Europe Glufosinate Market Size, Share, Trends And Growth Forecast Report, Segmented By Crop Type, Form Type, Application and Country (United Kingdom, France, Spain Germany And Italy, Russia, Sweden, Denmark, Switzerland, Netherlands And Rest of Europe), Industry Analysis on From 2026 to 2034

Europe Glufosinate Market Size

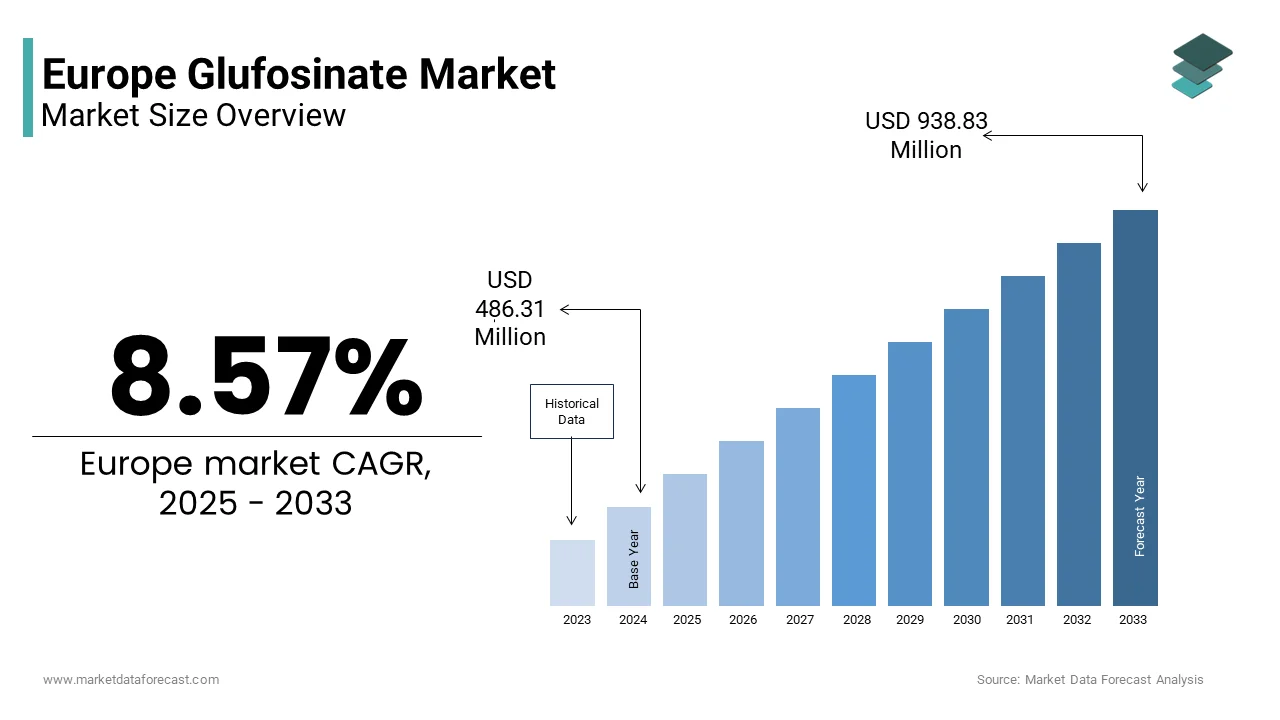

The European glufosinate market size was valued at USD 486.31 million in 2025 and is anticipated to reach USD 527.99 million in 2026 to reach USD 1019.30 million in 2034, growing at a CAGR of 8.57% during the forecast period from 2026 to 2034.

Glufosinate is a non-selective and post-emergence herbicide that inhibits the glutamine synthetase enzyme in plants, which leads to rapid ammonia accumulation and plant death. In Europe, it serves as a vital tool for weed management in non-crop areas, orchards, vineyards, and herbicide-tolerant genetically modified crops grown under controlled authorizations or in research settings. Unlike glyphosate, glufosinate degrades more rapidly in soil and exhibits lower groundwater leaching potential, which aligns with the European Union’s sustainable use directives. As per sources, the European Union has a significant area dedicated to permanent crops, and there is an ongoing scientific and agricultural debate about the effects of various weed control practices, from mechanical tillage to approved herbicides, on soil health and root integrity. Furthermore, the European Commission’s Farm to Fork Strategy targets a 50 percent reduction in chemical pesticide use by 2030, intensifying scrutiny on all active substances yet simultaneously creating demand for targeted, lower-risk alternatives. In Europe's developing framework for weed control, shaped by evolving laws and agricultural methods, glufosinate occupies a position that is complex but strategically significant.

MARKET DRIVERS

Expanded Cultivation of Permanent Crops Drives Selective Herbicide Demand

The steady expansion of high-value permanent crops across the Southern and Western regions of the continent has significantly elevated demand for precise and non-residual herbicides, which in turn boosts the growth of the Europe glufosinate market. Unlike annual row crops, vineyards, olive groves, and fruit orchards require weed control solutions that do not translocate through roots or persist in soil, as residual herbicides can damage perennial plants over time. As per research, the area dedicated to permanent crops across the EU has shown a modest upward trend over the past decade, contrary to potential declines in total agricultural land use. Spain holds a significant majority of the EU's olive grove area, while Spain, France, and Italy collectively represent the vast majority of the European Union's total vineyard surface. These systems favor glufosinate due to its contact activity and rapid soil inactivation, typically within a few weeks under temperate conditions, as per various studies. Besides, glufosinate’s compatibility with mechanical weeding and cover cropping aligns with the EU’s agroecological transition goals. The use of glufosinate is prohibited within the European Union, and sustainability initiatives in countries like Austria and Germany are promoting a general reduction in herbicide reliance within vineyards. This agronomic specificity ensures sustained relevance despite tightening chemical regulations.

Regulatory Preference for Lower Environmental Persistence Enhances Adoption

Glufosinate benefits from a comparatively favorable environmental risk profile that supports its continued authorization in key European countries under the EU’s rigorous pesticide evaluation framework. This further contributes to the expansion of the Europe glufosinate market. Unlike certain persistent herbicides, glufosinate exhibits a soil half-life of several days under aerobic conditions, as per research, which significantly reduces risks of groundwater contamination and off-target drift. This transient behavior aligns with the European Green Deal’s emphasis on reducing long-term chemical residues in ecosystems. The European Environment Agency emphasizes a general shift of widespread pesticide contamination in European water bodies, with ongoing challenges in meeting water quality standards, though monitoring shows some decreasing trends in exceedances for certain substances. National authorities in the EU are required to implement measures and potentially restrict substances with high leaching potential to groundwater, as mandated by directives to manage and reverse pollution trends. Glufosinate is an herbicide on the market, sometimes considered an alternative to other substances, but its use and risk profile are subject to rigorous evaluation and ongoing national authorization processes within the EU regulatory framework. In Germany and across the EU, the authorization of plant protection products is subject to regular renewal processes that involve detailed assessments of environmental fate, including degradation and potential for bioaccumulation, by relevant federal and EU agencies. These regulatory distinctions enable glufosinate to maintain access in environmentally sensitive regions, supporting its role in compliant, sustainable farming systems across Europe.

MARKET RESTRAINTS

Stringent EU Pesticide Approval Process Constrains Long-Term Availability

The European Union’s rigorous pesticide re-authorization regime poses a major constraint for the Europe glufosinate market. This affects the consistent availability of glufosinate across member states. Under Regulation EC 1107 2009, active substances must undergo a comprehensive scientific review by the European Food Safety Authority every few years, with approval contingent on meeting strict toxicological, ecotoxicological, and environmental criteria. As per research, the re-approval process for substances is highly scrutinised, considering new scientific knowledge at the time of renewal. National divergences further complicate access. The EU regulatory system for plant protection products allows for some variation in national-level authorisations and restrictions, even for substances approved at the EU level. This regulatory fragmentation forces farmers to navigate inconsistent legal landscapes, undermining planning certainty. There is an ongoing trend of increased focus on minimizing environmental emissions and residues of plant protection products in the EU. Such uncertainty discourages long-term investment in glufosinate-dependent agronomic systems and incentivizes shifts toward non-chemical alternatives, even where glufosinate remains technically permitted.

Public and Institutional Opposition to Synthetic Herbicides Limits Acceptance

Growing societal aversion to synthetic herbicides in the region exerts substantial pressure on glufosinate use, irrespective of its scientific risk profile, which ultimately hinders the expansion of the Europe glufosinate market. Civil society organizations, organic farming lobbies, and municipal governments increasingly advocate for herbicide-free land management, particularly in public spaces and near residential zones. According to a study, across the EU, there is a consistent and high level of public concern regarding the health and environmental risks associated with pesticide use and chemical exposure in daily life. This sustained public demand for stricter regulations drives EU policy initiatives like the European Green Deal and the Chemicals Strategy for Sustainability. This sentiment translates into policy action. A significant and growing movement exists where numerous local authorities and municipalities across France, Belgium, the Netherlands, and Germany have actively implemented or are working toward local policies to eliminate or significantly reduce synthetic pesticide use in public spaces. These efforts emphasize a push for sustainable alternatives at the local level. Furthermore, major retailers now require suppliers to demonstrate reduced herbicide use in fresh produce supply chains, indirectly discouraging glufosinate adoption. Even in professional agriculture, cooperatives in regions have voluntarily phased out synthetic herbicides in response to consumer demand. These socio-political dynamics create a challenging operational environment where scientific approval does not guarantee social license, constraining market potential despite agronomic utility and regulatory legality in many contexts.

MARKET OPPORTUNITIES

Development of Glufosinate-Tolerant Crop Systems Opens New Avenues

Its role in the European supply chain is indirectly bolstered by permissible food and feed import thresholds and controlled field trials, despite the absence of domestic commercial cultivation of glufosinate-tolerant organisms, which provides new opportunities for the growth of the Europe glufosinate market. The EU imports millions of metric tons of soybeans annually, primarily from Brazil and the United States, where glufosinate-tolerant varieties constitute a portion of the soybean area, as per research. To facilitate these imports, the European Commission has established maximum residue limits for glufosinate in soy meal and oilseed, ensuring compliance with food safety standards. This regulatory accommodation maintains demand for glufosinate in global supply chains that feed European livestock and processing industries. Moreover, Research and regulation in the European Union and France emphasize a shift away from reliance on chemical herbicides like glufosinate-ammonium, which has been phased out due to safety concerns. Glufosinate remains a relevant tool in Europe's agricultural innovation system, sustaining scientific and commercial interest through new developments, all while large-scale GM planting remains politically off the table.

Integration into Non-Chemical Weed Resistance Management Strategies

It is increasingly positioned as a strategic component in herbicide rotation programs designed to combat the rising threat of glyphosate-resistant weeds across the regional farmland, which thereby offers fresh prospects for the expansion of the Europe glufosinate market. Populations of glyphosate-resistant weeds are an increasing concern across Europe, with Italian ryegrass and blackgrass presenting significant challenges in cereal systems in the UK and Germany. Because glufosinate operates via a distinct biochemical mechanism, glutamine synthetase inhibition rather than EPSPS pathway disruption, it remains effective against many glyphosate-resistant biotypes. National integrated pest management guidelines in countries like Spain and the Netherlands now explicitly recommend glufosinate as a rotational partner to delay resistance evolution. Furthermore, its non-systemic activity allows targeted application in inter-row zones of mechanized systems, minimizing overall chemical load. This role in resistance stewardship aligns with the EU’s Sustainable Use Regulation, which mandates anti-resistance strategies for all professional pesticide users. The higher the weed resistance pressure, the more valuable glufosinate becomes as a strategic tool for breaking resistance cycles, elevating its role beyond simple weed control.

MARKET CHALLENGES

Fragmented National Authorization Undermines Market Cohesion

The absence of harmonized national authorizations for glufosinate across the European Union is one of the challenges to the Europe glufosinate market. This creates a fragmented operational environment that complicates supply chain planning and limits economies of scale for distributors. Following EU-level approval of an active substance like glyphosate, individual member states maintain the autonomous authority to determine national product authorizations, allowing them to implement additional restrictions based on localized risk assessments and specific national circumstances. As per research, some EU member states have maintained full authorization for glyphosate, but a considerable number have chosen a different path, applying national-level use restrictions, which include partial bans in specific contexts. The variation in national regulations across EU member states for products containing glyphosate creates logistical challenges for suppliers and distributors, leading to increased operational complexities and costs in managing diverse product inventories and complying with disparate rules. Such inefficiencies deter smaller agrochemical retailers from stocking the product, reducing availability in rural areas. This regulatory heterogeneity not only inflates operational complexity but also erodes farmer confidence in the long-term viability of glufosinate as a reliable weed control option, which ultimately constrains its adoption even where scientifically and legally permissible.

Risk of Regulatory Reclassification Due to Ongoing Toxicological Scrutiny

Glufosinate remains under active scientific review by European regulatory bodies due to unresolved questions about its potential neurodevelopmental effects, despite current approval, which creates uncertainty that deters long-term investment in its use, and negatively impacts the expansion of the Europe glufosinate market. A chemical substance is currently being evaluated for classification as a reproductive or developmental neurotoxin. This assessment follows findings from certain laboratory studies. A separate assessment concluded that no such classification was necessary given expected exposure levels. Advocacy groups continue to propose different information to support stricter regulation of the substance. Multiple jurisdictions formally requested an additional review of the substance's potential neurotoxicity. This request for re-evaluation has led to the need for more information from manufacturers. Such reviews can lead to sudden regulatory shifts. This persistent scientific and political contestation maintains glufosinate in a state of regulatory limbo, discouraging farmers from integrating it into long-term crop plans and prompting manufacturers to diversify their portfolios toward bioherbicides. The lack of a definitive safety assessment will continue to restrain industry expansion and new developments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.57% |

| Segments Covered | By Crop Type, Form, Application, & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | Bayer AG, Nufarm Ltd, E. I. du Pont de Nemours and Company, The Dow Chemical Company, Syngenta AG, UPL, Jiangsu Huangma Agrochemicals Co Ltd., Jiangsu Seven Continent Green Chemical Co Ltd., Zhejiang Yongnong Chem. Ind. Co. Ltd, Hebei Veyong Bio-Chemical Co. Ltd. |

SEGMENTAL ANALYSIS

By Crop Insights

In 2024, the conventional crops segment held the prominent share of the Europe glufosinate market. The near absence of commercial genetically modified crop cultivation in the region and the legal and political landscape have mainly contributed to the dominance of the conventional crops segment. The European Union has a highly restrictive approach to genetically modified (GM) crop cultivation, with only one specific insect-resistant maize variety remaining authorized for commercial planting, and its cultivation area remains minimal across the Member States, according to multiple sources. Consequently, glufosinate is deployed almost exclusively in non-GM systems where it serves as a burndown herbicide in no till or reduced tillage fields and for directed spraying in permanent crops. A further key driver of this segment is its compatibility with integrated weed management in high-value horticulture. For example, in Spain's extensive olive sector, there is a general trend toward adopting integrated weed management strategies that combine mechanical and chemical controls, moving away from a primary reliance on specific herbicides to align with evolving environmental regulations and soil health concerns. These agronomic and regulatory realities firmly anchor glufosinate’s use within conventional agriculture.

The genetically modified crops segment is predicted to witness the highest CAGR of 8.7% from 2025 to 2033. The swift growth of the genetically modified crops segment is fuelled by indirect demand stemming from EU import dependencies and confined research activities. The European Union imports millions of metric tons of soybeans annually, primarily from the Americas, where glufosinate-tolerant varieties now occupy a portion of the soybean area, as per research. To facilitate trade, the European Commission maintains maximum residue limits for glufosinate in imported soy meal used in livestock feed, sustaining global production and thus indirectly the European market. An additional growth driver of this segment is the continuation of authorized field trials under Directive 2001 18 EC. Besides, the European Food Safety Authority’s risk assessments increasingly reference global GM crop data to inform residue tolerances, creating a feedback loop that maintains glufosinate’s regulatory relevance. Political obstacles prevent commercial GM planting, but related research and imports are fostering a small yet growing need for glufosinate applications.

By Form Insights

The liquid formulations segment led the Europe glufosinate market and captured a significant share in 2024. Factors such as superior application efficiency, faster phytotoxic action, and compatibility with modern spray technologies, along with operational practicality, drive the growth of the liquid formulations segment. Liquid glufosinate dissolves readily in water, enabling uniform tank mixing with adjuvants and other agrochemicals, which is essential for integrated pest management. According to research, a notable share of professional sprayers in Western Europe use low-volumetric, high-precision nozzles that require liquid concentrates to avoid clogging, a constraint that dry forms cannot reliably satisfy. Regulatory alignment with drift mitigation policies also propels the growth of this segment. The European Commission’s Directive on Sustainable Use of Pesticides mandates reduced spray drift near water bodies and residential zones, and liquid formulations can be precisely calibrated with anti-drift agents to meet these requirements. Furthermore, national pesticide databases in countries like the Netherlands and France list most of the authorized glufosinate products as liquid concentrates, which reflects regulatory and agronomic preference for this format across professional agriculture.

The dry formulations segment is estimated to register the fastest CAGR of 6.3% over the forecast period, owing to niche demand in non-agricultural settings and logistical advantages in remote areas. These forms are gaining traction in municipal and industrial weed control, where storage stability and transport safety are prioritized over rapid efficacy. A further growth driver is the hazardous substance transport regulations enforced by the European Agreement concerning the International Carriage of Dangerous Goods by Road, which classifies concentrated liquid herbicides as Class 9 hazardous materials. In contrast, solid formulations, water-dispersible granules are exempt, reducing shipping costs and regulatory paperwork, particularly beneficial for distributors in Eastern Europe and Scandinavia. A second factor is extended shelf life. Dry glufosinate retains potency for several months under ambient storage, which makes it ideal for seasonal or infrequent use. These logistical and safety attributes are gradually carving a sustainable niche within Europe’s evolving herbicide landscape.

By Application Insights

The agricultural use segment dominated the Europe glufosinate market by accounting for a substantial share in 2024. Its irreplaceable role in perennial crop systems, resistance management in arable farming, and selective utility in high-value permanent crops, where systemic herbicides pose root damage risks, propel the expansion of the agricultural use segment. Spain's fruit and nut orchard sector relies on glufosinate for targeted weed control between tree rows to preserve soil structure and root health. Italy's vineyard area uses glufosinate in many estates, citing its compatibility with cover cropping and minimal residue persistence. A different driver of this segment is its strategic role in combating glyphosate-resistant weeds. Glufosinate, with its distinct mode of action, is increasingly integrated into pre-sowing burndown programs to reset weed pressure.

The non-agricultural segment is anticipated to witness the fastest CAGR of 9.1% from 2025 to 2033 due to demand from infrastructure maintenance and urban green space management. The use of certain herbicides in public areas is increasing as municipalities seek effective options with specific time limitations. A major reason for this trend is a general regulatory emphasis on minimizing chemical persistence in sensitive environments. Herbicides with a shorter soil half-life are often considered more appropriate compared to those that last longer. These preferred herbicides are being adopted for tasks such as vegetation management near infrastructure like railways, roads, and industrial areas. The adoption of these products helps municipalities comply with regulations regarding the use of persistent chemicals in public spaces. A further growth driver is regulatory exemptions. Under the EU Sustainable Use Directive, non-agricultural applications are permitted in areas where mechanical weeding is unsafe or impractical, such as steep embankments or under power lines. These institutional and environmental factors position non-agricultural use as a high-growth frontier.

COUNTRY ANALYSIS

Spain Glufosinate Market Analysis

Spain was the top performer in the Europe glufosinate market and captured a 24.6% share in 2024. The leading position of the Spanish market is driven by its vast expanse of permanent crops and Mediterranean climate conducive to year-round weed pressure. The country cultivates millions of hectares of olive groves and vineyards, both of which depend on pre-emergent herbicides to protect shallow root systems. Apart from these, Spain faces significant infestations of glyphosate-resistant ryegrass in cereal zones of Castilla y León, prompting agronomists to recommend glufosinate in burndown rotations. The national pesticide registry lists many glufosinate-based products, the highest in Europe, reflecting deep regulatory acceptance. Hence, Spain’s agronomic and climatic conditions create an unmatched demand environment for glufosinate.

France Glufosinate Market Analysis

France was the next prominent country in the Europe glufosinate market and held a 19. 2% share in 2024. Its strong regulatory framework and high density of professional vineyards and orchards have fuelled the growth of the French market. The country maintains a significant number of hectares of vineyards, primarily in Bordeaux and Champagne, where mechanical weeding is often impractical due to vine spacing and slope. Glufosinate is authorized for directed spraying in all permanent crops when strict drift control measures are implemented. It has become a consideration for certified sustainable winegrowers as a potential tool in their practices. Many surveyed vineyards use glufosinate as one component of their integrated weed management strategies. Efforts to reduce reliance on high-risk pesticides may not apply equally to all substances, sometimes making exceptions for those with more favorable environmental profiles. This policy nuance, combined with robust distributor networks in rural regions, sustains consistent demand despite national anti-pesticide sentiment.

Germany Glufosinate Market Analysis

Germany is also a major player in the Europe glufosinate market because of its advanced precision agriculture infrastructure and stringent environmental laws. The country’s viticulture sector, concentrated in the Rhine and Mosel valleys, heavily utilizes glufosinate for targeted weed control to comply with the Federal Soil Protection Act, which prohibits persistent herbicides near waterways. Beyond horticulture, glufosinate is integral to resistance management in cereal farming. A specific agricultural practice is integrated into pre-sowing protocols on many large arable farms in a northern German region to help manage blackgrass challenges. Authorization for a particular substance was renewed in the country, following a rigorous evaluation process that considered data suggesting minimal effects on non-target organisms. This science-led regulatory stance ensures stable market access.

Italy Glufosinate Market Analysis

Italy experienced a consistent growth in the Europe glufosinate market owing to its diverse portfolio of high-value permanent crops and region-specific weed challenges. The country cultivates notable hectares of vineyards and olive groves, particularly in Tuscany and Puglia, where traditional farming practices limit mechanical intervention. Glufosinate is widely applied in perennial agricultural systems and is a favored herbicide following the use of glyphosate. This preference is attributed to its effective contact action and the characteristic lack of translocation into plant roots. A significant portion of agricultural producers, particularly olive growers in southern regions, use glufosinate to manage various invasive species without causing harm to tree roots. Apart from these, Italy faces severe infestations of Sorghum halepense in maize fields, which shows cross-resistance to multiple herbicide classes, making glufosinate a critical rotation tool. Regional pesticide regulations in Lombardy and Emilia Romagna explicitly permit its use in buffer zones, further supporting adoption. These localized agronomic needs sustain steady demand despite national scrutiny on synthetic inputs.

Netherlands Glufosinate Market Analysis

The Netherlands is anticipated to expand in the Europe glufosinate market over the forecast period due to its export-focused greenhouse and open field horticulture sectors and progressive chemical management policies. The country manages large hectares of open field vegetables, fruits, and ornamentals, many destined for European supermarket supply chains that require residue compliance and sustainable certification. Dutch growers value its rapid rainfastness, effective within two hours, as critical in the country’s high precipitation climate. Furthermore, the Netherlands leads in digital agriculture. Professional farms are using advanced spray robo, which favor liquilow-drift formulations that align with the physical properties of glufosinate. The use of glufosinate has increased as part of a strategy for managing resistance in rotations involving bulb and potato crops. This blend of export quality demands, climate adaptation, and technological integration solidifies the Netherlands as a high-value market.

COMPETITIVE LANDSCAPE

Competition in the Europe Glufosinate Market is shaped by a handful of global agrochemical firms that leverage deep regulatory expertise, manufacturing scale, and agronomic credibility rather than price competition. The market remains highly sensitive to regulatory developments, with participants continuously generating environmental and toxicological data to defend the substance’s approval status. Differentiation occurs through formulation science—enhancing efficacy under European climatic conditions—and stewardship services that support integrated weed management. While generic suppliers from Asia have entered the technical ingredient space, branded players retain influence through trusted product performance and compliance support. Geographic disparities in national authorizations create fragmented commercial landscapes, requiring localized strategies. Companies also face indirect competition from mechanical weeding and bioherbicides, prompting innovation in precision application and resistance management positioning. Overall, sustained market presence hinges on scientific engagement, regulatory agility, and alignment with Europe’s sustainability-driven agricultural transformation.

KEY MARKET PLAYERS

Some of the major companies dominating the Glufosinate market include

- Bayer AG

- BASF SE

- Nufarm Ltd

- E. I. du Pont de Nemours and Company

- The Dow Chemical Company

- Syngenta AG

- UPL

- Jiangsu Huangma Agrochemicals Co Ltd.

- Jiangsu Seven Continent Green Chemical C,o Ltd.

- Zhejiang Yongnong Chem. Ind. Co. Ltd

- Hebei Veyong Bio-Chemical o.,, Ltd.

Top Players In The Market

- BASF SE is a global leader in crop protection and a key innovator in glufosinate-based herbicide solutions. The company markets glufosinate under its well-established Liberty brand and supplies both formulated products and technical grade active ingredient to partners worldwide. In Europe, BASF maintains strong regulatory dossiers across major agricultural countries and actively engages in stewardship programs to promote responsible use. It also collaborated with European research institutes to generate field data supporting its environmental safety profile, reinforcing its position amid tightening pesticide regulations.

- Bayer AG plays a pivotal role in the global glufosinate ecosystem through its legacy LibertyLink technology and ongoing stewardship of the active substance. Although genetically modified LibertyLink crops are not cultivated in Europe, Bayer continues to support the herbicide’s use in conventional and non-agricultural settings across the region. The company has invested in reformulating glufosinate products to enhance rainfastness and reduce drift potential, aligning with EU sustainable use directives. These efforts underscore its commitment to maintaining glufosinate’s relevance within integrated weed control strategies.

- UPL Limited has emerged as a significant participant in the Europe Glufosinate Market by leveraging its global manufacturing scale and regulatory expertise. The company supplies technical glufosinate and co-formulated products to European distributors under strict compliance with EU biocidal and pesticide regulations. UPL’s strategy focuses on affordability and logistical reliability, particularly in Southern and Eastern Europe, where cost sensitivity influences procurement. It also partnered with local agronomic advisors to deliver field demonstration trials on glyphosate-resistant control, strengthening trust among professional users and reinforcing its presence in Europe’s evolving herbicide landscape.

Top Strategies Used By The Key Market Participants

Key participants in the Europe Glufosinate Market prioritize regulatory compliance and scientific substantiation to maintain product authorizations amid stringent EU pesticide policies. They invest in field-based agronomic trials to demonstrate environmental safety and resistance management benefits, supporting national approval processes. Companies reformulate products to reduce drift, enhance rainfastness, and improve user safety in alignment with the Sustainable Use Directive. Strategic partnerships with local distributors and agronomic advisors ensure region-specific adoption and technical support. Additionally, firms leverage digital platforms to deliver application guidance, stewardship training, and resistance monitoring tools, enhancing professional user confidence and promoting responsible use across diverse European cropping systems.

MARKET SEGMENTATION

This market research report on the European glufosinate market is segmented and sub-segmented into the following categories.

By Crop Type

- Genetically Modified Crops

- Conventional Crops

By Form

- Liquid

- Dry form

By Application

- Agricultural

- Non-agricultural

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is glufosinate used for?

Glufosinate is a non-selective herbicide used to control broadleaf weeds and grasses in agriculture, horticulture, and specialty crops.

Why is glufosinate demand increasing in Europe?

Farmers are turning to glufosinate as an alternative due to restrictions on other herbicides and rising herbicide-resistant weeds.

Which crops commonly use glufosinate in Europe?

It is widely used in vineyards, orchards, cereals, oilseeds, vegetables, and specialty crops grown under integrated weed management programs.

How does glufosinate compare to glyphosate?

Glufosinate is often used when glyphosate resistance becomes an issue and is preferred in crops where contact-based weed control is needed.

What regulatory factors influence the Europe glufosinate market?

EU pesticide regulations, safety assessments, and residue limits significantly impact product approvals and usage patterns.

Which countries lead glufosinate consumption in Europe?

France, Germany, Spain, and Italy remain key users due to extensive fruit, vegetable, and vineyard cultivation.

What challenges does the market face?

Stringent regulatory scrutiny, concerns over toxicity, rising compliance costs, and limited product alternatives in some regions.

Are safer or bio-based weed control options affecting demand?

Yes, growing interest in bio-herbicides and mechanical weed control is influencing long-term market dynamics.

How is technology improving glufosinate application?

Precision spraying systems, drone-based weed monitoring, and AI-driven decision tools are helping optimize herbicide efficiency.

What is the future outlook for the Europe glufosinate market?

Moderate growth is expected as farmers seek glyphosate alternatives, but evolving EU regulations will shape adoption levels.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com