- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

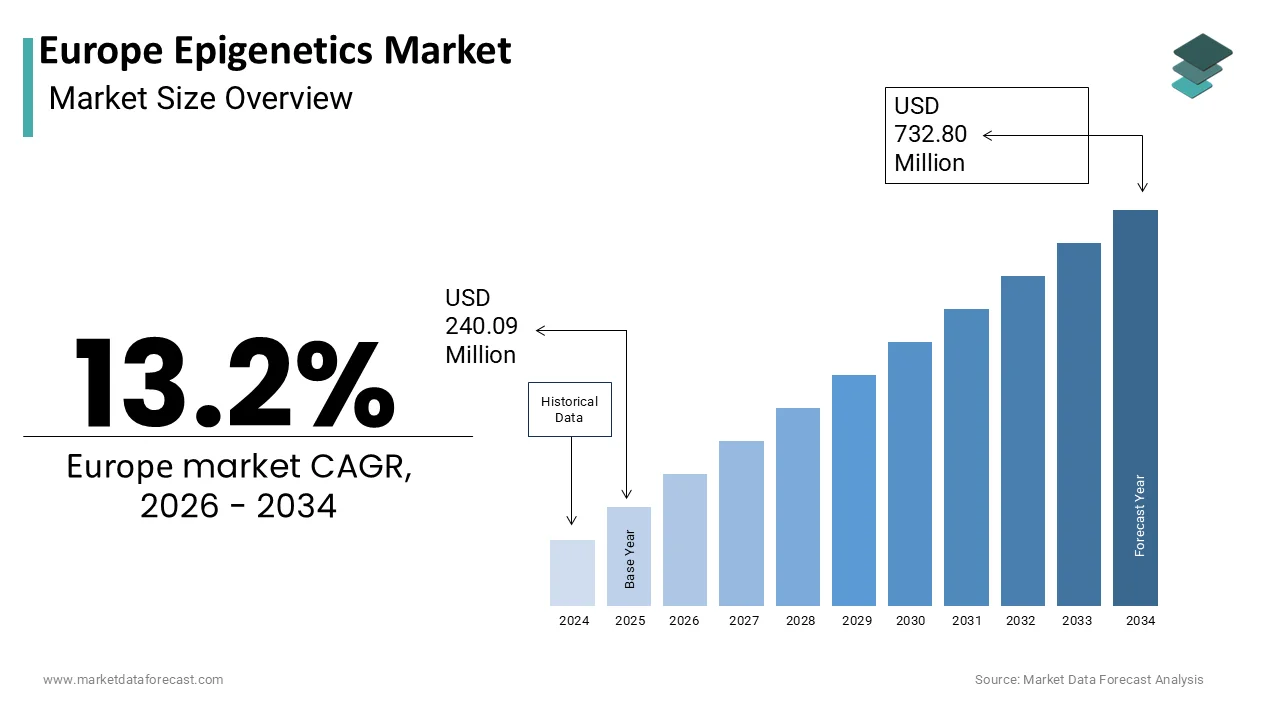

Market Size, 2025

$240.09 MnMarket Estimate, 2026

$271.78 MnMarket Forecast, 2034

$732.80 MnCAGR, 2026–2034

13.2%Europe Epigenetics Market Summary

Market Size & Growth

- The Europe Epigenetics Market was valued at USD 240.09 million in 2025.

- Expected to reach USD 732.80 million by 2034, growing at a CAGR of 13.2% from 2026 to 2034.

- Germany held the largest country share at 19.4% in 2025; the kits segment is the fastest-growing product segment at a CAGR of 14.3%.

Key Market Segments

- By Product: Reagents (leading, 42.6% share in 2025), Kits (fastest growing), Enzymes, Instruments and Consumables.

- By Research Area: Oncology (58.1% share in 2025), Drug Delivery (fastest growing, CAGR of 16.8%), Developmental Biology.

- By Enzymes: DNA-Modifying Enzymes (63.5% share in 2025), RNA-Modifying Enzymes (fastest growing, CAGR of 18.1%), Protein-Modifying Enzymes.

