Europe Facial Treatment Market Research Report By Product Type and Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands and Rest of Europe) - Industry Analysis, Size, Share, Growth, Trends and Forecast (2026 to 2034)

Market Size, 2025

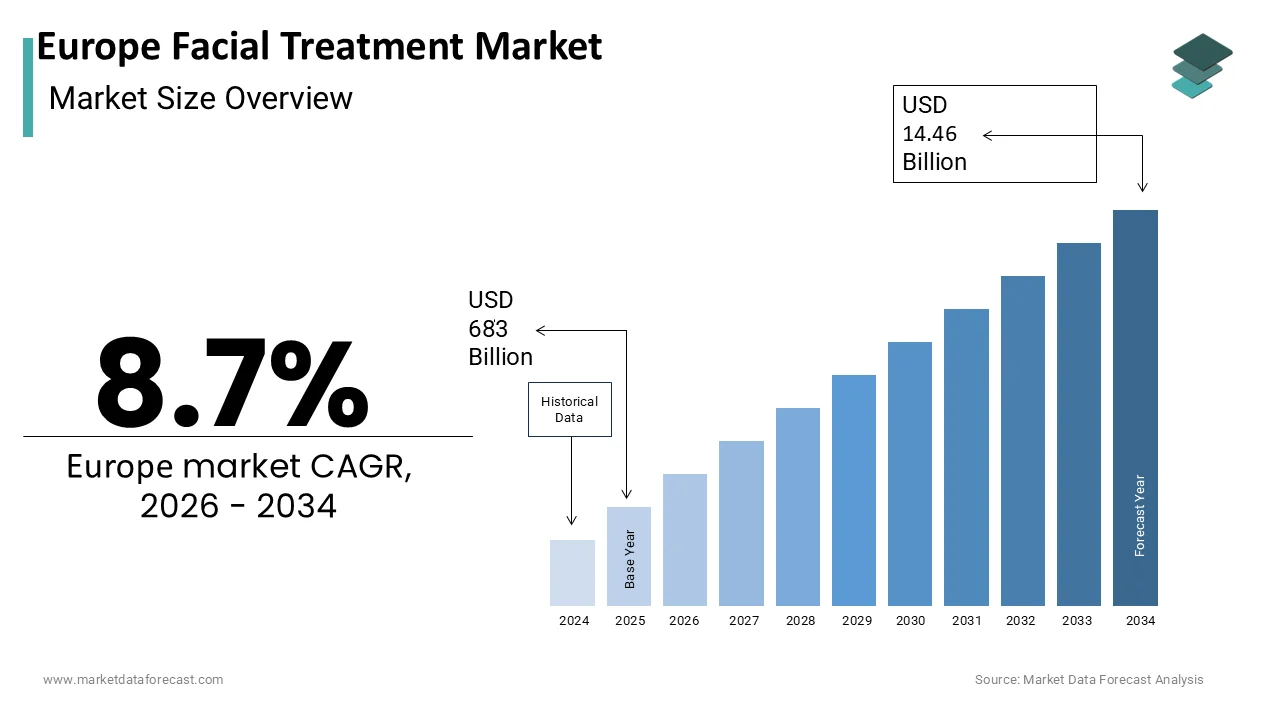

$6.83 BnMarket Estimate, 2026

$7.42 BnMarket Forecast, 2034

$14.46 BnCAGR, 2026–2034

8.7%Europe Facial Treatment Market Size

The europe facial treatment market was valued at USD 6.83 billion in 2025, is expected to have an 8.7 % CAGR from 2026 to 2034 and be worth USD 14.46 billion by 2034 from USD 7.42 billion in 2026.

Facial treatments are professional and semi-professional skincare interventions designed to address concerns such as aging, hyperpigmentation, acne, and barrier dysfunction. These range from non-invasive procedures like chemical peels, microdermabrasion, and LED therapy to advanced modalities including radiofrequency, ultrasound tightening, and injectable biostimulators administered in medical aesthetic clinics. Unlike over-the-counter skincare, facial treatments deliver targeted, clinically observable results through controlled delivery of active ingredients or energy-based technologies. According to sources, doctors in France and Germany have a mandatory obligation to pursue continuing medical education (CME/CPD) throughout their careers, as is common for medical professionals across much of Europe. Consumer behavior reflects growing sophistication. As per sources, a share of adults have undergone at least one professional facial treatment in the past two years. This integration of dermatological science, consumer wellness, and regulatory rigor defines the European Facial Treatment Market as a convergence point between beauty, health, and technology.

MARKET DRIVERS

Rising Prevalence of Skin Conditions Linked to Environmental Stressors

Urbanization and environmental pollution have significantly increased the incidence of reactive and inflammatory skin conditions in the region, which drives the growth of the European facial treatment market. According to the European Environment Agency, a notable share of the EU urban population was exposed to air pollution levels exceeding World Health Organization guidelines, with particulate matter and nitrogen dioxide identified as key contributors to oxidative skin damage. This exposure correlates with a measurable rise in dermatological complaints. In addition, clinics in cities like London, Paris, and Milan have introduced “detox” facial protocols featuring chelating agents, antioxidant serums, and lymphatic drainage techniques. Furthermore, the EU’s Green Deal Urban Agenda has spurred public awareness campaigns linking environmental health to skin integrity, normalizing professional intervention as preventive care. Climate-related skin issues are now endemic, which prompts the reclassification of facial treatments from luxuries to essentials in metropolitan skincare.

Integration of Medical Aesthetics into Mainstream Wellness Culture

The normalization of medical aesthetics as part of holistic wellness has redefined consumer attitudes, which in turn boosts the expansion of the European facial treatment market. No longer confined to vanity-driven interventions, procedures such as radiofrequency tightening and biostimulatory injectables are increasingly framed as proactive health investments. According to research, non-surgical facial procedures in Europe grew, with the largest uptake among professionals aged 30 to 45 seeking preventive aging solutions. This shift is amplified by digital health platforms, which now list aesthetic dermatology alongside general practitioners, reducing stigma and improving access. Social media further legitimizes these choices. This cultural reframing positions facial treatments as essential components of modern self-care rather than indulgent luxuries.

MARKET RESTRAINTS

Stringent Regulatory Classification and Practitioner Licensing Requirements

Operational constraints due to fragmented and rigorous regulatory frameworks governing treatment classification and practitioner qualifications obstruct the growth of the European facial treatment. Unlike regions with unified aesthetic regulations, the EU delegates oversight to national health authorities, resulting in divergent rules on what constitutes a medical versus cosmetic procedure. Furthermore, practitioner licensing varies drastically; in France, only physicians may perform injectables, while in the Czech Republic, certified aestheticians can administer certain biostimulators. The inconsistencies deter investment, delay product launches, and increase legal risk. The lack of progress in regulatory alignment under the EU Medical Devices Regulation means market fragmentation will continue to hinder scalable expansion.

High Consumer Sensitivity to Treatment Downtime and Recovery Periods

European consumers exhibit pronounced aversion to procedures requiring visible recovery time, which limits the adoption of more aggressive modalities and thereby inhibits the expansion of the European facial treatment market. Many potential clients reject treatments involving more than 48 hours of redness, peeling, or social downtime. This preference favors lunchtime procedures such as gentle enzyme peels, LED therapy, and superficial hyaluronic acid infusions, while constraining demand for deeper resurfacing or ablative lasers. The trend is especially pronounced in Northern Europe, where workplace cultures emphasize consistent appearance. Consequently, clinics report underutilization of high-efficacy but higher-downtime technologies. This risk-averse mindset pressures providers to prioritize immediacy over longevity, potentially compromising long-term outcomes. Consumer tolerance will continue to restrict the therapeutic potential of the market until innovations can provide effective results without requiring any recovery time.

MARKET OPPORTUNITIES

Expansion of At-Home Professional Grade Treatment Ecosystems

The convergence of in-clinic expertise with at-home maintenance through connected devices and subscription protocols provides potential opportunities for the growth of the European facial treatment market. Leading dermatological clinics are now bundling professional sessions with curated home regimens featuring medical-grade serums and FDA-cleared or CE-marked devices like microcurrent wands and LED masks. Brands have partnered with clinics to offer co-branded kits that sync with treatment calendars via mobile apps. This hybrid model enhances treatment efficacy, builds recurring revenue, and deepens client loyalty, redefining the facial treatment journey as continuous rather than episodic.

Growth of Personalized Skin Diagnostics and AI-Driven Treatment Planning

The integration of artificial intelligence and advanced skin diagnostics is opening fresh prospects for the expansion of the European facial treatment market. High-resolution imaging systems quantify parameters such as pore volume, melanin distribution, and wrinkle depth, enabling data-driven protocols. These tools generate individualized treatment roadmaps that combine modalities for optimal synergy. Furthermore, the EU’s General Data Protection Regulation has spurred the development of on-premises AI systems that process skin data locally, which addresses privacy concerns. Startups are collaborating with dermatologists to refine algorithms using diverse European skin types. The shift in consumer preference toward precision over generic solutions means AI-driven diagnostics are key to establishing facial treatments as leaders in personalized aesthetics.

MARKET CHALLENGES

Persistent Shortage of Qualified Aesthetic Practitioners in Emerging Markets

The acute shortage of certified practitioners in Central and Eastern Europe, where demand is rising faster than training capacity, affects the growth of the European facial treatment market. According to research, countries have fewer than five accredited aesthetic training centers each, which produces fewer qualified professionals annually despite a combined population of millions. This gap fuels an unregulated shadow market. The consequence is inconsistent outcomes and safety risks, undermining consumer confidence. Occasional pop-up clinics by Western European practitioners are a temporary measure, but the model itself is not a viable, long-term solution. The EU’s Erasmus+ program has allocated limited funding for cross-border aesthetic education, but systemic accreditation reform remains slow. Regional growth will be hampered by quality and safety issues until the local workforce's skills meet current industry demands.

Escalating Cost Pressures from Energy-Intensive Treatment Technologies

The high energy consumption of modern aesthetic devices, exacerbated by the region’s elevated electricity costs, challenges the expansion of the European facial treatment market. Technologies such as fractional CO2 lasers, high-intensity focused ultrasound, and multi-modality platforms require substantial power for cooling and operation. The pressure forces difficult trade-offs. Some clinics have reduced treatment hours or deferred equipment upgrades to manage bills. Moreover, the EU’s Carbon Border Adjustment Mechanism indirectly affects imported devices by increasing manufacturing costs for non-compliant suppliers. "The initial expense of energy-efficient models presents a significant financial hurdle for small practices, despite some brands offering them. High energy expenses will diminish profitability and hinder the uptake of new technology until renewable energy sources are better integrated or device efficiency is enhanced, especially for independent providers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Lutronic Corporation, Cutera Inc., Lynton Lasers Ltd., Sciton Inc., Alma Lasers Ltd., Solta Medical Inc., Lumenis Ltd., Cynosure Inc., Strata Skin Sciences Inc., Syneron Medical Ltd., Venus Concept Canada Corporation, Fotona d.d. |

SEGMENTAL ANALYSIS

By Product Type Insights

In 2025, the laser-based devices segment led the European facial treatment market and held a 32.4% share. Their unmatched precision in treating pigmentation, vascular lesions, and photoaging has mainly contributed to the growth of the laser-based devices segment. Unlike broad-spectrum technologies, lasers deliver monochromatic light at specific wavelengths, enabling selective photothermolysis with minimal collateral damage. Clinical validation further reinforces dominance. Regulatory clarity also plays a role. The EU Medical Devices Regulation classifies most aesthetic lasers as Class IIa or IIb, providing a defined approval pathway that encourages manufacturer investment. Apart from these, the aging population amplifies demand. This combination of clinical efficacy, regulatory maturity, and demographic alignment ensures laser-based devices remain the cornerstone of professional facial treatments.

The LED devices segment is on the rise and is expected to be the fastest-growing segment in the regional market by witnessing a CAGR of 15.8% from 2025 to 2033 due to their non-invasive nature, zero downtime, and expanding evidence base for anti-inflammatory and collagen-stimulating effects. LED therapy modulates cellular activity using specific wavelengths, like blue light for acne and red/near infrared for rejuvenation, which differentiates itself from ablative or thermal methods that can damage tissue. Regulatory advantages further boost adoption. Under EU classification, most LED panels are categorized as low-risk wellness devices, bypassing stringent medical device requirements. This enables deployment in beauty clinics, spas, and even at home. Moreover, rising consumer interest in skin fasting and barrier-friendly treatments aligns perfectly with LED’s gentle mechanism. The growing practice among dermatologists of prescribing LED therapy for ongoing care between intensive procedures is transforming its status from an optional extra to an indispensable component, and thereby fuelling continuous growth.

By End User Insights

The dermatology clinics segment captured a leading share of 58.7% of the European facial Treatment Market in 2025. The dominance of the dermatology clinics segment is attributed to their role as the primary providers of medically supervised, high-efficacy interventions. These clinics are staffed by board-certified dermatologists who can legally perform advanced procedures such as deep laser resurfacing, radiofrequency microneedling, and injectable biostimulators, modalities restricted to medical professionals in most EU countries. Patient trust is a critical factor. Furthermore, national health systems in countries like Germany and Sweden increasingly recognize certain facial treatments, such as laser therapy for rosacea or acne scarring, as medically indicated, enabling partial insurance coverage and expanding access. The integration of diagnostic tools like dermoscopy and AI skin analysis within dermatology workflows also enables personalized treatment planning unmatched by non-medical settings. This clinical authority, regulatory legitimacy, and diagnostic sophistication solidify dermatology clinics as the dominant end-user segment.

The beauty clinics segment is expected to exhibit a noteworthy CAGR of 13.2% over the forecast period, owing to evolving scope of practice laws in select EU countries and rising consumer demand for accessible non-medical aesthetic care. In nations like Spain, Italy, and the Czech Republic, certified aestheticians can legally operate certain Class II devices, including IPL, RF, and LED, under defined protocols, enabling beauty clinics to offer professional-grade treatments without physician oversight. Urbanization further supports this trend. Apart from these, social media has normalized aesthetic care, with beauty clinics leveraging Instagram and TikTok to showcase before-and-after results and educational content. As regulatory frameworks gradually expand permissible procedures, beauty clinics are positioned to capture mainstream demand for preventive and maintenance skincare.

COUNTRY LEVEL ANALYSIS

Germany Facial Treatment Market Analysis

Germany dominated the European facial Treatment Market and accounted for a 20.3% share in 2025. The prominence of Germany is primarily driven by its rigorous medical standards and high density of certified dermatologists. The country enforces strict regulations under the Heilmittelwerbegesetz, which prohibits non-physicians from performing invasive or energy-based treatments, ensuring that advanced procedures remain within clinical settings. Public health infrastructure supports access; statutory health insurers cover laser treatments for conditions like severe acne scarring and port wine stains, reaching millions of patients annually. Consumer behavior reflects this medicalized approach. Apart from these, Germany hosts leading aesthetic device manufacturers, which fosters innovation and local supply chains. This ecosystem of regulatory clarity, clinical excellence, and domestic manufacturing cements Germany’s dominance in high-quality, medically supervised facial care.

France Facial Treatment Market Analysis

France followed closely in the European facial treatment market and occupied a 17.8% share in 2025. The growth of France is fuelled by its cultural emphasis on skincare as an art form and its progressive yet controlled regulatory environment. French law permits only physicians to perform injectables and ablative procedures, but allows trained estheticians to use non-ablative devices like LED and superficial RF under medical supervision. A large number of dermatologists and plastic surgeons are authorized to deliver aesthetic treatments, concentrated in urban centers like Paris and Lyon. Luxury beauty houses operate high-end facial studios that blend heritage techniques with cutting-edge technology, attracting international clientele. Moreover, France’s Agence Nationale de Sécurité du Médicament actively monitors device safety, maintaining consumer confidence. This fusion of cultural prestige, medical oversight, and luxury positioning ensures France remains a high-value and high-volume market.

United Kingdom Facial Treatment Market Analysis

The United Kingdom is another notable player in the European facial Treatment Market, with a dynamic mix of private dermatology practices and premium beauty clinics operating under evolving regulatory scrutiny. Unlike many EU nations, the UK lacks a centralized licensing system for aesthetic practitioners, though recent reforms under the Health and Care Act 2022 mandate registration for all injectable providers. London hosts licensed beauty and medical aesthetic centers, as per data from the Local Government Association. Consumer demand is robust. The rise of “skinfluencers” and telehealth consultations via platforms like Zava has further normalized access. Despite regulatory gaps, the UK’s entrepreneurial ecosystem, high disposable income, and media-driven beauty culture sustain its position as a key growth engine.

Italy Facial Treatment Market Analysis

Italy grew steadily in the European facial treatment market because of its rapid adoption of non-invasive technologies and strong regional disparities in access. Northern regions like Lombardy and Emilia Romagna feature advanced dermatology centers offering laser and RF treatments, while Southern Italy relies more on traditional beauty institutes. Cultural factors drive demand. The Italian Ministry of Health permits certified aestheticians to operate Class II devices, enabling beauty clinics to offer IPL and LED treatments without a physician's presence. Apart from these, medical tourism boosts the sector. Cities attract clients from Eastern Europe and the Middle East seeking high-quality care at lower costs than Paris or London. This blend of cultural priority, regulatory flexibility, and tourism appeal positions Italy as a resilient and expanding market.

Sweden Facial Treatment Market Analysis

Sweden is predicted to grow in the European facial Treatment Market during the forecast period. It is emerging as a leader in evidence-based, sustainability-oriented aesthetic care. The Swedish healthcare system integrates dermatological aesthetics into public clinics for medically indicated conditions, while private providers focus on wellness-driven treatments. Consumer behavior reflects national values. Stockholm and Gothenburg host innovation hubs where startups like Foreo and Lyma develop at home and professional devices with circular design principles. Furthermore, Sweden’s stringent advertising laws prohibit exaggerated claims, fostering trust in realistic outcomes. The country also leads in gender inclusivity. This convergence of scientific rigor, sustainability, and social progressivism defines Sweden’s distinctive and growing role in the European landscape.

COMPETITIVE LANDSCAPE

The European facial Treatment Market features intense competition among global device manufacturers, regional innovators, and emerging technology startups. Dominance is held by established players like Lumenis and Candela, which leverage decades of clinical validation and strong relationships with dermatologists. However, the regulatory complexity of the EU Medical Devices Regulation creates high barriers to entry, limiting the number of new entrants but favoring companies with robust quality management systems. Competition is less about price and more about clinical outcomes, safety profiles, and practitioner support. Differentiation arises through technological sophistication, such as picosecond lasers or impedance-controlled RF, and integration with digital diagnostics. Regional players in Germany and France focus on niche applications like rosacea or post-inflammatory erythema, while Nordic startups emphasize sustainability and energy efficiency. Despite consolidation trends, the market remains dynamic due to rapid innovation in non-invasive modalities and evolving scope of practice laws that expand treatable indications. Trust, compliance, and clinical proof remain the ultimate competitive currencies.

KEY MARKET PLAYERS

A few of the major companies operating in the europe facial treatment market profiled in this report are

- Lutronic Corporation

- Cutera Inc.

- Lynton Lasers Ltd.

- Sciton Inc.

- Alma Lasers Ltd.

- Solta Medical Inc.

- Lumenis Ltd.

- Cynosure Inc.

- Strata Skin Sciences Inc.

- Syneron Medical Ltd.

- Venus Concept Canada Corporation

- Fotona d.d.

TOP LEADING PLAYERS IN THE MARKET

- Lumenis Ltd is a global leader in energy-based aesthetic devices with a strong presence in the European facial Treatment Market through its advanced laser and IPL platforms. The company’s M22 and Stellar M platforms are widely adopted by dermatology clinics for treating pigmentation, vascular lesions, and skin rejuvenation. Lumenis has reinforced its European footprint by aligning its devices with the EU Medical Devices Regulation and establishing training academies in Germany and France to certify practitioners. Its commitment to clinical validation and physician education strengthens trust among medical professionals across the region.

- Candela Corporation plays a pivotal role in the European facial Treatment Market with its GentleMax Pro and PicoWay laser systems, renowned for precision in pigment and tattoo removal. The company emphasizes regulatory compliance and has secured CE certification for all its facial treatment devices under the updated MDR framework. Candela has expanded its clinical support network across Southern Europe, offering on-site training and treatment protocol development for dermatologists. Its focus on innovation and medical credibility positions it as a preferred partner for high-end aesthetic practices.

- Ellman International Inc. contributes to the European facial Treatment Market through its Surgitron radiofrequency and plasma devices used for skin tightening and minimally invasive resurfacing. The company targets both dermatology and plastic surgery clinics with devices that offer sub-ablative precision and rapid recovery. Ellman has strengthened its European presence by partnering with local distributors in Italy and the Netherlands to provide localized service and regulatory guidance. Its emphasis on safety, minimal downtime, and physician-centric design supports sustained adoption in regulated European markets.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Facial Treatment Market prioritize regulatory compliance with the EU Medical Devices Regulation to ensure device certification and market access. They invest heavily in clinical evidence generation through multicenter trials to support efficacy claims and practitioner confidence. Companies establish regional training academies to certify dermatologists and aestheticians on proper device use, enhancing safety and treatment outcomes. Strategic partnerships with dermatology associations and aesthetic societies bolster credibility and facilitate protocol standardization. Product innovation focuses on smart features such as real-time skin feedback, AI-driven parameter adjustment, and integrated cooling systems. Expansion into hybrid models that combine in-clinic treatments with at-home maintenance kits drives patient retention. These strategies collectively address Europe’s emphasis on safety, evidence, and professional oversight in aesthetic care.

MARKET SEGMENTATION

This research report on the europe facial treatment market has been segmented and sub-segmented into the following categories.

By Product Type

- IPL Devices

- RF Devices

- Ultrasound Devices

- LED Devices

- Laser-Based Devices

By End User

- Dermatology Clinics

- Beauty Clinics

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which consumer trends are shaping the Europe Facial Treatment Market?

Key trends in the Europe Facial Treatment Market include a shift toward clean beauty, personalized products, and growing preference for sustainable, organic formulations among Europeans.

2. What role does technology play in the Europe Facial Treatment Market?

The Europe Facial Treatment Market is increasingly utilizing AI and data analytics for product customization, skin condition analysis, and targeted facial solutions.

3. Who are the leading countries in the Europe Facial Treatment Market?

Germany, the UK, France, Spain, and Italy are the primary contributors to the Europe Facial Treatment Market’s growth due to their established beauty culture and infrastructure.

4. Why is facial care preferred over other beauty treatments in the Europe Facial Treatment Market?

Facial care products in the Europe Facial Treatment Market dominate due to strong consumer demand for skin health, anti-aging, and wellness, reflecting Europe’s aging population.

5. Are natural and organic products trending in the Europe Facial Treatment Market?

Yes, natural and organic facial treatments have seen a surge in the Europe Facial Treatment Market as consumers seek products free from harmful chemicals and synthetic additives.

6. How are social media platforms influencing the Europe Facial Treatment Market?

Social media and beauty influencers have a significant impact on brand visibility and consumer choices within the Europe Facial Treatment Market, shaping purchasing behavior across Europe.

7. What challenges does the Europe Facial Treatment Market face?

High costs of facial care products, concerns over side effects, and a shortage of trained personnel for advanced treatments present challenges in the Europe Facial Treatment Market.

8. How is the e-commerce boom affecting the Europe Facial Treatment Market?

Increased online shopping in Europe enables wider access to facial treatment products, boosting growth and accessibility for both brands and consumers in the Europe Facial Treatment Market.

9. What are the most popular facial treatments in the Europe Facial Treatment Market?

Anti-aging, skin-brightening, facial injectables, and device-based treatments like microcurrents and LED therapy are highly sought after in the Europe Facial Treatment Market

10. How are sustainability concerns shaping the Europe Facial Treatment Market?

European consumers favor eco-friendly packaging and naturally-derived ingredients, prompting brands to adopt sustainable practices within the Europe Facial Treatment Market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com