Europe Electric Commercial Vehicle Market Size, Share, Trends, and Growth Forecast Research Report, Segmented By Propulsion Type, Vehicle Type, Range Type, Component Type and Country (United Kingdom, France, Spain Germany And Italy, Russia, Sweden, Denmark, Switzerland, Netherlands and Rest of Europe), Industry Analysis From 2026 to 2034

European Electric Commercial Vehicle Market Size

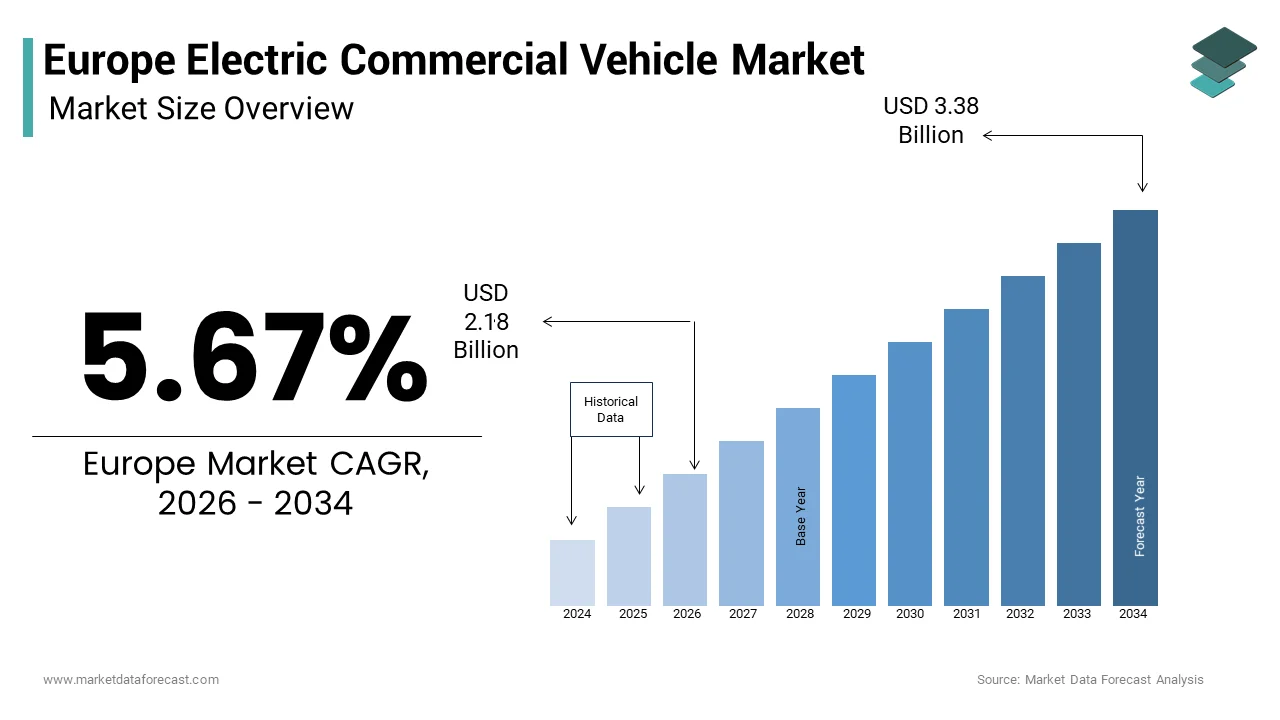

The European electric commercial vehicle market size was valued at USD 2.06 billion in 2025 and is anticipated to reach USD 2.18 billion in 2026 to reach USD 3.38 billion by 2034, growing at a CAGR of 5.67% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Electric Commercial Vehicle Market