- By Country: Germany leads (19.4%); United Kingdom second (16.8%); followed by France, Switzerland, and Sweden.

Key Drivers

- Rising incidence of chronic diseases — including cancer and cardiovascular conditions — is accelerating demand for epigenetic diagnostics and liquid biopsy tools across Europe.

- Expansion of precision medicine frameworks, with national programs in France and Sweden integrating methylation profiling into standard genomic diagnostics.

- Over EUR 8 billion allocated to health research under the Horizon Europe program (2021–2027), directly funding epigenetic research and biomarker validation.

Key Players

Thermo Fisher Scientific, Inc., QIAGEN N.V., Abcam plc., Illumina, Inc., Merck and Co., New England Biolabs, Inc., Sigma-Aldrich Corporation, Active Motif, Diagenode, Inc., and Zymo Research Corporation.

Europe Epigenetics Market Size

The Europe Epigenetics Market is projected to grow from USD 240.09 million in 2025 to USD 271.78 million in 2026 and reach USD 732.80 million by 2034, registering a CAGR of 13.2% during the forecast period from 2026 to 2034.

Epigenetics refers to the techniques, instruments, ts and reagents designed to study heritable changes in gene expression that occur without alterations to the underlying DNA sequence. These mechanisms include DNA methylation, ion histone modification,tion and non-coding RNA regulation, all of which play pivotal roles in developmental biology, disease progression, and therapeutic response. In recent years , the European scientific community has intensified its focus on epigenetic research as a gateway to understanding complex diseases such as cancer, neurodegenerative disorders,, and autoimmune conditions. European research institutions are increasingly incorporating advanced molecular profiling, including epigenetic analysis, into their genomics research to gain a deeper understanding of disease mechanisms and gene expression regulation. The European Commission has allocated substantial funding, specifically over eight billion euros, to health-related research under the dedicated "Health" cluster of the Horizon Europe program (2021-2027) to address major public health challenges and promote well-being. Furthermore, national health initiatives are increasingly integrating advanced molecular profiling, including comprehensive genomic sequencing and other emerging fields like epigenomics, into research programs to inform and improve the development of diagnostics and personalized therapies. These developments underscore a growing institutional and scientific commitment to epigenetics as a foundational discipline rather than a niche field, thereby establishing Europe as a critical hub for epigenetic innovation and application.

MARKET DRIVERS

Rising Incidence of Chronic Diseases Fuels Demand for Epigenetic Diagnostics

The escalating burden of chronic diseases across the region is significantly accelerating research and clinical interest in epigenetic diagnostics, which in turn drives the growth of the European epigenetics market. Cardiovascular diseases are a significant health concern across the European Union. Cancer also represents a major health challenge in Europe, with millions of new cases recorded. Current research suggests that epigenetic alterations may be important for understanding the early development of malignancy. Epigenetic biomarkers offer non-invasive detection methods, particularly in liquid biopsies, enabling earlier diagnosis and monitoring of treatment efficacy. For instance, hypermethylation of the SEPT9 gene is now used in blood-based colorectal cancer screening tests approved in several European countries. Public health agencies, including the European Centre for Disease Prevention and Control, have begun evaluating epigenetic signatures as part of long term surveillance strategies for chronic disease risk stratification. This convergence of clinical need,scientificc validation, ion, and regulatory acceptance is transforming epigenetic diagnostics from experimental tools into integrated components of Europe’s healthcare infrastructure, structure,tructure thereby driving sustained market activity.

