Global Electric Commercial Vehicle Market Size, Share, Trends & Growth Forecast Report, Segmented By Propulsion (BEV, HEV, PHEV and FCEV), Vehicle Type (Bus, Truck, Van and Pick-up Trucks), Range (0-150 miles, 151-250 miles, 251-500 miles, 500 miles and above), Component (Electric Motor, EV Battery and Hydrogen Fuel Cell) and Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa), Industrial Analysis (2026 to 2034)

Global Electric Commercial Vehicle Market Size

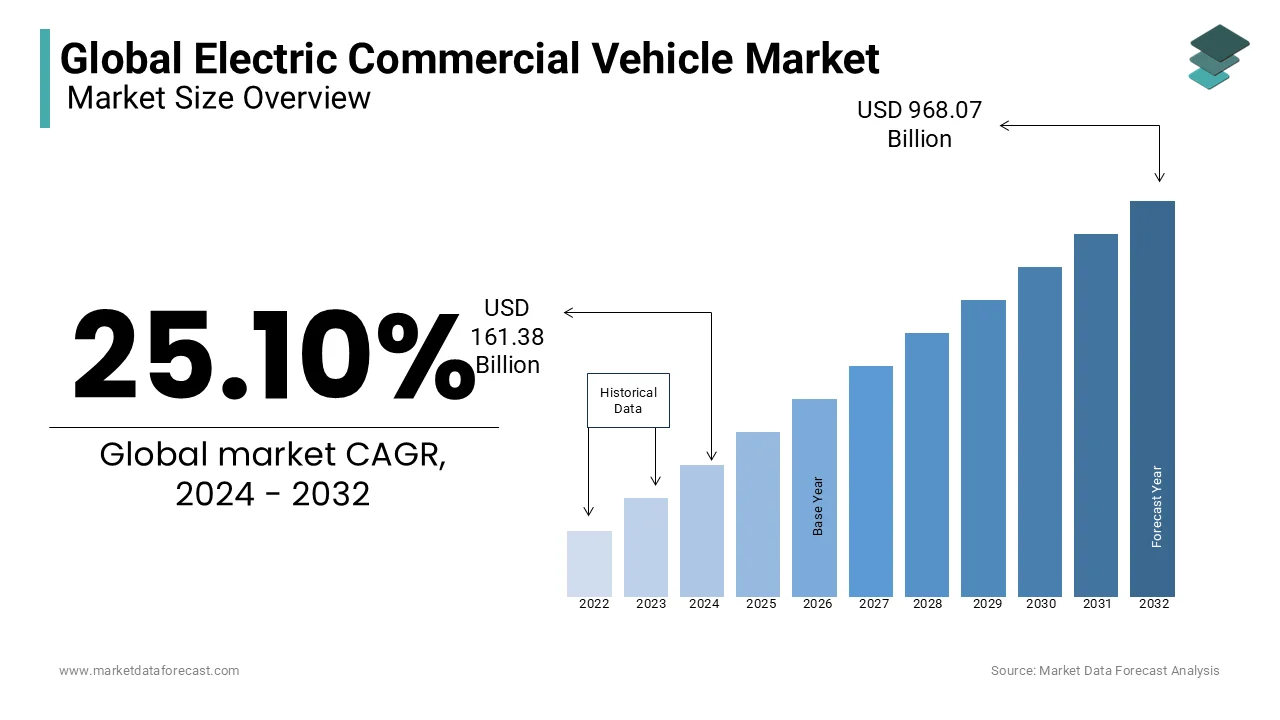

The global electric commercial vehicle market was valued at USD 201.89 billion in 2025 and is anticipated to reach USD 263.82 billion in 2026 to reach USD 1582.60 billion by 2034, growing at a CAGR of 25.10% during the forecast period from 2026 to 2034.

The Electric Commercial Vehicle (ECV) is electrically powered and used for transporting goods or passengers in commercial operations. This includes electric delivery vans, buses, trucks, and light- and heavy-duty utility vehicles designed for logistics, public transport, and freight services. The shift toward electric commercial transportation is being driven by regulatory mandates, advancements in battery technology, and growing awareness of environmental sustainability. According to the International Energy Agency (IEA), the global stock of electric commercial vehicles surpassed 1.2 million units in 2023, with Europe and China leading adoption rates. Moreover, the rise of e-commerce has amplified demand for clean delivery fleets, particularly in last-mile logistics. Companies like DHL, Amazon, and UPS have committed to electrifying portions of their fleets, further accelerating market expansion.