An Electric Commercial Vehicle (ECV) is a battery-powered truck, van, or bus used for business operations, logistics, and public transport. These vehicles are distinguished by zero tailpipe emissions, reduced noise pollution, and integration with smart fleet management systems that optimize routing and energy consumption. The European regulatory environment has become a decisive catalyst, with the European Union’s Fit for 55 package mandating a 100 percent reduction in CO2 emissions from new light commercial vehicles by 2035. According to the European Environment Agency (2022/2023 data), road transport accounts for over 21% of the EU's total greenhouse gas emissions, with light-duty vehicles (cars and vans) accounting for over 50% of those transport emissions. As per data up to 2024, the total stock of registered light commercial vehicles (vans) in the EU has surpassed 28 million units, serving as the backbone of last-mile delivery, with new electric van registrations in 2024 accounting for approximately 6-7% of new sales. Municipalities are increasingly restricting internal combustion engine vehicles through low emission zones. Currently, hundreds of low-emission zones are in operation across the EU (with around 70 to 80 in Germany alone), a number that is rapidly expanding, directly accelerating the electrification of urban logistics and public service fleets.

MARKET DRIVERS

Stringent Urban Emission Regulations and Low Emission Zones

Municipal policies enforcing low emission zones across European cities constitute a primary driver for the Europe electric commercial vehicle market. These zones restrict or penalize access for internal combustion engine vehicles based on Euro emission standards, compelling logistics companies and municipal fleets to transition to zero emission alternatives. Driven by national legislation, the number of low-emission zones in European cities is rapidly increasing, with major capitals tightening restrictions and implementing daily charges for non-compliant vehicles. Following the expansion of London’s ULEZ, significant revenue is generated from non-compliant vehicle charges, with net proceeds reinvested into public transport. Meanwhile, the European Commission’s Alternative Fuels Infrastructure Regulation (AFIR) mandates widespread, high-powered charging infrastructure for electric commercial vehicles along major transport corridors and at key urban nodes. This regulatory pressure is particularly acute for last mile delivery operators, who conduct high frequency stops in city centers where air quality limits are most stringent. Companies like DHL and La Poste have publicly committed to electric urban delivery fleets by 2030, citing compliance with evolving municipal rules as a core operational necessity rather than a voluntary sustainability choice.

Corporate Decarbonization Commitments and Fleet Electrification Pledges

Private sector sustainability targets are accelerating the expansion of the Europe electric commercial vehicle market. This is because corporations are embedding zero-emission logistics into their environmental strategies. Major retailers, e commerce platforms, and industrial firms operating in Europe have signed onto initiatives such as the Climate Group’s EV100 campaign, pledging full electrification of their delivery fleets by 2030. According to multiple studies, numerous major corporations with significant European operations have committed to transitioning their light-duty vehicle fleets to electric powertrains within this decade as part of global, high-level corporate sustainability initiatives. Amazon has made a significant investment in an electric delivery fleet, with thousands of vans already operating across various European countries, while Deutsche Post DHL Group continues to expand its low-emission, last-mile delivery fleet. These commitments are not merely symbolic; they translate into long term procurement contracts that provide manufacturers with demand certainty and justify investments in production scaling and battery innovation, thereby reinforcing the market’s growth trajectory.

MARKET RESTRAINTS

Inadequate Public Charging Infrastructure for Heavy Duty Segments

The lack of high power charging infrastructure tailored to medium and heavy duty electric commercial vehicles remains a critical restraint to the Europe electric commercial vehicle market. This is the case despite progress in passenger vehicle charging. Unlike light vans that can recharge overnight at depots, larger electric trucks require megawatt level charging during operational hours, a capability scarcely available across European transport corridors. The European Automobile Manufacturers Association reports that high-capacity charging infrastructure is expanding across the EU but remains heavily concentrated in a few Western European member states. Furthermore, industry bodies and auditors indicate that specialized charging infrastructure for heavy-duty vehicles is currently insufficient, with deployment significantly lagging behind projected needs. This gap forces fleet operators to rely on depot based charging, limiting route flexibility and increasing capital expenditure for on site electrical upgrades. For cross border logistics, the absence of harmonized payment systems and connector standards further complicates operations. High-power charging along corridors must expand rapidly to align with Alternative Fuels Infrastructure Regulation milestones. Otherwise, the electrification of regional and long-haul commercial transport will remain constrained.

High Total Cost of Ownership for Small and Medium Enterprises

The elevated upfront cost of ECV is a significant barrier for small and medium-sized enterprises and a major obstacle to the growth of the Europe electric commercial vehicle market. These businesses dominate Europe’s logistics and service sectors. The total cost of ownership can be favorable over time due to lower fuel and maintenance expenses. However, according to the International Council on Clean Transportation, the initial purchase price remains higher than comparable diesel models. For SMEs operating on thin margins, such as independent courier services, plumbing contractors, or local food distributors, this premium represents a substantial financial hurdle, especially without access to large scale financing or government subsidies. Although national incentive schemes exist, their availability varies widely. For instance, France provides direct financial support to incentivize the purchase of heavy-duty electric trucks, whereas Italy continues to utilize substantial, high-demand, and quickly exhausted, government-backed subsidy programs to drive the adoption of electric vehicles. As per Eurostat, SMEs account for 99 percent of all EU enterprises and employ two thirds of the private sector workforce, making their participation essential for broad market penetration. The transition will remain skewed toward large corporations with balance sheet resilience, slowing overall adoption rates. This is due to a lack of standardized, accessible financing mechanisms and predictable subsidy frameworks across member states.

MARKET OPPORTUNITIES

Expansion of Renewable Powered Depot Charging Solutions

The integration of on-site renewable energy generation with depot charging infrastructure offers a compelling opportunity for the Europe electric commercial vehicle market. This approach enhances the economic and environmental value proposition of electric commercial fleets. Forward looking logistics operators are installing solar canopies and battery storage systems at distribution centers to power vehicle charging with clean, low cost electricity while reducing grid dependence. According to SolarPower Europe, the commercial and industrial solar segment in the European Union has seen continued expansion, while logistics centers have become central to solar deployment due to their large rooftop capacity. Major logistics firms are integrating onsite solar power into their European operations, allowing for increased daytime electric vehicle charging while reducing grid reliance during high-tariff periods. The European Commission’s Net Zero Industry Act further supports this trend by fast tracking permits for renewable projects linked to industrial decarbonization. When combined with time of use electricity pricing and vehicle to grid capabilities, these microgrids can transform depots from passive refueling points into active energy assets, lowering operational costs and improving grid stability. This synergy between clean energy and electric mobility creates a self reinforcing cycle that strengthens the business case for fleet electrification beyond regulatory compliance.

Growth of Urban Micro Mobility and Cargo Bike Integration

The rise of zero emission urban logistics ecosystems that combine electric vans with electric cargo bikes offers a potential prospect to optimize last mile delivery efficiency, which is likely to promote the growth of the Europe electric commercial vehicle market. In dense European cities where traffic congestion and narrow streets impede conventional vehicles, logistics providers are adopting hub and spoke models: electric vans transport parcels to neighborhood micro hubs, from which cargo bikes complete final deliveries. European cities are experiencing rapid growth in cargo bike usage for deliveries, with electric cargo bikes replacing a substantial number of daily urban van trips. Major European logistics companies are also expanding their electric cargo bike fleets to achieve emission-free, last-mile delivery goals. This model reduces delivery times, lowers noise pollution, and aligns with municipal sustainability goals. Critically, it also increases asset utilization by allowing vans to serve multiple micro hubs without entering restricted zones. This integrated approach becomes operationally necessary as cities expand pedestrian zones and reduce parking. Consequently, there is a growing demand for compact electric vans that function as mobile distribution nodes instead of traditional delivery vehicles.

MARKET CHALLENGES

Battery Supply Chain Vulnerabilities and Raw Material Dependence

The region’s reliance on imported battery cells and critical minerals poses a systemic challenge to the scalability and resilience of the Europe electric commercial vehicle market. Europe remains heavily reliant on Asian markets for lithium-ion batteries despite growing domestic manufacturing efforts. A small group of nations controls the majority of essential battery inputs, with China dominating the refining capacity for key materials. This dependency exposes European manufacturers to geopolitical risks and price volatility. For instance, Significant price volatility in the lithium market, including a sharp rise and subsequent collapse, has created substantial planning uncertainty. European initiatives are targeting increased localization of the battery value chain, though current production faces challenges in meeting the high-performance requirements for heavy-duty applications. Europe must secure diversified, ethical, and circular supply chains, including through recycling and alternative chemistries like sodium ion. Until it does, the cost competitiveness and production stability of electric commercial vehicles will remain vulnerable to external disruptions.

Limited Vehicle Range and Payload Capacity Trade Offs

The inherent trade-off between battery weight, cargo volume, and driving range continues to constrain the operational viability and the expansion of the Europe electric commercial vehicle market. This is particularly true in the medium and heavy-duty segments. Current battery technology adds significant mass, reducing allowable payload under EU axle weight limits. For example, a typical 7.5 ton electric truck may carry up to 1,200 kilograms less payload than its diesel counterpart, according to the International Council on Clean Transportation. This penalty directly impacts revenue per trip, especially for high density goods like beverages or construction materials. Additionally, real world range often falls short of advertised figures under cold weather or hilly terrain. Tests by the German Aerospace Center show winter range reductions of up to 40 percent for electric vans. While newer models promise 300 to 400 kilometers, this remains inadequate for regional routes exceeding 500 kilometers without mid journey charging—a scenario impractical for time sensitive deliveries. Fleet operators must carefully redesign logistics networks around vehicle limitations until solid-state batteries or other breakthroughs alleviate current constraints. As a result, the scope of electrification remains limited to predictable, short-radius operations, delaying broader adoption across diverse commercial use cases.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.67% |

| Segments Covered | By Propulsion Type, Vehicle Type, Range, Component Type, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | AB Volvo (Sweden), VDL Bus and Coach (Netherlands), Daimler (Germany), CAF (Spain), EBUSCO (Netherlands), Scania (Sweden), Continental AG, Tesla, Nissan Corporation, Emoss Mobile Systems, and Others. |

SEGMENTAL ANALYSIS

By Propulsion Insights

The Battery Electric Vehicle (BEV) segment dominated the Europe electric commercial vehicle market and accounted for a substantial share in 2025. The dominance of the segment is primarily driven by regulatory alignment and operational simplicity. Unlike hybrid variants, BEVs produce zero tailpipe emissions, making them fully compliant with the European Union’s increasingly stringent urban access regulations, including low emission zones in over 300 cities. According to studies on European mobility, battery electric vehicles demonstrate significantly lower lifecycle greenhouse gas emissions compared to diesel counterparts, particularly as the electricity mix in the EU becomes cleaner. Furthermore, the absence of internal combustion components reduces maintenance complexity and cost, a critical factor for high utilization fleets. National incentive schemes in select European countries are heavily prioritizing zero-emission, pure electric commercial vehicles over combustion engines, with targeted subsidies available for large, heavy-duty electric vans and trucks to support fleet electrification. The European Union's updated Alternative Fuels Infrastructure Regulation (AFIR) mandates the expansion of public and depot charging points along major transport corridors and by vehicle type, placing a strong emphasis on providing sufficient charging capacity for electric heavy-duty vehicles to meet climate goals. These structural advantages position BEVs as the default choice for logistics operators seeking regulatory compliance, operational predictability, and long term cost efficiency.

The Fuel Cell Electric Vehicle (FCEV) segment is predicted to witness the highest CAGR of 34.7% from 2026 to 2034 due to its unique suitability for heavy duty, long range applications where battery weight and charging downtime pose limitations. FCEVs offer refueling times under 15 minutes and ranges exceeding 500 kilometers, aligning with the operational needs of regional freight and refuse collection services. The European Union is heavily funding hydrogen infrastructure and mobility projects through public-private partnerships and the Connecting Europe Facility, focusing on connecting industrial hubs in Western Europe. The International Energy Agency indicates a rapid expansion of hydrogen refueling infrastructure in Europe, with targets to significantly increase the availability of specialized stations for heavy-duty vehicles by the end of the decade. Major manufacturers including Daimler Truck and Volvo have launched FCEV truck prototypes undergoing real world trials with logistics partners like DB Schenker and PostNL. Additionally, the EU’s Net Zero Industry Act designates electrolyzer and fuel cell manufacturing as strategic priorities, accelerating domestic supply chain development. As green hydrogen costs decline, FCEVs are poised to capture niche but critical segments of the commercial transport ecosystem.

By Vehicle Insights

In 2025, vans segment led the Europe electric commercial vehicle market and captured a significant share. The leading position of the segment is attributed to its centrality to last mile delivery networks, which have expanded dramatically due to e commerce growth and urbanization. Driven by e-commerce, courier and parcel service volumes continue to rise significantly across the European Union, with a substantial portion of these last-mile deliveries occurring within dense city centers that are implementing stricter emission regulations. Light commercial vans under 3.5 tons are ideal candidates for electrification due to predictable daily routes averaging 80 to 120 kilometers, well within the range of current battery technology. Major European cities, notably in the Netherlands, are implementing zero-emission zones for logistics vehicles in city centers, significantly driving demand for courier companies to transition their fleets to electric alternatives. Leading logistics firms including UPS, DHL, and La Poste have already deployed tens of thousands of electric vans across Western Europe. Moreover, the vehicle architecture allows for straightforward battery integration without significant payload compromise, unlike heavier trucks. The sheer scale of the EU van market means that minor gains in electrification translate into significant volume, solidifying the segment's dominant market share.

The segment is estimated to register the fastest CAGR of 28.9% during the forecast period owing to the convergence of regulatory pressure, technological maturation, and corporate decarbonization mandates targeting medium and heavy duty transport. The European Union’s revised CO2 standards require a 45 percent reduction in emissions from new heavy duty vehicles by 2030 and 90 percent by 2040, effectively mandating electrification for urban and regional haulage. Certain European countries have seen growth in the adoption of electric trucks. However, the broader regional market for these vehicles has recently experienced a decline due to mixed performance across major member states. Companies like Amazon, IKEA, and Maersk have placed large orders for 18 to 26 ton electric trucks from manufacturers such as Scania, MAN, and Tesla Semi for intra European logistics. European regulations now mandate the consistent placement of high-capacity charging stations for heavy vehicles along major transport corridors to ensure the operational feasibility of long-distance electric freight. Additionally, National financial incentives for electric heavy-duty vehicles have shifted as major European economies reassess their direct purchase support programs for commercial fleets. Battery energy density is improving, and the total cost of ownership is expected to reach parity by 2027. Consequently, this segment is set for exponential adoption.

By Range Insights

The 151 to 250 miles range segment held the majority share of 58.2% of the Europe electric commercial vehicle market in 2025. This range aligns precisely with the operational realities of urban and suburban logistics, where daily routes rarely exceed 200 kilometers. According to research, a significant majority of light commercial vehicle operations in the European Union consist of short-distance trips that can typically be completed within a single day, aligning with the range capabilities of modern electric delivery vehicles. Vehicles in this range category, such as the Ford E Transit Custom and Renault Master E Tech, offer optimal balance between battery size, payload capacity, and acquisition cost. They avoid the excessive weight and expense of larger packs while providing sufficient buffer for cold weather performance degradation, which can reduce effective range. Municipal delivery fleets, postal services, and utility companies prioritize this range due to depot based overnight charging feasibility using standard AC or low power DC infrastructure. National incentive programs in France and the Netherlands further calibrate subsidies to favor vehicles with ranges between 200 and 300 kilometers, reinforcing market concentration in this segment.

The more than 500 miles range segment is anticipated to witness the fastest CAGR of 31.2% between 2026 and 2034. The rapid growth of the segment is fueled by advancements in both battery and hydrogen technologies enabling long haul zero emission freight. While currently a small share, demand is surging among logistics providers operating on intercity corridors such as Rotterdam to Milan or Hamburg to Lyon. These are routes where daily distances exceed 400 kilometers. The European Union's comprehensive climate package establishes legally binding, tiered carbon reduction targets for various vehicle classes, requiring substantial emissions decreases for heavy-duty transport over the next decade to encourage early industry investment. Major international energy organizations and European regulators are coordinating the expansion of a standardized hydrogen refueling network across the continent to support the deployment of long-haul fuel cell trucks capable of covering significant distances on a single tank. Simultaneously, solid state battery prototypes from companies like Northvolt and CATL promise energy densities above 400 Wh/kg, potentially enabling BEV trucks with 600 kilometer ranges by 2027. Pilot deployments by DB Schenker and DHL using Nikola Tre FCEVs and Mercedes eActros LongHaul demonstrate commercial readiness. Green hydrogen costs are declining, and ultra-fast charging infrastructure is scaling. Consequently, this segment will transition from niche to mainstream.

By Component Insights

The electric vehicle batteries segment was the largest segment in the Europe electric commercial vehicle market and occupied a 65.3% share in 2025 because of its role as the primary enabler of vehicle range, performance, and total cost of ownership. Lithium ion chemistries, particularly nickel manganese cobalt and lithium iron phosphate, power nearly all electric vans and trucks, with pack sizes ranging from 40 kWh in small vans to over 600 kWh in heavy duty models. Emerging European regulations now require comprehensive digital tracking for all large-scale batteries to ensure transparency and safety throughout their lifecycle, coinciding with a growing need for advanced management systems as the commercial electric fleet expands. Europe is implementing new industrial laws to build a more resilient domestic supply chain for essential battery minerals, supported by a rapidly increasing number of local manufacturing facilities aimed at reducing reliance on external suppliers by the end of the decade. Battery leasing models, pioneered by companies like Arrival and Volta Trucks, further decouple upfront vehicle cost from battery ownership, enhancing affordability. As the long-term value of electric transport becomes increasingly dependent on how well batteries perform over time, manufacturers are offering significantly longer durability guarantees, making battery health the primary area of technical development and market competition.

The hydrogen fuel cells segment is likely to experience the fastest CAGR of 36.8% over the forecast period. The swift expansion of the segment is propelled by its critical role in enabling zero emission heavy duty transport where battery constraints persist. Fuel cells convert hydrogen into electricity onboard, producing only water vapor as a byproduct, and offer high power density suitable for continuous operation. The European Clean Hydrogen Partnership has funded numerous fuel cell stack development projects since 2021, with companies like Bosch and Symbio scaling production capacity. Although the deployment of fuel cell systems in European public transit and heavy utility fleets is growing rapidly compared to previous years, they currently represent only a small fraction of the total zero-emission commercial vehicle market. New European industrial regulations classify fuel cell manufacturing as a critical sector for achieving climate goals, establishing targets for domestic production capacity to meet a significant portion of the region's total deployment requirements by the end of the decade. Partnerships between Air Liquide, Linde, and truck OEMs are establishing integrated hydrogen ecosystems, while falling green hydrogen prices enhance economic viability. As regulatory deadlines for heavy duty decarbonization approach, fuel cells are transitioning from experimental to essential.

COMPETITIVE LANDSCAPE

Competition in the Europe electric commercial vehicle market is intensifying as legacy OEMs, new entrants, and technology firms vie for dominance across van, truck, and bus segments. Established players like Daimler, Volvo, and Renault leverage decades of commercial vehicle expertise and service networks, while startups such as Arrival and Volta Trucks focus on agile, software defined architectures tailored to urban logistics. The competitive landscape is further shaped by regulatory deadlines, with the EU’s 2035 zero emission mandate forcing rapid product cycles. Differentiation increasingly hinges on total ecosystem offerings—not just the vehicle but also charging infrastructure, energy management, and fleet analytics. Price competition remains moderate due to high development costs, but value is shifting toward operational support and lifecycle services. Cross industry alliances with utilities, logistics firms, and city governments are becoming essential to secure pilot deployments and scale sustainably in a market where technological readiness must align with policy and infrastructure maturity.

KEY MARKET PLAYERS

These are some of the major key players involved in the European electric commercial vehicle market.

- AB Volvo (Sweden)

- VDL Bus and Coach (Netherlands)

- Renault

- Daimler (Germany)

- CAF (Spain)

- EBUSCO (Netherlands)

- Scania (Sweden)

- Continental AG

- Tesla

- Nissan Corporation

- Emoss Mobile Systems

Top Players In The Market

- Volvo Group is a leading force in the Europe electric commercial vehicle market through its comprehensive portfolio of electric buses, trucks, and construction equipment. The company has played a pivotal role globally by pioneering heavy duty electric transport solutions, with its FL and FE electric trucks widely adopted by urban logistics and waste management fleets across Sweden, Germany, and the Netherlands. In recent years, it launched the Volvo ETRUCK program, offering integrated charging infrastructure and fleet advisory services. The company also established a dedicated electric vehicle assembly line in Ghent, Belgium, to localize production and reduce delivery lead times, thereby strengthening its European supply chain resilience and customer responsiveness.

- Daimler Truck AG significantly influences the Europe electric commercial vehicle landscape through its Mercedes Benz eActros and FUSO eCanter platforms, which serve light to heavy duty segments. Globally, the company has committed to offering only CO2 neutral new vehicles by 2039, accelerating its electrification roadmap. In Europe, Daimler has deployed electric trucks in real world customer trials with partners like DB Schenker and Rhenus Logistics. It also co founded the CharIN megawatt charging standard initiative, ensuring interoperability and future proofing its vehicles for high power depot and en route charging across the continent.

- Renault Group holds a strategic position in the Europe electric commercial vehicle market through its Mobilize and Renault Pro+ divisions, offering best selling electric vans such as the Kangoo E Tech and Master E Tech. The company leverages its extensive dealer and service network across France, Spain, and Italy to provide end to end fleet solutions including financing, charging, and maintenance. Globally, Renault has exported its electric van technology to markets in Latin America and North Africa, demonstrating platform versatility. Recently, it partnered with Enel X to deploy smart charging ecosystems for urban delivery fleets and launched a battery leasing program to lower upfront costs for small businesses. These initiatives enhance accessibility and operational flexibility, solidifying Renault’s role as a key enabler of urban freight electrification in Europe.

Top Strategies Used By the Key Market Participants

Key players in the Europe electric commercial vehicle market employ five core strategies to strengthen their positions. First, they vertically integrate battery and powertrain development to control performance and cost. Second, they form strategic partnerships with energy providers and charging infrastructure developers to offer turnkey fleet solutions. Third, they localize manufacturing within Europe to comply with trade regulations and reduce supply chain risks. Fourth, they introduce battery as a service or leasing models to lower customer acquisition barriers. Fifth, they invest in digital fleet management platforms that optimize routing energy consumption and predictive maintenance, thereby enhancing total cost of ownership advantages over conventional vehicles.

MARKET SEGMENTATION

This research report on the Europe electric commercial vehicle market has been segmented and sub-segmented into the following categories.

By Propulsion Type

- Battery Electric Vehicle (BEV)

- Hybrid Electric Vehicle (HEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Fuel Cell Electric Vehicle (FCEV)

By Vehicle Type

- Bus

- Pick-up Trucks

- Van

- Trucks

By Range Insights

- Less than 150 miles

- 151-250 miles

- 251-500 miles

- More than 500 miles

By Component Insights

- Electric Motor

- Hydrogen Fuel Cell

- Electric Vehicle Battery

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

Why are European fleet operators shifting toward electric commercial vehicles?

Lower operating costs and urban emission restrictions make electric fleets financially practical.

What type of commercial vehicles are electrifying fastest in Europe?

Delivery vans are leading adoption due to predictable urban driving routes.

How do low-emission zones influence electric vehicle purchases?

Restricted city access pushes companies to replace diesel vehicles with compliant alternatives.

Why do logistics companies see electric vehicles as a strategic investment?

Fleet electrification improves brand image while reducing long-term fuel volatility risks.

What operational advantage do electric commercial vehicles offer in cities?

Quiet operation enables early-morning and late-night deliveries without noise violations.

How does battery range affect fleet planning decisions?

Route predictability determines whether current battery capacity meets daily mileage needs.

Why are charging infrastructure partnerships important for fleet growth?

Reliable charging access directly impacts vehicle uptime and scheduling efficiency.

How does total cost of ownership compare to diesel vehicles?

Maintenance and fuel savings often offset higher upfront purchase prices over time.

What challenge do transport companies face during electrification?

Balancing vehicle downtime for charging with tight delivery schedules requires careful planning.

Why are governments supporting commercial vehicle electrification?

Reducing transport emissions is essential for meeting climate targets.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com