to waterlogging and fungal diseases that damage crops. These climatic variabilities make it difficult for farmers to predict harvest volumes and maintain a consistent supply. The quality of beans is also compromised under stress conditions, resulting in smaller seeds and lower market value. Insurance costs for pulse crops are rising as weather risks intensify, making farming less economically viable for some producers. The lack of drought-resistant bean varieties adapted to specific European microclimates further exacerbates the issue. Research into climate-resilient strains is ongoing, but deployment takes time. Until adaptive measures are widely adopted, the market will face supply disruptions and price spikes. This instability discourages long-term investment in bean cultivation and affects retailer confidence in securing steady supplies.

Regulatory Hurdles and Pesticide Residue Standards

Strict regulatory standards regarding pesticide residues and genetic modification are further challenging the regional market growth. The European Union maintains some of the toughest maximum residue limits for pesticides globally, which can lead to rejection of shipments that exceed these thresholds. For instance, several consignments of imported dry beans were rejected at European borders in 2023 due to detected levels of unauthorized pesticides. Compliance with these standards requires rigorous testing and certification, which increases operational costs for suppliers. The ban on certain neonicotinoid pesticides has also limited the tools available to farmers for pest control, potentially affecting yields. Organic certification, while beneficial, commands a premium price that not all consumers are willing to pay. The complexity of navigating different national regulations within the EU adds an administrative burden to traders. Small-scale farmers often lack the resources to implement comprehensive residue monitoring programs. This regulatory environment creates a barrier to entry for new suppliers and limits market access for conventional producers. Importers must invest in advanced testing facilities to ensure compliance, which raises overall costs. Any deviation from strict standards can result in significant financial losses and reputational damage. These hurdles necessitate continuous adaptation and investment in clean production methods.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.48% |

| Segments Covered | By Type, Grade, Cultivation Method, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Bonduelle Group, Princes Group, Conserve Italia, Cirio, Hodmedod's, Lupa Foods, Brusco Food Group, CIACAM, Forest Whole Foods, Merchant Gourmet, Bioitalia, D'aucy, Pedon S.p.A., Napolina, Valfrutta. |

SEGMENTAL ANALYSIS

By Type Insights

The common beans segment led the market by accounting for the major share of the European market in 2025 due to their exceptional versatility and deep integration into traditional European cuisines. These beans, including varieties like cannellini and borlotti, are staples in Mediterranean diets, particularly in Italy and Spain, where they feature prominently in soups, stews, and salads. According to the Food and Agriculture Organization, legumes are a critical component of the Mediterranean diet, which is recognized by UNESCO as an intangible cultural heritage. This cultural endorsement drives consistent demand across households and food service establishments. Common beans absorb flavors well and maintain texture during long cooking processes, making them ideal for hearty winter dishes that remain popular in Northern Europe. Retailers stock a wide variety of common beans, reflecting consumer preference for diverse culinary options. The adaptability of these beans to both traditional recipes and modern fusion cuisines ensures broad appeal. In France, common beans are essential for cassoulet, a national dish that sustains high consumption levels year-round. The widespread availability of recipes and cooking instructions further supports their dominance. Consumers appreciate the mild flavor profile that allows for creative seasoning. This culinary flexibility, combined with cultural significance, secures the leading status of common beans in the European market.

However, the black beans segment is estimated to exhibit the fastest CAGR in the European market over the forecast period, owing to the rising popularity of international and fusion cuisines. The influence of Latin American and Caribbean culinary traditions has introduced black beans to European palates through dishes like tacos, burritos, and rice bowls. For instance, the number of Mexican and Latin American restaurants in Europe has increased by 20% in the last five years, exposing more consumers to black bean-based meals. Younger demographics, particularly in urban centers, are eager to experiment with global flavors, driving demand for authentic ingredients. Social media platforms play a crucial role in popularizing black bean recipes among millennials and Gen Z consumers who seek diverse dining experiences. Food bloggers and influencers frequently feature black beans in healthy bowl recipes, enhancing their visibility and appeal. Supermarkets have responded by expanding their ethnic food aisles to include black beans alongside other international staples. The distinct earthy flavor and firm texture of black beans make them suitable for modern salad bars and grain bowls. This culinary trend is not limited to restaurants but extends to home cooking as consumers recreate restaurant-style meals. The growing acceptance of multicultural diets ensures sustained growth for black beans in the European market.

