Europe Furniture Market Size, Share, Trends & Growth Forecast Report By Product, Material, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Furniture Market Size

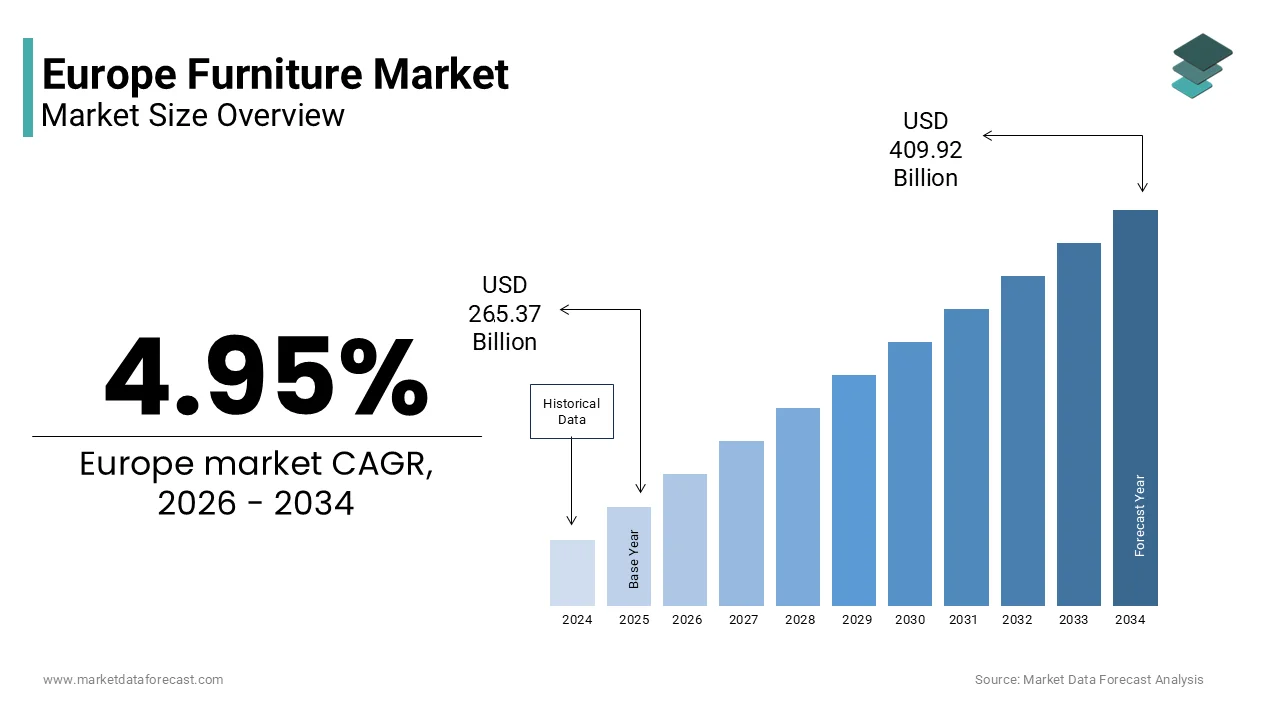

The Europe furniture market size was valued at USD 265.37 billion in 2025, and is projected to reach USD 409.92 billion by 2034 from USD 278.51 billion in 2026, growing at a CAGR of 4.95%.

Furniture refers to movable objects designed to support various human activities such as seating (chairs, sofas), eating (tables), storing items (cabinets, shelves), working (desks), and sleeping (beds). It is characterized by a blend of artisanal craftsmanship, industrial manufacturing, and digital innovation, shaped by cultural heritage, sustainability mandates, and evolving spatial needs. Unlike purely transactional marketsEurope’s furniture sector operates within a regulatory and social framework that prioritizes circularity, transparency, terial trtransparencycy and ergonomic safety. As per the study, a portion of European households reported purchasing at least one new furniture item in 2023, reflecting sustained engagement with home furnishing. Furthermore, the European Commission’s Ecodesign for Sustainable Products Regulation mandates that by 2030, furniture placed on the EU market must be repairable and recyclable, a ble and accompanied by a digital product passport. National policies also influence consumption, with countries promoting design excellence through public grants and export support. This convergence of traditional regulation and lifestyle trends defines the European furniture market as a dynamic ecosystem balancing aesthetic functionality, type, and environmental responsibility.

