Europe Feed Flavors And Sweeteners Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Livestock, Type And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis 2025 to 2033

Europe Feed Flavors and Sweeteners Market Size

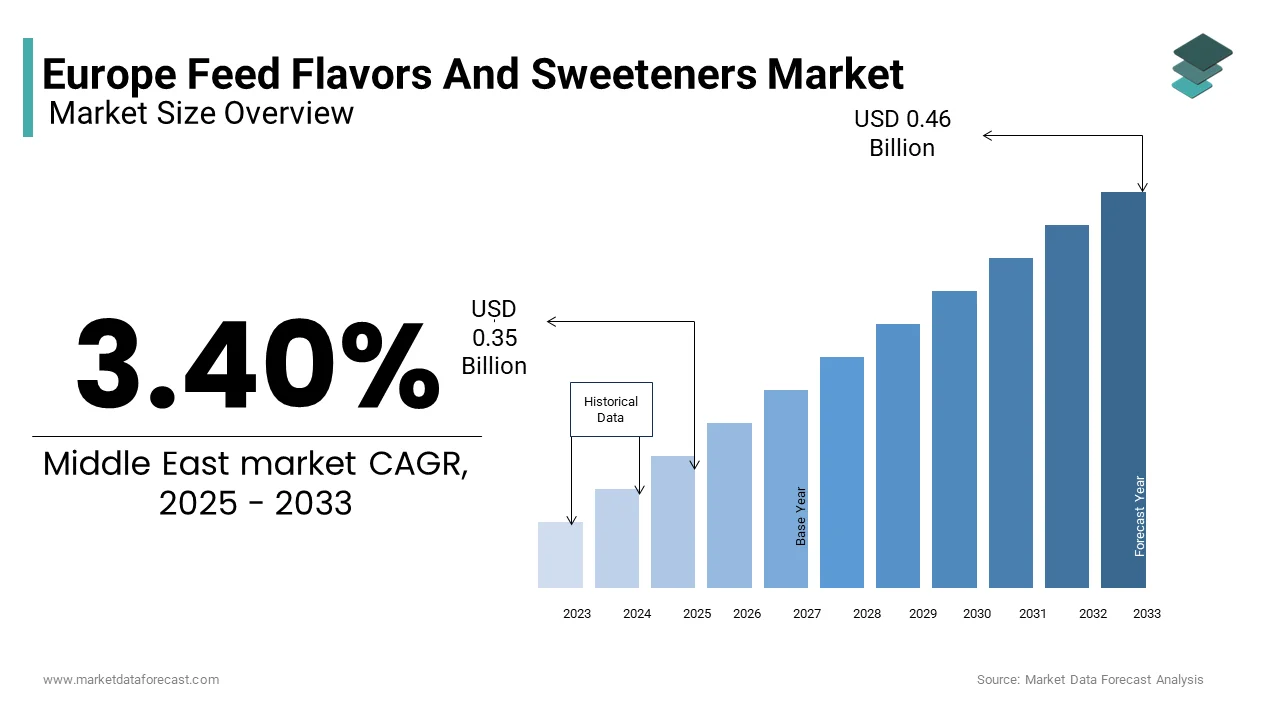

The Europe feed flavors and sweeteners market was valued at USD 0.34 billion in 2024 and is anticipated to reach USD 0.35 billion in 2025, from USD 0.46 billion by 203,3, and d estimated to grow at a CAGR of 3.40% during the forecast period from 2025 to 2033.

The Feed Flavors and Sweeteners additives play a crucial role in improving feed consumption, digestion, and overall animal health, thereby supporting productivity in the livestock industry. Feed flavors are primarily used to mask the bitter taste of certain ingredients and medications, while sweeteners act as taste enhancers and energy sources. The market is witnessing growing demand for natural and functional flavoring agents due to rising consumer awareness regarding animal welfare and food safety. Additionally, regulatory bodies such as the European Food Safety Authority (EFSA) have established guidelines that influence the formulation and application of these additives. This trend aligns with broader shifts toward sustainable farming practices and optimized feed efficiency across Europe’s agri-food systems.

MARKET DRIVERS

Rising Demand for Animal Protein Across Europe

One of the key drivers propelling the Europe Feed Flavors and Sweeteners Market is the growing consumption of animal protein in countries like Germany, France, and the Netherlands. According to the Food and Agriculture Organization (FAO), per capita meat consumption in Europe stood at approximately 70 kilograms in 2023, significantly higher than the global average. This increased demand has led to intensified livestock production, which in turn necessitates enhanced feed formulations to ensure optimal growth and health of animals. Feed flavors and sweeteners play an essential role in improving feed intake, especially among young animals, where early nutritional support is critical for long-term productivity. Moreover, the European Union's robust dairy and meat export sector has further stimulated the need for high-quality feed additives. The incorporation of flavors and sweeteners not only enhances palatability but also supports consistent feed consumption, which aids in better weight gain and feed conversion ratios.

Increasing Adoption of Natural and Organic Feed Additives

A significant trend shaping the Europe Feed Flavors and Sweeteners Market is the shift toward natural and organic feed additives driven by stringent regulations and evolving consumer preferences. As per the European Commission’s Farm to Fork Strategy, there is a strong push to reduce the use of synthetic additives and antibiotics in animal feed, promoting cleaner label products. This policy direction has encouraged feed manufacturers to incorporate plant-based flavors and sweeteners derived from sources such as molasses, licorice, and citrus extracts. The demand for natural feed additives is particularly strong in premium livestock sectors such as organic dairy and free-range poultry, where product differentiation is key. This transition not only aligns with sustainability goals but also opens new growth avenues for ingredient suppliers focusing on botanical extracts and functional sweeteners tailored to animal nutrition.

MARKET RESTRAINTS

Regulatory Restrictions on Synthetic Additives

One of the primary constraints affecting the Europe Feed Flavors and Sweeteners Market is the tightening regulatory framework surrounding synthetic additives in animal feed. The European Food Safety Authority (EFSA) has implemented rigorous approval processes for feed additives under the EU Regulation (EC) No 1831/2003, requiring extensive safety and efficacy evaluations before market entry. As a result, several artificial flavors and sweeteners previously used in feed formulations have been restricted or removed entirely due to potential health or environmental risks.

For instance, in 2022, EFSA re-evaluated the use of synthetic ethyl vanillin, a common flavoring agent, and imposed stricter usage limits due to concerns about its impact on gut microbiota in livestock. This regulatory scrutiny has increased the cost and time required for product development, discouraging smaller players from entering the market. According to a report by Cogent Economics, compliance costs for feed additive manufacturers in the EU rose by approximately 18% between 2020 and 2023, limiting innovation in synthetic flavor development. Consequently, many companies are shifting focus toward natural alternatives, which often come with their challenges, including variability in sourcing and higher production costs. These regulatory pressures continue to shape the market landscape, which is compelling industry participants to prioritize transparency and scientific validation in their product offerings.

Volatility in Raw Material Prices Affects Production Costs

Another critical challenge impeding the growth of the Europe Feed Flavors and Sweeteners Market is the fluctuation in raw material prices, particularly those sourced from agricultural commodities. Ingredients such as molasses, citrus extracts, and sugar beet derivatives commonly used in natural sweeteners and flavor formulations are subject to price volatility due to climatic conditions, geopolitical instability, and supply chain disruptions. According to the International Sugar Organization, the price of sugar beet, a key component in feed sweeteners, surged by over 25% in 2023 due to reduced yields in major producing regions like France and Germany.

This volatility directly impacts production costs for feed additive manufacturers, which is leading to inconsistent pricing for end-users such as livestock producers. Moreover, small and medium-sized enterprises (SMEs) face heightened financial pressure, as they lack the purchasing power to secure bulk discounts or hedge against commodity price swings. This economic uncertainty hampers the scalability of innovative feed flavor and sweetener products, despite growing demand.

MARKET OPPORTUNITIES

Expansion of Precision Livestock Farming Technologies

One of the most promising opportunities in the Europe Feed Flavors and Sweeteners Market is the rapid adoption of precision livestock farming (PLF) technologies, which enable real-time monitoring and customization of animal diets. PLF integrates data analytics, IoT sensors, and automated feeding systems to optimize livestock nutrition based on individual animal needs. These advanced systems create a demand for specialized feed additives, including targeted flavors and sweeteners designed to improve palatability and nutrient uptake in precision-fed diets. For example, smart feeders can adjust flavor profiles based on the age, weight, and health status of animals, enhancing feed intake consistency. Companies such as DeLaval and Lely are actively integrating feed customization modules into their PLF platforms, driving innovation in feed additive applications. Additionally, the European Innovation Partnership for Agricultural Productivity and Sustainability (EIP-AGRI) has funded multiple initiatives aimed at developing sensor-driven flavor delivery mechanisms, further reinforcing the synergy between digital agriculture and feed enhancement.

Growing Demand for Functional Feed Additives in Aquaculture

Aquaculture is emerging as a key growth area within the Europe Feed Flavors and Sweeteners Market, driven by the expanding seafood farming industry and increasing emphasis on sustainable protein sources. Unlike terrestrial livestock, aquatic species often require highly palatable feeds to ensure adequate consumption during early developmental stages.

Flavors and sweeteners play a vital role in stimulating appetite and improving feed acceptance in fish and shellfish. Studies conducted by the Institute of Marine Research in Norway have shown that the addition of marine-based flavor enhancers can increase feed intake by up to 20%, directly contributing to improved growth rates and feed efficiency. Moreover, the trend toward plant-based aquafeeds to reduce dependency on fishmeal has created a need for flavor masking agents to counteract undesirable tastes. Companies such as Skretting and Biomar are investing heavily in research to develop customized flavor profiles that align with alternative protein sources.

MARKET CHALLENGES

Complexity in Flavor Standardization Across Species and Diets

One of the foremost challenges facing the Europe Feed Flavors and Sweeteners Market is the difficulty in standardizing flavor formulations across different animal species and dietary requirements. According to the French National Institute for Agriculture, Food, and Environment (INRAE), studies have revealed that flavor perception in pigs differs significantly from that of cattle, necessitating tailored formulations to achieve desired feed intake improvements. Additionally, variations in feed composition, such as the inclusion of medicated ingredients, alternative proteins, or fiber-rich components, further complicate flavor compatibility. This inconsistency poses a significant hurdle for manufacturers seeking to develop scalable, multi-species flavor solutions. Moreover, the growing adoption of precision feeding systems requires precise flavor calibration, adding another layer of complexity to product development.

Consumer Skepticism Toward Artificial Ingredients in the Food Chain

Consumer skepticism regarding the use of artificial ingredients in the food chain remains a considerable challenge for the Europe Feed Flavors and Sweeteners Market. A 2023 survey conducted by the European Consumer Organisation (BEUC) found that 72% of respondents expressed concern about chemical additives in animal feed, fearing potential residual effects in meat, dairy, and eggs. Such perceptions have prompted retailers and food service providers to impose stricter ingredient policies. For example, major supermarket chains like Carrefour and Rewe have introduced private-label livestock products certified as free from synthetic additives, influencing upstream feed suppliers to reformulate their offerings. This shift has placed additional pressure on feed flavor and sweetener manufacturers to replace artificial compounds with natural alternatives, even though the latter may be less stable, more expensive, or harder to source consistently.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2023 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.40% |

| Segments Covered | By Type, Livestock, and Region. |

|

Various Analyses Covered | Global, Regional and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Biomin GMBH, E. I. Dupont, Eli Lilly and Company, Ferrer Internacional, Industrial Técnica Pecuaria, Jefo NutritioInc.NC, Kerry Group PLC, Phytobiotics, Prino v, and Tanke International Group. |

SEGMENTAL ANALYSIS

By Type Insights

The natural segment was the largest and held 58.5% of the Europe Feed Flavors and Sweeteners Market share in 202,4, with an expected CAGR of 6.8% during the forecast period. Moreover, the shift toward organic and free-range farming practices in countries like Germany, France, and the Netherlands has further amplified the adoption of natural flavoring agents. The natural feed flavors and sweetness, projected to grow at a CAGR of 6.8% during the forecast period (2023–2030. This rapid expansion is fueled by increasing regulatory support for sustainable agriculture and rising investments in green feed technologies. The European Food Safety Authority (EFSA) has intensified its scrutiny of synthetic additives, which is leading to stricter approval processes and withdrawal of several artificial compounds from the market. In 2022 alone, EFSA re-evaluated over 15 synthetic flavor ingredients by restricting their use based on new toxicity assessments.

Simultaneously, advancements in biotechnology have enabled the development of high-purity plant-based flavors and fermentation-derived sweeteners that offer enhanced stability and performance. Furthermore, the rise of premium livestock segments such as organic poultry and grass-fed beef has created niche demand for customized flavor profiles.

By Livestock Insights

The Europe Feed Flavors and Sweeteners Market is also segmented by livestock category into cattle, swine, poultry, aquaculture, and others, with poultry dominating the market and capturing around 32% of total consumption in 2023. This leadership is primarily driven by the massive scale of poultry production across Europe, particularly in countries like Poland, Germany, and France. According to Eurostat, the EU produced over 14 million metric tons of poultry meat in 2023, which is making it the most consumed meat type in the region. High feed intake rates among broilers and layers necessitate consistent palatability improvements to ensure optimal growth and egg yield. Another key driver is the widespread use of feed flavors and sweeteners to enhance feed acceptance in young chicks, which is crucial for early-stage nutrition and immunity development. A study published by Wageningen Livestock Research in 2023 found that flavored starter feeds increased feed intake by up to 18% in broiler chickens, directly contributing to improved weight gain and feed conversion ratios. Moreover, the growing integration of automated feeding systems in large-scale poultry farms has boosted demand for customized flavor blends that align with precision nutrition strategies.

The livestock segment is projected to expand with a CAGR of 7.2% from 2025 to 2033. According to the European Maritime and Fisheries Fund (EMFF), aquaculture production in the EU reached 1.3 million metric tons in 2023, with salmon, trout, and sea bream being the dominant species cultivated. Additionally, scientific research conducted by the Institute of Marine Research in Norway demonstrated that the inclusion of marine-based flavoring compounds significantly improves feed intake and digestion in farmed fish, boosting growth performance. In 2023, Skretting, a leading aquafeed manufacturer, reported a 22% increase in sales of flavored aquafeed formulations, reflecting strong market adoption. Government-backed blue economy initiatives, such as the EU’s Strategic Aquaculture Guidelines, are also promoting sustainable feed solutions, including innovative flavoring technologies.

COUNTRY ANALYSIS

Germany was the largest contributor by occupying 18.2% of the Europe Feed Flavors and Sweeteners Market share in 2024. According to the German Farmers’ Association (DBV), the country produced over 50 million metric tons of compound feed in 2023, which is making it the top feed producer in the EU. The domestic livestock industry, particularly in swine and poultry, heavily relies on feed additives to improve productivity and meet stringent food safety regulations. Additionally, the country's strong emphasis on sustainable livestock practices, backed by the Federal Ministry of Food and Agriculture (BMEL), has accelerated the adoption of clean-label feed ingredients. A 2023 report by the Fraunhofer Institute noted that over 45% of German feed producers had transitioned to plant-based flavoring agents, which aligns with national sustainability goals.

France ranked second with 12.3% of the Europe Feed Flavors and Sweeteners Market share in 2024. As one of the continent’s largest agricultural economies, France plays a pivotal role in shaping feed additive demand in the cattle and poultry sectors. One of the primary drivers fueling France’s strong position in the market is the government’s active promotion of organic and sustainable farming through the Ecophyto Plan and National Low-Carbon Strategy. Leading French feed manufacturers such as LDC and Cooperl are increasingly incorporating natural flavoring agents to meet both domestic and international clean-label expectations. France continues to be a key market for feed flavors and sweeteners across Europe, with strong institutional backing and a growing focus on eco-conscious livestock production.

The Netherlands' feed flavors and sweeteners market is estimated to have significant growth opportunities. A key factor contributing to the Netherlands' strong market position is its advanced feed manufacturing infrastructure and strategic location as a logistics gateway for neighboring EU countries. Dutch companies such as Nutreco and Royal Agrifirm Group are at the forefront of developing customized feed flavors and sweeteners tailored to precision livestock farming systems. Additionally, the Dutch government’s commitment to sustainable agriculture under the “Circular Economy by 2050” initiative has encouraged the adoption of plant-based feed additivesSpain'sin feed flavors and sweeteners market growth is largely driven by the country’s prominence is largely driven by its robust livestock industry, particularly in pork and poultry production, where Spain ranks among the top producers in the EU. A major growth driver for Spain’s feed flavors and sweeteners market is the increasing adoption of functional feed additives aimed at improving gut health and feed efficiency. Additionally, the rise of organic livestock operations, supported by government incentives under Spain’s CAP Strategic Plan, has led to greater incorporation of natural flavors and sweeteners. Companies like EFECE and Vilomix Iberia are actively developing plant-based feed additives tailored to local livestock needs, which is reinforcing Spain’s expanding footprint in the regional feed enhancement market.

Italy's feed flavors and sweeteners market is substantially to grow substantially with prominent growth opportunities in the coming years. The country is a major producer of dairy, swine, and poultry, with the Italian National Institute of Statistics (ISTAT) reporting that over 25 million pigs and 55 million poultry birds were raised in 2023. As per Coldiretti, Italy’s largest agricultural association, over 40% of dairy farmers have adopted specialized feed formulations enriched with natural flavors and sweeteners to ensure consistent milk composition and flavor profiles. The growing presence of feed additive manufacturers such as Sacco System and DSM Italia further supports market expansion by ensuring Italy remains a key market for feed flavors and sweeteners in Southern Europe.

KEY MARKET PLAYERS

Biomin GMBH, E. I. Dupont, Eli Lilly and Company, Ferrer Internacional S.A., Industrial Técnica Pecuaria, Jefo NutritionInc.c, Kerry Group PLC, Phytobiotics, Prinova, and Tanke International Group. These are the market players that are dominating the Europe feed flavors and sweeteners market.

Top Players In The Market

One of the leading companies in the Europe Feed Flavors and Sweeteners Market is BASF SE. The company's extensive R&D capabilities enable it to offer innovative flavoring agents tailored for various livestock species. Its commitment to sustainability and animal nutrition has positioned it as a key player in both synthetic and natural feed additive segments. Another major contributor is Evonik Industries AG, a specialty chemicals company known for its advanced feed ingredient formulations. Evonik focuses on improving feed efficiency through customized flavor and sweetener solutions that support animal health and performance. DSM Nutritional Products AG is also a dominant force in the market, offering a broad portfolio of feed flavors and sweeteners designed to optimize animal feed intake and digestion. DSM emphasizes innovation and sustainability by integrating natural ingredients into its product lines.

Top Strategies Used By Key Market Participants

One of the primary strategies employed by key players in the Europe Feed Flavors and Sweeteners Market is product innovation and customization. Companies are increasingly focusing on developing tailored flavor and sweetener blends that cater to specific livestock needs, enhancing feed intake and performance. This approach allows them to differentiate their offerings and meet the rising demand for precision nutrition in modern farming systems.

Another crucial strategy is expanding strategic partnerships and collaborations. Leading firms are engaging in joint ventures, research alliances, and co-development initiatives with feed manufacturers, academic institutions, and biotech firms. These collaborations help accelerate product development, improve formulation efficacy, and align with evolving regulatory requirements across the region.

Sustainability-driven product development has become a central focus. Market leaders are shifting toward plant-based, natural, and eco-friendly feed additives to comply with stringent EU regulations and consumer expectations. Companies strengthen their brand positioning and future-proof their portfolios in a rapidly transforming market landscape by investing in green technologies and clean-label ingredients.

COMPETITION OVERVIEW

The competition in the Europe Feed Flavors and Sweeteners Market is characterized by a mix of established multinational corporations and emerging regional players striving to capture market share through innovation and differentiation. With increasing demand for sustainable and natural feed additives, companies are under pressure to continuously refine their product portfolios and align with evolving regulatory frameworks. Major players leverage their extensive R&D capabilities to develop customized flavor and sweetener solutions tailored for different livestock categories, thereby strengthening their foothold in niche segments. At the same time, smaller firms are gaining traction by offering specialized, cost-effective alternatives, particularly in organic and plant-based formulations. Strategic acquisitions, partnerships, and technology integration have become common tactics to expand distribution networks and enhance product efficacy. Additionally, the growing emphasis on precision livestock farming is pushing companies to integrate digital tools into feed additive applications, further intensifying competitive dynamics.

RECENT HAPPENINGS IN THE MARKET

- In June 2023, BASF launched a new line of natural feed flavor enhancers specifically designed for poultry and swine diets. This product line is aimed at improving feed palatability while supporting digestive health, which is reinforcing BASF’s commitment to sustainable livestock nutrition.

