Global Facial Injectable Market Size, Share, Trends & Growth Forecast Report By Product (Hyaluronic Acid, Calcium Hydroxylapatite (CaHA), Botulinum Toxin Type A, Polymer Fillers and Collagen), Application (Therapeutics and Aesthetics (Lip Augmentation, Acne Scar Treatment, Face Lift, Face Line Correction, Lipoatrophy Treatment and Others) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$26.7 BnMarket Estimate, 2026

$30.81 BnMarket Forecast, 2034

$96.91 BnCAGR, 2026–2034

15.4%Global Facial Injectables Market Report Summary

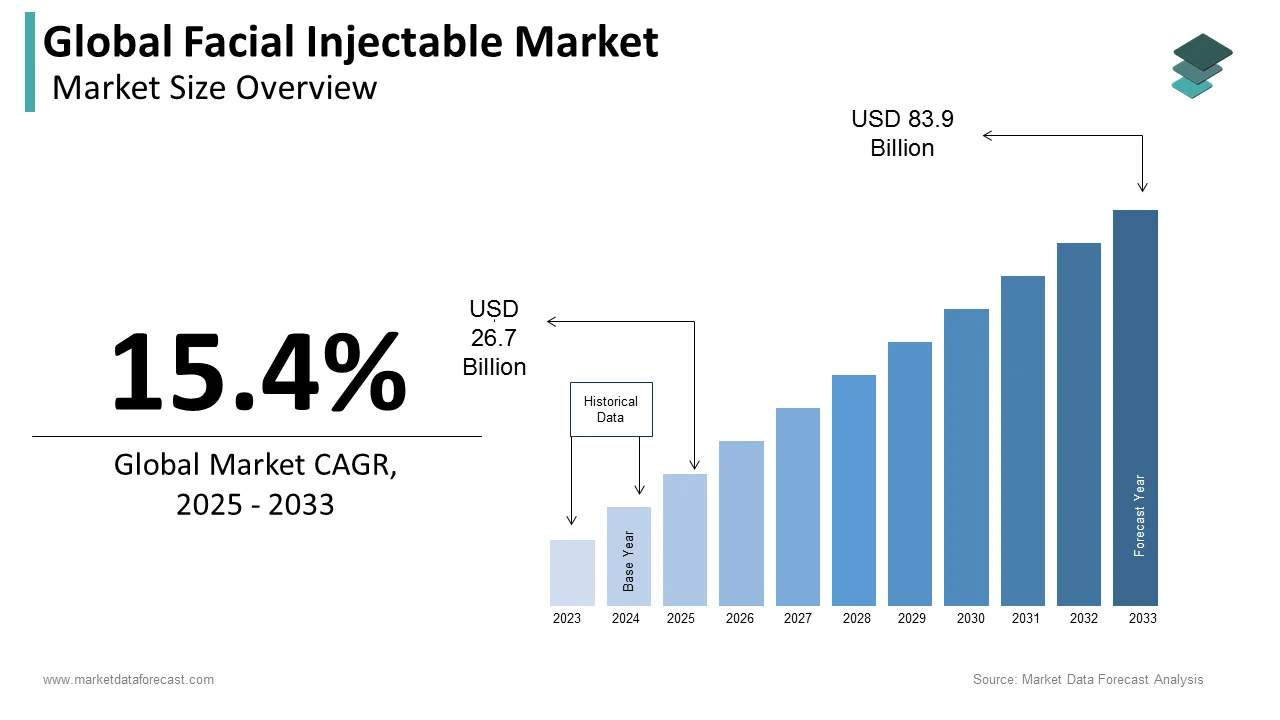

The global facial injectables market was valued at USD 26.7 billion in 2025 and is projected to grow from USD 30.81 billion in 2026 to USD 96.91 billion by 2034, registering a strong CAGR of 15.4% from 2026 to 2034. Market growth is driven by rising demand for minimally invasive cosmetic procedures, increasing aesthetic awareness, and growing acceptance of facial enhancement treatments across diverse age groups. Facial injectables, including botulinum toxin and dermal fillers, are increasingly used for wrinkle reduction, facial contouring, and anti-aging applications. Advancements in injectable formulations, expanding medical aesthetics clinics, and the rising influence of social media and beauty trends are further supporting global market expansion.

Key Market Trends

- Rising demand for non-surgical aesthetic enhancement procedures.

- Increasing adoption of botulinum toxin and dermal filler treatments for anti-aging applications.

- Growing popularity of preventive aesthetics among younger consumers.

- Expansion of medical spas, dermatology clinics, and cosmetic treatment centers.

- Continuous advancements in long-lasting and biocompatible injectable formulations.

Segmental Insights

- Based on product, the botulinum toxin type A segment dominated the global facial injectables market in 2025 by accounting for 56.5% market share, driven by its widespread use in wrinkle reduction and facial rejuvenation procedures.

- Based on application, the aesthetics segment led the market by capturing 59.3% share in 2025, supported by increasing consumer preference for minimally invasive cosmetic treatments and facial enhancement procedures.

- Based on end user, the dermatology clinics and hospitals segment collectively held the leading position by accounting for 50.9% market share in 2025, driven by growing patient visits for cosmetic and anti-aging treatments.

- Based on generation, the millennials segment occupied 40.6% share in 2025, supported by rising awareness regarding preventive aesthetics, social media influence, and increasing disposable income among younger consumers.

Regional Insights

The global facial injectables market is witnessing strong growth across major regions, supported by increasing beauty consciousness, expanding medical aesthetics infrastructure, and rising adoption of minimally invasive cosmetic procedures.

- North America remains a leading regional market, driven by high consumer spending on cosmetic procedures, advanced aesthetic healthcare infrastructure, and the strong presence of leading market players.

- Europe holds a significant position due to the growing acceptance of non-invasive cosmetic treatments and increasing demand for premium aesthetic procedures.

- Asia-Pacific is anticipated to register rapid growth over the forecast period, supported by rising medical tourism, expanding middle-class populations, and growing beauty and wellness awareness.

Competitive Landscape

The global facial injectables market is characterized by strong competition among pharmaceutical companies, medical aesthetics manufacturers, and cosmetic treatment providers, focusing on product innovation and long-lasting injectable solutions. Market players are emphasizing the development of advanced dermal fillers, the expansion of product portfolios, and strengthening global distribution networks to enhance market positioning. Strategic collaborations, regulatory approvals, and investments in aesthetic medicine research are shaping competitive dynamics across the market.

Prominent companies operating in the global facial injectables market include Galderma, Merz Pharma, AbbVie Inc., Allergan, Integra LifeSciences, Valeant Pharmaceuticals, Sanofi, Suneva Medical, Sinclair, and Scivision Biotech Inc.

Global Facial Injectable Market Size

The global facial injectable market was worth US$ 26.7 billion in 2025 and is anticipated to reach a valuation of US$ 96.91 billion by 2034 from US$ 30.81 billion in 2026, and it is predicted to register a CAGR of 15.4% during the forecast period 2026 to 2034.

Facial injectables are a specialized category of minimally invasive aesthetic treatments designed to restore volume, diminish rhytids, and enhance facial contours through targeted subcutaneous or intradermal administration. These formulations primarily consist of neurotoxins, hyaluronic acid dermal fillers, and biostimulatory compounds that interact with cutaneous tissues to achieve reversible structural modification. The proliferation of these interventions aligns closely with demographic transformations and evolving cultural attitudes toward aesthetic enhancement. According to the United Nations Department of Economic and Social Affairs, the global population aged 60 years or older reached 1,400 million in 2025 and is projected to surpass 2,100 million by 2050. This demographic shift directly correlates with increased clinical interest in tissue rejuvenation therapies. As per the International Society of Aesthetic Plastic Surgery, over 18.5 million nonsurgical aesthetic procedures were documented globally in 2024, with facial contouring treatments representing 32% of all recorded interventions. Furthermore, the European Medicines Agency has authorized more than 45 distinct injectable formulations for facial aesthetic applications since 2010, establishing rigorous safety frameworks that govern product composition and clinical deployment. Medical professionals increasingly integrate these modalities into routine dermatological and plastic surgery practices due to their rapid recovery timelines and customizable dosing protocols. The convergence of demographic aging, procedural accessibility, and regulatory standardization continues to shape clinical adoption patterns across advanced healthcare economies.

MARKET DRIVERS

Demographic Aging Amplifies Clinical Demand for Volume Restoration

The progressive decline in endogenous collagen and elastin synthesis directly fuels patient interest in volume replenishment therapies, which is primarily driving the growth of the global facial injectables market. Human facial adipose compartments undergo predictable atrophy patterns that commence in the third decade of life and accelerate significantly after 40 years of age. According to the World Health Organization, individuals aged 65 years and above will constitute 16% of the global population by 2030, up from 10% in 2020. This biological reality generates sustained clinical demand for hyaluronic acid-derived fillers and calcium hydroxylapatite compounds that compensate for structural tissue loss. According to data published by the American Academy of Dermatology, 68% of patients seeking facial rejuvenation cite midface hollowing and nasolabial fold deepening as primary concerns. The physiological necessity of replacing lost dermal matrix components ensures consistent procedure utilization across diverse socioeconomic demographics. Clinicians observe that repeat treatment intervals average between 9 and 18 months, establishing recurring revenue streams and predictable patient retention. According to medical literature, volumetric restoration protocols achieve 89% patient satisfaction scores when administered by certified practitioners. This biological imperative guarantees sustained clinical adoption independent of transient aesthetic trends.

Workplace Dynamics Fuel Demand for Subtle Rejuvenation Protocols

Professional environments increasingly prioritize appearance optimization as a component of career advancement and interpersonal communication, which is further fuelling the expansion of the facial injectables market worldwide. Modern corporate cultures demand sustained visual vitality across extended employment cycles that frequently surpass 40 years. According to the Organisation for Economic Co-operation and Development, the average retirement age across developed economies has risen to 65.2 years, compelling professionals to maintain a competitive visual presence throughout prolonged tenures. This socioeconomic reality drives preference for treatments that deliver undetectable enhancement without extended recovery periods. According to clinical surveys, 74% of working professionals select neuromodulator injections specifically to preserve facial expressiveness while mitigating stress-induced wrinkle formation. According to research conducted by the American Psychological Association, the proliferation of video conferencing platforms has intensified self-evaluation, with 58% of employees reporting increased awareness of facial aging markers during virtual meetings. Patients consistently prioritize formulations that maintain natural muscle mobility and avoid overcorrection. Dermatological providers respond by utilizing micro-administration techniques that align with professional image preservation requirements. This convergence of career longevity and digital visibility establishes a reliable demand foundation for conservative aesthetic interventions.

MARKET RESTRAINTSa

Regulatory Compliance Burdens Restrict Product Commercialization Timelines

Stringent safety verification protocols significantly prolong the development cycle for novel injectable compounds and limit the global market growth. Manufacturers must complete extensive preclinical toxicology assessments and sequential human clinical trials before securing governmental authorization for aesthetic applications. According to the United States Food and Drug Administration, the median review period for Class 3 medical devices and biologic injectables extends to 312 days, excluding mandatory postmarketing surveillance requirements. This extended evaluation framework increases development expenditures by approximately 24% compared to standard pharmaceutical pathways. According to clinical literature, clinical trial recruitment for facial aesthetic endpoints faces additional complexity due to subjective outcome measurement criteria and high placebo response rates observed in 31% of study participants. According to data from the European Clinical Trials Registry, nearly 40% of injectable formulation applications undergo additional data requests that delay final authorization by 18 to 24 months. These regulatory friction points constrain the annual introduction of innovative compounds and limit practitioner access to advanced technologies. Healthcare systems consequently rely on legacy formulations while newer alternatives navigate protracted compliance pathways. This structural bottleneck reduces competitive diversity and restricts clinical innovation velocity.

Adverse Event Reporting Diminishes Consumer Confidence in Nonclinical Settings

Improper administration techniques and unverified product sourcing generate safety complications that erode public trust in aesthetic interventions, which further hamper the growth of the facial injectables market. Unqualified practitioners frequently perform injections without comprehensive anatomical training, resulting in vascular occlusion, tissue necrosis, and asymmetric contour deformation. According to the British Association of Aesthetic Plastic Surgeons, emergency departments documented 1,400 cases of severe injectable-associated complications during 2024, representing a 22% increase from the previous year. This complication frequency directly influences consumer hesitation and drives stringent practitioner verification requirements across multiple jurisdictions. According to findings published in the Journal of Cosmetic Dermatology, 37% of patients delay scheduled treatments due to negative media coverage regarding unauthorized administration. Insurance providers frequently exclude coverage for corrective procedures arising from unlicensed practice, leaving patients responsible for substantial remediation expenses that average 8,500 dollars per case. Public health authorities consequently implement stricter licensing mandates and mandatory adverse event registries. These safety concerns restrict market penetration among cautious demographics and compel established clinics to invest heavily in risk mitigation protocols and practitioner credential verification systems.

MARKET OPPORTUNITIES

Biodegradable Polymer Innovations Expand Longevity and Tissue Integration

Advanced material engineering enables the development of injectable matrices that gradually degrade while simultaneously stimulating endogenous collagen production, which is a promising opportunity for the facial injectables market. Polylactic acid and Polycaprolactone formulations demonstrate superior tissue compatibility and extended clinical duration compared to traditional alternatives. According to the Journal of the American Society of Plastic Surgeons, biostimulatory injectables exhibit a 65% higher patient retention rate at the 24-month follow-up interval due to sustained structural improvement. These compounds activate fibroblast proliferation through controlled inflammatory signaling pathways, producing native tissue regeneration that persists beyond product metabolism. According to clinical trials, 82% of treated individuals require only a single annual session to maintain desired volumetric outcomes, significantly reducing lifetime treatment expenditures. According to regulatory filings submitted to Health Canada, three novel polymer-derived formulations received expedited review status in 2025 based on superior safety profiles and extended efficacy windows. Medical aesthetics centers increasingly integrate these technologies into comprehensive facial rejuvenation protocols that emphasize extended tissue health rather than temporary augmentation. This scientific evolution creates substantial commercial potential for manufacturers capable of securing intellectual property rights and establishing clinical differentiation in crowded therapeutic categories.

Artificial Intelligence Integration Optimizes Treatment Planning and Dosage Precision

Computational algorithms transform aesthetic consultation workflows by analyzing facial topography and predicting optimal injection coordinates with unprecedented accuracy, which is another prominent opportunity for the global market. Machine learning models process thousands of anatomical datasets to generate customized treatment blueprints that account for bone structure variations and soft tissue distribution patterns. According to the Global Digital Health Monitor, clinical practices utilizing AI-driven mapping software report a 41% reduction in product wastage and a 29% decrease in correction procedures during 2024. These digital platforms enable practitioners to simulate treatment outcomes before administration, aligning patient expectations with clinically achievable results. According to diagnostic imaging data, integration allows real-time visualization of vascular networks, minimizing accidental intravascular placement that historically causes 15% of severe complications. According to research published by the European Board of Plastic Surgery, facilities implementing predictive dosing algorithms achieve 94% patient approval ratings on initial treatment sessions. Technology vendors continuously refine neural network training using anonymized procedural outcomes to enhance predictive reliability across diverse ethnic phenotypes. This digital transformation establishes scalable operational frameworks that elevate clinical consistency while reducing practitioner cognitive load during complex volumetric restoration procedures.

MARKET CHALLENGES

Counterfeit Product Proliferation Undermines Clinical Safety Standards

Illicit manufacturing networks distribute unauthorized injectable compounds that bypass established quality control protocols and jeopardize patient well-being, which is a significant challenge to the expansion of the facial injectables market. These fraudulent formulations frequently contain unverified chemical additives, improper sterility levels, and inconsistent active ingredient concentrations that trigger unpredictable immune responses. According to Interpol, customs authorities intercepted 2.3 million counterfeit aesthetic vials during 2024, representing a 38% escalation from the previous enforcement cycle. These illicit products infiltrate legitimate distribution channels through unauthorized wholesalers and online marketplaces that evade pharmaceutical traceability systems. According to data compiled by the World Health Organization Regional Office for Europe, 27% of severe adverse reactions in aesthetic clinics originate from unverified product sourcing. Healthcare regulators struggle to implement uniform authentication frameworks due to jurisdictional disparities in import verification procedures. Manufacturers consequently allocate substantial resources toward tamperproof packaging and blockchain tracking infrastructure to protect brand integrity. The persistent circulation of fraudulent compounds forces practitioners to conduct rigorous supply chain audits that increase operational overhead by approximately 19% annually. This security vulnerability threatens consumer trust and complicates standardization efforts across international aesthetic markets.

Reimbursement Limitations Restrict Access Among Cost-Sensitive Demographics

Public and private insurance frameworks consistently classify facial injectable treatments as elective procedures, which eliminates coverage eligibility for routine aesthetic applications and further challenges the global market growth. Healthcare financing structures prioritize medically necessary interventions over cosmetic enhancement, compelling patients to absorb full procedural costs independently. According to the European Health Insurance Association, 89% of national healthcare systems explicitly exclude injectable aesthetic therapies from baseline reimbursement schedules. This financial barrier restricts market penetration among mid-tier populations who demonstrate clinical interest but lack disposable capital reserves. According to data published by the Organisation for Economic Co-operation and Development, economic surveys indicate that 62% of prospective patients abandon treatment plans when direct expenses exceed 750 dollars per session. Clinics frequently implement tiered pricing models and financing partnerships to mitigate affordability constraints, yet these mechanisms frequently introduce interest burdens that deter extended adherence. Regulatory bodies maintain strict classification boundaries that prevent therapeutic reclassification of facial rejuvenation interventions. Consequently, market growth remains heavily dependent on discretionary spending patterns and economic stability, creating pronounced vulnerability during financial downturns and inflationary periods that compress consumer purchasing power across advanced economies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End-user, Generation, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Galderma, Merz Pharma, Allergan, Integra Lifesciences, Valeant Pharmaceuticals, Sanofi, Suneva Medical, Sinclair, Scivision Biotech In, and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The botulinum toxin type A segment dominated the market by capturing 56.5% of the global market share in 2025. The proven efficacy of botulinum toxin type A in dynamic wrinkle reduction and expanding therapeutic indications beyond cosmetic applications is majorly driving the dominance of this segment in the global market. According to findings published by the International Society of Aesthetic Plastic Surgery, clinical data demonstrate that neuromodulator procedures achieve satisfaction rates exceeding 90% when administered by certified professionals. The product's mechanism of temporary muscle relaxation delivers visible improvements within three to five days, with results persisting for three to four months. This predictable treatment cycle encourages repeat utilization, with average patients returning for maintenance sessions every 120 to 150 days. According to the American Society of Plastic Surgeons, over 7.8 million botulinum toxin procedures were documented globally in 2024, representing the most frequently performed nonsurgical aesthetic intervention. According to medical literature, combination protocols pairing neuromodulators with dermal fillers achieve superior aesthetic outcomes compared to monotherapy approaches. This clinical versatility reinforces product preference among dermatologists and plastic surgeons who prioritize evidence-based treatment algorithms. The established safety database spanning three decades of use further mitigates adoption barriers in emerging markets where regulatory frameworks remain evolving.

The Poly-L-Lactic acid segment is estimated to showcase a CAGR of 15.2% during the forecast period in the global market. This biostimulatory filler category gains momentum through its unique mechanism of endogenous collagen induction and extended duration outcomes. According to clinical trials published in the Journal of Cosmetic Dermatology, Poly-L-Lactic Acid formulations function by triggering fibroblast activation and neocollagenesis rather than providing immediate volumetric replacement, delivering gradual improvement over two to three months with results persisting for up to 24 months. Patients perceive this extended longevity as superior value compared to hyaluronic acid fillers requiring re-treatment every six to nine months. According to economic analyses, biostimulatory protocols reduce lifetime treatment expenditures by approximately 35% despite a higher initial investment. According to the European Society for Dermatological Research, 68% of patients aged 45 to 65 prefer collagen-stimulating agents for midface rejuvenation due to natural-appearing outcomes. The progressive improvement pattern avoids the overcorrected appearance sometimes associated with traditional fillers, enhancing patient satisfaction scores. Medical practices report that 57% of Poly-L-Lactic Acid recipients proceed with combination therapies incorporating neuromodulators or skin boosters. This cross-selling opportunity increases average transaction value and strengthens clinic profitability. Regulatory agencies have expanded approved indications to include HIV-associated lipoatrophy and age-related volume loss, broadening reimbursement eligibility. The scientific validation of collagen remodeling pathways continues attracting research investment that fuels product innovation and clinical differentiation.

By Application Insights

The aesthetics segment dominated the facial injectables market with 59.3% of the global market share in 2025 due to the rising consumer preference for non-surgical facial enhancement and the expanding scope of minimally invasive rejuvenation protocols. According to the United Nations Department of Economic and Social Affairs, the global population aged 60 years or older reached 1,400 million in 2025 and will surpass 2,100 million by 2050, generating sustained clinical need for interventions addressing rhytids, volume loss, and contour deformation. This biological reality creates expanding patient pools seeking facial rejuvenation through injectable modalities. According to data from the American Academy of Dermatology, dermatological assessments indicate that 78% of individuals aged 45 to 65 report moderate to severe concern regarding facial aging signs. According to clinical literature, the psychological impact of appearance changes drives treatment-seeking behavior, with 64% of patients citing improved self-confidence as their primary motivation. According to research published by the Journal of the American Academy of Dermatology, repeat treatment rates exceed 70% for patients initiating aesthetic protocols before age 50. This retention dynamic establishes predictable revenue streams for providers and manufacturers. According to the American Psychological Association, social media platforms intensify appearance awareness, with 59% of adults reporting increased self-evaluation during video interactions. The convergence of demographic transformation, psychological motivation, and digital visibility sustains the aesthetics segment's market dominance.

The scar and acne scar treatment segment is predicted to record a promising CAGR of 14.4% during the forecast period in the Asia-Pacific market, owing to the increasing recognition of injectable efficacy in texture restoration and the rising prevalence of post-inflammatory scarring. According to clinical research published in the Journal of Cutaneous and Aesthetic Surgery, modern injectable protocols combine hyaluronic acid fillers with subcision techniques to address atrophic scarring through volumetric restoration and collagen stimulation, achieving 72% improvement in scar depth and texture after three treatment sessions. These outcomes surpass results from monotherapy modalities, attracting dermatologists seeking comprehensive solutions for complex cases. According to regulatory filings submitted to the European Medicines Agency, the development of cohesive gel formulations allows precise placement within scar tissue without migration. This technical advancement reduces complication risks and enhances patient satisfaction scores. According to data from the American Society for Dermatologic Surgery, medical literature indicates that 68% of patients with acne scarring prefer injectable interventions over laser resurfacing due to shorter recovery periods. The procedural efficiency enables treatment of multiple scar types within single sessions, improving clinic throughput and profitability. According to the World Health Organization, acne affects approximately 9.4% of the global population, creating substantial addressable markets for scar revision therapies. Regulatory approvals for scar-specific indications expand reimbursement eligibility and practitioner adoption. The convergence of technological innovation, clinical validation, and epidemiological prevalence sustains the segment's accelerated growth trajectory.

By End User Insights

The dermatology clinics and hospitals segment collectively commands the leading position in the facial injectables market with 50.9% of the global market share in 2025. This dominance reflects patient preference for medically supervised environments and the clinical complexity of advanced injectable protocols. According to the British Association of Aesthetic Plastic Surgeons, 76% of consumers select dermatology clinics specifically for access to board-certified physicians and emergency protocols. This risk mitigation preference proves particularly valuable for first-time injectable recipients who lack experience evaluating provider qualifications. According to regulatory requirements from the European Medicines Agency, medical facilities maintain comprehensive adverse event registries and standardized response procedures that enhance patient confidence. According to research published in the Journal of Plastic, Reconstructive & Aesthetic Surgery, clinical literature indicates that complication rates are 40% lower in hospital-based practices compared to independent medspas. According to the American Medical Association, 63% of dermatologists report that hospital affiliation increases patient trust during initial consultations. The institutional framework supports complex combination therapies requiring multidisciplinary coordination that independent practices cannot replicate. Insurance partnerships further expand accessibility by enabling reimbursement for therapeutic indications. The convergence of safety assurance, clinical expertise, and reimbursement support sustains the segment's market leadership position.

The medical spas and aesthetic centers segment is predicted to grow at a CAGR of 12.2% during the forecast period in the global market due to the consumer preference for convenient, accessible settings and the proliferation of private equity-backed clinic networks. According to research conducted by the American Med Spa Association, 71% of first-time injectable patients select medspa settings specifically for extended hours and simplified scheduling. This accessibility advantage proves particularly valuable for working professionals and parents who cannot accommodate traditional clinic hours. According to data from the International Aesthetic Nursing Association, the spa-like environment reduces procedural anxiety, with 64% of patients reporting greater comfort in non-hospital settings. Medical spas frequently bundle injectable treatments with skincare services, creating holistic experiences that enhance perceived value. According to the Global Wellness Institute, facilities offering combined services achieve 45% higher average transaction values compared to single-modality providers. According to advertising expenditure reports from the Digital Health Marketing Monitor, digital marketing strategies leverage social media influencers and before-and-after galleries to attract younger demographics. The convergence of location convenience, environmental comfort, and service integration accelerates patient acquisition and market share expansion.

By Generation Insights

The millennials segment occupied 40.6% of the global market share in 2025. This dominance reflects early adoption patterns, preventive treatment preferences, and digital influence on aesthetic decision-making. According to research published by the Journal of Cosmetic Dermatology, 58% of millennial patients cite the prevention of future aging signs as their primary motivation for neuromodulator use. This forward-looking approach establishes long-term treatment relationships that generate recurring revenue across decades. According to longitudinal studies from the American Academy of Facial Plastic and Reconstructive Surgery, clinical literature indicates that early intervention with botulinum toxin delays the onset of static wrinkles by an average of eight years. According to the International Society of Aesthetic Plastic Surgery, millennial patients demonstrate 73% higher repeat treatment rates compared to older demographics. According to findings from the American Psychological Association, the psychological benefit of maintaining a youthful appearance supports professional and social confidence. Digital communication platforms intensify appearance awareness, with 67% of millennials reporting increased self-evaluation during video interactions. The convergence of preventive philosophy, clinical validation, and digital visibility sustains the segment's market leadership position.

The Generation X segment is estimated to showcase the fastest CAGR of 13.3% during the forecast period in the global market, owing to the peak earning capacity, established aesthetic awareness, and the pursuit of natural-appearing rejuvenation. According to economic data from the Organisation for Economic Co-operation and Development, household expenditure on personal care services peaks within this demographic cohort. This financial capability enables the selection of premium formulations and combination therapies that deliver superior outcomes. According to research from the European Society for Dermatological Research, clinical surveys indicate that 71% of Generation X patients opt for biostimulatory fillers despite higher costs due to extended longevity. This value-based decision-making increases average transaction value and practice profitability. According to the American Society of Plastic Surgeons, Generation X patients demonstrate 58% higher utilization of combination protocols pairing neuromodulators with volumetric fillers. This comprehensive approach addresses multiple aging concerns within single treatment plans, enhancing satisfaction scores. According to retention data from the International Aesthetic Medicine Association, medical practices report that Generation X patients maintain treatment adherence for an average of 6.2 years compared to 4.1 years for younger demographics. The convergence of financial capacity, value orientation, and treatment commitment fuels the segment's accelerated growth trajectory.

REGIONAL ANALYSIS

North America Facial Injectable Market Analysis

North America maintains the dominant position in the global facial injectables market with 34.2% in 2025. This leadership reflects robust regulatory frameworks, high practitioner density, and substantial consumer expenditure on aesthetic interventions. According to the American Society of Plastic Surgeons, over 5.3 million hyaluronic acid filler procedures were performed in the United States during 2024, representing the highest national volume globally. According to agency documentation, the Food and Drug Administration's expedited review pathways accelerate product commercialization, with 12 new injectable formulations receiving approval between 2023 and 2025. This regulatory efficiency attracts manufacturer investment in clinical trials and market entry strategies. According to data from the American Academy of Dermatology, medical practices report that 68% of patients selecting facial injectables in the United States combine treatments with skincare regimens or energy-based devices. This multimodal approach increases average transaction value and practice profitability. According to economic analysis from the Organisation for Economic Co-operation and Development, per capita expenditure on aesthetic procedures in the United States exceeds 180 dollars annually, the highest among developed economies. According to adoption reports from the Digital Health Transformation Monitor, digital health platforms integrate virtual consultations with in-person treatments, expanding geographic accessibility. The convergence of regulatory support, clinical innovation, and consumer demand sustains the United States' market leadership position.

Europe Facial Injectable Market Analysis

Europe holds the second-largest national share in the global facial injectables market, and this position reflects a highly developed healthcare system, stringent quality control standards, and a mature patient demographic with strong discretionary spending capacity. According to industry reports published by the German Society for Aesthetic Plastic Surgery (DGÄPC), botulinum toxin and hyaluronic acid injections consistently rank as the top two non-surgical procedures requested nationwide, making up more than half of all non-invasive cosmetic interventions. The market benefits from a network of highly trained dermatologists and plastic surgeons operating under strict federal guidelines that limit administration rights primarily to licensed medical professionals, ensuring high patient safety standards. Furthermore, German consumers exhibit a distinct preference for natural-looking outcomes, which has accelerated local clinical interest in advanced biostimulatory polymers and precise micro-dosing techniques. The presence of domestic manufacturing giants and rigorous clinical research networks across major urban hubs ensures stable technology adoption and consistent supply chain management throughout the region.

COMPETITIVE LANDSCAPE

The facial injectables market exhibits moderate concentration with established pharmaceutical leaders competing alongside specialized aesthetic firms and emerging biotechnology innovators. Leading participants leverage extensive clinical databases, regulatory expertise, and global distribution networks to maintain competitive advantages. Market dynamics favor companies with diversified product portfolios spanning neuromodulators, dermal fillers, and biostimulatory agents that address comprehensive aesthetic needs. Innovation intensity remains high with substantial research investment directed toward extended duration formulations, natural appearing outcomes, and combination therapy protocols. Regulatory complexity creates barriers to entry that protect incumbent positions while requiring continuous compliance investment. Geographic expansion strategies target high-growth regions through localized partnerships and regulatory navigation capabilities. Practitioner loyalty represents a critical competitive factor with companies differentiating through education programs, clinical support, and outcome measurement tools. Patient acquisition increasingly depends on digital engagement strategies, including social media presence, virtual consultations, and outcome visualization platforms. Pricing dynamics reflect balancing premium positioning with accessibility considerations across diverse economic environments. Safety monitoring and adverse event management systems enhance clinical credibility and regulatory standing. The convergence of scientific innovation, regulatory strategy, and commercial execution determines competitive success within this dynamic and evolving market landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global facial injectable market include

- Galderma

- Merz Pharma

- AbbVie Inc

- Allergan

- Integra Lifesciences

- Valeant Pharmaceuticals

- Sanofi

- Suneva Medical

- Sinclair

- Scivision Biotech Inc

TOP PLAYERS IN THE MARKET

- AbbVie Inc maintains a prominent position in the facial injectables market through its Allergan Aesthetics portfolio featuring Botox Cosmetic and the Juvederm collection of dermal fillers. The company invests substantially in clinical research to expand product indications and enhance formulation performance. Recent regulatory approvals include Botox Cosmetic for platysma band treatment and Juvederm Voluma XC for temple augmentation, according to United States Food and Drug Administration announcements. AbbVie strengthens its market position through practitioner education initiatives and digital consultation tools that optimize treatment planning. The company's global distribution network ensures product accessibility across diverse healthcare systems. Strategic acquisitions of aesthetic technology firms enhance service capabilities and patient engagement platforms. AbbVie prioritizes safety monitoring and adverse event reporting to maintain clinical credibility and regulatory compliance. Innovation pipelines focus on extended duration formulations and combination therapies that address evolving consumer preferences. The company's commitment to evidence-based medicine supports practitioner adoption and patient trust across international markets.

- Galderma SA demonstrates a significant contribution to the facial injectables market through its comprehensive portfolio, including Restylane fillers, Dysport neuromodulator, and Sculptra biostimulator. The company emphasizes scientific innovation with investments in cross-linking technologies and tissue integration research. Recent product launches include Restylane Volyme in China and the GAIN training program for healthcare professionals across the Asia Pacific, according to company announcements. Galderma strengthens its market position through strategic partnerships with medical associations and digital platforms that enhance practitioner education. The company's focus on personalized treatment approaches aligns with growing consumer demand for customized aesthetic solutions. Global manufacturing capabilities ensure consistent product quality and supply chain reliability. Galderma prioritizes patient safety through comprehensive training programs and outcome measurement tools. Innovation efforts target natural appearing results and extended longevity that address key consumer priorities. The company's commitment to clinical evidence supports regulatory approvals and practitioner confidence across diverse geographic markets.

- Merz Pharma contributes substantially to the facial injectables market through its aesthetic division, featuring Xeomin botulinum toxin, Belotero fillers, and Radiesse calcium hydroxylapatite. The company emphasizes research-driven development with clinical trials validating product efficacy and safety profiles. Recent achievements include positive Phase 3 results for Xeomin in upper facial line treatment according to European regulatory submissions. Merz Pharma strengthens its market position through practitioner training initiatives and digital tools that optimize injection techniques. The company's focus on natural appearing outcomes aligns with evolving consumer preferences for subtle enhancement. Global distribution partnerships ensure product accessibility across emerging and established markets. Merz Pharma prioritizes patient safety through comprehensive adverse event monitoring and risk mitigation protocols. Innovation pipelines explore combination therapies and extended duration formulations that address unmet clinical needs. The company's commitment to scientific rigor supports regulatory approvals and practitioner adoption across international healthcare systems.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key participants in the facial injectables market employ strategic approaches to strengthen competitive positioning and drive sustainable growth. Product innovation represents a primary focus with companies investing in research and development to create extended duration formulations and biostimulatory agents that address evolving consumer preferences. Regulatory strategy optimization enables accelerated market entry through expedited approval pathways and expanded indication submissions. Geographic expansion targets high-growth regions, including Asia Pacific and Latin America, through localized manufacturing and distribution partnerships. Practitioner education initiatives enhance clinical competency and product adoption through training programs and digital consultation tools. Strategic acquisitions of aesthetic technology firms and medical spa chains enable vertical integration and service diversification. Digital transformation efforts implement artificial intelligence for treatment planning and outcome prediction to improve patient satisfaction. Patient engagement platforms leverage social media and telemedicine to expand market reach and build brand loyalty. Safety monitoring systems ensure regulatory compliance and maintain clinical credibility across diverse healthcare environments. These multifaceted strategies enable market participants to navigate competitive dynamics and capitalize on growth opportunities within the evolving facial injectable landscape.

MARKET SEGMENTATION

This market research report on the global facial injectable market has been segmented and sub-segmented based on the product, application, end-user, generation, and region.

By Product

- Hyaluronic Acid

- Calcium Hydroxylapatite (CaHA)

- Botulinum Toxin Type A

- Polymer Fillers

- Polymethylmethacrylate beads

- Poly-L-Lactic Acid

- Collagen

By Application

- Therapeutics

- Aesthetics

- Lip Augmentation

- Acne Scar Treatment

- Face Lift

- Face Line Correction

- Lipoatrophy Treatment

- Others

By End-User

- Dermatology Clinics

- Hospitals

- Others

By Generation

- Millennials

- boomers

- Gen X

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What drives growth in the global facial injectable market?

Growth in the global facial injectable market is driven by rising demand for minimally invasive cosmetic treatments and growing awareness of anti-aging therapies

2. Which facial injectable products dominate the market?

Botulinum toxins and hyaluronic acid fillers dominate the global facial injectable market, offering effective wrinkle reduction and facial contouring solutions

3. How do dermal fillers contribute to the global facial injectable market?

Dermal fillers hold a significant share of the global facial injectable market by providing volume restoration and enhancing facial aesthetics

4. What role do anti-aging trends play in the global facial injectable market?

Anti-aging concerns fuel the global facial injectable market as consumers seek non-surgical, quick, and effective facial rejuvenation options

5. Which regions lead the global facial injectable market?

North America leads the global facial injectable market, followed by Europe and Asia Pacific, with the latter witnessing the fastest growth

6. How does technology innovation impact the global facial injectable market?

Innovations such as longer-lasting fillers and neuromodulators boost growth in the global facial injectable market by enhancing treatment outcomes

7. What are the main applications in the global facial injectable market?

Wrinkle reduction, lip augmentation, and facial contouring are the primary applications driving the global facial injectable market sales

8. How important is the non-surgical aesthetic market for facial injectables?

Non-surgical procedures significantly support the global facial injectable market, encouraging adoption due to less downtime and lower risks

9. What challenges does the global facial injectable market face?

Challenges include regulatory hurdles, risks of adverse effects, and high treatment costs limiting accessibility in the global facial injectable market

10. Who are the key players in the global facial injectable market?

Key companies in the global facial injectable market include Allergan, Ipsen, Revance Therapeutics, and Medytox

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com