- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

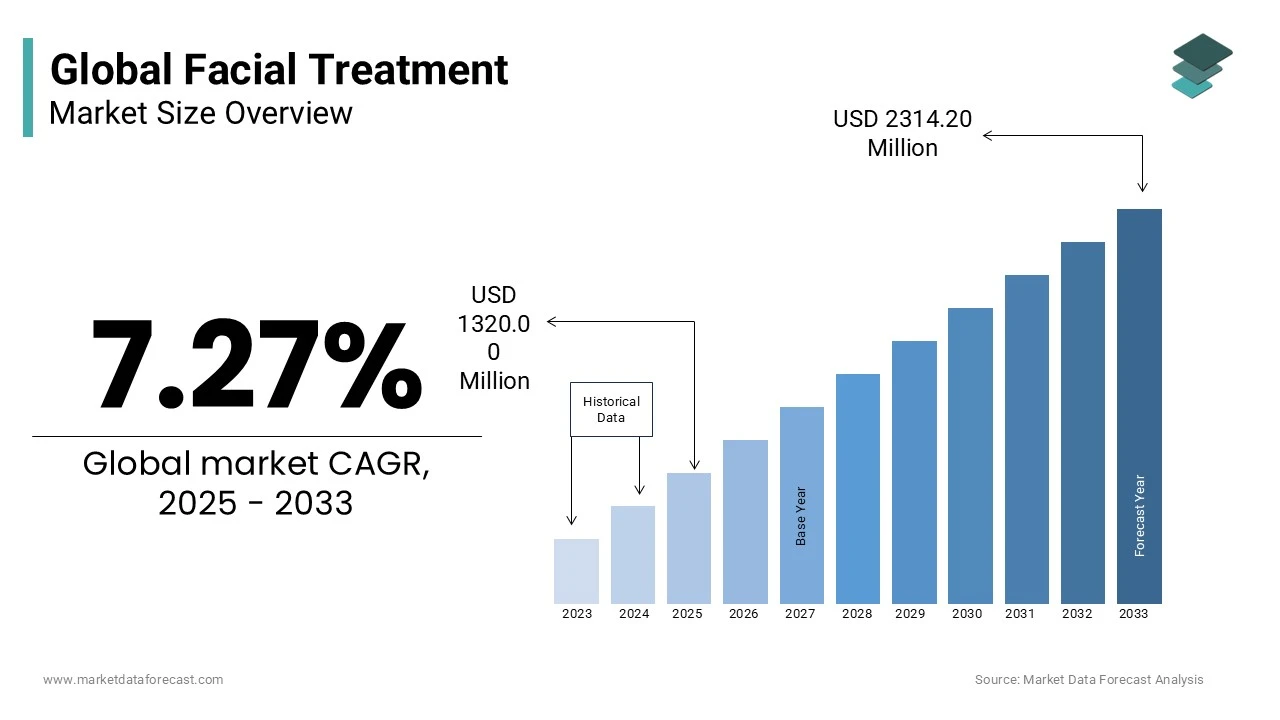

Global Facial Treatment Market Size

The global ethylene market size was valued at USD 1230.54 million in 2024 and is anticipated to reach USD 1320.00 million in 2025 from USD 2314.20 million by 2033, growing at a CAGR of 7.26% during the forecast period from 2025 to 2033.

Facial treatments are non-invasive and minimally invasive procedures designed to enhance skin health, address dermatological concerns, and improve aesthetic appearance through cleansing, exfoliation, hydration, and targeted interventions. These treatments are administered in professional settings such as dermatology clinics, medical spas, and aesthetic centers, utilizing advanced technologies and scientifically formulated products. According to the World Health Organization, skin conditions affect about 1.9 million people globally at any given time, making skin health a critical component of personal well-being. Additionally, the Global Burden of Disease Study indicates that psychosocial disorders linked to skin appearance contribute to over 45 million disability-adjusted life years annually. These underlying health and emotional dimensions underscore the growing integration of facial treatments into holistic dermatological care.

MARKET DRIVERS

Rising Awareness of Preventive Skincare Regimens

The increasing adoption of preventive skincare, particularly among younger demographics who are prioritizing long-term skin health over reactive solutions is a pivotal driver of the facial treatment market. Most individuals aged 18–34 in the United States now engage in regular professional facial treatments as part of a proactive skincare routine. This shift is fueled by dermatologist-led public education campaigns and digital dermatology platforms that emphasize early intervention to delay signs of aging and environmental damage. Also, consistent use of clinical facials incorporating antioxidants and peptides can reduce the onset of fine lines over the years. Furthermore, school-based skin health programs in countries like Australia and Canada have increased adolescent awareness. This cultural pivot toward prevention is transforming facial treatments from luxury indulgences into essential components of dermatological wellness.

Expansion of Medical-Grade Aesthetic Technologies

The proliferation of advanced, non-surgical facial technologies is significantly amplifying demand for professional treatments. Devices such as radiofrequency microneedling, intense pulsed light (IPL), and laser resurfacing offer measurable improvements in skin texture, pigmentation, and elasticity, attracting patients seeking clinical efficacy without surgical intervention. The integration of AI-driven skin analysis systems further enhances treatment precision, reinforcing consumer confidence in professional facial interventions.

MARKET RESTRAINTS

Regulatory Fragmentation in Aesthetic Device and Product Approval

The facial treatment market faces significant constraints due to inconsistent regulatory oversight across regions, particularly concerning the classification and approval of aesthetic devices and cosmeceuticals. In the United States, the Food and Drug Administration (FDA) regulates certain laser and radiofrequency devices as Class II medical equipment, requiring rigorous premarket notification, while similar devices in Southeast Asia may be cleared under less stringent cosmetic guidelines. This regulatory disparity creates compliance challenges for multinational providers and undermines consumer safety, deterring widespread adoption in regions where oversight remains weak or inconsistently enforced.

Shortage of Certified Aesthetic Practitioners

The global deficit of trained and certified professionals qualified to administer advanced facial treatments safely is a critical restraint on market growth. Even in high-income nations, the demand for aesthetic practitioners exceeds supply. The absence of standardized training curricula across countries further exacerbates the issue.

MARKET OPPORTUNITIES

Integration of AI-Powered Skin Diagnostics in Treatment Planning

The emergence of artificial intelligence in dermatological assessment presents a transformative opportunity for the facial treatment market. AI-driven imaging systems can analyze skin conditions with greater accuracy than human observation, detecting early signs of aging, pigmentation, and barrier dysfunction. Also, AI algorithms achieve diagnostic accuracy in identifying skin conditions from high-resolution facial scans. Companies like L’Oréal and Canfield Scientific have deployed tools and partnerships with clinics/retailers. Also, clinics using AI diagnostics reported an increase in patient retention due to enhanced treatment transparency and outcome predictability. This technological evolution is paving the way for hyper-personalized, data-driven facial therapies that improve efficacy and elevate consumer engagement.

Growth of Hybrid At-Home and In-Clinic Treatment Models

The convergence of professional and at-home skincare is creating a dynamic new market segment where consumers receive clinical treatments supplemented by personalized home regimens. This hybrid model extends treatment efficacy and strengthens patient adherence. In Japan, dermatology clinics increasingly prescribe customized serum kits alongside in-office procedures. Additionally, tele-dermatology platforms like First Derm and SkinVision are enabling remote follow-ups. This integrated approach not only enhances outcomes but also builds long-term patient loyalty, transforming facial treatments into continuous care journeys rather than isolated services.

MARKET CHALLENGES

Standardization and Safety Concerns in Non-Clinical Settings

The growing proliferation of treatments in non-medical environments such as beauty salons and spas, where procedural standards and emergency preparedness are often inadequate, is one of the foremost challenges facing the facial treatment market. Furthermore, complications from improperly administered chemical peels have risen since 2020. The absence of universal protocols for device usage, product concentration limits, and client screening in non-clinical venues undermines the credibility of the entire sector and deters risk-averse consumers from engaging in otherwise beneficial treatments.

Environmental Impact of Single-Use Materials in Facial Procedures

The facial treatment industry faces mounting scrutiny over its environmental footprint, particularly the extensive use of disposable gloves, wipes, applicators, and packaging. In addition, the European Environment Agency has called for stricter sustainability mandates in cosmetic services, urging a shift toward reusable tools and eco-certified products. However, sterilization requirements and hygiene regulations complicate the transition.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Key Market Players | Lutronic Corporation, Cutera Inc., Lynton Lasers Ltd., Sciton Inc., Alma Lasers Ltd., Solta Medical Inc., Lumenis Ltd., Cynosure Inc., Strata Skin Sciences Inc., Syneron Medical Ltd., Venus Concept Canada Corporation, and Fotona d.d. |

SEGMENTAL ANALYSIS

By Product Type Insights

The laser-based devices segment dominated the facial treatment product type by capturing 36.7% of the global market in 2024. Their position is due to unmatched precision in targeting pigmentation, vascular lesions, and skin resurfacing. These devices are clinically validated for treating melasma, acne scars, and photoaging. The integration of cooling mechanisms and variable wavelength options has also improved safety across skin types, broadening patient eligibility and reinforcing clinical adoption.

The LED devices segment is expanding at a CAGR of 10.3% from 2025 to 2033 and is making it the fastest-growing product segment in the facial treatment market. This surge is driven by their non-invasive nature, minimal downtime, and proven efficacy in managing inflammatory skin conditions. As per a clinical study published in Lasers in Surgery and Medicine, blue and red LED therapy reduced moderate acne lesions by 64% after eight weeks of treatment. The technology’s safety profile allows use in sensitive populations, including pregnant women and those with darker skin tones, where lasers pose hyperpigmentation risks. In Japan, the Ministry of Health, Labour and Welfare recognizes LED phototherapy as a standard adjunct in acne and rosacea management. Additionally, the rise of at-home LED masks has catalyzed professional adoption, with clinics now offering LED as a maintenance therapy between intensive procedures.

By End-User Insights

The dermatology clinics segment led the global facial treatment market in 2024. Their dominance is anchored in medical credibility, access to advanced technologies, and integration with diagnostic dermatology. These clinics treat a broad spectrum of conditions, from acne and rosacea to precancerous lesions, utilizing evidence-based protocols. A notable share of patients seeking facial treatments for hyperpigmentation or acne scarring prefer dermatologist-administered care due to lower complication risks. In Germany, statutory health insurance covers certain laser treatments for severe acne, increasing patient flow to dermatology-led facilities. The integration of AI skin analyzers and electronic health records in dermatology practices also enhances treatment personalization, reinforcing their position as the gold standard in facial care delivery.

The beauty clinics segment is growing at a CAGR of 9.7% which is driven by their accessibility, affordability, and focus on aesthetic enhancement rather than medical intervention, as projected by the Global Spa and Wellness Institute. These centers cater to a younger demographic seeking preventative and cosmetic improvements, offering services such as LED therapy, chemical peels, and radiofrequency tightening. In India, the number of licensed beauty clinics increased between 2020 and 2023, fueled by rising disposable income and social media influence. Strategic partnerships with skincare brands and installment payment options have further expanded.

REGIONAL ANALYSIS

North America Facial Treatment Market Analysis

North America holds a 35.8% share of the global facial treatment market, establishing it as the most technologically advanced and high-spending region. The United States drives this leadership through a dense network of dermatology clinics, high consumer awareness, and rapid adoption of cutting-edge devices. Canada complements this landscape with universal healthcare coverage for certain dermatological conditions, enabling early intervention. The presence of leading device manufacturers like Cutera and Solta Medical fosters innovation, while FDA approvals ensure rapid clinical translation.

Europe Facial Treatment Market Analysis

Europe commands a significant share of the global facial treatment market, with strong clinical standards and regulatory rigor underpinning its market status. Germany, France, and the United Kingdom lead in both service volume and technological adoption, supported by robust dermatology education systems. The EU Medical Device Regulation (MDR) has elevated safety standards for energy-based devices, ensuring only clinically validated products reach the market. Public health systems in Scandinavia cover laser therapy for severe acne, increasing accessibility. These factors, combined with rising demand for natural-looking results, position Europe as a mature yet evolving hub for evidence-based facial care.

Asia Pacific Facial Treatment Market Analysis

Asia Pacific holds a notable share of the global facial treatment market and is the most dynamic growth region due to cultural emphasis on skin clarity and youthfulness. South Korea leads with the highest per capita spending on facial treatments. Japan follows with a strong focus on preventive care. China’s private healthcare expansion has enabled rapid clinic proliferation. Local innovation in combination therapies and herbal-infused treatments further distinguishes the region’s market trajectory.

Latin America Facial Treatment Market Analysis

Latin America is also a key player in the global facial treatment market, as reported by the Pan American Society of Aesthetic Surgery in 2023, with Brazil and Mexico serving as primary growth engines. Brazil, in particular, has a deeply ingrained culture of aesthetic enhancement. The country’s universal health system does not cover cosmetic treatments, yet private spending remains robust. Mexico’s proximity to the U.S. has facilitated technology transfer. Additionally, social media influence is accelerating demand among younger demographics, with Instagram and TikTok driving awareness of treatments like radiofrequency and chemical peels. Despite economic volatility, the region’s aesthetic ambition sustains steady market expansion.

Middle East and Africa Facial Treatment Market Analysis

The Middle East and Africa collectively account for a small share of the global facial treatment market, with stark contrasts between sub-regions. Gulf Cooperation Council (GCC) nations, particularly the UAE and Saudi Arabia, are emerging as luxury aesthetic destinations, with Dubai attracting over 250,000 medical tourists in 2023 for skin rejuvenation, according to the Dubai Health Authority. In Saudi Arabia, Vision 2030 includes investments in private healthcare. Conversely, Sub-Saharan Africa faces significant access barriers; the World Health Organization estimates that most of the population lacks access to basic dermatological care. However, private clinics in South Africa, Kenya, and Nigeria are expanding, offering affordable LED and chemical peel treatments, signaling nascent but promising growth potential.

COMPETITIVE LANDSCAPE

The competition in the facial treatment market is intensifying as global medtech and cosmetic giants converge on a sector once dominated by independent clinics and spas. The landscape is now defined by technological superiority, clinical validation, and integrated care models that blend devices, biologics, and digital diagnostics. While multinational corporations leverage R&D scale and regulatory expertise, regional players are gaining ground by offering culturally attuned formulations and cost-effective delivery models. Differentiation hinges on precision targeting of regional skin concerns such as melasma, post-inflammatory hyperpigmentation, and pollution damage. Regulatory compliance, practitioner training, and outcome transparency have become critical competitive levers. Additionally, the rise of AI-powered consultations and at-home devices is blurring the line between professional and consumer markets, forcing companies to innovate beyond hardware into ecosystems of care. As consumer expectations shift toward personalized, data-backed results, the race is on to deliver safe, visible, and sustainable facial treatments across diverse global populations.

KEY MARKET PLAYERS

Some of the most promising companies leading the global facial treatment market profiled in this report are

- Lutronic Corporation

- Cutera Inc.

- Lynton Lasers Ltd.

- Sciton Inc.

- Alma Lasers Ltd

- Solta Medical Inc

- Lumenis Ltd.

- Cynosure Inc.

- Strata Skin Sciences Inc.

- Syneron Medical Ltd.

- Venus Concept Canada Corporation

- Fotona d.d.

Top Players in the Facial Treatment Market

L’Oréal Group (Through Dermatological Beauty Division: La Roche-Posay, CeraVe, SkinCeuticals)

L’Oréal has established a dominant presence in the Asia Pacific facial treatment market by integrating dermatological science with consumer accessibility. Through its SkinCeuticals brand, the company offers professional-grade antioxidant serums and chemical peels administered in over 2,500 dermatology clinics across China, Japan, and South Korea. The company also partnered with Apollo Hospitals in India to co-develop in-clinic facial protocols for urban consumers with pollution-induced skin damage. Additionally, L’Oréal’s acquisition of Modiface in 2018 continues to drive augmented reality consultations, now deployed in 600 premium clinics across the region. These initiatives reflect a strategic fusion of biotechnology, digital diagnostics, and clinical partnerships that reinforce its leadership in science-backed facial care.

Cutera, Inc.

Cutera has significantly expanded its footprint in the Asia Pacific facial treatment market by introducing medical-grade energy-based devices tailored for diverse skin types and regional dermatological concerns. The company’s Excel HR laser and Joule platform are widely used in clinics across Australia, South Korea, and Thailand for pigmentation correction and skin resurfacing. It also initiated clinical training programs in Malaysia and Indonesia in collaboration with local dermatological societies to ensure safe and effective device utilization. Cutera’s ProWave IPL system has been adopted in over 400 clinics in India, addressing high demand for melasma treatment. The company’s focus on compact, user-friendly systems with adjustable parameters for Fitzpatrick skin types III–VI has strengthened its relevance in a region with wide ethnic and phototype diversity.

Candela Medical (A Solta Medical Company)

Candela Medical has solidified its influence in the Asia Pacific facial treatment landscape through advanced laser technologies and strong clinical engagement. Its Vbeam pulsed dye laser, renowned for treating vascular lesions and rosacea, is a staple in premium dermatology centers across Taiwan, Thailand, and Australia. The company also launched the GentleMax Pro laser in China, combining Alexandrite and Nd: YAG wavelengths to safely treat a broad range of skin tones. Candela’s partnership with the Thai Dermatological Association enabled the rollout of certified training modules for laser safety, enhancing practitioner confidence. Additionally, its participation in regional medical conferences such as the Asia-Pacific Dermatologic Surgery Congress has amplified brand visibility and clinical trust, positioning Candela as a leader in high-precision, evidence-based facial interventions.

RECENT HAPPENINGS IN THE MARKET

- In January 2024, L’Oréal launched its AI-powered Skin Genius diagnostic platform in Hong Kong, enabling real-time facial skin analysis in premium clinics and enhancing treatment personalization across urban Asia in the Facial Treatment Market.

- In March 2023, Cutera received PMDA approval for its Secret RF microneedling device in Japan, expanding its portfolio of minimally invasive facial treatments for acne scars and aging skin in the Facial Treatment Market.

- In August 2023, Candela Medical initiated a certified training program with the Thai Dermatological Association, equipping over 300 clinicians with laser safety and application protocols to strengthen clinical adoption in the Facial Treatment Market.

- In May 2024, Solta Medical opened a regional innovation center in Seoul, focused on developing energy-based facial devices optimized for East Asian skin types and accelerating product localization in the Facial Treatment Market.

- In February 2024, Amorepacific partnered with a Seoul-based biotech firm to launch a clinical-grade fermented serum line for use in medical spa facial treatments, integrating K-beauty innovation with dermatological efficacy in the Facial Treatment Market.

MARKET SEGMENTATION

This research report on the global facial treatment market has been segmented and sub-segmented based on the product type, end-user, and region.

By Product Type

- IPL Devices

- RF Devices

- Ultrasound Devices

- LED Devices

- Laser-Based Devices

By End User

- Dermatology Clinics

- Beauty Clinics

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa