Europe Feed Ingredients Market Size, Share, Trends & Growth Forecast Report, Segmented By Ingredient Type, Supplement Type, Animal Type, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Feed Ingredients Market Size

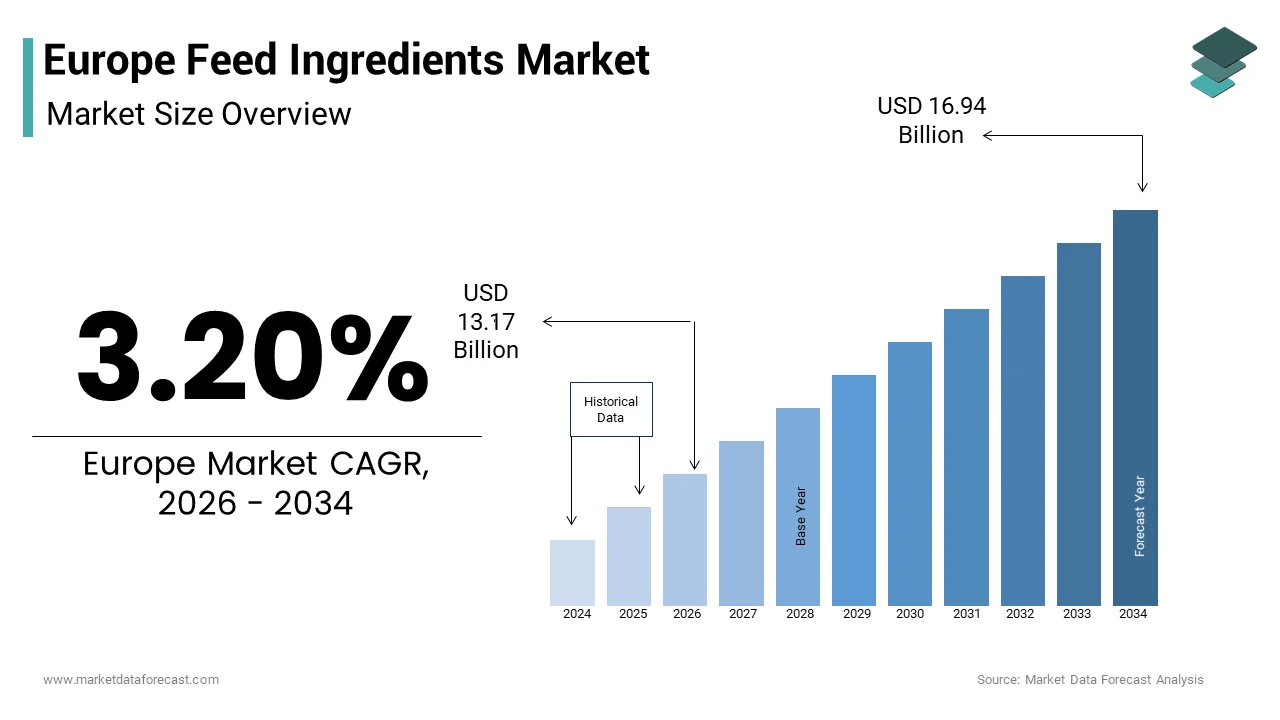

The European feed ingredients market size was valued at USD 12.76 billion in 2025 and is anticipated to reach USD 13.17 billion in 2026 to reach USD 16.94 billion by 2034, growing at a CAGR of 3.20% during the forecast period from 2026 to 2034.

Feed ingredients include proteins, amino acids, vitamins, minerals, enzymes, and specialty additives that are used in formulating balanced diets for livestock, poultry, aquaculture, and companion animals across the European Union. Unlike commodity feed markets, this segment focuses on ohigh-valueue, functional inputs that enhance animal health, feed efficiency, and product quality while complying with Europe’s stringent food safety and sustainability standards. According to FEFAC, the EU produced around 147 million metric tons of compound feed in 2024, which is supporting one of the world’s most regulated and technologically advanced livestock sectors. Concurrently, as per the European Commission’s Farm to Fork Strategy, livestock production must reduce environmental impact by cutting antibiotic use by 50% by 2030, as objectives that place immense pressure on feed formulators to innovate. These regulatory and ecological imperatives have transformed feed ingredients from mere nutritional supplements into strategic tools for achieving animal welfare, climate resilience, and circular economy goals across European agriculture.

MARKET DRIVERS

EU Farm to Fork Strategy Mandates Reduction in Antibiotic Use, Driving Demand for Functional Alternatives

The binding target of the European Union to reduce antimicrobial use in livestock by 50% by 2030 has catalysed widespread adoption of functional feed ingredients such as phytogenics, organic acids, probiotics, and prebiotics as antibiotic growth promoter replacements, which is one of the key factors propelling the regional market growth. According to the European Medicines Agency, sales of veterinary antimicrobials in the EU declined by 28% between 2018 and 2022, reflecting early compliance with this mandate. However, this reduction has intensified the need for alternatives that maintain gut health, immunity, and growth performance without compromising productivity. In response, many commercial pig and poultry farms across Europe have integrated multiple functional feed additives into their rations. Similarly, research institutions in France have increased trials involving yeast-based immunomodulators in dairy cattle feed to reduce mastitis incidence. These shifts underscore how regulatory pressure is reshaping feed formulation toward biologically active, health-promoting ingredients that align with Europe’s vision of sustainable, antibiotic-free animal production.

Rising Consumer Demand for High-Quality Animal Protein Fuels Premium Feed Formulation

European consumers increasingly associate animal diet with the nutritional and ethical quality of meat, milk, and eggs, driving producers to invest in premium feed ingredients that enhance product attributes such as omega-3 content, marbling, or yolk pigmentation, which is further contributing to the growth of the regional market. For instance, a majority of EU citizens are willing to pay more for animal products derived from animals fed natural or enriched diets. This sentiment is reflected in retail trends; the UK’s Soil Association reported that sales of organic products, including enriched eggs, which grew by 6% in 2024, and driven by the inclusion of algal oil or flaxseed in layer rations. Similarly, Spanish pork producers participating in the “Iberian Acorn Fed” certification program use specialized feeds supplemented with antioxidants to preserve meat quality during extended curing. These premium segments require consistent, traceable ingredient sourcing, which is creating stable demand for high-purity amino acids, specialty oils, and natural pigments that deliver measurable product differentiation in a competitive retail landscape.

MARKET RESTRAINTS

Strict EU Regulations on Novel and Genetically Modified Feed Ingredients Limit Ingredient Innovation

The European Union maintains one of the world’s most cautious approval frameworks for novel and genetically modified feed components, which significantly constrains the availability of next-generation ingredients such as insect protein, single-cell proteins, and GM soy derivatives and impedes the regional market growth. According to the European Food Safety Authority, the average authorization timeline for a novel feed ingredient exceeds 24 months,s, with only a limited number of approvals granted between 2020 and 2024. Although insect meal from Tenebrio molitor (mealworm) was authorized for poultry and pigs in 2021 and Hermetia illucens (black soldier fly) for aquaculture in 2023, commercial-scale adoption remains limited due to high production costs and unclear labeling rules. Furthermore, genetically modified soy that accounts for around 80% of global soybean production faces import restrictions and mandatory labeling, which is deterring many EU compounders from using it despite its protein density. This regulatory bottleneck forces feed formulators to rely on conventional, often less sustainable ingredients like soybean meal from South America or rapeseed meal, which is limiting the sector’s ability to fully embrace circular and low footprint alternatives envisioned under the Farm to Fork Strategy.

Volatility in Global Supply Chains and Geopolitical Disruptions Threaten Raw Material Security

The heavy reliance of Europe on imported protein meals, particularly soybean meal from Brazil and Argentina, exposes the feed ingredients market to significant supply chain instability, which is further hampering the regional market expansion. According to the European Commission, the EU imported around 30 million metric tons of soybean equivalents in 20,24, with the majority sourced from outside the bloc. This dependence became critically evident during the 2023 Red Sea shipping crisis, which increased freight costs significantly and delayed soy shipments, which is triggering regional shortages. Similarly, the ongoing war in Ukraine disrupted sunflower meal flows, a key alternative protein source for poultry and pigs. For instance, many compound feed mills experienced ration reformulations in 2024 due to ingredient unavailability or price spikes. Without accelerated development of domestic protein crops or diversified sourcing from certified sustainable origins, Europe’s feed sector will remain vulnerable to external shocks that compromise livestock productivity and food security.

MARKET OPPORTUNITIES

Expansion of Insect Protein Authorization Creates New Sustainable Protein Channel

A major opportunity in the Europe feed ingredients market lies in the gradual regulatory opening of insect-derived proteins as sustainable alternatives to imported soy and fishmeal. Following the European Commission’s 2023 authorization of processed animal protein from black soldier fly larvae for use in poultry and pig feed, commercial production is scaling rapidly. For instance, insect protein production capacity in the EU expanded significantly in 2024 with facilities in the Netherlands, France, and Germany converting organic food waste into high-quality protein meal containing 55 to 65% crude protein. These systems align with circular economy principles by valorizing unavoidable food losses while requiring minimal land and water. Trials conducted in Denmark showed that replacing a portion of soybean meal with insect meal in broiler diets improved feed conversion efficiency and reduced nitrogen excretion. As the EU finalizes carbon footprint methodologies for feed ingredients, insect protein is poised to become a cornerstone of low-emission, locally sourced animal nutrition.

Integration of Precision Fermentation Enables On-Demand Production of Specialty Additives

Emerging biotechnology platforms are unlocking opportunities for European feed producers to source high-value ingredients through precision fermentation, bypassing traditional agricultural constraints. Companies are now using engineered microbes to produce essential amino acids, enzymes, and even milk proteins in controlled bioreactors. Fermentation-derived phytase enzymes now account for a significant share of the EU market due to their high stability and dosing precision. Beyond enzymes, startups in Belgium and Sweden are scaling production of fermentation-based methionine and lysine that reduce reliance on petrochemical synthesis. According to the European Investment Bank, in 2024 that it allocated substantial funding to support biomanufacturing hubs for sustainable feed additives, which is recognizing their potential to decouple nutrition from volatile crop markets. As regulatory pathways for novel fermentation products streamline under the EU’s Innovation Deal, this technology could redefine ingredient security, traceability, and carbon efficiency across the European feed value chain.

MARKET CHALLENGES

Fragmented National Interpretations of Feed Additive Regulations Impede Market Harmonization

Despite EU-wide legislation under Regulation (EC) No 1831/2003, member states continue to apply divergent interpretations of feed additive approvals, labeling, and usage limits, which is creating barriers to cross-border trade and innovation and challenging the feed ingredients market in Europe. According to the European Feed Manufacturers’ Federation, several member states imposed additional national restrictions on certain phytogenic or organic acid products in 2024, even when these ingredients held EU authorization. For instance, while a probiotic strain may be approved for use in piglets at the EU level, Germany may require supplementary dossiers while Italy bans its use in organic production. This regulatory fragmentation forces feed companies to maintain multiple formulations for different markets, which increases R&D and compliance costs. For instance, many exporters delayed product launches in 2024 due to unpredictable national requirements. Until the European Commission enforces stricter harmonization through the Single Market Enforcement Action Plan, this patchwork will continue to stifle scale, investment, and innovation in the feed ingredients sector.

Limited Adoption of Digital Nutrition Platforms Hinders Precision Feeding Implementation

While Europe leads in animal welfare and sustainability policy, the practical implementation of precision feeding remains underdeveloped due to insufficient integration of digital tools in feed formulation, which is further challenging the regional market expansion. According to the European Commission’s Digital Agriculture Report 2024, less than one-third of EU livestock farms used connected feeding systems that adjust nutrient delivery based on growth stage, health status, or environmental conditions. This gap stems from fragmented farm data ecosystems, a lack of interoperability between feed mills and farm management software, and limited technical capacity among small and mid-sized producers. Consequently, even when advanced ingredients like enzyme complexes or amino acid blends are available, their full potential is unrealized due to static herd-level formulations. As per the research from the French National Institute for Agricultural Research, precision feeding could reduce nitrogen excretion and improve feed efficiency, yet adoption barriers persist. Without coordinated investment in open data standards, cloud-based nutrition platforms, and farmer digital literacy, Europe will struggle to translate ingredient innovation into measurable farm sustainability outcomes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.23% |

| Segments Covered | By Ingredient Type, Supplement, Animal, By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | BASF, Adisseo, Bunge, Cargill, Ingredion Incorporated, DSM, Novus International Inc., Alltech, Archer Daniels Midland Company, and Yara. |

