Europe Edible Packaging Market Size, Share, Trends & Growth Forecast Report – Segmented By Material (Protein, Polysaccharides, Lipid, and Others), Product Type, End Use, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Edible Packaging Market Size

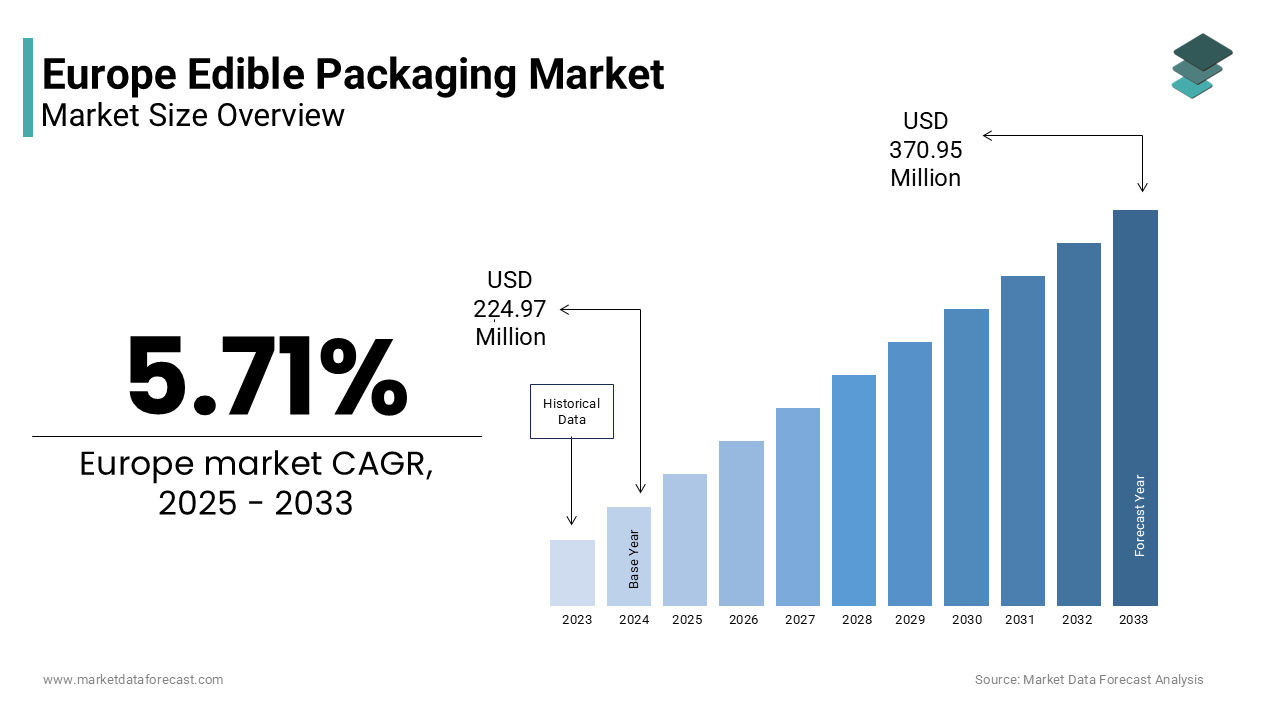

The Europe edible packaging market size was valued at USD 224.97 million in 2024 and is projected to reach USD 370.95 million by 2033 from USD 237.83 million in 2025, growing at a CAGR of 5.71%.

Edible packaging refers to biodegradable films or containers made from food grade materials such as seaweed starch cellulose or proteins that safely encase consumables and can be eaten or composted without environmental residue. In Europe this innovation responds directly to legislative pressure and consumer rejection of single use plastics. The EU is enacting stronger packaging regulations to boost reuse and recycling, while fostering new sustainable solutions like edible packaging to meet broader environmental goals. According to research, significant amounts of plastic packaging waste, heavily driven by food packaging, are generated in the EU, prompting stricter measures against single-use plastics. A strong majority of Europeans favor banning non-essential, single-use plastic packaging for convenience items, indicating public demand for stricter controls on these products. Pilot deployments by major brands, such as edible water pods at music festivals in Sweden and seaweed based soup sachets in German supermarkets, demonstrate real world viability. These developments position edible packaging not as a novelty but as a functional response to Europe’s binding circular economy obligations and evolving consumer ethics.