MARKET DRIVERS

Rising Home Renovation and Interior Refurbishment Activities Drive Demand

Increased investment in home improvement across Europe is a primary driver for the European furniture market. Households prioritize functionality, li, li, ty, and aesthetic renewal. According to sources, a large portion of European households engaged in home renovation projects focused mainly on kitchen and living space improvements. As per studies, many homeowners in Germany have benefited from government-supported energy efficiency programs that include furniture replacement as part of complete home upgrades. As per research, France has widened its national renovation initiative to incorporate built-in furniture, encouraging stronger demand for kitchen furnishings. The post-pandemic shift toward multi-functional living spaces has also amplified demand for modular and space-saving furniture. These structural and policy-driven trends ensure consistent furniture consumption beyond new housing starts.

Strong Cultural Emphasis on Design Aesthetics and Craftsmanship Sustains Premium Segment

Europe’s deep-rooted appreciation for design heritage and artisanal quality continues to fuel demand for high-end and locally made furniture, which propels the expansion of the European furniture market. Countries like Italy, Denmark, and Sweden are globally recognized for their design philosophies, which blend minimal functional,ity, and material integrity. According to sources, Italy’s furniture industry continues to focus on high-end and design-centered products that appeal to both domestic and international buyers. As per studies, Denmark is supporting its small furniture manufacturers through programs that encourage sustainable practices and digital innovation in production. Similarly, Sweden certifies products meeting strict criteria for longevity and ethical production, with certified brands reporting higher customer retention, as per the Swedish Trade Council. This cultural capital transforms furniture from a utilitarian good into an expression of identity and taste, which strengthens willingness to pay for quality and authenticity across generations.

MARKET RESTRAINTS

Escalating Raw Material and Energy Costs Burden Profit Margins

Cost inflation due to volatile prices for wood, metals, and upholstery materials, compounded by high energy expenses, restricts the growth of the rope furniture market. According to the Confederation of European Woodworking Industries, the price of solid beech lumber in the EU increased between 2021 and 2023, driven by supply chain disruptions and increased demand for sustainable timber. Energy costs further strain production. Small workshops are especially vulnerable as they lack the scale to hedge input costs or pass full increases to consumers. These financial burdens limit investment in innovation and force difficult trade-offs between quality, affordability, and sustainability in an already competitive landscape.

Stringent Environmental Regulations Increase Compliance Complexity

environmental regulations that govern material sourcing, emissions, and enend-of-lifeanagement are creating operational and financial burdens, which in turn slow down the expansion of the European furniture market. According to sources, new sustainability regulations in the European Union require furniture products to include detailed digital documentation covering materials and environmental impact. As per studies, manufacturers are facing higher compliance costs due to updated chemical safety requirements that limit the use of certain production materials. Small artisans struggle to afford third-party certifications or lifecycle assessment software. These policies advance circularity even though they disproportionately impact SMEs that form the backbone of Europe’s furniture ecosystem.

MARKET OPPORTUNITIES

Growth of Circular Furniture Models and Resale Platforms Creates New Revenue Streams

The rise of circular economy principles is unlocking new opportunities for the growth of the European furniture market. According to sources, many European furniture brands are introducing buyback and resale programs to encourage product reuse and sustainability. As per studies, laws in France are driving large retailers to incorporate repair or resale services through collaborations with specialized partners. Also, digital platforms are enabling consumers across Europe to lease furniture directly from peers, reflecting growing interest in circular business models. According to sources, the European Union is also funding small manufacturers to adopt modular and repairable product designs that extend furniture lifespan and reduce waste. These models not only reduce waste but also cultivate brand loyalty and recurring revenue in a maturing market.

Expansion of Smart and Multifunctional Furniture for Urban Living Addresses Space Constraints

The proliferation of compact urban dwellings is driving demand for intelligent, adaptable furniture that maximizes utility in limited square footage, and thereby gives fresh prospects for the European furniture market. In addition, companies have integrated motorized mechanisms, wireless charging, and IoT connectivity into modular systems. Besides, public housing authorities in the Netherlands and Austria now specify multifunctional furniture in new social housing units to improve livability. This convergence of urbanization technology and design innovation positions smart furniture as a high-growth frontier.

MARKET CHALLENGES

Intensifying Competition from Low-CNon-EUn EU Imports Threatens Domestic Producers

The mounting burden from imported goods continues to hinder the growth of the European furniture market. It is primarily from Vietnam, Turkey, and China, where labor and environmental compliance costs are significantly lower. According to Eurostat, furniture imports from non-EU countries reached a notable mark by representing an increase, with Vietnam alone accounting for a portion of wooden furniture imports. These products often undercut European prices while bypassing stringent sustainability and safety checks. Despite anti-dumping duties on certain categories, enforcement remains fragmented across member states. This unfair competition erodes market share for European SMEs that invest in certified sustainable wood and fair labor practices, ultimately affecting the EU’s circular economy and green transition goals.

Fragmented Retail Landscape and Digital Disruption Challenge Traditional Distribution

A highly fragmented retail environment, where small independent showrooms compete against global e-commerce giants and direct-to-consumer brands, further hinders the expansion of the European furniture market. According to the European Furniture FFederationover 65 percent of furniture retailers in the EU are micro enterprises with fewer than ten employees, limiting their ability to invest in digital marketing or logistics. According to sources, major e-commerce platforms are dominating Europe’s online furniture market by leveraging competitive pricing and rapid delivery options. Traditional furniture retailers are facing challenges with high return rates for online orders caused by product fit and color discrepancies. As per research, while augmented reality tools are being introduced to improve the digital shopping experience, adoption remains limited due to financial and technical constraints. This digital divide threatens the survival of local retailers who provide tactile experiences and design consultation that algorithms cannot replicate.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.95% |

| Segments Covered | By Product, Material, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | IKEA, BoConcept, B&B Italia, Poltrona Frau, Natuzzi Italia, Ligne Roset, Roche Bobois, JYSK, Maisons du Monde, Steinhoff International, DFS Furniture, Vitra, and others. |

SEGMENTAL ANALYSIS

By Product Insights

The seating furniture segment led the European furniture market by accounting for 38.5% from 2026 to 2034. The prominence of the seating furniture segment is driven by its central role in both residential and commercial environments and high replacement frequency driven by style and comfort preferences. Sofas, armchairs, nd office chairs are essential in living rooms, working spaces, and hospitality venues where ergonomic and aesthetic demands are constant. According to sources, a portion of European households purchased seating, with urban dwellers replacing items every five to seven years on average. The rise of hybrid work further amplifies demand, with a share of home office setups including dedicated ergonomic chairs. Iconic designs from Danish and Italian brands continue to influence trends. This blend of functional necessity, lifestyle evolution, and design prestige sustains seating as the market’s dominant category.

The storage furniture segment is predicted to witness the highest CAGR of 6.7% from 2026 to 2034, owing to urban densification, shrinking living spaces, and the demand for multifunctional interiors. As per EuEurosta, 42 percent of Europeans aged 25 to 34 reside in apartments under 60 square meters, creating an acute need for space-optimizing solutions. National housing policies are also driving this trend. In the Netherlands, the government mandates minimum storage volume in new social housing units, leading to standardized built-inabinetry specifications. Similarlyermany’s urban planning strategy prioritizes infill housing with integrated storage to maximize utility. These structural, demographic, and policy forces position storage furniture as the highest growth segment, addressing Europe’s spatial constraints with intelligent design.

By Material Insights

The wood segment remained the dominant segment of the European furniture market by capturing a 52.6% share in 2025. The growth of the wothe od segment is due to its cultural resonance, aesthetic warmth, and alignment with sustainability values. European consumers consistently prefer solid wood and engineered wood products for their durability and biodegradability. Countries like Sweden and Finland leverage domestic timber resources. The EU’s Ecodesign Regulation further supports wood’s dominance by favoring renewable materials with low embedded carbon. This deep integration of wood into design, heritage, environmental policy, and consumer preference ensures its continued dominance across residential and commercial segments.

The metal segment is estimated to register the fastest CAGR of 7.2% from 2026 to 2034. The rapid growth of the metal segment is driven by industrial design trends demand for durabilityy, and the rise of outdoor and commercial applications. Aluminum and steel are increasingly used in modular seating frames, storage systems, nd outdoor furniture due to their strength, recyclability, and resistance to weathering. According to studies, the use of recycled steel in furniture rose as manufacturers aligned with circular economy mandates. In urban settingmetal-basedsed street furniture such as benches and bike racks saw higher municipal procurement, as per the study. The hospitality sector also favors metal for its low maintenance. Furthermore, Scandinavian brands like Hay and Muuto have popularized minimalist metal designs in residential interiors. These functional and aesthetic advantages position metal as the most dynamic material segment sustainability-conscious market.

REGIONAL ANALYSIS

Germany Market Analysis

Germany was the top performer in the European furniture market by accounting for r2.5% share in 2025. The dominance the Germany is driven by its advanced manufacturing, strong domestic consumption, and prominence in sustainable production. The country hosts numerous furniture companies, including global players like IKEA Germany and regional specialists such as Bulthaup and Rolf Benz. Germany’s stringent environmental regulations mandate that 85 percent of new furniture must be recyclable by 2026, a policy accelerating innovation in modular design. Apart from these, the “Inner Development” urban policy drives demandspace-savingaving furniture in compact city apartments. This combination of industrial capacity, regulatory foresight, and consumer demand strengthens Germany’s market dominance.

Italy Market Analysis

Italy is the second largest in the European furniture market by capturing 18.5% share in 2025. The country is home to iconic brands such as Poltrona Frau B,,&B Italia, nd Cassina that define global aesthetics in high-end residential and contract furniture. According to sources, Italy’s furniture industry remains focused on exporting high-quality and design-driven products that appeal to global markets. As per studies, major design events in Milan continue to strengthen the country’s position as a leading hub for innovation and creativity in furniture design. As per research, government-backed programs are supporting the industry by funding digital development and expanding international promotion efforts. Italian manufacturers also lead in sustainable upholstery using bio-based foams and natural dyes compliant with EU Ecolabel standards. This fusion of artistry, style innovation, and policy support ensures Italy’s enduring influence in global furniture culture.

United Kingdom Market Analysis

The United Kingdom is another key region in the European furniture market due to dynamic retail landscapes, strong e-commerce adoption, and growing interest in British design heritage. London serves as a creative hub with studios like Tom Dixon and Benchmark Furniture blending traditional joinery with contemporary aesthetics. The government’s “Green Homes Grant”, although scaled back, spurred demand for energy-efficient built-in storage and kitchen systems. Besides, the residential living spaces in cities like Manchester and Bristol drive demand for modular and durable furniture. This mix of digital ag, ility design, re,vival and urban innovation sustains the UK’s influential role.

France Market Analysis

France grew steadily in the European furniture market, which is driven by its robust artisanal sector, strong public procurement, and progressive circular economy policies. The country is home to over 8000 furniture works, many specializing in regional styles such as Provençal or Breton craftsmanship. According to sources, public institutions in France are steadily investing in durable and ergonomic furniture to meet long-term use requirements in schools and healthcare facilities. As per studies, new sustainability regulations are driving major retailers to expand into repair and resale initiatives through certified pre-owned product lines. Paris remains a design capital. This balance of traditional regulation and innovation ensures France’s continued relevance in both mass and artisanal furniture segments.

Sweden Market Analysis

Sweden is likely to grow in the European furniture market during the forecast period, owing to its dominance in democratic design,s and flat pack innovation. The country pioneered the concept of affordable functional furniture with IKEA’s global model originating from Älmhult. Swedish brands emphasize timeless aesthetics and repairability. The government’s “Sustainable Consumption” strategy mandates that all public procurement prioritize circular products, which boosted demand for modular office and school furniture. Apart from these, Sweden leads in smart furniture integration with startups like NOD developing IoT-enabled storage for small urban homes. This commitment to accessibility, environmental responsibility user-centered design cements Sweden’s position as a forward-looking furniture market.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the European furniture market are

- IKEA

- BoConcept

- B&B Italia

- Poltrona Frau

- Natuzzi Italia

- Ligne Roset

- Roche Bobois

- JYSK

- Maisons du Monde

- Steinhoff International

- DFS Furniture

- Vitra

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players inEuropeanurope furniture market prioritize circular business models by implementing take-back and a nd refurbishment programs to comply with EU sustainability mandates. They invest in digital transformation through augmented reality room planners, AI-driven customization tools, nd digital product passports for material transparency. Strategic use of certified sustainable materials, such as FFwood andleaderss ensures alignment with eco-conscious consumer preferences. Companies also strengthen local manufacturing to reduce their carbon footprint and support “the ade in Europe” narrative. Besides, they enhance-store experiences with design consultancy services to differentiate from pure e-commerce competitors and build emotional brand connections.