Expansion of Precision Medicine Frameworks Across European Healthcare Systems

The region’s strategic pivot toward precision medicine is creating a robust demand environment for epigenetic technologies, which further contributes to the expansion ofEuropeanurope epigenetics market. European health initiatives are incorporating molecular profiling, which includes epigenetic markers, into standard cancer care practices. Many European countries are adopting national strategies for precision medicine, with epigenetic information becoming a central element in guiding therapy selection. The French national program has facilitated extensive genomic sequencing efforts, integrating methylation profiling to inform the treatment of rare diseases and blood cancers. Sweden's national approach to genomic medicine involves including data layers related to epigenetics within its data systems to enhance predictions regarding responses to medication. The European Medicines Agency has also issued scientific guidelines encouraging the submission of epigenetic evidence in regulatory dossiers for targeted therapies. Academic medical centers in the Netherlands and Switzerland are piloting epigenetic companion diagnostics for immune checkpoint inhibitors, specifically where the s where methylation status of certain genes correlates with clinical outcomes. This institutional embedding of epigenetics within precision medicine pathways not only validates its scientific utility but also ensures long term funding procurement and clinical adoption across diverse therapeutic areas, reinforcing its position as a cornernext-generationeneration healthcare in Europe.

MARKET RESTRAINTS

High Complexity and Cost of Epigenetic Analysis Technologies Limit Accessibility

The deployment of epigenetic technologies across the region remains constrained by their technical complexity and substantial costs, which hamper the growth of the European epigenetics market. Such expenses render large-scale clinical application economically unfeasible, particularly in publicly funded healthcare systems facing budgetary pressures. Moreover, the interpretation of epigenetic data demands specialized bioinformatics expertis,e, which is unevenly distributed across European regions. Sample preparation protocols also introduce variability. These technical hurdles delay integration into routine diagnostics and reduce reproducibility across studies. Furthermore, the absence of standardized reference materials for epigenetic assays complicates cross-institutional validation. Efforts to address these challenges, including the European Reference Genome Atlas project, are currently in initial implementation stages. Consequently, the high barrier to entry restricts epigenetic applications primarily to well-resourced research hospitals and academic centers, thereby slowing broader clinical translation and market penetration across Europe.

Stringent Regulatory and Ethical Frameworks Governing Genomic Data Use

The region’s comprehensive regulatory landscape, while protective of patient rights,,ient rights poses significant operational challenges for epigenetic research and commercialization, which ultimately hinders the expaEuropeanEuropeane Europe epigenetics market. The General Data Protection Regulation includes specific provisions for the handling of genetic and epigenetic data. These types of data are considered special categories that require strict consent procedures. Cross-border research collaborations involving data of this nature have experienced delays. These delays are often associated with differing national interpretations of the regulation's requirements. Countries such as Germany and France impose additional restrictions requiring ethics committee approval for each data access request, even within national biobanks. The European Group on Ethics in Science and New Technologies has further cautioned against the potential misuse of epigenetic information in insurance and employment contexts, leading to cautious policy stances. As per a study, only a y few EU member states have clear legal provisions permitting the reuse of epigenetic data for secondary research purposes. These fragmented and often restrictive frameworks complicate large-scale data aggregation necessary for robust biomarker discovery. Moreover, the lack of harmonized guidelines on data anonymization for epigenetic datasets increases legal uncertainty for private sector developers. Consequently, companies face prolonged timelines for product validation and market entry, while academic researchers encounter barriers to international cocollaborationlaboration thereby collectively dampening innovation velocity and commercial scalability in the European epigenetics market.

MARKET OPPORTUNITIES

Growing Integration of Epigenetics into Agricultural and Environmental Research

The continent is witnessing a notable expansion of epigenetic applications in agriculture and environmental science, which offers a significant opportunity for the European epigenetic markClimate-induceduced stressors such as drought and soil salinity are prompting European agritech firms to explore epigenetic mechanisms that regulate crop resilience. Epigenetic modifications in plants, such as DNA methylation changes in response to water scarcity, have been shown to enhance yield stability without altering genetic sequences. Institutions like Wageningen University in the Netherlands are developing epigenetic markers to predict crop performance under variable climate conditions. Similarly, environmental epigenetics is gaining traction in ececotoxicology where methylation patterns in sentinel species like zebrafish serve as early warning indicators of water pollution. This diversification in non-clinical domains not only broadens the epigenetics market base but also across-sectoral investment and publicfunding, thereby creating new revenue streams and technological synergies across Europe’s innovation ecosystem.

Public-Private Partnerships Catalyzing Epigenetic Innovation Ecosystems

A surge in structured collaborations between public institutions and private enterprises is opening new growth possibilitiesEuropeane Europe epigenetics market. The Innovative Health Initiative,itiative a joint undertaking between the European Union and industryconsortia have committed funds to projects that inmulti-omicsti om,ics data, including epigenetics for disease stratification and drug development. According to the European Federation of Pharmaceutical Industries and Associations,sociations mthirty-five public-privatec private partnerships active between 2021 and 2025 specifically listed epigenetic biomarker discovery as a core objective. Notable examples include the EpiPredict consortium,nsortium which unites academic h,,ospitals biote, biotechh firms, and diagnostic developers across multiple countries to validate methylation signatures in breast cancer therapy resistance. Inn parallel national innovation agencies have launched funding lines that sco-developmentdevelopment of epigenetic platforms for early disease detection. These partnde-risk early-stagely stage innovation by sharing infrastructure, reducing costs data, resources, es and regulatory navigation burdens. Such models acceleratechnology, and transfer to me to market, and foster regional innovation, particularly in hubs. Europe's epigenetics landscape is being transformed from disjointed academic efforts into a unified, investment-ready pipeline through collaborations that merge scientific discovery with commercial viability.

MARKET CHALLENGES

Interpretational Ambiguity of Epigenetic Biomarkers in Clinical Contexts

The contextual ambiguity of biomarker interpretation challenges the growth of the European epigenetics market. Unlike genetic mutations,,ons which often have clear pathogenic implications, cations epigenetic modifications are dynamic r,e versible atissue-specifice specific. A limited number of proposed biomarkers in this field have consistently demonstrated predictive value during independent evaluations. The consistent performance of many potential DNA methylation biomarkers has not been established across different patient cohorts. This variability stems from biological factors such as ge circadia,,n rhythms and environmental exposures,l exposures all of which modulate the epigenome. Furthermore, the lack of large-scale reference epigenomes across diverse European populations exacerbates misinterpretation risks. Without standardized baseline maps, distinguishing pathological from physiological epigenetic variation remains fraught with uncertainty. This interpretational gap undermines clinician confidence, hinders regulatory approval, and complicates reimbursement decisions by national health technology assessment bodies. Consequently, despite promising analytical performance,e many epigenetic assays stall in the translation phase,se unable to demonstrate consistent clinical utility across heterogeneous patient populations.

Insufficient Reimbursement Pathways for Epigenetic Diagnostics

The absence of established reimbursement codes and coverage policies for epigenetic tests poses an impedimEuropean the European epigenetics market. Unlike conventional genetic tests, which are increasingly covered under nationalhealth schemesl,th schemes epigenetic diagnostics often fall into regulatory grey zones due to their novel nature and evolving clinical evidence. Fewer than five European countries have established specific reimbursement categories for methylation-based assays. In Germany, for example, even following the approval of a specific test for colorectal cancer screening by the relevant committee, the actual reimbursement rate remains low due to strict authorization requirements. Similarly, in the United Kingdom, the National Institute for Health and Care Excellence has not yet issued technology appraisal guidance for any epigenetic diagnostic or tic diagnostic, limiting National Health Service procurement. This coverage gap forces laboratories to operaself-payself pay or resear,, ch basi,s drastically curtailing patient access and market volume. Moreover, the fragmented nature of Europe’s healthcare systems means that even when a test gains approval in one country it may face years of additional health technology assessments elsewhere. Epigenetic innovations struggle to achieve widespread adoption and investment because there are no common pathways or defined evidence standards for coverage.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Research Area, Enzymes, Instruments & Consumables, KITS, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Abcam plc., Illumina, Inc., QIAGEN N.V., Merck & Co., New England Biolabs, Inc., Sigma-Aldrich Corporation, Thermo Fisher Scientific, Inc., Active Motif, Diagenode, Inc., and Zymo Research Corporation. |