MARKET DRIVERS

EU Regulatory Push to Eliminate Single Use Plastic Packaging

The European Union’s binding legislative framework against single use plastics has created a structural opening for edible alternatives, which propels the growth of the Europe edible packaging market. Regulatory frameworks increasingly mandate a shift towards reusable or economically viable recyclable packaging alternatives. Proposed regulations are recognizing edible packaging as a strategy for reducing material use at the source. Observations indicate that a substantial portion of municipal waste is attributed to packaging materials. National legislation has been introduced in some regions to prohibit plastic wrapping for designated fresh produce items. Following these changes, retailers are experimenting with edible coatings on produce. Government bodies are also allocating dedicated funding to support pilot programs for edible packaging in sectors like hospitality and takeaway services. These regulatory interventions transform edible packaging from experimental to strategically necessary.

Consumer Rejection of Plastic Waste in Food Consumption Contexts

European consumers increasingly view plastic packaging as incompatible with sustainable lifestyles particularly in on the go food and beverage scenarios, which further fuels the expansion of the Europe edible packaging market. A notable majority of consumers in some regions indicate a significant level of discomfort with the use of single-use plastic packaging for condiments and beverages during public events. More than half of shoppers express a preference for products with innovative, sustainable packaging solutions, such as those that are edible or water-soluble, even when this choice involves a higher cost. Urban consumer groups, particularly the millennial demographic, appear to be early adopters of these new packaging formats. A considerable number of food vendors in major cities have independently transitioned to incorporating plant-based alternatives for single-use items like sauce pods. Major event and festival organizers are increasingly implementing policies that require the use of reusable or edible packaging options as part of their operational licensing, contributing to a substantial reduction in waste generated per attendee. This behavioral shift creates organic demand that complements regulatory drivers and accelerates commercial scaling of edible formats in high visibility consumption settings.

MARKET RESTRAINTS

High Production Costs and Limited Economies of Scale

The commercial viability of edible packaging remains constrained by significantly higher production expenses compared to conventional plastics, which restricts the growth of the edible packaging market. The average cost of edible seaweed-based water pods is notably higher than that of standard plastic bottles. Manufacturing processes for edible protein-based films currently operate at a fraction of their theoretical capacity, constrained by batch processing and a lack of continuous high-speed machinery. Consequently, economies of scale have not been realized. A small proportion of food packaging manufacturers have invested in edible film extrusion equipment, indicating uncertainty about the return on investment. The economic unfeasibility for small and medium food brands to absorb the cost differential will persist until public subsidies or shared infrastructure address the significant capital expenditure barriers, despite supportive market trends.

Technical Limitations in Barrier Properties and Shelf Life

Edible packaging materials often lack the moisture oxygen and grease barrier performance required for many food applications leading to premature spoilage or textural degradation, which impedes the expansion of the Europe edible packaging market. Starch-based films generally demonstrate a high rate of water vapor transmission compared to common synthetic packaging materials. Protein-based sachets have been observed to lose structural integrity relatively quickly when exposed to typical ambient humidity levels, limiting their viability for conventional retail supply chains. Cellulose films treated with a lipid layer have a limited capacity to prevent the onset of rancidity in products with high fat content over an extended period. These limitations restrict edible packaging to dry short shelf life or refrigerated items thereby excluding large segments like baked goods snacks and frozen foods. The technology's environmental benefits are clear, but widespread adoption is hindered because material science has not yet provided durable, multi-functional edible structures.

MARKET OPPORTUNITIES

Integration Into Event and Hospitality Sustainability Mandates

Festivals stadiums and corporate cafeterias across the region are adopting edible packaging as a visible tool to meet zero waste commitments, which is predicted to drive the growth of the Europe edible packaging market. A significant number of major events have required food services to eliminate conventional plastic use entirely, incorporating novel solutions like edible water containers and sauce packets. Certain regional authorities have established requirements for event organizers to submit specific waste reduction plans, favoring innovative packaging alternatives in their evaluations. Large-scale corporate dining facilities are increasingly incorporating edible items, such as stirrers and seaweed-based cups, into their daily operations to reduce waste volume. Some national regulatory bodies have formally acknowledged edible materials as viable alternatives under existing waste reduction legislation. This institutional adoption creates high visibility pilots that normalize the technology and generate performance data to inform broader commercial use in retail and food service chains.

