Europe ePharmacy Market (Online Pharmacy Market) Size, Share, Trends & Growth Forecast Report By Product Type, Drug Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) Industry Analysis From 2026 to 2034.

Europe ePharmacy Market Size

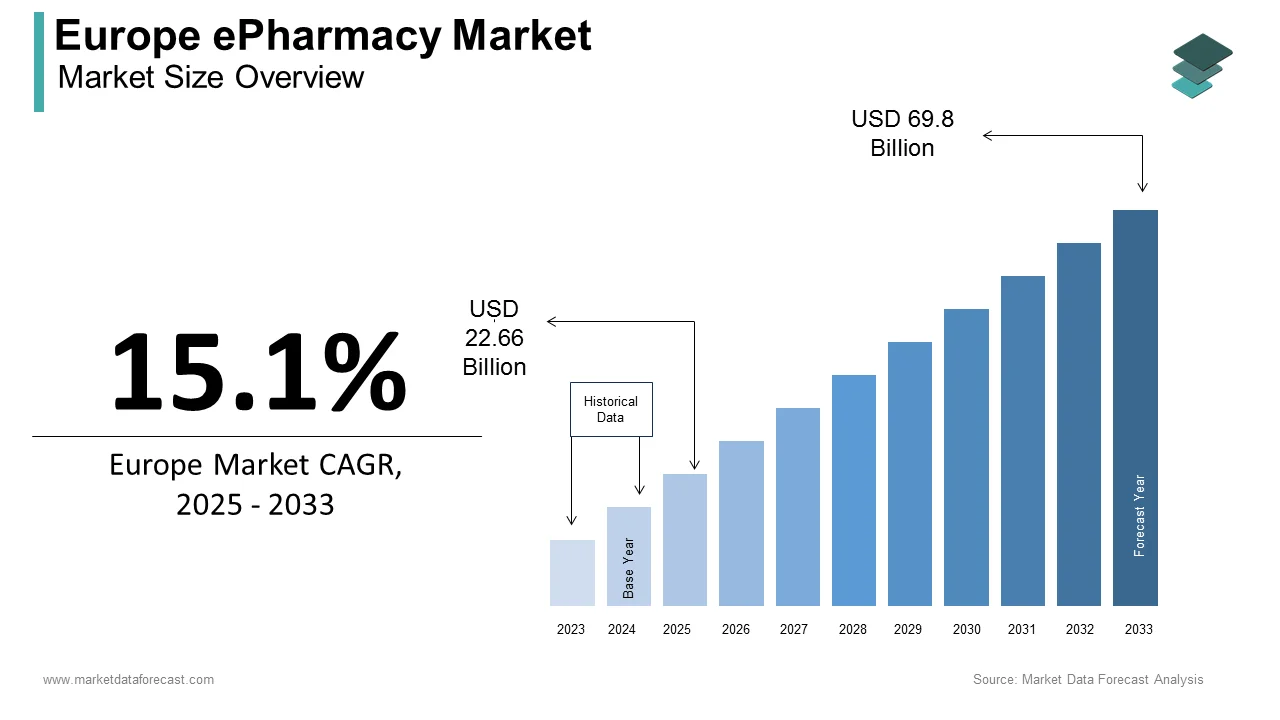

The size of the Europe ePharmacy market was valued at USD 22.66 billion in 2025. This market is expected to grow at a CAGR of 15.1% from 2026 to 2034 and be worth USD 80.34 billion by 2034 from USD 26.08 billion in 2026.

The ePharmacy is the digital ecosystem enabling the online ordering, dispensing, and delivery of prescription and over-the-counter medicines through licensed platforms compliant with national pharmaceutical regulations. According to the European Commission, as of 2023, all 27 EU member states have established national electronic prescription systems or are in advanced implementation phases, laying the groundwork for integrated digital pharmacy services. Telehealth integration has further accelerated adoption, as per the Organisation for Economic Co-operation and Development, which notes that 18 European countries now allow ePharmacies to fulfill prescriptions issued during virtual consultations.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Fuels Demand for Continuous Medication Access

The growing burden of chronic non-communicable diseases across Europe is majorly boosting the growth of the Europe ePharmacy market. As per the European Centre for Disease Prevention and Control, over 44 % of adults in the European Union live with at least one chronic condition, such as hypertension, diabetes, or cardiovascular disease, requiring long-term pharmacotherapy. As per the European Patients’ Forum, 68% of chronic disease patients in France and Italy preferred online pharmacy services for maintenance medications due to reduced travel burden and wait times.

Expansion of Digital Health Infrastructure Enables Seamless ePrescription Fulfillment

The maturation of Europe’s digital health infrastructure, like national electronic prescription systems, is additionally fuelling the growth of Europe's ePharmacy market. As per the European Commission’s Digital Health and Care Progress Report 2023, 21 EU member states have fully operational ePrescription networks that allow prescribers to send secure digital scripts directly to patients’ chosen pharmacies, including licensed online providers. These systems eliminate paper-based inefficiencies, reduce prescription errors, and empower patient choice.

MARKET RESTRAINTS

Fragmented National Regulatory Frameworks Impede Cross-Border Scalability

The significant regulatory fragmentation across member states is limiting pan-European operational models, which is limiting the growth of the Europe ePharmacy market. As per the European Association of ePharmacies, only 15 of the 27 EU countries permit cross-border online medicine sales to consumers, while others, such as Spain and Italy, restrict ePharmacies to domestic operations only. Prescription verification protocols also vary widely in France; electronic prescriptions require a unique secure token issued by the Assurance Maladie system, whereas in Poland, a simple digital signature suffices. These discrepancies force companies to develop country-specific compliance architectures, increasing operational complexity and cost.

Persistent Consumer Skepticism Regarding Medicine Authenticity and Safety

The rising concerns over counterfeit medicines and data privacy despite robust regulatory safeguards, are also hampering the growth of the Europe ePharmacy market. Although the EU Falsified Medicines Directive mandates safety features like unique identifiers and anti-tampering devices on all prescription packs, public awareness of these measures remains low. Rebuilding trust requires coordinated public education and transparent verification mechanisms beyond regulatory compliance alone.

MARKET OPPORTUNITIES

Integration with Telemedicine Platforms Creates End-to-End Digital Care Journeys

The strategic convergence of ePharmacy with telemedicine services presents a high potential opportunity to deliver seamless virtual care experiences across Europe. Germany’s DiGA framework has approved 38 digital health applications that include ePrescription and pharmacy fulfillment modules, enabling statutory health insurers to reimburse the full care pathway. This integration is especially impactful for mental health; in Sweden, the Mindler platform connects patients with psychiatrists and automatically routes prescriptions to affiliated ePharmacies with discreet packaging.

Growth of Personalized and Specialty Medication Demand Opens Premium Service Avenues

The rising use of personalized and specialty medicines, such as biologics, orphan drugs, and pharmacogenomically tailored therapies that is likely to create new opportunities for the growth of the Europe ePharmacy market. As per the European Organisation for Rare Diseases, over 30 million people in Europe live with one of 6,000 rare conditions, many requiring complex cold chain logistics and patient support programs. Companies like Zur Rose in Switzerland have launched dedicated specialty divisions offering 24/7 pharmacist hotlines and digital adherence tools. The European Medicines Agency approved 18 new orphan drugs in 2023 alone, signaling sustained pipeline growth.

MARKET CHALLENGES

Cybersecurity Vulnerabilities Threaten Patient Data and Operational Integrity

The digitization of pharmacy services exposes the Europe ePharmacy market to escalating cybersecurity risks that jeopardize sensitive health data and supply chain integrity. In 2022, a major German ePharmacy suffered a breach affecting over 200,000 customer accounts, including national insurance numbers and medication histories, as reported by the Federal Office for Information Security.

Workforce Shortages in Community Pharmacy Strain Hybrid Service Models

The operational paradox, as chronic workforce shortages in traditional community pharmacy undermine the hybrid models many online providers rely on, is also hampering the growth of the Europe ePharmacy market. Since most European ePharmacies are legally required to employ licensed pharmacists for prescription verification and patient counseling, this scarcity constrains scalability. In Italy, where online pharmacies must be linked to a physical apothecary, the closure of over 1,200 rural pharmacies between 2018 and 2023 has directly limited ePharmacy licensing opportunities as documented by the Italian National Institute of Statistics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Drug Type, and Country. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe. |

| Market Leaders Profiled | Wal-Mart Stores, Inc.; CVS Health; Express Scripts Holding Company; DocMorris (Zur Rose Group AG); The Kroger Co.; Walgreen Co.; Rowlands Pharmacy; OptumRx, Inc, Giant Eagle, Inc., and Others. |

SEGMENTAL ANALYSIS

By Product Type

The vitamins segment held 31.2% of the Europe ePharmacy market share in 2024, with the heightened consumer awareness of preventive health, accelerated by post-pandemic wellness trends and national public health messaging. The UK’s National Health Service launched a national vitamin D supplementation campaign in 2021, targeting at-risk populations, directly boosting online sales through affiliated ePharmacies.

The weight loss segment is projected to grow with an expected CAGR of 16.2% during the forecast period owing to the rising obesity prevalence and the medicalization of weight management, particularly with the advent of GLP-1 receptor agonists like semaglutide. As per the World Health Organization’s European Regional Office, 59 % of adults in the EU are overweight or obese, creating substantial demand for clinically supported interventions. Additionally, the European Commission’s 2022 “EU Action Plan on Childhood Obesity” has spurred parental interest in safe adolescent weight management solutions available through regulated online channels.

By Drug Type

The over-the-counter medicines segment was the largest and held a dominant share of the Europe ePharmacy market in 2024. As per the European Commission, over 80 % of European households manage minor ailments through self-care, with 54 % preferring online channels for convenience and price comparison, according to a 2022 Eurobarometer health survey. Retail dynamics further favor OTC; ePharmacies like Apotea in Sweden generate over 75 % of revenue from OTC bundles that include vitamins, skincare, and pain relief. The absence of electronic prescription dependencies allows seamless cross-border sales by enabling platforms to serve multiple markets with standardized inventories. This regulatory and operational flexibility ensures OTC remains the backbone of Europe’s digital pharmacy ecosystem.

The prescription drugs segment is lucratively growing with an expected CAGR of 14.7 % throughout the forecast period, with the continent-wide rollout of national ePrescription systems and policy shifts enabling digital dispensing for chronic and specialty medications. As per the European Commission, 21 EU countries now support direct electronic transmission of prescriptions to licensed online pharmacies, eliminating paper referrals.

COUNTRY LEVEL ANALYSIS

Germany Market Analysis

Germany was the largest contributor in the Europe ePharmacy market with 26.3% of share in 2024, with high digital literacy, strong consumer demand for convenience, and a progressive yet regulated legal framework. The country’s statutory health insurance system covers over 87 % of the population, and recent reforms allow ePharmacies to process electronic prescriptions directly from physicians through the national TI platform. Major players like DocMorris and Shop Apotheke have invested heavily in AI-driven adherence tools and same-day delivery networks in urban centers.

United Kingdom Market Analysis

The United Kingdom was ranked second by capturing 19.2% of the Europe ePharmacy market share in 2024, with the early adoption, mature e-commerce infrastructure, and integration with the National Health Service digital ecosystem. As per the Medicines and Healthcare products Regulatory Agency, a public register of licensed online sellers, fostering consumer trust that Boots and Chemist4U together account for over 60 % of online prescription volume.

France Market Analysis

France ePharmacy market growth is likely to expand with an expected CAGR of 14.3% during the forecast period. According to the French National Order of Pharmacists, only 450 online pharmacies were licensed in 2023, all required to be extensions of brick-and-mortar pharmacies and prohibited from selling prescription drugs online. The Assurance Maladie system’s Carte Vitale enables instant reimbursement for eligible OTC items purchased online, a unique feature in Europe.

COMPETITIVE LANDSCAPE

The Europe ePharmacy market features a competitive landscape shaped by a mix of regional specialists, multinational retailers, and digital health innovators. Established players like Zur Rose Apotea and Boots dominate through regulatory compliance, robust logistics, and deep integration with national health systems. These companies leverage their licensed pharmacy status to offer both prescription and over-the-counter products while maintaining strict adherence to the EU Falsified Medicines Directive. Simultaneously agile startups are entering niche segments such as personalized supplementation and chronic disease management using AI-driven platforms. Competition intensifies around user experience, delivery speed, and data security with firms investing heavily in mobile applications, automated warehouses, and cybersecurity protocols. Regulatory fragmentation across member states creates both barriers and opportunities as companies tailor operations to local rules while pursuing cross-border scalability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe ePharmacy market include

- Wal-Mart Stores, Inc.

- CVS Health

- Express Scripts Holding Company

- DocMorris (Zur Rose Group AG)

- The Kroger Co.

- Walgreen Co.

- Rowlands Pharmacy

- OptumRx, Inc.

- Giant Eagle, Inc.

Top Players in the Europe ePharmacy Market

- Zur Rose Group is a leading European ePharmacy headquartered in Switzerland with extensive operations across Germany, France, and the Netherlands. The company operates under well-known brands such as DocMorris and has pioneered digital health integration by offering teleconsultations, medication delivery, and adherence support through a unified platform. Zur Rose has strengthened its position by obtaining national pharmacy licenses in multiple EU countries and investing in automated fulfillment centers to ensure next-day delivery. Recently, the company launched a personalized health assistant powered by artificial intelligence that provides medication reminders and lifestyle tips based on user profiles.

- Apotea AB is a prominent Swedish ePharmacy that has established a strong presence in the Nordic region and expanded into Germany and the Netherlands. The company is recognized for its seamless integration with Sweden’s national ePrescription system and its customer-centric logistics model offering same-day dispatch and carbon-neutral delivery. Apotea has enhanced its market position by developing a proprietary digital platform that combines medication management, health tracking, and pharmacist chat support. In recent years, the company introduced subscription services for chronic medication and wellness products, enabling automated refills and cost savings for users.

- Boots UK, a subsidiary of Walgreens Boots Alliance, operates one of the most trusted online pharmacy platforms in Europe, serving millions of customers across the United Kingdom and Ireland. The company leverages its extensive physical pharmacy network to support hybrid services, including click and collect prescription fulfillment and virtual consultations with registered pharmacists. Boots has strengthened its digital offering by integrating its ePharmacy platform with the NHS Electronic Prescription Service, enabling seamless prescription processing for repeat medications.

Top Strategies Used by the Key Market Participants

Key players in the Europe ePharmacy market employ several strategic approaches to enhance competitiveness and ensure regulatory compliance. They invest in advanced digital platforms that integrate electronic prescriptions, telehealth consultations, and medication adherence tools to deliver end-to-end care. Companies prioritize logistics optimization through automated fulfillment centers and sustainable last-mile delivery networks to guarantee speed and reliability. Strategic partnerships with national health systems, insurers, and electronic health record providers facilitate seamless data exchange and reimbursement. Compliance with country-specific pharmacy laws and GDPR remains central to operational design. Additionally, firms expand product portfolios beyond medicines to include vitamins, skincare and wellness bundles to increase basket size and customer retention in a highly regulated yet evolving digital health environment.

MARKET SEGMENTATION

This Europe ePharmacy market research report is segmented and sub-segmented into the following categories.

By Product Type

- Skin Care

- Cold and Flu

- Vitamin

- Dental Care

- Weight Loss

- Others

By Drug Type

- Prescription Drugs

- Over The Counter (OTC)

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe ePharmacy Market and what are the key growth drivers?

The Europe ePharmacy Market involves online platforms that enable consumers to purchase prescription and OTC medications digitally. Growth is driven by rising internet penetration, growing chronic disease prevalence, telemedicine integration, and government support for digital healthcare solutions

2. Which countries lead the Europe ePharmacy Market?

The United Kingdom leads with high digital adoption and NHS telemedicine initiatives, followed by Germany, France, Spain, and Italy

3. How is telemedicine influencing the Europe ePharmacy Market?

Telemedicine integration facilitates digital prescriptions and remote consultations, raising demand for convenient online medication services

4. What types of products dominate the Europe ePharmacy Market?

Prescription medicines and OTC products comprise the major offerings, with increasing demand for chronic disease management medications

5. What are the regulatory challenges in the Europe ePharmacy Market?

Diverse national regulations on online drug sales, digital prescriptions, and safety compliance pose challenges to pan-European market integration

6. How is technology shaping the Europe ePharmacy Market?

AI-driven personalized medicine, secure payment systems, blockchain-based drug verification, and mobile app platforms are key technological enablers

7. What role does consumer behavior play in Europe’s ePharmacy Market growth?

Increasing preference for home delivery, contactless transactions, and digital health management drives consumer adoption

8. Who are the major players in the Europe ePharmacy Market?

Leading companies include DocMorris (Zur Rose Group), CVS Health, Walgreens Boots Alliance, The Kroger Co., and Walmart

9. How does chronic disease prevalence impact the Europe ePharmacy Market?

Chronic illnesses like diabetes and cardiovascular diseases increase recurring medicine needs, fueling online pharmacy growth

10. How important is logistics and last-mile delivery in the Europe ePharmacy Market?

Efficient logistics and quick doorstep deliveries are critical to customer satisfaction and market expansion, especially in rural areas

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com