SEGMENTAL ANALYSIS

By Product Insights

The reagents segment held the leading share of 42.6% of theEuropeane epigenetics market in 2025. The dominance of the reagents segment is driven by its indispensable role across nearly all epigenetic workflows,,ows including chromatin immunoprecipitation,pitation bisulfite conversion,onvemethylation-specificn specific PCR. Unlike capital-intensive instruments, NTSS reagents are consumed r,epeatedly enabl, enabling steady recurring revenue streams for supplierhigh-throughputoughput nature of modern epigenetic research, particularge-scalerge scale initiatives such as the European Prospective Investigation into Cancer andNutritionN,utrition further amplifies demand. Moreover, the trend toward multiplexed assays, which require specialized antibody-based and enzymatic rreagentsnts has intensified procurement volumes. Public research funding has also reinforced this segment as national science agencies prioritize consumable budgets over equipment in grant allocations. The ver,,satility standar,,dization and rapid innovation cycle of reagents ensure their continued centrality in both academic and industrial epigenetic research across Europe.

The kits segment is likely to experience the fastest CAGR of 14.3% between 2025 and 2033. The rapid acceleration of the kits segment is primarily fuelled by the demand for st,andardized rep,,roductime-efficientefficient,wo time-efficient workflows especially among clinical and diagnostic laboratories transitiresearch-gradeearch grade to regulated environments. Commercially available kits for DNA methylation analysis, designed to detect specific gene promoters, have received necessary certification for use in oncology diagnostics across various European countries. The adoption of commercial epigenetic kits by molecular pathology labs in Western Europe is a trend aimed at increasing standardization and fulfilling specific accreditation requirements. Besides, the rise of decentralized research networks under Horizon Europe necessitates protocoharmonization,nization which kits facilitate by pre-optimized reagent combinations and validated protocols. The integration of digital protocQR-coded reagent tracnext-generation kits further enhances compliance with EU in vitro diagnostic regulations, thereby reinforcing adoption across regulated healthcare settings and accelerating market penetration beyond traditional research domains.

By Research Area Insights

The oncology segment was the largest in the European epigenetics market by capturing a 58.1% share in 2025. The prominence of the oncology segment is attributed to the pivotal role of epigenetic mechanisms in cancer initiation, progression, and therapeutic resistance. Aberrant DNA methylation patterns hi, histone modifications, nd dysregulated non-coding RNAs are now recognized as hallmarks of malignancies ranging from glioblastoma to hematologic cancers. Epigenetic profiling has been recognized for potential use in categorizing patients for clinical studies across various cancer types, highlighting its relevance for potential future application in treatments. In Europe, the large number of cancer cases creates a continuing need for improved detection and individualized treatment strategies. Certain non-invasive methods utilizing specific methylation biomarkers for cancer diagnosis are currently covered by health systems in some European countries. Apart from these, targeted therapies that influence epigenetic processes have been evaluated by the European regulatory body in recent years, some of which may eventually require specific diagnostic tools to guide their use. National cancer plans in the United Kingdom, Italy, and Sweden explicitly allocate funding for epigenetic biomarker validation, reinforcing institutional demand. The convergence of clinical urgency,y regulatory support, rt and therapeutic innovation solidifies oncology as the cornerstone of epigenetic application in Europe.

The drug delivery segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 16.8% during the forecast period due to the emergence of epigenetic modulators as therapeutic agents and the parallel need for advanced delivery systems to overcome bioavailability and targeting challenges. Epigenetic drugs such as histone deacetylase inhibitors often suffer from poor solubility, rapid clearance, and off-target effects, necessitating nanoformulations and ligand-conjugated carriers. Funding initiatives support a variety of projects developing advanced delivery platforms for epigenetic treatments, such as those utilizing lipid nanoparticles and polymer-based vectors. Research is exploring novel systems for delivering RNA-modifying enzymes, often employing exosome mimetics, which show promise in enhancing targeted accumulation in preclinical studies. A number of clinical trials are currently underway across the region, focusing on new epigenetic drug delivery methods, with many specifically addressing solid tumors. Regulatory incentives for platform technologies further accelerate translational pipelines. This convergence of material science, molecular biology,gy and regulatory science is redefining epigenetic therapeutics and establishing drug delivery as the most dynamic frontier in the European epigenetics landscape.