Expansion in Pharmaceutical and Supplement Single Dose Formats

The European pharmaceutical sector is exploring edible packaging for unit dose vitamins supplements and oral care products where purity and waste reduction align with regulatory and consumer expectations. This generates fresh prospects for the Europe edible packaging market. A substantial volume of single-dose sachets, primarily composed of non-recyclable laminated plastic, are routinely utilized for the consumption of specific vitamins and supplements across many regions. A shift in packaging materials is emerging, with the introduction and approval of edible, bio-based film wrappers for certain types of health products. Consumer acceptance of this innovative, edible packaging format has been positive following its introduction in certain markets. Industry-wide regulatory frameworks and material safety standards for these types of edible components are currently under consideration by authoritative bodies. Several products utilizing edible film strips for ingredient delivery have been successfully introduced into retail markets. The push for sustainable healthcare in the EU opens high-margin doors for edible packaging, providing a manageable regulatory path for this niche.

MARKET CHALLENGES

Inconsistent Food Safety and Cross Contamination Regulations

The regulatory classification of edible packaging remains ambiguous across EU member states creating compliance uncertainty, which is among the major challenges for the Europe edible packaging market. Regulatory bodies are observing edible films through a dual lens, categorizing them as both direct food ingredients and materials that contact food. The approach to classifying and permitting these films is not uniform, varying significantly among different regions. One jurisdiction requires comprehensive safety assessments for protein-derived films, whereas another permits certain seaweed derivatives through simplified historical consumption rules. This lack of consistency among different regional frameworks creates complexity, which can affect how quickly developers can bring new products to market. Official guidance has recognized these inconsistencies in classification. However, comprehensive standardization across the varied frameworks has not yet been established. Consequently, a seaweed pod approved in the Netherlands may face rejection in Spain due to differing allergen labeling interpretations. The lack of a consolidated EU approach to safety assurance and certification will hinder innovation, leading to companies exploiting regulatory loopholes and facing significant legal liability.

Consumer Hesitation Due to Sensory and Hygiene Perceptions

Many European consumers remain reluctant to adopt edible packaging due to concerns about taste texture and cleanliness, despite environmental appeal, which holds back the expansion of the Europe packaging market. A notable portion of consumers in certain European regions express unease about consuming packaging materials that have been touched or exposed to external environments, even if the material is certified as safe for food contact. Consumer concerns about the safety of edible films during the transportation phase have led to a substantial volume of public inquiries in one specific European country. Sensory experience is a key barrier to acceptance, with a significant percentage of trial participants in one country rejecting specific types of edible pods due to an undesirable residual taste. Neutral flavor formulations exist, but they result in increased cost and complexity. These perceptual hurdles are particularly strong in conservative food cultures where the boundary between product and container is culturally ingrained. For edible packaging to move beyond a niche and into the mainstream market, consumers must be educated and assured through transparent hygiene certifications, or technical progress will not be enough.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.71% |

| Segments Covered | By Material, Product Type, End Use, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Tate & Lyle PLC, Ingredion, Incorporated, DuPont de Nemours, Inc., Koninklijke DSM N.V., Kerry Group PLC, MonoSol, LLC (KURARAY CO., LTD.), Cargill Corporation, Notpla Limited, Lactips, Pace International, LLC (Valent BioSciences LLC), and TIPA Corp Ltd |

SEGMENTAL ANALYSIS

By Material Insights

The polysaccharides segment dominated the Europe edible packaging market by accounting for a 48.6% share in 2024. The dominance of the polysaccharides segment is credited to the abundance and regulatory acceptance of seaweed-based materials, as well as superior film formation and mechanical strength. Seaweed derived polysaccharides such as sodium alginate and carrageenan benefit from established use in food applications and favorable regulatory status across the EU. A variety of seaweed species is recognized as suitable for human consumption, facilitating rapid product introduction when traditional processing techniques are applied. When certain seaweed-derived materials are used as processing aids, it simplifies regulatory and labeling burdens for food manufacturers. Companies are scaling up manufacture of novel product forms, such as edible pods for liquids and sauces, and there is a trend towards commercial deployment at major public events. The expansion of regional cultivation is projected to establish a reliable domestic supply chain. Polysaccharide based films exhibit excellent mechanical properties and transparency making them ideal for visible packaging applications. Observations indicate that certain types of films derived from marine plant matter demonstrate mechanical properties that align with conventional, petroleum-derived film materials. The same films are noted to possess characteristics that allow for complete consumption and biological decomposition. Specific blends of starches and marine plant polymers have been observed to sustain structural integrity over a three-day duration when kept in typical climate-controlled environments. These characteristics have driven adoption in bakery wraps fresh produce stickers and single serve condiment pods. Polysaccharide films offer a sustainable, drop-in solution for Europe's millions of tons of fruit and vegetable packaging waste, aligning performance with circularity and cementing their market leadership.

The protein based edible packaging segment is expected to exhibit a noteworthy CAGR of 21.3% between 2025 and 2033 due to High Barrier Properties Against Oxygen and Aromas, and valorization of dairy and agricultural byproducts. Protein films derived from whey soy and zein offer exceptional oxygen barrier performance critical for preserving sensitive foods like nuts dairy and baked goods. Milk protein isolate films exhibit low oxygen permeability, outperforming standard polysaccharide alternatives. This enhanced barrier quality facilitates the extension of shelf life for food products without the need for synthetic coatings. There is an observable pattern of incorporating milk-based edible wraps into premium food product lines to reduce conventional plastic use while maintaining product freshness. Casein films demonstrate effectiveness in preventing lipid oxidation in specific snack food items under typical retail conditions. Protein-based barriers are unlocking new edible packaging applications for short-shelf-life foods, meeting the EU's push for plastic elimination. Protein based films align with Europe’s circular bioeconomy strategy by transforming waste streams into high value materials. There is an observable trend toward repurposing manufacturing byproducts that were previously considered low-value waste. Significant quantities of liquid byproducts from one production process are being redirected to become primary material inputs for different product types. The application of specific proteins derived from manufacturing remnants is shifting toward the creation of edible packaging materials. Demonstration projects have successfully scaled the use of a plant-based press cake into molded trays for retail food products. Support is evident for commercial initiatives exploring the conversion of spent grain proteins into durable items like edible cutlery. The European Commission’s Circular Economy Action Plan explicitly encourages such cascading use of biomass. Protein films are transforming waste into valuable assets, which is spurring investment through public funding and corporate partnerships; this, in turn, is speeding up research and development and expanding their use beyond specialized applications.

By Product Type Insights

The films segment led the Europe edible packaging market by capturing a share of 52.3% in 2024. The leading position of the films segment is driven by versatility in wrapping and lidding applications, and compatibility with existing food processing infrastructure. Edible films serve as direct replacements for plastic wraps lids and sachets across diverse food categories. Experimental use of starch-based film material in the packaging of fresh pasta demonstrated a complete replacement of single-use plastic while maintaining product quality during trials with retailers. A range of commercial applications for edible films have been documented, spanning various product categories such as bakery overwraps, cheese lidding, and pouches for frozen fruit. Their thin flexible nature allows integration into existing form fill seal machinery with minimal retrofitting. This adaptability across high volume and high visibility settings ensures films remain the dominant format. Unlike rigid edible containers films can be produced via continuous casting or extrusion processes compatible with current packaging lines. According to sources, a notable of horizontal flow wrappers used in confectionery can accommodate edible films with only minor tension adjustments. This lowers adoption barriers for small and medium food producers who lack capital for new equipment. Scalable solutions such as films are essential for plastic reduction within Europe's food manufacturing sector, largely made up of SMEs, thus ensuring sustained demand for such innovations.

The edible coatings segment is predicted to witness the highest CAGR of 24.1% over the forecast period owing to direct application on fresh produce to extend shelf life, and reduction of post harvest losses in horticultural supply chains. Edible coatings applied directly to fruits vegetables and eggs create a protective barrier that reduces moisture loss respiration and microbial growth, eliminating the need for plastic overwraps. The application of a specific coating to a delicate fruit variety has been observed to extend its shelf life during retail presentation. A different type of produce coating was noted for its ability to preserve textural integrity and visual appeal over a period of several weeks in an organic context. Certain retailers are now offering specific coated fruit and vegetable items without conventional plastic packaging in several regions. So, these coatings offer a regulatory compliant and consumer accepted alternative, which drives explosive adoption. Europe loses millions of tons of food annually post harvest, according to sources, with fresh produce accounting for a portion of waste. Edible coatings directly address this by enhancing durability during transport and storage. The application of a specific type of organic coating on certain fruits has been observed to mitigate physical damage during simulated supply chain conditions. In one region, financial support for the use of coating applicators by producers of a particular fruit variety correlated with a noticeable reduction in the volume of produce that was unsuitable for market sale after processing. The emphasis on reducing the overall volume of discarded food products within a major economic area suggests that technologies enhancing product durability are becoming strategically important for various stakeholders throughout the supply chain. Their dual benefit of waste reduction and plastic elimination positions them as the highest growth vector in edible packaging.

By End Use Insights

The Food & Beverages segment held the majority share of the Europe edible packaging market in 2024. The supremacy of the Food & Beverages segment is led by regulatory mandates against plastic in fresh food packaging, and consumer demand for plastic free on the go consumption. A regulatory measure requires the removal of plastic packaging for numerous categories of loose fruits and vegetables. This directive applies across a wide range of produce items, covering several dozen specific types. The change suggests a significant reduction in the quantity of plastic materials previously used for produce identification and wrapping will occur annually once the new rule is in full effect. Retailers like Lidl and Aldi have already launched pilot programs using edible chitosan coatings on citrus and tomatoes in Germany and Spain. Food and beverage applications naturally dominate the market because edible films and coatings provide similar functionality to traditional packaging without requiring expensive or extensive changes to existing infrastructure. European shoppers increasingly reject plastic in ready to eat and beverage contexts. According to a study, a notable share of respondents in Sweden Denmark and the Netherlands supported bans on plastic water bottles and condiment sachets at public events. This sentiment has driven large scale adoption of edible pods at festivals stadiums and airports. Large-scale athletic events and cultural festivals have begun integrating biodegradable seaweed-based alternatives to traditional single-use beverage containers. International retailers are transitioning away from plastic condiment packaging in favor of edible starch-based solutions across their regional operations. These high visibility deployments normalize edible packaging and generate performance data that accelerates retail adoption—cementing food and beverage as the primary end use segment.

The pharmaceuticals segment is estimated to register the fastest CAGR of 28.7% from 2025 to 2033. The rapid expansion of the pharmaceuticals segment is fuelled by demand for plastic free unit dose delivery of vitamins and supplements, and regulatory incentives for sustainable healthcare packaging. There is substantial consumption of single-dose vitamin and supplement packets across the region, with the majority of this packaging comprising non-recyclable laminated plastic materials. Alternative materials, such as those derived from edible pullulan or starch, are being identified as potentially compliant substitutes for existing packaging solutions. A change in the regulatory landscape has been observed, with a national authority in one major country recently approving the use of an edible wrapper for a common vitamin product, confirming its stability and equivalent bioavailability. A specific brand has successfully introduced melatonin products utilizing an edible strip format into several major cities within a particular market, reporting high rates of repeat customer purchases. The European Pharmacopoeia is finalizing monographs for edible excipients which will standardize safety assessments across member states. The EU Green Deal's focus on healthcare sustainability is driving rapid expansion in a lucrative, specialized market segment. Regulatory guidance within a major economic bloc has started to specifically promote the adoption of ingestible or readily dissolving materials for certain types of common medications. A key healthcare provider in one nation has integrated packaging waste reduction criteria, including the use of consumable formats, into its supplier evaluation metrics. Across another country, a shift in policy permits the reimbursement of certain wellness products when they utilize certified consumable delivery systems. These policy signals create commercial viability even at small scale. Edible packaging presents a viable strategy for pharmaceutical firms to reduce their plastic footprint while maintaining crucial sterility and regulatory compliance amid escalating ESG scrutiny by positioning it as the highest-growth end-use despite its current low market volume.

REGIONAL ANALYSIS

Germany Edible Packaging Market Analysis

Germany was the top performer in the Europe edible packaging market and accounted for a 20.4% share in 2024. The prominence of the German market is attributed to stringent packaging laws the Circular Economy Act and a dense network of food manufacturers seeking plastic alternatives. Major retailers including Aldi and Lidl launched edible coated produce pilots in all federal states. Additionally Germany hosts leading edible packaging innovators like Leaf Republic and Skipping Rocks Lab’s European production hub. Germany's vast food processing sector, coupled with strict sustainability reporting, creates a dual force, regulatory pressure and market demand, that cements its leadership in sustainable practices, driving innovation and compliance across numerous SMEs.

France Edible Packaging Market Analysis

France followed closely in the Europe edible packaging market and captured a 15.8% share in 2024. There has been a transition in the approach to packaging materials, moving away from conventional options toward alternatives that can be consumed or composted. Major retailers have begun using organic, seaweed-derived materials for identification purposes on select produce items. Certain fruits are now being coated with naturally sourced, edible substances across the nation's stores. Initiatives at the regional level are supporting the creation of protective films developed from common agricultural byproducts. Additionally, France’s strong culinary culture embraces edible solutions like wafer cups for ice cream and rice paper wraps for charcuterie. France is a key market for edible packaging due to its leadership in food innovation, highlighted by Paris hosting major summits, and its strong commitment to waste reduction, with ambitious national targets making it ripe for sustainable solutions like edible containers.

United Kingdom Edible Packaging Market Analysis

The United Kingdom is another major player in the Europe edible packaging market. There is a continued trend of regulatory alignment with broad environmental objectives. Significant advancements are being made in the deployment of biodegradable packaging at large-scale public events. Major retailers are implementing innovative, edible barrier technologies for specific fresh produce items. There is increased investment in the development of domestically sourced, bio-based film alternatives London’s concentration of food tech startups and retailer headquarters creates a dynamic ecosystem that drives both innovation and adoption.

Netherlands Edible Packaging Market Analysis

The Netherlands is growing steadily in the Europe edible packaging market owing to its role as Europe’s agricultural and logistics hub combined with advanced food technology research. Wageningen University operates the EU’s largest edible packaging pilot plant producing seaweed and dairy protein films for commercial trials. The Dutch Ministry of Agriculture supports circular packaging through the Green Deal Plastic Free Produce which includes edible coatings as a priority solution. The Netherlands, leveraging Rotterdam's import hub, acts as a vital testbed for integrating edible packaging into high-volume fresh produce logistics.

Sweden Edible Packaging Market Analysis

Sweden is anticipated to expand in the Europe edible packaging market from 2025 to 2033 due to high consumer environmental awareness and progressive municipal policies. Stockholm and Gothenburg require all public event vendors to use edible or compostable packaging with seaweed pods now standard at concerts and sports arenas. A major international furniture and home goods retailer headquartered in the region has initiated a wide-scale rollout of food-safe starch capsules for edible products across its European markets. The national agricultural authority is channeling financial support towards the exploration of innovative, forest-derived food packaging films, utilizing materials sourced from sustainably managed woodlands. A favorable climate for the adoption and widespread acceptance of novel, consumable packaging solutions appears to be present, buoyed by the region's strong public support for limiting conventional plastics and a long-term goal of eliminating landfill waste.

COMPETITIVE LANDSCAPE

The Europe edible packaging market features a dynamic competitive landscape characterized by innovation driven startups regulatory responsiveness and cross sector collaboration. While global packaging giants remain cautious due to technical and scalability challenges nimble specialized firms dominate through agile R and D and targeted applications. Competition centers on material performance including barrier properties shelf life extension and taste neutrality as well as cost competitiveness against conventional plastics. Regulatory knowledge is a critical differentiator with companies that navigate the dual frameworks of food safety and packaging waste legislation gaining faster market entry. The market remains fragmented with no single technology prevailing allowing seaweed starch protein and lipid based solutions to coexist based on application needs. Public funding and retailer partnerships significantly influence commercial viability making collaboration as important as proprietary technology. Despite high growth potential the sector faces barriers in scaling manufacturing and achieving consistent quality which limits competition to a select group of technically adept and well financed innovators.

KEY MARKET PLAYERS

Some of the notable key players in the European edible packaging market are

- Tate & Lyle PLC

- Ingredion, Incorporated

- DuPont de Nemours, Inc.

- Koninklijke DSM N.V.

- Kerry Group PLC

- MonoSol, LLC (KURARAY CO., LTD.)

- Cargill Corporation

- Notpla Limited

- Lactips

- Pace International, LLC (Valent BioSciences LLC)

- TIPA Corp Ltd.

Top Players in the Market

- Notpla Ltd is a pioneering force in the Europe edible packaging market renowned for its seaweed derived packaging solutions that replace single use plastics in beverage and food service applications. The company’s technology transforms brown seaweed into biodegradable and edible films and pods that decompose naturally within weeks. Notpla has deployed its products at high profile events across Europe including the London Marathon and Tomorrowland Festival serving millions of units. Its solutions are now used by major chains such as Lucozade Ribena Suntory and Just Eat. Notpla’s scalable seaweed platform has also attracted global interest with pilot programs in the United States and Asia reinforcing its role as an innovation leader in sustainable packaging worldwide.

- Evoware International BV contributes significantly to the Europe edible packaging market through its plant based edible films made from seaweed and other renewable resources. The company supplies food service operators and retailers with customizable edible sachets wrappers and containers that align with EU plastic reduction mandates. Evoware emphasizes zero waste and ocean friendly materials with all products certified compostable and safe for human consumption. It also collaborated with German event organizers to provide edible water capsules at music festivals. These strategic engagements position Evoware as a key enabler of circular food packaging in Europe while supporting its global mission to replace conventional plastics in emerging and developed markets alike.

- Tipa Corp Ltd plays a strategic role in the Europe edible packaging landscape by complementing its compostable flexible packaging with research into next generation edible barrier layers. While primarily known for fully compostable films Tipa has invested in hybrid edible coating technologies to enhance moisture and oxygen resistance for fresh food applications. The company works closely with European organic food brands and fresh produce exporters to develop packaging that meets both EU sustainability standards and retail shelf life requirements. It also integrated seaweed based edible inks into its labeling systems. These initiatives demonstrate Tipa’s commitment to pushing the boundaries of functional sustainable packaging while maintaining compliance with European regulatory frameworks and expanding its influence across global fresh food supply chains.

Top Strategies Used by the Key Market Participants

Key players in the Europe edible packaging market focus on regulatory alignment material innovation and high visibility pilot deployments. They develop solutions that comply with EU directives banning single use plastics particularly for fresh produce and food service. Companies invest in scalable production of seaweed starch and protein based materials to improve performance and reduce costs. Strategic partnerships with retailers event organizers and public institutions enable real world validation and consumer education. Geographic localization of raw material sourcing and manufacturing ensures supply chain resilience and sustainability credentials. These strategies collectively enhance credibility functionality and market readiness in a region defined by environmental ambition and regulatory rigor.

MARKET SEGMENTATION

This research report on the European edible packaging market has been segmented and sub-segmented based on categories.

By Material

- Protein

- Polysaccharides

- Lipid

- Others

By Product Type

- Films

- Coatings

- Spoon & Fork

- Others

By End Use

- Food & Beverages

- Fresh Food

- Bakery & Confectionary

- Dairy Products

- Others

- Pharmaceuticals

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe edible packaging market?

The Europe edible packaging market includes food-grade packaging materials made from natural, biodegradable ingredients that can be safely consumed along with the packaged product.

2. What factors are driving the growth of edible packaging in Europe?

Key drivers include increasing environmental concerns, strict regulations on plastic waste, growing consumer demand for sustainable packaging, and innovation in food-grade materials.

3. What materials are commonly used in edible packaging?

Common materials include starch, seaweed, proteins, lipids, polysaccharides, and other plant-based or natural biopolymers.

4. Which applications dominate the Europe edible packaging market?

Food and beverage applications dominate the market, particularly for snacks, confectionery, ready-to-eat foods, and beverage packaging.

5. How does edible packaging support sustainability goals?

Edible packaging reduces plastic waste, lowers carbon footprint, and aligns with circular economy and zero-waste initiatives across Europe.

6. What role do regulations play in shaping the market?

European food safety and packaging regulations strongly influence product development, requiring edible packaging to meet strict hygiene, labeling, and safety standards.

7. Which countries are leading the Europe edible packaging market?

Countries such as Germany, the United Kingdom, France, and the Netherlands are leading due to strong sustainability policies and high adoption of eco-friendly packaging.

8. What challenges does the edible packaging market face in Europe?

Challenges include high production costs, limited shelf life, moisture sensitivity, and the need for consumer education regarding usage and safety.

9. Who are the key players in the Europe edible packaging market?

Major companies include Tate & Lyle PLC, Ingredion, DuPont de Nemours, Kerry Group PLC, Cargill Corporation, and Notpla Limited, among others.

10. What is the future outlook for the Europe edible packaging market?

The market is expected to grow steadily, driven by sustainability initiatives, regulatory support, and increasing adoption in the food and beverage sector.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com