MARKET DRIVERS

Stringent Government Regulations on Emissions

One of the primary forces propelling the growth of the Electric Commercial Vehicle Market is the implementation of stringent government regulations aimed at curbing greenhouse gas emissions from the transportation sector. Across the globe, policymakers are enforcing emission reduction targets and imposing penalties on high-emission fleets to combat air pollution and climate change.

According to the European Environment Agency, road transport accounts for nearly 27% of the EU's total carbon dioxide emissions, with commercial vehicles contributing significantly to this figure. In response, the European Union has mandated that all new commercial vehicles must achieve a 45% reduction in average CO₂ emissions by 2030 compared to 2021 levels. These policies are pushing manufacturers and fleet operators to transition toward electric alternatives. In the United States, the Environmental Protection Agency (EPA) introduced the Clean Trucks Plan in 2023, setting stricter emission standards for medium- and heavy-duty vehicles starting from model year 2027.

Expansion of Charging Infrastructure and Government Incentives

Another significant driver of the Electric Commercial Vehicle Market is the rapid expansion of charging infrastructure, supported by substantial government incentives and private investments aimed at facilitating seamless fleet electrification. The availability of reliable and widespread charging networks is critical for commercial operators who require consistent uptime and efficient route planning. In the United States, the Department of Transportation launched the National Electric Vehicle Infrastructure (NEVI) Formula Program in 2022, allocating $7.5 billion to build a nationwide network of EV charging stations along major highways. Additionally, governments are offering direct subsidies and tax incentives to encourage fleet electrification.

MARKET RESTRAINTS

High Upfront Cost of Electric Commercial Vehicles

A major restraint impeding the widespread adoption of electric commercial vehicles is their high upfront cost compared to conventional internal combustion engine (ICE) vehicles. While total cost of ownership (TCO) benefits exist over time due to lower fuel and maintenance expenses, the initial capital expenditure remains a barrier, especially for small and mid-sized fleet operators. This cost disparity is primarily attributed to the expensive lithium-ion battery packs that constitute a substantial portion of the vehicle’s total value. Moreover, limited financing options and uncertainty regarding residual values further discourage fleet managers from making the switch.

Limited Range and Battery Degradation Concerns

Range limitations and concerns about battery degradation are among the most pressing constraints affecting the adoption of electric commercial vehicles, particularly in long-haul and high-utilization applications. Unlike passenger cars, commercial vehicles often operate under demanding conditions involving continuous use, heavy payloads, and extensive daily distances, which can significantly impact battery performance. According to the U.S. Department of Energy, the average range of a Class 6 electric delivery truck is approximately 150–200 miles per charge, which may be insufficient for certain logistics routes without access to fast-charging infrastructure. Long-haul electric trucks, such as those used for intercity freight transport, face even greater challenges, with real-world ranges often falling short of manufacturer claims under full load and adverse weather conditions.

Battery degradation also poses a concern for fleet operators seeking predictable operational lifespans. A study conducted by Argonne National Laboratory in 2023 found that commercial-grade lithium-ion batteries can lose up to 15% of their original capacity after five years of intensive use, depending on charging frequency and ambient temperatures. Until improvements in battery chemistry, energy density, and thermal management systems provide greater reliability and longevity, range anxiety will continue to hinder broader market penetration.

MARKET OPPORTUNITIES

Growth of Urban Logistics and Last-Mile Delivery Demand

A significant opportunity fueling the Electric Commercial Vehicle Market is the exponential growth of urban logistics and last-mile delivery demand in densely populated metropolitan areas. With the rapid expansion of e-commerce and same-day delivery expectations, companies are increasingly turning to electric commercial vehicles to meet logistical needs efficiently and sustainably. Cities worldwide are also implementing low-emission zones and restricting access for high-polluting vehicles, encouraging logistics firms to adopt electric alternatives. For instance, London’s Ultra Low Emission Zone (ULEZ) expansion in 2023 effectively barred older diesel vans from central areas unless retrofitted or replaced. Furthermore, urban delivery routes typically involve frequent stops and moderate speeds, making them ideal for electric vehicles that benefit from regenerative braking and lower energy consumption under such conditions.

Electrification of Public Transit Fleets

Another promising opportunity for the Electric Commercial Vehicle Market lies in the electrification of public transit fleets, including city buses and municipal service vehicles. Governments and urban transit authorities are prioritizing the replacement of aging diesel fleets with electric alternatives to improve air quality and comply with environmental regulations. According to the International Energy Agency (IEA), over 600,000 electric buses were in operation globally in 2023, with China accounting for the majority. However, Europe is rapidly catching up, with countries like Sweden, Norway, and the Netherlands leading the transition. The European Commission’s Green Deal aims to achieve climate neutrality by 2050, with a target of zero-emission public transport in all urban areas by 2035. To support this, member states have allocated billions in subsidies for electric bus procurement. Additionally, advancements in fast-charging infrastructure and depot electrification have made it more feasible for municipalities to transition entire fleets. Cities like Paris and Madrid have already begun replacing their diesel-powered public transport with electric models to reduce noise pollution and emissions.

MARKET CHALLENGES

Supply Chain Constraints and Raw Material Shortages

A critical challenge confronting the Electric Commercial Vehicle Market is the persistent supply chain disruptions and shortages of essential raw materials required for battery production. The manufacturing of lithium-ion batteries, which power the majority of electric commercial vehicles, relies heavily on scarce resources such as lithium, cobalt, nickel, and graphite. According to a 2023 report by the U.S. Geological Survey (USGS), global lithium reserves are concentrated in a few regions, with Chile, Australia, and Argentina accounting for over 75% of total production. Cobalt, another vital battery component, faces ethical sourcing concerns and supply bottlenecks. The Democratic Republic of Congo supplies over 70% of the world’s cobalt, but mining practices there have raised environmental and human rights issues. Nickel and graphite also experience fluctuating availability due to mining limitations and refining capacity constraints. These supply-side pressures directly affect battery production timelines and pricing stability, ultimately influencing the affordability and scalability of electric commercial vehicles.

Grid Capacity Limitations and Energy Management Challenges

Another significant challenge facing the Electric Commercial Vehicle Market is the strain placed on electrical grids due to the rising demand for charging infrastructure. According to the European Network of Transmission System Operators for Electricity (ENTSO-E), the projected electricity demand from electric vehicles in Europe could reach 1,200 TWh annually by 2040. This surge necessitates upgrades to grid infrastructure, smart energy distribution systems, and localized energy storage solutions to prevent overloads and ensure a stable power supply. Charging depots for commercial fleets, especially those operating multiple electric trucks or buses, require high-capacity connections that many existing grid networks cannot accommodate. In Germany, several logistics companies reported delays in installing fast-charging stations due to insufficient local grid capacity, as detailed in a 2023 report by the German Energy Agency (DENA). Additionally, energy management complexities arise when coordinating simultaneous charging cycles across large fleets. Without intelligent load-balancing systems, utilities risk experiencing voltage fluctuations and inefficiencies that compromise both vehicle performance and grid stability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 25.10% |

| Segments Covered | By Propulsion, Electric Vehicle, Range, Component, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | AB Volvo, Alexander Dennis Ltd., Alstom–NTL, Anhui Ankai Automobile Co. Ltd., Ashok Leyland Ltd., Bluebus SAS, Bozankaya A.S., BYD Co. Ltd., Caetanobus - Fabrico De Autocarros E Carrocarias S.A., Chariot Motors, Dongfeng Motor Corp., Ebusco B.V., Nanjing Golden Dragon Bus Co. Ltd., Proterra Inc., and Tata Motors Ltd. The major electric truck manufacturers are Cummins Inc., E-Force One AG, Hino Motors Ltd., Isuzu Motors Ltd., Iveco S.p.A., Nikola Corp., Nissan Motor Co. Ltd., Scania AB, Workhorse Group Inc., and Others. |

SEGMENTAL ANALYSIS

By Propulsion Insights

The Battery Electric Vehicles (BEVs) segment was the largest by capturing a prominent share of the Electric Commercial Vehicle Market in 2024. According to BloombergNEF, over 80% of new electric commercial vehicle registrations globally in 2023 were BEVs, driven largely by urban delivery applications that benefit from short-range operations and frequent charging opportunities. In Europe, cities like Oslo and Amsterdam have implemented strict low-emission zone policies, effectively phasing out internal combustion engine vehicles and promoting BEV adoption. Additionally, major logistics companies such as DHL, UPS, and Amazon are investing heavily in BEV fleets for last-mile delivery operations. Amazon alone plans to deploy 100,000 Rivian electric vans by 2025, further reinforcing BEV dominance in the commercial vehicle space.

The Fuel Cell Electric Vehicles (FCEVs) segment is likely to grow with a projected CAGR of 37.2% in the coming years. This rapid growth is fueled by the unique advantages of hydrogen fuel cells, particularly in long-haul and heavy-duty transportation, where battery limitations become more pronounced. As per data from the International Energy Agency (IEA), global FCEV commercial vehicle deployments increased by over 60% in 2023, with significant traction observed in Japan, South Korea, and Germany. Furthermore, FCEVs are gaining interest in industries requiring high uptime and extended range, such as intercity freight and refuse collection. Companies like Hyundai and Toyota have introduced hydrogen-powered trucks tailored for these applications by offering ranges exceeding 400 miles on a single tank.

By Vehicle Insights

The electric vans segment held 42.1% of the Electric Commercial Vehicle Market share in 2024. This dominance stems from the growing demand for efficient, clean-energy solutions in urban logistics and last-mile delivery services. According to the European Environment Agency (EEA), nearly 70% of goods transported within EU cities are moved via vans, making them a critical focus area for emissions reduction strategies. Major logistics players, including FedEx, DHL, and Amazon, are rapidly electrifying their fleets to meet sustainability targets and reduce operating costs. Amazon, for example, has already deployed thousands of electric delivery vans manufactured by Rivian, with plans to scale up to 100,000 units by 2025. In addition, government incentives are accelerating van electrification. In France, businesses purchasing electric delivery vans can receive subsidies of up to €20,000 through the Ecotax exemption program, significantly lowering acquisition costs.

The pick-up trucks segment is swiftly growing with an expected CAGR of 29.8% from 2025 to 2033. According to the U.S. Department of Energy, over 600,000 pick-up trucks were registered for commercial use in the United States in 2023, with a growing portion transitioning to electric models. Automakers such as Tesla, Ford, and Rivian have launched high-performance electric pick-ups like the Cybertruck, F-150 Lightning, and Enduro, respectively, targeting both individual buyers and small businesses. These vehicles offer strong payload capacities, advanced towing capabilities, and onboard power features ideal for construction, agriculture, and field service applications. European automakers are also entering this space, with Volkswagen unveiling its electric Amarok pick-up in late 2023, signaling broader acceptance across global markets.

By Range Insights

The 151–250 miles range segment held the dominant share of the Electric Commercial Vehicle Market in 2024. According to McKinsey & Company’s 2023 report on commercial vehicle electrification, over 65% of medium-duty delivery routes in Europe and North America fall within the 100–200 mile range, which is making this segment highly suitable for current battery technologies without necessitating excessive weight or cost. Logistics operators prefer vehicles in this range due to their balance of efficiency, payload capacity, and practicality for overnight depot-based charging. Companies such as DHL and DB Schenker have reported higher utilization rates and lower downtime with vehicles in this category, enhancing overall fleet productivity.

The 251–500 miles range segment is lucratively growing by registering a CAGR of 33.4% in the coming years. This segment is particularly attractive to logistics companies engaged in inter-city freight movement, where daily driving distances often exceed the limits of shorter-range BEVs. Fleets operating between distribution hubs and regional centers are increasingly adopting these vehicles to reduce carbon footprints while maintaining operational efficiency. Furthermore, improvements in lithium-ion battery chemistry and thermal management systems have enabled manufacturers to produce heavier electric trucks with extended range capabilities.

By Component Insights

The EV battery component segment led the Electric Commercial Vehicle Market by capturing 54.3% of the share in 2024. Advances in lithium-ion technology, including nickel-manganese-cobalt (NMC) and lithium iron phosphate (LFP) chemistries, have significantly improved energy density and durability, which is making them indispensable for commercial applications. China remains the largest producer and consumer of EV batteries, with companies like CATL and BYD supplying components to global automakers. Europe and North America are also ramping up domestic battery manufacturing to reduce dependency on Asian suppliers.

The hydrogen fuel cell segment is witnessing a CAGR of 41.6% in the coming years. According to the International Energy Agency (IEA), global hydrogen fuel cell shipments for commercial vehicles grew by 68% in 2023, with notable expansion in Germany, Japan, and South Korea. These regions are investing heavily in hydrogen infrastructure to support large-scale deployment of FCEVs in freight, bus, and industrial transport segments. In addition, automotive manufacturers such as Hyundai and Toyota are scaling up production of hydrogen fuel cell modules tailored for commercial use.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific was the largest contributor with 46.3% of the global Electric Commercial Vehicle Market share in 2024. According to the China Association of Automobile Manufacturers (CAAM), over 1.1 million electric commercial vehicles were sold in China in 2023, supported by aggressive government policies mandating fleet electrification and offering direct purchase subsidies. Cities like Shenzhen and Shanghai have fully electrified their public bus fleets, setting benchmarks for other urban centers. Japan and South Korea are also making strides in electric truck and van adoption, particularly in logistics and municipal services. Toyota and Hyundai have been pioneers in introducing hydrogen fuel cell commercial vehicles, broadening the region’s technological portfolio. Additionally, India is emerging as a key growth market, with initiatives like the Faster Adoption and Manufacturing of Electric Vehicles (FAME II) scheme boosting EV adoption in commercial transport. As per NITI Aayog, India’s EV penetration in commercial fleets is expected to reach 15% by 2030.

Europe Market Analysis

Europe electric commercial vehicle market was positioned second by holding 23.1% of the share in 2024. The European Green Deal, launched in 2019, aims to make the continent climate-neutral by 2050, with a key focus on electrifying freight and public transport. Automotive giants such as Mercedes-Benz, Volvo Trucks, and Renault are actively rolling out electric commercial models, supported by partnerships with logistics firms eager to decarbonize their fleets. Additionally, municipalities are replacing aging diesel buses with electric alternatives, further strengthening the market.

North America Market Analysis

North America Electric Commercial Vehicle Market is gaining huge traction with the United States' aggressive push toward fleet electrification in logistics, public transit, and municipal services. The Biden administration has played a crucial role in shaping the market through policies like the Inflation Reduction Act (IRA), which provides tax credits of up to $7,500 for commercial EV purchases. Additionally, the National Electric Vehicle Infrastructure (NEVI) Program is investing $7.5 billion to build a nationwide fast-charging network, facilitating long-haul electric trucking. Canada is also contributing to regional growth, with provinces like Quebec and British Columbia offering financial incentives for fleet electrification. Public transit agencies in Toronto and Vancouver are piloting electric bus programs to replace older diesel models.

Latin America Market Analysis

Latin American electric Commercial Vehicle Market is expected to have a steady growth rate in the coming years. According to the Brazilian Association of Electric Mobility (ABVE), over 12,000 electric commercial vehicles were registered in Brazil in 2023, primarily in urban delivery and municipal services. São Paulo and Rio de Janeiro have initiated pilot programs for electric garbage trucks and school buses, supported by federal incentives aimed at reducing urban air pollution.

Middle East and Africa

The Middle East and Africa Electric Commercial Vehicle Market is growing steadily, with the UAE, Saudi Arabia, and South Africa leading adoption efforts. According to the Dubai Electricity and Water Authority (DEWA), the UAE has deployed over 3,000 electric commercial vehicles as part of its Smart Dubai initiative, focusing on logistics, waste management, and municipal services. Saudi Arabia, under its Vision 2030 strategy, is investing in smart city projects such as NEOM, where electric commercial vehicles will form a core part of the transportation ecosystem. The country is also exploring hydrogen-powered commercial transport options in collaboration with international partners.

COMPETITIVE LANDSCAPE

The competition in the Electric Commercial Vehicle Market is intensifying as traditional automotive giants, emerging EV startups, and technology-driven mobility firms vie for dominance in a rapidly evolving sector. Established manufacturers such as Daimler, Volvo, and BYD are leveraging their extensive supply chains and engineering expertise to scale up production and improve vehicle performance. At the same time, new entrants from the tech and logistics sectors are disrupting conventional business models by introducing software-integrated fleet solutions and subscription-based ownership plans. This dynamic environment fosters innovation, pushing companies to differentiate through advanced battery systems, extended ranges, and enhanced connectivity features. Competitive pressure is further heightened by the need to meet stringent emissions regulations and align with corporate sustainability goals.

KEY MARKET PLAYERS

Some of the major players engaged in the electric commercial vehicles market across the globe include

- AB Volvo

- Alexander Dennis Ltd.

- Alstom–NTL

- Tesla, Inc.

- Anhui Ankai Automobile Co. Ltd.

- Ashok Leyland Ltd.

- Daimler Truck AG (Mercedes-Benz)

- Bluebus SAS

- Bozankaya A.S.

- BYD Co. Ltd.

- Caetanobus - Fabrico De Autocarros E Carrocarias S.A.,

- Chariot Motors

- Dongfeng Motor Corp.

- Ebusco B.V.

- Nanjing Golden Dragon Bus Co. Ltd.

- Proterra Inc.

- Tata Motors Ltd

- Cummins Inc.

- E-Force One AG

- Hino Motors Ltd

- Isuzu Motors Ltd

- Iveco S.p.A.

- Nikola Corp.

- Nissan Motor Co. Ltd.

- Scania AB

- Workhorse Group Inc.

Top Players In The Market

- Tesla has played a transformative role in advancing electric commercial vehicles through its innovative approach and strong brand influence. The company’s entry into the heavy-duty trucking segment with the Tesla Semi has challenged traditional automakers to accelerate their electrification efforts. By leveraging its expertise in battery technology and autonomous driving features, Tesla is reshaping expectations for performance, efficiency, and sustainability in commercial transportation. Its influence extends beyond product development, as it also drives industry-wide shifts toward cleaner logistics solutions.

- Daimler Truck, a global leader in commercial vehicle manufacturing, has made significant strides in electrifying its fleet through brands like Mercedes-Benz Trucks. The company has introduced a range of electric trucks tailored for urban distribution and regional transport, emphasizing scalability and operational efficiency. With a strong presence in Europe and expanding reach in North America and Asia, Daimler is actively partnering with energy providers and logistics firms to support charging infrastructure development and accelerate adoption across key markets.

- BYD is a dominant force in the global electric commercial vehicle space, particularly in China, and is expanding rapidly into international markets. Known for its vertically integrated production model, BYD offers a comprehensive portfolio including electric buses, trucks, and delivery vans. The company has been instrumental in deploying large-scale electric public transit fleets worldwide, contributing significantly to urban air quality improvements. BYD's strategic partnerships and investments in overseas manufacturing facilities have prompted its position as a leading exporter of electric commercial vehicles.

Top Strategies Used by Key Market Participants

One of the primary strategies employed by leading players in the Electric Commercial Vehicle Market is product diversification and platform expansion. Companies are developing a broad range of electric models across different vehicle types such as vans, trucks, and buses to cater to diverse customer needs and maximize market coverage.

Another critical approach is strategic collaboration with charging infrastructure providers. Recognizing that widespread EV adoption hinges on accessible and reliable charging networks, major automakers are forming alliances with energy companies and tech firms to co-develop fast-charging stations along key freight corridors and within urban centers.

Firms are increasingly focusing on deepening relationships with fleet operators through customized financing and service packages. Manufacturers are making it easier for businesses to transition to electric vehicles while ensuring long-term customer loyalty by offering tailored leasing options, maintenance contracts, and digital fleet management tools.

MARKET SEGMENTATION

This research report on the global electric commercial vehicle market has been segmented and sub-segmented based on the propulsion, electric vehicle, range, component, and region.

By Propulsion Type

- BEV

- HEV

- PHEV

- FCEV

By Vehicle Type

- Bus

- Truck

- Van

- Pick-up Trucks

By Range

- 0-150 Miles

- 151-250 Miles

- 251-500 Miles

- 500 Miles & Above

By Component

- Electric Motor

- EV Battery

- Hydrogen Fuel Cell

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is currently driving growth in the global electric commercial vehicle market?

Rising demand for low-emission transport and government incentives is driving growth.

Why are electric commercial vehicles gaining popularity worldwide?

They reduce fuel costs and lower environmental impact.

How would you explain electric commercial vehicles in simple terms?

They are trucks, buses, or vans powered by electricity instead of fuel.

Where are electric commercial vehicles most commonly used globally?

They are widely used in logistics, public transport, and delivery services.

What makes electric commercial vehicles important for sustainable transport?

They reduce greenhouse gas emissions and improve energy efficiency.

From a business perspective, are electric commercial vehicles a worthwhile investment?

Yes, they lower operating costs over time and support sustainability goals.

What challenges are affecting the global electric commercial vehicle market?

High upfront costs and limited charging infrastructure are key challenges.

How is government policy influencing this market?

Incentives and regulations are encouraging adoption of electric vehicles.

Which segments contribute the most to electric commercial vehicle demand?

Electric buses and delivery vans are major contributors.

Is the global electric commercial vehicle market growing steadily?

Yes, it is expanding with increasing focus on clean transportation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com