COMPETITION OVERVIEW

The Europe furniture market features intense competition among global mass retail, luxury design houses, and agile digital native brands. IKEA dominates through scale, affordability, nd circular initiative,,s while Italian and Scandinavian brands like Poltrona Frau and BoConcept compete on heritage aesthetics and sustainability. The market is further fragmented by thousands of local artisans and SMEs that cater to niche segments with bespoke offerings. E giants such as Amazon and Wayfair exert pricing burden, particularly in standardized categories, et struggle to replicate tactile experiences and design guidance. Regulatory complexity, including the EU’s Ecodesign Regulation and national ananti-wasteaws creates both barriers and opportunities favoring players with robust compliance systems. Innovation in smart furniture m,, modular design, and circular services is reshaping competitive dynamics with sustainability, ty engagement, and urban adaptability becoming key differentiators. Success requires balancing cost, accessibility, and authenticity in a rapidly evolving consumer landscape.

TOP PLAYERS IN THE MARKET

- IKEA Group is a dominant force in the European furniture market with an extensive retail and manufacturing footprint across the continent. The company revolutionized home furnishing through its flat pack, model democratic design philosophy, and vertical integration from forest to store. These initiatives support IKEA’s global prominence in sustainable, affordable furniture while deepening its integration into Europe’s circular economy framework.

- Poltrona Frau Group is a premier Italian luxury furniture manufacturer renowned for its artisanal craftsmanship and heritage, high-end residential and automotive interiors. The company owns iconic brands including Poltrona Frau C,appellini a, nd Cassina w,hich supply bespoke furniture to global embassies, luxury hotels and design collectors. It also expanded the made-to-order digital configurator across European markets, enhancing customization and reducing waste. These actions support its position as a guardian of European design excellence on the world stage.

- BoConcept is a leading Danish furniture brand specializing in m,, modern mo,dularspace-efficientcient solutions for urban living. BoConcept’s signature approach combines Scandinavian minimalism with personalized in-store design consultations and rapid delivery. It also transitioned its entire upholstery lineGOTS-certifiedfied fabrics and recycled foam. These innovations strengthen BoConcept’s appeal in compact city markets while aligning with Europe’s sustainability and digitalization trends.

MARKET SEGMENTATION

This research report on the European furniture market has been segmented and sub-segmented based on categories.

By Product

- Bedroom Furniture

- Mattresses

- Beds

- Nightstands

- Seating Furniture

- Chairs

- Sofa & Couches

- Others (lounges & recliners)

- Storage Furniture

- Wardrobes & Dressers

- Cabinets & Shelves

- TV Stands/Entertainment Units

- Others (Drawers, Chests, etc.)

- Desk and Tables

- Others

By Material

- Metal

- Wood

- Plastic

- Glass

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe Furniture Market?

The Europe Furniture Market includes the design, manufacturing, and sale of furniture products across residential, commercial, and institutional sectors in European countries.

2. Which countries lead the Europe Furniture Market?

Germany, Italy, France, and the UK are among the largest markets due to strong manufacturing bases and high consumer demand.

3. What are the main types of furniture sold in Europe?

The main types include bedroom furniture, seating furniture, storage furniture, desks and tables, and other specialty furniture items.

4. What materials are commonly used in European furniture?

Key materials include wood, metal, plastic, glass, and composite or other materials.

5. What factors are driving the Europe Furniture Market?

Market growth is driven by rising urbanization, increasing disposable incomes, demand for home remodeling, and the popularity of modern and sustainable furniture designs.

6. Who are the key players in the Europe Furniture Market?

Major players include IKEA, BoConcept, B&B Italia, Poltrona Frau, Natuzzi Italia, Ligne Roset, Roche Bobois, JYSK, Maisons du Monde, Steinhoff International, DFS Furniture, and Vitra.

7. What are the major trends in the Europe Furniture Market?

Trends include growing demand for modular and multifunctional furniture, increasing adoption of sustainable and eco-friendly materials, and the rise of e-commerce and online furniture sales.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com