By Enzymes Insights

TDNA-modifying enzymes segment led the European epigenetics market by accounting for a 63.5% share in 2025. The supremacy of the DNA modifying enzymes segment is credited toits fundamental role in causing and reversing DNA methylation, the most extensively studied epigenetic mark. Enzymes such as DNA methyltransferase,s DNM, Ts, and ten eleven translocation TET dioxygenases are essential for both basic research and diagnostic applications. The widespread use of bisulfite conversion, a process dependent on controlled enzymatic activity in methylation sequencing workflows, underpins consistent demand. Furthermore, the clinical adoptiomethylation-basedbased biomarkers in oncology promoter methylation testing for glioblastoma treatment relies on precise enzymatic reactions. National genomics initiatives have standardized enzymatic workflows across sequencing centers, ensuring bulk procurement. The irreplaceable biochemical function of these enzymes in both discovery and validation phases ensures their sustained dominance in the epigenetic enzyme landscape.

The RNA modifying enzymes segment is expected to exhibit a noteworthy CAGR of 18.1% over the forecast period,d dueto the rising recognition of epitranscriptomi, cs, the study of post transcriptional RNA modifications as a critical layer of gene regulation. Modifications such as N6 methyladenosine m6A regulate mRNA stability, splicing,g and translation with direct implications in cancer immunology and neurodevelopment. The European Molecular Biology Organization has designated epitranscriptomics as a strategic priority,, ty with dedicated core facilities established in Heidelberg and Barcelona, equipped for high-throughput RNA modification profiling. Pharmaceutical companies have launched internal programs targeting RNA demethylases, with several candidates entering preclinical development. Additionally, the development of antibody-free detection methods, such as nanopore direct RNA sequencing, which requires enzymatic adaptation,n has further stimulated demand. RNA-modifying enzyme procurement has increased in European laboratories. This increase reflects a shift toward exploring epigenetics with a focus on RNA. The growth establishes the segment as a leader in enzymatic innovation.

COUNTRY LEVEL ANALYSIS

Germany Epigenetics Market Analysis

Germany dominated the European epigenetics market by capturing a 19.4% share in 2025. The supremacy of the German market is because of its robust research infrastructure, strong publifunding,g,, and advanced healthcare integration of molecular diagnostics. The country hosts numerous specializedepigenetic laboratoriee,,s primarily concentrated in tRhine-Ruhruhr and Munich innovation corridors. National investment has been directed toward epigenetics-related projects as part of a national research strategy and a specific initiative addressing cancer. The country's health insurance system has granted approval for the reimbursement of certain epigenetic tests, which include methylation-based assays for both colorectal and lung cancer screening. These approved tests have been used for patient screenings. The presence of global life science companies further anchors the domestic supply chain, enabling rapid technology transfer. Moreover, German universities lead Europe in epigenetics publications. This synergy between policy science and industrystrengthensn Germany’s position and sustains high market activity across academic, clinclinicala nd commercial domains.

United Kingdom Epigenetics Market Analysis

The United Kingdom was the second largest country in Euroin the pe epeepigeneticset and accounted for a 16.8% share in 2025. The growth of the UK market is driven by its world-class genomics ecosystem and strategic emphasis on data-driven medicine. The 100,000 Genomes Project has expanded into a national genomic medicine service that integrates epigenetic analysis into diagnostics for cancer and rare diseases. Large-scale patient genome sequencing now frequently incorporates matched methylation profiles to facilitate the identification of new biomarkers. Substantial funding has been directed toward epigenetic research, particularly concerning the developmental origins of health and disease alongside oncological studies. Academic powerhouses such as the University of Cambridge and the Francis Crick Institute host dedicated epigenetics centers funded through long-term strategic awards from the Wellcome Trust and Cancer Research UK. Notabl,, the Medicines and Healthcare products Regulatory Agency has established a fast track evaluation route for epigenetic companion diagnostics linked to targeted therapies. DeDespite Brexit-relatedhallenges, the UK maintains strong scientific collaboration with EU partners through associate membership in Horizon Europe. This sustained investment in data infrastructure and translational science ensures the UK remains a pivotal force in the European epigenetics market.

France Epigenetics Market Analysis

France holds a noteworthy position in the European epigenetics market, with centralized national strategies and high clinical research throughput. Moreover, its growth is also due to a national plan designed to integrate advanced genomic analyses into regional platforms. These platforms are now routinely incorporating epigenetic information into many of the generated genomic profiles. Oncology currently represents a majority of cases where these epigenetic annotations are utilized. A major research center in the country launched a specific program to examine methylation signatures related to therapy resistance in certain types of cancer. Funding has been allocated to numerous research projects in epigenetics. Emphasis for this funding includes the study of environmental epigenetics and how traits might be inherited across generations. Regulatory alignment with EU standards enables French developers such as IntegraGen to commercialize epigenetic kits across the bloc. Additionally, France’s biobank network,k comprising over three million annotated samples with epigeneticmetadataa ,ta provides unparalleled resources for biomarker validation. This integration of national planning,ing scientific excellence,ence and clinical scale positions France as a high-throughput engine of epigenetic innovation in Europe.

Switzerland Epigenetics Market Analysis

Switzerland experienced a steady expansion in the European epigenetics market due to its concentration of pharmaceutical innovation and precision diagnostics. Switzerland is fully associated with Horizon Europe, despite not being a member of the EU, and hosts several European Molecular Biology Laboratory (EMBL) outposts specializing in chromatin dynamics. The presence of global pharmaceutical giants such as Roche and Novartis, headquartered in Basell,l drives demand for advanced epigenetic tools in drugdiscovery, particularly for epigenetic target validation and biomarker identification. Swiss academic institutions lead in developing novel enzymatic tools for epigenome editing. Furthermore, Switzerland’s regulatory agency,, Swissmedic,dic maintains mutual recognition agreements with the European MedicinesAgencyg,ency expediting approval of epigenetic tests developed domestically. The unique blend of private sector investment,tment academic rigor, ,and regulatory agility enables Switzerland to punch far above its population weight in the European epigenetics ecosystem.

Sweden Epigenetics Market Analysis

Sweden is likely to grow Euthe ropean Euigenetics market from 2025 to 2033 ,,owing to its command in population-based epigenetic epidemiology and digital health integration. Longitudinal biobanks in Sweden provide substantial data resources, including information related to epigenetics. The national genomics platform in Sweden incorporates epigenetic assessments into standard diagnostic procedures for specific childhood conditions and developmental disorders. A clinical epigenomics unit, located in Stockholm, provides specialized methylation profiling for certain inherited disorders and for the classification of tumors. Digital health infrastructure, including the national patient data pportall allows secure linkage of epigenetic profiles with electronic healthrecordsr enabling real-worldld evidence generation. This fusion of population science, clinical implementationn,n and data interoperability establishes Sweden as a model for scalable epigenetic medicine in Europe.

COMPETITIVE LANDSCAPE

Competition in the European epigenetics market is characterized by a dynamic interplay between global life science leaders and specialized European innovators. The landscape features intense rivalry in reagent and kit developent,, where performance reproducibility and regulatory compliance serve as key differentiators. Larger corporations leverage their integrated platforms to ooffer end-to-endepigenetic workflows, while niche players compete through superior antibody specificity or novel enzymatic tools. Academic collaboration is a critical battleground with companies vying for inclusion in publicly funded consortia such as those under Horizon Europe. Intellectual property around epigenetic biomarkers and detection methodologies further intensifies strategic positioning. Although pricing pressure exists in the research segsegmentclinical adoption is driving demand for standardizeCE-markede,d solutions, creating a bifurcated competitive environment that rewards both scientific excellence and regulatory agility across diverse European healthcare ecosystems.

KEY MARKET PLAYERS

A few of the notable companies operating in the europe epigenetics market profiled in this report are

- Abcam plc.