SEGMENT ANALYSIS

By Ingredient Insights

The cereals segment held 38.8% of the regional market share in 2024. The dominance of the cereals segment in the European market is primarily due to its role as the foundational energy source in compound feed formulations across all major livestock sectors. Wheat, barley, and maize constitute the bulk of cereal usage, offering readily digestible starch, moderate protein, and cost-effective caloric density. According to Eurostat, the EU produced around 270 million metric tons of cereals in 2024, with a significant share allocated to animal feed, which indicates domestic agricultural alignment with livestock demand. This reliance is further reinforced by the EU’s Common Agricultural Policy, which incentivizes cereal cultivation through direct payments and crop diversification schemes to ensure stable supply and price moderation. As per the European Commission’s Farm Accountancy Data Network, a large share of cereal-based feed in Western Europe uses domestically grown grains to reduce import dependency and carbon footprint. For instance, the German feed industry sources most of its wheat and barley from national farms to minimize logistics emissions and support rural economies. This synergy between agricultural policy, supply chain resilience, and sustainability priorities cements cereals as the structural backbone of European feed formulation.

The feed additives segment is anticipated to exhibit the fastest CAGR of 8.04% over the forecast period in this regional market, owing to the EU’s binding Farm to Fork targets, which mandate a 50% reduction in antibiotic use and a 20% cut in nutrient losses by 2030 as goals unattainable without advanced nutritional interventions. Feed additives enable precision nutrition that enhances digestibility, gut health, and emission efficiency without compromising productivity. The rising demand for antibiotic-free livestock production, driven by retailer and consumer pressure, is further boosting the expansion of the feed additives segment in the European market. For instance, a majority of EU shoppers in 2024 preferred meat and dairy from animals raised without routine antibiotics. In response, major poultry integrators in the Netherlands and France have reformulated rations to include multi-enzyme complexes and yeast derivatives that improve feed conversion and immune resilience. For instance, enzyme-supplemented diets reduced nitrogen excretion while maintaining growth rates, which directly supports EU environmental mandates. As regulatory and market forces converge, feed additives are transitioning from optional supplements to essential tools for compliant, competitive animal production.

By Supplement Insights

The enzymes segment accounted for 30.7% of the regional market share in 2024. The growth of the enzymes segment in the European market is attributed to their proven efficacy in improving nutrient utilization and reducing environmental emissions. Phytase, xylanase, and protease enzymes are routinely added to monogastric diets to break anti-nutritional factors in plant-based ingredients and thereby enhance phosphorus, energy, and amino acid availability. Phytase is now widely included in commercial poultry and swine feed across the EU to reduce inorganic phosphate supplementation and lower phosphorus runoff into waterways. The regulatory alignment with EU sustainability goals is also contributing to the growth of the enzymes segment in this regional market. The European Commission’s 2024 Nutrient Management Strategy explicitly endorses enzyme use as a best available technique for mitigating livestock’s environmental footprint. For instance, multi-enzyme blends in pig feed improved feed conversion efficiency and reduced methane intensity, which supports environmental and productivity goals. These quantifiable benefits have made enzymes a non-discretionary component in modern, precision feed formulations across Europe.

The antioxidants segment is growing at a prominent CAGR during the forecast period in this regional market. The need to stabilize lipid-rich feed formulations and protect animal health under heat stress conditions exacerbated by climate change is driving the growth of the antioxidants segment in the European market. The inclusion of synthetic and natural antioxidants in poultry and swine feed has increased in recent years due to the rising use of unsaturated fats like linseed and algae oils to enrich meat and egg omega-3 content. The EU’s strict regulations on feed oxidation and rancidity are further boosting the segmental expansion in this regional market. The European Food Safety Authority mandates maximum peroxide values in compound feed, requiring antioxidants to preserve fat quality during storage and transport. Additionally, heat waves across Southern Europe in 2023–2024 increased oxidative stress in livestock, prompting producers to supplement diets with antioxidants to maintain immune function and meat quality. For instance, many intensive pig farms in Spain adopted antioxidant fortified rations in 2024 to counter summer performance drops. As climate volatility intensifies and premium fat sources expand, the growth of the antioxidant segment will continue to rise across European feed systems.

By Animal Insights

The poultry segment had 33.9% of the European feed ingredients market share in 2024. The dominance of the poultry segment in the European market is attributed to the sector’s high feed conversion efficiency, short production cycles, and dominant role in meat consumption. According to Eurostat, the EU produced around 13 million metric tons of poultry meat in 2024, which is making it the most consumed meat in the region. Broiler production alone requires approximately 22 million tons of compound feed annannuallyith precise amino acid and enzyme balancing essential to achieve efficient feed conversion ratios. The leadership of the poultry industry in adopting antibiotic-free and welfare-certified production models is further propelling the growth of the segment in this regional market. Industry reports indicate that a large share of broiler farms in the Netherlands, Germany, and France now operate under certified antibiotic reduction programs, necessitating advanced feed formulations with probiotics, organic acids, and highly digestible protein meals. Retailer commitments—such as the UK’s “Better Chicken Commitment”—further drive demand for feed ingredients that support lower-growing breeds with higher nutritional needs. This convergence of volume, regulatory pressure, and market differentiation solidifies poultry as the primary driver of feed ingredient innovation and consumption in Europe.

The aquaculture segment is the fastest-growing animal segment and is expected to expand at a CAGR of 9.12% over the forecast period in this regional market, owing to the EU’s Blue Economy strategy, which aims to triple sustainable aquaculture production by 2030 to enhance food security and reduce seafood import dependency. According to the European Commission, EU aquaculture output reached about 1.2 million metric tons in 202,4, with salmon, sea bass, and trout leading growth with each requiring special high-protein feed formulations. The regulatory push to replace fishmeal with novel ingredients is further boosting the expansion of the aquaculture segment in this regional market. The EU’s Sustainable Aquaculture Guidelines mandate that feed sustainability be prioritized, accelerating ng adoption of insect meal, algal oils, and single-cell proteins. Norway’s collaboration with EU producers under the EEA agreement has spurred trials in Denmark and Greece, where black soldier fly meal replaced a portion of fishmeal in seabream diets without compromising growth. The European Investment Bank allocated significant funding in 2024 to support aquafeed innovation hubs in Spain and the Netherlands. As marine ingredient scarcity intensifies and consumer demand for farmed fish rises, aquaculture will drive premium, sustainable feed ingredient adoption at the fastest pace in Europe.

COUNTRY ANALYSIS

Germany Feed Ingredients Market Analysis

Germany dominated the feed ingredients market in Europe in 2024 by accounting for 21.9% of the regional market share. The dominance of Germany in the European market is attributed to its status as the EU’s top pork and poultry producer and its highly integrated agri-feed industry. Germany operates over 300 compound feed mills that produced around 24 million metric tons of feed in 2024, as per the German Feed Industry Association. Strict national implementation of the EU Farm to Fork Strategy has accelerated the adoption of enzyme and probiotic supplements. Additionally, Germany’s strong biotech sector supports domestic production of fermentation-derived amino acids and enzymes, reducing import reliance. With robust R&D collaboration between universities, feed mills, and ingredient suppliers, Germany sets the benchmark for science-based, sustainable feed formulation in Europe.

France Feed Ingredients Market Analysis

France commanded a substantial share of the European market during the forecast period due to its diverse livestock base and proactive agricultural policies. According to France’s Ministry of Agriculture, the country produced around 19 million metric tons of compound feed in 2024, with strong emphasis on circular feed ingredients like bakery by-products and locally grown peas. The “Proteins Plan” launched in 2023 aims to double domestic protein crop area by 2030, directly supporting feed self-sufficiency. French feed formulators are also pioneers in phytogenic integration, with many swine diets containing plant-based additives to replace zinc oxide. This blend of policy support, agricultural diversification, a nd innovation makes France a high-volume, high-sophistication feed ingredients market.

Netherlands Feed Ingredients Market Analysis

The Netherlands is a prominent market for feed ingredients in Europe due to its export-oriented livestock sector and global leadership in feed technology. Despite its small land area, the Netherlands is Europe’s largest exporter of poultry and dairy genetics that require premium, consistent feed formulations. As per the Dutch Feed Industry Association, a large share of compound feed produced in 2024 included precision enzyme and vitamin premixes tailored to genetic potential. The country also hosts major R&D centers for global ingredient companies, which are driving trials in insect protein, algae oils, and digital feed formulation. Strict manure and emission regulations under the Nitrogen Action Programme further incentivize nutrient-dense, low-excretion diets. The Netherlands thus serves as a high-tech, compliance-driven hub for advanced feed ingredient adoption.

Spain Feed Ingredients Market Analysis

Spain is predicted to hold a notable share of the Europe feed ingredients market during the forecast period, owing to its rapidly expanding intensive livestock sectors, particularly pig and poultry. Spain’s Ministry of Agriculture reported that the country produced around 38 million pigs in 2024, which is driving massive demand for cereals and protein meals. Persistent drought conditions have increased reliance on imported soybean meal, but also spurred innovative water-efficient feed additives like betaine and yeast derivatives to mitigate heat stress. Additionally, Spain’s aquaculture output has grown steadily in recent years, which is creating new demand for sustainable aquafeed ingredients. With strong agro-industrial capacity and climate adaptation needs, Spain represents a dynamic growth market for resilient, high-performance feed solutions.

United Kingdom Feed Ingredients Market Analysis

The United Kingdom is projected to grow at a healthy CAGR in the European feed ingredients market during the forecast period, owing to its post-Brexit regulatory autonomy and strong retailer-driven animal welfare standards.

The UK produced about 10 million metric tons of compound feed in 2024, according to the Agricultural Industries Confederation, with a majority of poultry and pig farms adhering to toantibiotic-freee or RSPCA-assured schemes. These certifications mandate specific feed ingredient inclusions—such as non-GM cereals, organic acids, and fiber sources—driving premium formulation. The UK’s departure from the EU CAP has also accelerated investment in domestic protein crops like field beans and lupins to reduce soy dependency. With influential retail sustainability commitments and agile regulatory frameworks, the UK remains a trendsetting market for ethical, traceable, and innovative feed ingredients.

COMPETITIVE LANDSCAPE

The Europe feed ingredients market features intense competition among multinational nutrition companies, specialized biotech firms, and regional premix producers, all operating under the EU’s stringent regulatory and sustainability framework. Differentiation is driven by scientific validation, environmental credentials, and digital integration rather than price alone. Global leaders leverage economies of scale and R&D depth to offer comprehensive portfolios, while agile startups focus on novel ingredients like insect protein, algae derivatives, and precision fermentation products. Regulatory compliance—particularly regarding novel food approvals, GMO restrictions, and carbon accounting—is a critical barrier to entry, favoring incumbents with established dossiers and government relationships. At the same time, retailer sustainability commitments and farmer profitability pressures create demand for transparent, traceable, and performance-proven solutions the EU advances its circular economy and climate neutrality goals, competition is increasingly defined by the ability to deliver feed ingredients that are scientifically effective, environmentally responsible, and economically viable across diverse European production systems.

KEY MARKET PLAYERS

Some of the major players in the feed ingredients market are

- BASF

- Adisseo

- Bunge

- Cargill

- Ingredion Incorporated

- DSM

- Novus International Inc.

- Alltech

- Archer Daniels Midland Company

- Yara.

Top Players In The Market

- DSM-Firmenich is a global science-driven leader in health, nutrition, and bioscience with a prominent role in the Europe feed ingredients market through its comprehensive portfolio of vitamins, carotenoids, enzymes, and specialty additives. The company supplies advanced nutritional solutions to major feed mills and integrators across Germany, France,ce and the Netherlands, focusing on gut health, emission reduc, and animal welfare. In 2024, DSM-Firmenich launched a next-generation phytase enzyme with enhanced thermostability for pelleted feed, validated in EU trials to reduce phosphorus excretion by 15%. It also expanded its sustainable sourcing program for vitamin E, ensuring full traceability from renewable feedstocks in alignment with the EU Green Deal and strengthening its position as a trusted innovator in precision animal nutrition.

- BASF SE contributes significantly to the Europe feed ingredients market through its global production of synthetic amino acids, vitamins, and feed preservatives that support efficient and sustainable livestock production. Headquartered in Germany, BASF leverages its integrated chemical expertise to deliver high-purity lysine, methionine, and antioxidants tailored to European feed formulations. In 2024, the company commissioned a new amino acid fermentation facility in Antwerp, Belgium, powered by renewable energy and designed to meet the EU’s stringent carbon footprint standards for feed additives. BASF also partnered with French and Dutch research institutes to develop enzyme-amino acid synergies that improve protein utilization in low crude protein diets, directly supporting the Farm to Fork Strategy’s environmental targets.

- Cargill Animal Nutrition maintains a strong presence in the Europe feed ingredients market through its extensive network of compound feed mills, specialty premix plants, and digital advisory services across 18 European countries. The company provides integrated solutions ranging from cereal-based feed to precision enzyme and probiotic blends for poultry, swine, and ruminants. In 20,24, Cargill launched a digital feed formulation platform in Spain and Germany that uses real-time ingredient pricing and nutritional data to optimize rations for cost and sustainability. It also scaled up its use of insect protein and algal oils in aquafeed through partnerships with EU-based biotech startups, reinforcing its commitment to circular and low-emission feed innovation aligned with European regulatory priorities.

Top Strategies Used By The Key Market Participants

Key players in the Europe feed ingredients market invest heavily in research and development to create enzyme and amino acid solutions that align with the EU Farm to Fork Strategy’s targets for antibiotic reduction and emission cuts. They prioritize sustainable sourcing and carbon footprint transparency for vitamins and specialty additives to meet retailer and consumer demands. Companies establish regional fermentation and production facilities powered by renewable energy to ensure supply security and comply with EU green manufacturing standards. Strategic partnerships with national agricultural research institutes enable localized validation of feed efficacy under European farming conditions. Continuous digitalization of feed formulation through AI-driven platforms helps customers optimize cost, nutrient balance, and environmental impact in real time across diverse livestock systems.

MARKET SEGMENTATION

This research report on the European feed ingredients market is segmented and sub-segmented into the following categories.

By Ingredient Type

- Cereals

- Wheat

- Corn

- Barley

- Sorghum

- Rye

- others

- Protein Meal

- Plant protein sources

- and Animal Protein Sources

- Fats and Oils

- Feed additives

- others

By Supplement Type

- Vitamins

- Enzymes

- Antibiotics

- Antioxidants

- Minerals

- Others

- sweeteners

- acidifiers

- amino acids

- flavors

By Animal Type

- Poultry

- Ruminants

- Swine

- Aquaculture

- others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are feed ingredients, and why are they essential in European livestock farming?

Feed ingredients—such as cereals, protein meals, amino acids, vitamins, and additives—form balanced rations that ensure animal health, productivity, and food safety. In Europe, strict regulations and sustainability goals make ingredient quality and traceability paramount.

Which ingredients dominate the European feed market?

Cereals (wheat, barley, maize) and protein sources (soybean meal, rapeseed meal, and increasingly, insect and single-cell proteins) lead in volume, while specialty additives like phytogenics and probiotics are fast-growing segments.

How is the EU’s Farm to Fork Strategy reshaping feed formulation?

The strategy’s target to cut antimicrobial use by 50% by 2030 is accelerating demand for natural growth promoters (e.g., prebiotics, organic acids) and alternative proteins to reduce reliance on soy imports and antibiotics.

Are novel proteins gaining regulatory approval in Europe?

Yes—insect meal (e.g., from black soldier fly) is now approved for poultry and pigs (2023), and EU-authorized algae and yeast-based proteins are scaling up, supporting circular economy and protein sovereignty goals.

Which countries are key producers and consumers of feed ingredients?

Germany, France, Spain, and the Netherlands lead in compound feed production, supported by strong grain sectors and advanced feed mills—while Eastern Europe is emerging as a sourcing hub for non-GMO and organic raw materials.

Who are the major players in the European feed ingredients space?

Leading suppliers include ADM, Cargill, BASF, Evonik, DSM-Firmenich, and specialty innovators like Ÿnsect and Protix—combining nutritional science, sustainability credentials, and digital feed formulation tools.

How is sustainability influencing ingredient sourcing?

Buyers prioritize locally sourced, low-carbon-footprint ingredients (e.g., European-grown faba beans, peas) and certified sustainable soy (via ProTerra or RTRS), reducing deforestation risk and transport emissions.

What role do feed additives play in reducing environmental impact?

Phytase enzymes and methane-reducing feed additives (e.g., 3-NOP, approved as Bovaer® in the EU in 2024) help cut phosphorus excretion and enteric methane—supporting the EU’s climate-neutral livestock ambitions.

What challenges does the market face?

Volatile commodity prices, geopolitical disruptions (e.g., Black Sea grain flows), and complex approval processes for novel ingredients can delay innovation and raise feed costs for farmers.

What’s the market outlook for 2025–2030?

The Europe feed ingredients market is set for moderate but transformative growth—driven by precision nutrition, alternative proteins, and regulatory pressure toward greener, healthier, and more transparent animal feed systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com