- In September 2023, Evonik Industries announced a strategic partnership with a leading European feed manufacturer to co-develop customized sweetener blends that enhance feed intake in young ruminants. This collaboration was intended to strengthen Evonik’s presence in the ruminant feed segment.

- In November 2023, DSM Nutritional Products introduced an advanced encapsulation technology for flavor delivery in aquafeed, ensuring improved stability and controlled release. This innovation targeted the growing aquaculture sector in Northern Europe.

- In February 2024, Cargill Animal Nutrition expanded its feed additive production facility in the Netherlands to include dedicated lines for natural flavor compounds by aiming to meet rising demand across Western Europe.

- In May 2024, Kemin Industries acquired a small European-based flavor formulation firm specializing in botanical extracts for livestock feed, which is strengthening Kemin’s portfolio of clean-label feed additives and expanding its regional footprint.

MARKET SEGMENTATION

This research report on the Europe Feed Flavors and Sweeteners Market is segmented and sub-segmented into the following categories.

By Type

- Natural and Artificial Feed Flavors and Sweeteners

By Livestock

- cattle

- swine

- poultry

- aquaculture

- others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the projected CAGR of the Europe Feed Flavors Market from 2024 to 2033?

The Europe feed flavors market is expected to grow at a CAGR of 3.40% from 2024 to 2030 , driven by increasing demand for palatable livestock feed, rising pet ownership, and growing focus on improving feed intake in young and stressed animals across major countries like Germany, France, and the Netherlands.

Which country leads in feed flavor adoption within Europe?

Germany accounts for over 22% of total feed flavor consumption , driven by its large-scale livestock operations, advanced feed manufacturing infrastructure, and strong presence of pet food producers. The German Association of Animal Nutrition (DVT) reported a 16% increase in flavored feed formulations since 2021 , particularly in piglet and dairy calf diets.

How much feed flavor was consumed across Europe in 2023?

As of 2023, over 8,200 metric tons of feed flavors were used across the EU, primarily in compound feed for pigs, poultry, and calves, according to the European Feed Manufacturers’ Federation (FEFANA) . Demand is highest in Western and Central Europe due to intensive farming practices.

What percentage of pet food in Europe contains added feed flavors?

Over 65% of premium dry pet food products sold in the EU include added feed flavors, especially in kibble-based dog foods, where palatability is crucial. According to Euromonitor International, flavored pet feeds accounted for nearly €11 billion in sales in 2023, reflecting strong consumer preference for taste-enhanced pet nutrition.

Which type of feed flavor dominates the European market?

Plant-based and herbal flavors , including anise, garlic, fenugreek, and mint derivatives , dominate the market, capturing nearly 40% of total feed flavor usage . These ingredients are favored for their natural appeal, digestive benefits, and compatibility with organic and clean-label feed formulations.

How has the shift toward antibiotic-free livestock production impacted feed flavor demand?

With the full implementation of EU Regulation (EC) No 1831/2003 promoting alternatives to in-feed antibiotics, feed manufacturers have increasingly turned to flavoring agents that stimulate appetite and improve gut health. As per EFSA’s 2023 report, flavored feed adoption increased by 14% among antibiotic-reduced feeding programs, especially in pig and poultry sectors.

How do feed flavors improve feed intake in weaned piglets?

Studies by Wageningen University & Research show that adding sweet and umami flavors to piglet starter feed improves feed intake by up to 18% , reducing post-weaning stress and enhancing growth performance. This has led to increased incorporation of vanillin, molasses, and amino acid-based flavor enhancers in early-life swine nutrition.

Which companies are leading innovation in natural feed flavors in Europe?

Key players such as Symrise AG, Pancosma S.A., and Delacon Biotechnik GmbH are driving R&D in botanical and phytogenic feed flavors , focusing on non-synthetic palatability enhancers that align with EU organic standards and sustainability goals.

What role do feed flavors play in reducing feed wastage?

According to the European Livestock and Meat Working Party , improved feed palatability through flavoring can reduce feed refusals by up to 12% , particularly in dairy cattle and broiler chickens, supporting better resource efficiency and cost management for farmers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com