By Grade Insights

The US No. 1 grade segment had the largest share of the European market in 2025 because it represents the standard for quality and consistency required by commercial buyers. This grade ensures uniform size, color, and minimal defects, which are critical for industrial processing and retail packaging. Large food manufacturers and institutional caterers prefer US No. 1 beans to maintain product consistency and minimize waste during preparation. The United States Department of Agriculture sets strict criteria for this grade, ensuring that beans meet high visual and physical standards. Importers rely on this certification to guarantee quality when sourcing from international suppliers. The reliability of US No. 1 beans reduces the risk of customer complaints and returns for retailers. In the food service sector, consistency is key to menu planning and cost control, making this grade the preferred choice. The widespread recognition of US No. 1 as a benchmark for quality facilitates trade and simplifies procurement processes. Distributors can easily market this grade, knowing it meets established expectations. The trust in this grading system supports its dominance in the market. Commercial contracts often specify US No. 1 to ensure supply chain efficiency. This standardization drives volume sales and establishes US No. 1 as the backbone of the European dry bean trade.

On the other hand, the organic certified segment is predicted to grow at a promising CAGR in the European market over the forecast period, owing to the increasing consumer demand for chemical-free and environmentally friendly products. European consumers are becoming more aware of the harmful effects of pesticide residues in food, leading to a shift toward organic options. According to the European Commission, the organic food market grew by 10% annually in recent years, reflecting this strong trend. Organic dry beans are produced without synthetic fertilizers or pesticides, aligning with consumer values regarding health and sustainability. Parents particularly seek organic beans for children to minimize exposure to potentially harmful chemicals. The label Organic Certified serves as a trust signal, assuring buyers of strict production standards. Retailers are expanding their organic sections to meet this growing demand. Online grocery platforms also highlight organic beans, making them easily accessible to health-conscious shoppers. The willingness to pay a premium for organic products supports market growth. Certifications provide transparency and credibility, encouraging trial and repeat purchases. As awareness of environmental issues rises, more consumers choose organic beans to support sustainable farming practices. This ethical consumption pattern drives the rapid expansion of the Organic Certified segment in the European market.

By Cultivation Method Insights

The conventional cultivation segment occupied the major share of the European market in 2025 and is estimated to remain the leading method in the Europe dry beans market over the forecast period due to its cost efficiency and ability to produce large volumes for mass-market accessibility. Conventional farming utilizes synthetic fertilizers and pesticides to maximize yields and protect crops from pests and diseases. This approach allows farmers to produce beans at lower costs, which translates to affordable prices for consumers. The majority of European households purchase conventional beans because they fit within tight household budgets. Supermarkets rely on the steady supply and low price point of conventional beans to drive volume sales. The established infrastructure for conventional farming, including machinery and supply chains, ensures reliable production. Most imported beans from major producing countries are grown conventionally, further reinforcing their dominance. The familiarity of conventional farming practices among growers reduces operational risks and complexity. While organic methods are gaining traction, they still represent a niche segment compared to the vast scale of conventional production. The affordability of conventional beans makes them a staple for institutional feeding programs and food aid initiatives. This economic advantage secures the leading position of conventional cultivation in the market.

However, the organic cultivation segment is the fastest-growing segment and is projected to progress at the fastest CAGR in the European market over the forecast period, owing to the increased health consciousness and the clean label trend among European consumers. Buyers are increasingly scrutinizing ingredient lists and production methods, preferring products free from synthetic additives. Organic dry beans appeal to this demographic as they are perceived as purer and safer. The clean label movement emphasizes transparency and naturalness, which aligns with organic certification standards. Consumers associate organic beans with better taste and higher nutritional value, although scientific consensus varies. The desire to avoid genetically modified organisms also drives interest in organic options, since GMOs are prohibited in organic farming. Marketing campaigns by health brands highlight the benefits of organic pulses, influencing consumer choices. Specialty stores and upscale supermarkets dedicate significant shelf space to organic beans, catering to this niche. The growth of online health food retailers further expands access to organic products. Younger consumers are particularly influenced by ethical considerations and personal health goals, favoring organic options. This shift in consumer mindset fuels the rapid expansion of the organic segment. As education on food quality improves, more people are likely to switch to organic beans.

REGIONAL ANALYSIS

Spain Dry Beans Market Analysis

Spain led the market by holding the major share of the European market in 2025 and is likely to strengthen its market position over the next few years by leveraging its agricultural expertise and culinary tradition to sustain production and export. The country is one of the largest producers of dry beans in Europe, particularly in regions like Castilla y León. Spanish consumers have a deep cultural connection to legumes, featuring them in traditional dishes like fabada asturiana. The government supports pulse production through subsidies aimed at improving sustainability and crop rotation. Spain exports a substantial portion of its bean harvest to other European countries, leveraging its high-quality reputation. The domestic market is robust, with high per capita consumption driven by health awareness. Retailers offer a wide variety of local and imported beans catering to diverse tastes. The focus on organic farming is growing in Spain, aligning with EU goals. Climate challenges pose risks, but irrigation investments help maintain output. Spain’s role as both producer and consumer makes it a key player in the regional market.

France Dry Beans Market Analysis

France is expected to maintain a prominent position in the Europe dry beans market through continued policy support for domestic plant protein production over the next several years. French cuisine values high-quality legumes such as flageolet and tarbais beans, which have protected geographical indications. The national protein plan encourages domestic production to reduce import dependence. Consumers in France are increasingly adopting flexitarian diets, boosting bean sales. Supermarkets feature extensive bean selections, including organic and heirloom varieties. The food service sector integrates beans into menus to meet sustainability targets. France imports significant volumes to meet demand during the off-season. Government campaigns promote the health benefits of pulses, influencing consumer behavior. The country’s strong retail network ensures wide availability. France’s emphasis on quality and origin supports premium bean segments. Its strategic initiatives strengthen its market standing.

Italy Dry Beans Market Analysis

Italy is anticipated to see steady demand and consistent production of high-quality legumes over the coming years, supported by a strong cultural preference for traditional ingredients. Iconic culinary uses of legumes in pasta, soups, and side dishes keep them at the heart of the Italian diet. Regions like Tuscany are famous for specific bean varieties such as cannellini, which are central to local identity. Italian consumers prioritize quality and flavor, driving demand for premium dried beans. The country produces high-value beans but also imports large quantities for industrial use. Retailers focus on traditional and organic options, appealing to health-conscious shoppers. The Mediterranean diet framework supports regular bean consumption. Italy’s food industry uses beans in ready meals and snacks, expanding market reach. Government incentives for sustainable agriculture benefit bean farmers. The cultural pride in local produce sustains strong domestic demand. Italy’s influence on European culinary trends boosts bean popularity.

Germany Dry Beans Market Analysis

Germany is likely to experience sustained growth in its dry beans market over the next few years as health and wellness trends continue to influence consumer preferences. Although not a traditional staple, bean consumption is growing rapidly among younger demographics. The country is a major importer of dry beans to meet increasing demand. German retailers offer diverse bean products, including organic and convenience formats. Public health initiatives encourage pulse intake to improve national diet quality. The food tech sector in Germany uses beans for alternative protein innovation. Supermarkets expand shelf space for legumes, reflecting consumer interest. Germany’s strong economy supports premium bean sales. The focus on sustainability drives preference for eco-friendly packaging. Germany’s dynamic market drives regional growth.

United Kingdom Dry Beans Market Analysis

The United Kingdom is expected to continue its focus on plant-based nutrition, with dry beans serving as an increasingly important component of the national diet over the next few years. British consumers are increasingly incorporating beans into daily meals for health and environmental reasons. The UK imports most of its dry beans, relying on global supply chains. Retailers promote beans as affordable and nutritious staples. The rise of veganism and vegetarianism boosts demand. Government dietary guidelines recommend higher pulse consumption. Convenience formats like canned beans are popular due to busy lifestyles. The UK market is sensitive to price and quality. Online sales of beans are growing rapidly. The country’s diverse population influences varied bean preferences. The UK’s market dynamics reflect broader European trends.

COMPETITION OVERVIEW

The competition in the Europe dry beans market is characterized by a mix of international traders, local distributors, and specialized organic brands who compete on quality, price, and sustainability credentials. Large importers dominate the volume segment by leveraging economies of scale and global sourcing networks to offer competitive prices to retailers and industrial buyers. Meanwhile, niche players focus on premium segments such as organic heirloom and fair trade beans, appealing to conscientious consumers willing to pay higher prices. The market is fragmented at the retail level with numerous private labels competing alongside established brands for shelf space. Differentiation is increasingly driven by transparency initiatives where companies provide detailed information about origin and farming practices. Regulatory compliance with European food safety standards acts as a barrier to entry for smaller, unverified suppliers. Innovation in packaging and convenience formats also serves as a competitive tool to attract busy urban consumers. Collaborative efforts between producers and retailers help promote pulse consumption through joint marketing campaigns. Price volatility due to weather conditions and global supply dynamics adds complexity to competitive strategies. Overall, the market rewards participants who can balance cost efficiency with strong sustainability narratives and consistent product quality.

KEY MARKET PLAYERS

A few major players of the Europe dry beans market include

- Bonduelle Group

- Princes Group

- Conserve Italia

- Cirio

- Hodmedod's

- Lupa Foods

- Brusco Food Group

- CIACAM

- Forest Whole Foods

- Merchant Gourmet

- Bioitalia

- D'aucy

- Pedon S.p.A

- Napolina, Valfrutta

Top Strategies Used by Key Market Participants

Key players in the Europe dry beans market primarily focus on product differentiation through the introduction of heirloom and specialty varieties to cater to diverse culinary preferences. Companies invest in sustainable sourcing practices to align with consumer demand for environmentally friendly and ethically produced foods. Strategic partnerships with local farmers and cooperatives help secure stable supply chains and ensure quality consistency. Marketing efforts emphasize the health benefits of pulses, including high protein and fiber content, to attract health-conscious consumers. Brands also leverage digital platforms to share recipes and cooking tips, which encourages trial and regular consumption. Packaging innovations such as resealable bags and eco-friendly materials enhance convenience and appeal to environmentally aware buyers. Retailers collaborate with manufacturers to create private-label organic lines that offer competitive pricing. Educational campaigns aim to overcome barriers related to preparation time by promoting quick-cook and pre-soaked options. These multifaceted strategies enable companies to capture value in a competitive landscape while supporting the growth of the plant-based diet trend across Europe.

Leading Players in the Europe Dry Beans Market

- Hurst Bean Company has established a strong presence in the European market by supplying premium quality heirloom and specialty dry beans to retailers and food service providers. The company focuses on educating consumers about the nutritional benefits and culinary versatility of various bean varieties through engaging digital content and recipe collaborations. Recent actions include expanding its distribution network across major European supermarkets and partnering with local chefs to promote traditional bean dishes. Hurst Bean Company also emphasizes sustainable farming practices by working directly with growers who adhere to strict environmental standards. This direct sourcing model ensures traceability and consistent quality, which appeals to health-conscious European consumers. The company actively participates in food festivals and agricultural exhibitions to increase brand visibility and connect with end users. By offering unique varieties not commonly found in standard retail outlets, Hurst Bean Company differentiates itself from competitors. Its commitment to preserving genetic diversity in legumes supports long-term agricultural resilience. These strategic initiatives strengthen its reputation as a provider of high-quality and distinctive dry bean products in Europe.

- Eosta is a leading distributor of organic fruits and vegetables that has significantly contributed to the Europe dry beans market by promoting organic and fair trade pulses. The company uses its Nature & More transparency system to provide detailed information about the social and environmental impact of bean production. This approach resonates with European consumers who prioritize ethical sourcing and sustainability. Eosta recently expanded its portfolio of organic dry beans by collaborating with smallholder farmers in Africa and South America. These partnerships ensure stable supply chains and fair compensation for producers. The company also invests in marketing campaigns that highlight the health benefits of organic legumes. Eosta works closely with retailers to create dedicated organic pulse sections that attract niche buyers. Its focus on storytelling and transparency builds trust and loyalty among customers. By championing regenerative agriculture practices, Eosta supports soil health and biodiversity. These efforts position the company as a key player in the sustainable segment of the European dry beans market.

- Agri Trading International plays a vital role in the Europe dry beans market by facilitating the import and distribution of large volumes of conventional and organic beans. The company leverages its extensive global network to source high-quality beans from major producing regions such as North America and Argentina. Agri Trading International recently invested in advanced storage facilities in Northern Europe to improve product preservation and reduce waste. This infrastructure enhancement allows the company to maintain a consistent supply even during seasonal fluctuations. The company also focuses on building long-term relationships with European processors and manufacturers who require reliable bulk ingredients. Agri Trading International adheres to strict quality control measures to meet European safety standards. Its logistical expertise ensures timely delivery and competitive pricing for clients. The company actively monitors market trends to adjust its sourcing strategies accordingly. By providing efficient supply chain solutions, Agri Trading International supports the stability of the European dry beans market. Its operational efficiency and reliability make it a preferred partner for many industry stakeholders.

MARKET SEGMENTATION

This research report on the Europe dry beans market has been segmented and sub-segmented based on type, grade, cultivation method, and region.

By Type

- Common Beans

- Navy Beans

- Kidney Beans

- Pinto Beans

- Black Beans

By Grade

- Choice

- Fancy

- US No. 1

- US No. 2

By Cultivation Method

- Organic

- Conventional

- Non-GMO

- Heirloom

By Region

- North America

- Europe

- South America

- Asia-Pacific

- Middle East and Africa

Frequently Asked Questions

1. What is driving the growth of the Europe Dry Beans Market?

Growing consumer preference for plant-based proteins, increasing health awareness, rising vegan and vegetarian populations, and demand for sustainable food products are key growth drivers.

2. Which type of dry bean holds the largest market share?

Kidney beans hold a significant share because they are widely used in soups, salads, ready meals, and traditional European cuisines.

3. What are the major applications of dry beans?

Dry beans are primarily used in household cooking, processed foods, canned products, ready-to-eat meals, soups, snacks, and foodservice applications.

4. Why is demand for dry beans increasing in Europe?

Consumers are seeking affordable, nutritious, and protein-rich foods, while the popularity of plant-based diets continues to rise across the region.

5. Which distribution channel leads the market?

Supermarkets and hypermarkets dominate the market due to their wide product selection, competitive pricing, and extensive retail networks.

6. What challenges does the Europe Dry Beans Market face?

Climate-related impacts on crop production, fluctuating raw material prices, import dependence, and supply chain disruptions are major challenges.

7. Who are the key players in the Europe Dry Beans Market?

Major companies include Bonduelle Group, Princes Group, Conserve Italia, Cirio, Pedon S.p.A., Bioitalia, and Valfrutta.

8. Which end-user segment accounts for the largest market share?

The household consumption segment holds the largest share due to increasing home cooking and healthy eating trends.

9. How is innovation shaping the Europe Dry Beans Market?

Manufacturers are introducing convenient packaging, pre-cooked beans, flavored bean products, and ready-to-cook meal solutions to attract consumers.

10. What is the future outlook for the Europe Dry Beans Market?

The market is expected to witness steady growth, supported by increasing demand for plant-based nutrition, sustainable agriculture, and convenient healthy food products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com