- Illumina, Inc.

- QIAGEN N.V.

- Merck & Co.

- New England Biolabs, Inc.

- Sigma-Aldrich Corporation

- Thermo Fisher Scientific, Inc.

- Active Motif

- Diagenode, Inc.

- Zymo Research Corporation

TOP LEADING PLAYERS IN THE MARKET

- Thermo Fisher Scientific maintains a prominent footprint in the European epigenetics market through its comprehensive portfolio of reagent kits and analytical instruments tailored for DNA methylation and chromatin studies. The company actively supports academic and clinical research by providing integrated workflows compatible with next-generation sequencing platforms. In recent years, it has expanded its epigenetic offerings through strategic enhancements to its Ion Torrent and Applied Biosystems product line,s enabling high-sensitivity detection of epigenetic modifications. Thermo Fisher also collaborates with European research consortia under Horizon Europe to validate novel epigenetic biomarkers. These initiatives reinforce its role as a critical enabler of translational epigenetics across the continent while strengthening its global leadership in life science tools.

- Qiagen plays a pivotal role in the European epigenetics market by delivering standardized sample preparation and assay solutions that underpin reproducible epigenetic research. Headquartered in Germany,,he company leverages its regional proximity to accelerate product development aligned with European regulatory and clinical standards. Qiagen’s EpiTect and PyroMark platforms are widely adopted for methylation analysis in oncology and infectious disease studieRecentlyen t,ly the company launched automated epigenetic workflows compatible with its QIAcube Connect syst,, enhancing throughput for diagnostic laboratories. It has also deepened partnerships with European biobanks and precision medicine initiatives to embed its technologiesin large-scalee epigenome mapping efforts. These actions solidify Qiagen’s influence in both research and regulated clinical epigenetics across Europe and globally.

- Abcam contributes significantly to the European epigenetics market through its extensive catalog of high-quality antibodies, enzymes,s and assay kits targeting histonemodificationso, ns DNA methylation, and chromatin regulators. The company’s emphasis on validation and reproducibility aligns closely with European research integrity standards. Based in the United Kingdom,gdom Abcam has intensified its focuCRISPR-basedbased epigenome editing tools and proximity ligation assays that enable spatial epigenetic profiling. Additionally, Abcam integrates digital protocols andbatch-specificc validation data into its product ecosystem, enhancing usability for academic and industrial researchers alike. These innovations position Abcam as a key scientific partner in advancing epigenetic discovery throughout Europe and beyond.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in theEuropeane epigenetics market predominantly employ product portfolio expansion through continuous innovation in reagents and kits tailored for clinical and research applications. They actively pursue strategic collaborations with academic institutions and public health initiatives to co-develop and validate epigenetic biomarkers. Geographic consolidation is achieved by strengthening local distribution and technical support networks, particularly in high-growth regions such as Southern and Eastern Europe. Regulatory alignment is prioritized through early engagement with agencies like the European Medicines Agency to facilitate CE IVD certification of diagnostic assays. Additionally, companies invest in digital integration by embeddingcloud-basedd data analysis and instrument connectivity features to enhance workflow efficiency and data reproducibility across laboratories.

MARKET SEGMENTATION

This research report on the europe epigenetics market has been segmented & sub-segmented into the following categories

By Product

- Enzymes

- Instruments & Consumable

- KITS

- Reagents

By Research Area

- Developmental Biology

- Oncology

- Drug Delivery

By Enzymes

- DNA-Modifying Enzymes

- Protein-Modifying Enzymes

- RNA-Modifying Enzymes

By Instruments & Consumables

- Mass Spectrometers

- Next-Generation Sequencers

- qPCR

- Sonicators

By KITS

- Bisulfite Conversion KITS

- Chip-Sequence KITS

- RNA Sequencing KITS

- Whole-Genome Amplification KITS

- 5-HMC and 5-MC Analysis KITS

By Reagents

- Antibodies

- Buffers

- Histones

- Magnetic Beads

- Primers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe