Global Glufosinate Market Size, Share, Trends, & Growth Forecast Report, Segmented By Crop Type (Genetically Modified Crops And Conventional Crops), Form (Liquid And Dryform), Application (Agricultura And Non-Agricultural), And By Region (North America, Europe, Asia Pacific, Latin America, Middle East And Africa), Industry Analysis from 2025 to 2033

Global Glufosinate Market Size

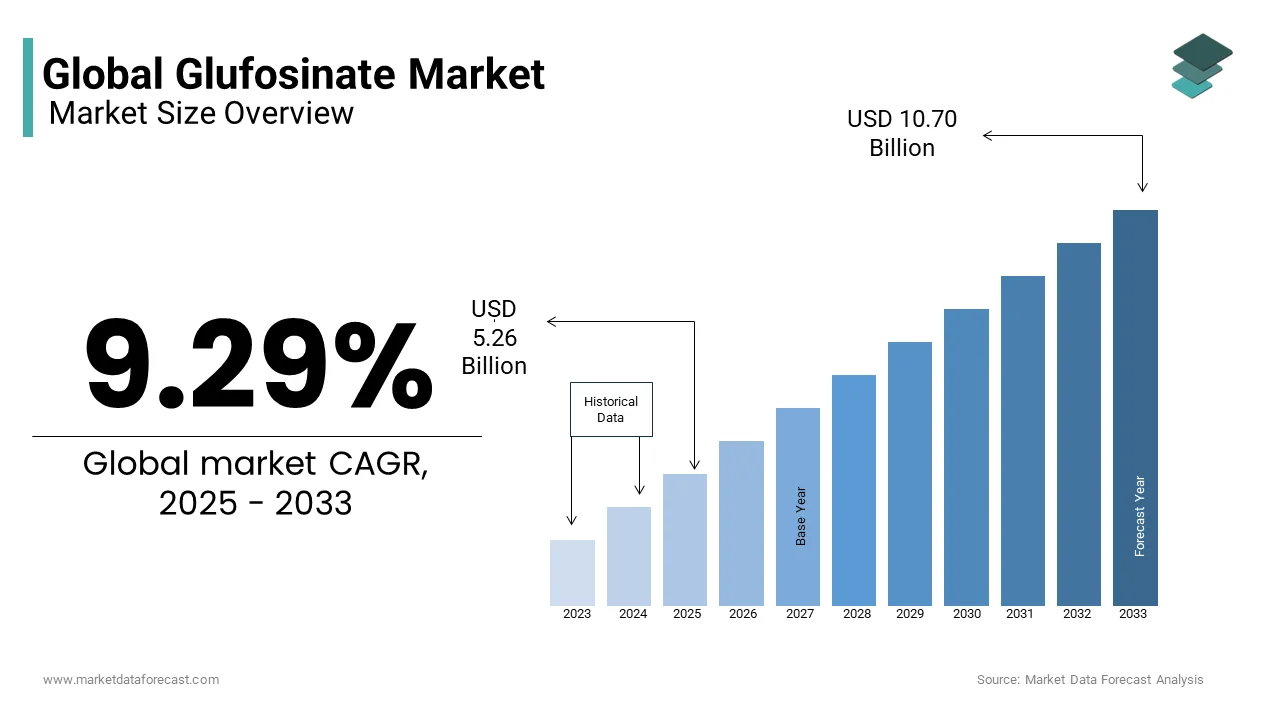

The global glufosinate market size was valued at USD 4.81 billion in 2024 and is anticipated to reach USD 5.26 billion in 2025 from USD 10.70 billion by 2033, growing at a CAGR of 9.29% during the forecast period from 2025 to 2033.

Glufosinate is a broad-spectrum, non-selective herbicide widely deployed in modern agriculture for effective weed control in genetically modified and conventional cropping systems. Chemically classified as a phosphinic acid derivative, it functions by inhibiting glutamine synthetase, thereby disrupting ammonia detoxification and photosynthesis in targeted plants, leading to rapid desiccation. Unlike glyphosate, glufosinate exhibits no soil residual activity and degrades primarily via microbial action, reducing long-term environmental persistence. According to sources, multiple countries have approved glufosinate for agricultural use, with registration in major economies reflecting its global agronomic relevance. The compound is particularly important in glufosinate-tolerant crop systems, where it enables crop weed management without a yield penalty. As per the International Survey of Herbicide-Resistant Weeds, many weed species globally have evolved resistance to glyphosate, which accelerates farmer reliance on alternative modes of action such as glufosinate. Regulatory evaluations by the European Food Safety Authority and the U.S. Environmental Protection Agency consistently reaffirm its favorable toxicological profile when applied according to label instructions, distinguishing it from more contentious herbicidal chemistries. Its role extends beyond row crops into orchards, vineyards, and industrial vegetation management, which emphasizes its status as a cornerstone of integrated weed resistance management strategies.

MARKET DRIVERS

Escalating Global Prevalence of Glyphosate-Resistant Weeds Necessitating Alternative Herbicide Adoption

The unchecked proliferation of glyphosate-resistant weed biotypes has rendered glufosinate indispensable in global crop production systems, which is driving the growth of the glufosinate market. It compels farmers to adopt it as a primary resistance management tool. According to studies, many weed species in countries have developed confirmed resistance to glyphosate, with Palmer amaranth and waterhemp affecting millions of acres of cropland. Also, Australian grain growers face similar pressures. Regulatory agencies endorse this shift. The U.S. Environmental Protection Agency recommends herbicide rotation with differing modes of action to delay resistance, embedding glufosinate into federal Best Management Practices. This structural dependency transcends price sensitivity, which drives demand in agronomic necessity rather than discretionary input choice.

Expansion of Glufosinate Tolerant Crop Adoption Accelerating In Crop Application Volumes

The commercial rollout of genetically engineered crops tolerant to glufosinate has fundamentally transformed their usage pattern from a burndown or directed spray herbicide to a systemic in-crop solution, which propels the expansion of the glufosinate market. This dramatically increases application frequency and volume. According to research, millions of hectares of glufosinate-tolerant crops were planted globally, with soybeans, corn, and cotton accounting for a portion of total acreage. Seed companies strengthen this trend through bundled trait packages. Corteva’s Enlist E3 soybeans combine glufosinate tolerance with resistance to 2,4-D and glyphosate, enabling multi-mode sequential applications. This genetic integration ensures recurring and non-substitutable demand directly tied to seed purchase decisions rather than standalone herbicide economics.

MARKET RESTRAINTS

Regulatory Uncertainty and Reapproval Delays in Key Agricultural Jurisdictions

Regulatory headwinds in several major agricultural regions are restricting the growth of the glufosinate market. This creates uncertainty that constrains investment, formulation innovation, and long-term farmer adoption. The European Union’s reapproval process for glufosinate ammonium has been repeatedly delayed since 2018, with the European Food Safety Authority still evaluating updated toxicological dossiers as of early 2024, which leaves its legal status in limbo across 27 member states. In Canada, the Pest Management Regulatory Agency extended its special review of glufosinate in 2023, citing concerns over potential endocrine disruption, despite Health Canada’s earlier 2019 conclusion affirming safety under labeled conditions. These regulatory vacillations deter agrochemical manufacturers from expanding production capacity or developing new formulations, as evidenced by BASF’s announced plans to cease production of glufosinate-ammonium at its Knapsack and Frankfurt sites in Germany by the end of 2024. Farmers respond by stockpiling existing inventories or shifting to alternative chemistries, which fragments demand and affects supply chain predictability even in regions where scientific consensus supports continued use.

Competition From Emerging Bioherbicides and Integrated Mechanical Weed Control Systems

The agricultural input sector is witnessing accelerated investment in non-chemical weed management technologies, which further constrains the expansion of the glufosinate market. As a result, this leads to a tangible substitution burden against synthetic herbicides, including glufosinate. According to research, the adoption of cover cropping for weed suppression increased among row crop farmers between 2020 and 2023, which reduced herbicide dependency. Startups have deployed autonomous robotic weeders utilizing computer vision and mechanical or laser-based elimination, with a large number of units in operation. Bioherbicide innovation is advancing rapidly. Even conventional growers are adopting integrated strategies. This diversification dilutes glufosinate’s market exclusivity and forces price compression to retain share against non-chemical alternatives, gaining agronomic credibility and consumer acceptance.

MARKET OPPORTUNITIES

Strategic Deployment in Herbicide Resistance Management Programs as a Stewardship Tool

It is increasingly positioned as a scientifically endorsed stewardship agent within formal resistance management frameworks by creating institutional and regulatory demand beyond pure efficacy, which provides new opportunities for the growth of the glufosinate market. According to the Weed Science Society of America, 89 percent of university extension weed management guides now designate glufosinate as a Group 10 herbicide essential for rotating modes of action in glyphosate-dominated systems. The United States Department of Agriculture’s Natural Resources Conservation Service includes glufosinate application in its Conservation Stewardship Program, offering financial incentives to farmers who adopt resistance delaying practices. Bayer and BASF have partnered with land grant universities to develop region-specific resistance management protocols, embedding glufosinate into digital agronomy platforms. Regulatory agencies support this positioning. The Australian Pesticides and Veterinary Medicines Authority requires resistance management plans for all new herbicide registrations, with glufosinate routinely included as a cornerstone component. This institutionalization transforms glufosinate from a commodity input into a compliance tool, which ensures baseline procurement regardless of short-term price fluctuations or competitive burdens.

Penetration Into High-Value Specialty Crop and Non-Crop Vegetation Management Segments

It is gaining traction in specialty horticulture, orchards, vineyards, and industrial vegetation control, offering distinct agronomic advantages due to its lack of soil residual activity and rapid degradation profile beyond its use in row crops, which opens fresh opportunities for the expansion of the glufosinate market. In Europe, despite regulatory uncertainty in agriculture, glufosinate remains approved for non-crop uses. Specialty crop growers value its lack of volatility and crop safety when applied with shielded sprayers. This diversification reduces reliance on genetically modified crop systems and opens premium-priced and less commoditized market segments.

MARKET CHALLENGES

Persistent Public and Retailer Perception Linking Synthetic Herbicides to Environmental Degradation

Consumer and retailer campaigns conflating synthetic herbicides with ecological harm hinder the growth of the glufosinate market. On the contrary, scientific evaluations show glufosinate is safe. Major food retailers, including Walmart, Tesco, and Carrefour, have adopted sustainable sourcing policies that penalize or exclude suppliers using non-organic herbicides, regardless of regulatory approval or environmental fate data. Foodservice giants mandate herbicide use reduction in their supply chains, which pressures growers to adopt mechanical or biological alternatives even when less effective. Non-governmental organizations, including the Pesticide Action Network, continue to petition regulatory agencies for bans, citing outdated or misinterpreted toxicology data. This reputational risk forces agrochemical manufacturers to invest heavily in stewardship communications and third-party sustainability certifications, which diverts resources from innovation. Farmers, particularly those supplying branded value chains, increasingly avoid glufosinate not due to agronomic failure but to maintain market access, creating demand erosion independent of scientific or regulatory reality.

Technical Limitations in Efficacy Against Perennial and Deep-Rooted Weed Species

Inconsistent control against established perennial species with extensive root systems or rhizomatous growth habits, which limits its utility in certain cropping systems and thereby obstructs the expansion of the glufosinate market. As per the Australian Herbicide Resistance Initiative, mature Johnson grass and nut sedges require two to three sequential glufosinate applications for suppression, which increases input costs and operational complexity. In orchard systems, University of California Cooperative Extension data show that repeated glufosinate use selects for tolerant biotypes of bermudagrass and dallisgrass, reducing long-term efficacy. Unlike systemic herbicides, glufosinate lacks root translocation, relying solely on foliar contact and requiring thorough spray coverage for consistent results, a challenge in dense canopies or windy conditions. Equipment calibration errors further reduce field performance. As per the American Society of Agricultural and Biological Engineers, 38 percent of self-propelled sprayers exhibit application inaccuracies exceeding 15 percent, compromising weed control. These biological and operational constraints necessitate tank mixing or sequential applications with other herbicides, increasing complexity and cost, and reducing glufosinate’s standalone value proposition in perennial weed-dominated environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.29% |

| Segments Covered | By Crop Type, Form, Application, and Region |

| Various Analyses Covered | Global, Regional, and andCountry-Levell Analysis, Segment-Level Analysis. DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Bayer, Syngenta, BASF, Dow AgroSciences, Monsanto (acquired by Bayer), Adama Agricultural Solutions, Nufarm, FMC Corporation, UPL Limited, Corteva Agriscience, Sipcam-Oxon, Jiangsu Huangma Agrochemicals, Zhejiang YongNong BioSciences, Nanjing Red Sun Co., Ltd., Zhejiang Wynca Chemical Industrial Group Co., Ltd., Nantong Jiangshan Agrochemical & Chemicals, Shandong Weifang Rainbow Chemical Co., Ltd., Rainbow Chemical, Lianyungang Liben Crop Science and Technology Co., Ltd. |

SEGMENTAL ANALYSIS

By Crop Insights

The genetically modified crops segment dominated the glufosinate market by accounting for a substantial share in 2024. The dominance of the genetically modified crops segment is driven by the global expansion of herbicide-tolerant trait platforms, particularly in soybean, corn, and cotton systems, where crop weed control is non-negotiable for yield preservation. As per studies, millions of hectares of glufosinate-tolerant crops were cultivated worldwide, with soybeans representing a portion of the total acreage. Canadian canola adoption is accelerating. Seed trait bundling strengthens dependency. Corteva’s Enlist E3 soybeans combine glufosinate tolerance with resistance to 2,4-D and glyphosate, which ensures recurring herbicide purchases tied to seed selection rather than standalone agronomic choice.

The conventional crop segment is predicted to witness the highest CAGR of 9.8% from 2025 to 2033. The rapid expansion of the conventional crop segment is propelled by its utility as a non-residual, contact-acting herbicide in crops where genetic modification is restricted or undesired, particularly in vegetables, orchards, vineyards, and organic transition systems. In Europe, where genetically modified crop cultivation remains minimal, glufosinate is approved for directed spraying in conventional orchards and industrial fallows. Australia’s vegetable sector is adopting glufosinate for stale seedbed preparation in lettuce and broccoli. Specialty crop growers value its rapid degradation profile, which allows planting within days post-application, as per sources. Regulatory agencies in Japan and South Korea permit glufosinate use in conventional rice and vegetable systems, further expanding its non-GM footprint. This growth reflects diversification beyond trait-dependent systems into precision and label-compliant applications where residual activity and volatility are unacceptable.

By Form Insights

The liquid formulations segment led the glufosinate market by capturing a significant share in 2024. Factors such as superior field efficacy, ease of tank mixing, compatibility with modern spray equipment, and established farmer familiarity across all major agricultural regions have significantly contributed to the liquid formulations segment. Liquid concentrates, typically formulated as ammonium salts, offer precise dilution control and uniform droplet distribution, vital for contact herbicides requiring thorough foliar coverage. According to sources, a portion of self-propelled and pull-type sprayers are calibrated for liquid application, with only a small portion equipped for dry product handling. Tank mixing with adjuvants, surfactants, and other herbicides is streamlined in liquid form, with university extension services recommending specific premix ratios to enhance weed control. Regulatory approvals also favor liquids. Storage, handling, and application infrastructure globally is optimized for liquids, which makes substitution economically and logistically impractical for most growers.

The dry formulations segment is estimated to register the fastest CAGR of 11.3% during the forecast period. The demand in water-scarce regions, smallholder farming systems, and specialty crop sectors, where liquid handling poses logistical or environmental challenges, is boosting the expansion of the dry formulations segment. According to research, dry formulations reduce water usage per hectare while maintaining efficacy against weedy rice and barnyardgrass. In sub-Saharan Africa, development agencies promote dry glufosinate sachets for small plot vegetable production. Dry forms also reduce transport weight and storage volume, important in remote areas with poor road infrastructure. BASF and UPL have launched dispersible granule products in Southeast Asia, where monsoon season humidity compromises liquid storage stability. Regulatory advantages exist in Europe, where dry formulations face fewer volatile organic compound restrictions. This niche expansion caters to underserved agronomic and geographic segments, which unlocks volume beyond traditional large-scale row crop markets.

By Application Insights

The agricultural uses segment held the leading share of the glufosinate market in 2024. The growth of the agricultural uses segment is fuelled by its irreplaceable role in modern weed management systems across row crops, vegetables, orchards, and plantations, where chemical control remains the most scalable and economically viable solution. Canadian canola, Argentine sunflower, and Australian wheat systems increasingly integrate glufosinate into resistance management programs. Specialty crops further anchor demand. Unlike non-agricultural uses, agricultural demand is recurrent, seasonally predictable, and tied to crop value, ensuring baseline volume stability even amid regulatory or pricing burdens.

The non-agricultural applications segment is anticipated to witness the fastest CAGR of 12.6% from 2025 to 2033. The expansion of the non-agricultural applications segment is led by its non-residual, non-staining, and low volatility profile, making it ideal for sensitive environments where soil persistence or chemical drift is unacceptable. Railway operators across North America and Europe increasingly specify glufosinate for trackside weed control. Utility companies follow suit. Municipalities are adopting it for sidewalk, park, and cemetery maintenance. Golf courses value their turf safety. Industrial sites, solar farms, and airport runways complete the demand matrix, where rapid burndown without soil contamination is mandatory. This diversification reduces reliance on agricultural cycles and opens institutional procurement channels with multi-year contracts.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer in the global glufosinate market in 2024 and occupied 35.7% in 2024. The domination of North America in the global market is primarily driven by the widespread cultivation of glufosinate-tolerant crops, particularly soybeans and corn, combined with escalating glyphosate resistance that necessitates alternative modes of action. Canada’s canola sector is rapidly adopting glufosinate-tolerant hybrids. The U.S. Environmental Protection Agency reaffirmed glufosinate’s registration in 2022 with no use restrictions, while Health Canada completed its re-evaluation in 2023, affirming safety under labeled conditions. Retail distribution is highly developed, with agrochemical outlets stocking glufosinate formulations. Farmer education programs led by land grant universities embed glufosinate into resistance management curricula, which ensures protocol compliance. The region’s market is characterized by high-per-acre intensity, trait integration, and institutional support by making it the most mature and volume-dense glufosinate market globally.

Latin America Market Analysis

Latin America was the second largest region of the glufosinate market by capturing 30.5% in 2024. Brazil is a key driver, with its vast soybean, corn, and cotton acreage confronting some of the world’s most aggressive glyphosate-resistant weed populations. Embrapa, Brazil’s agricultural research corporation, estimates that sourgrass and horseweed infest over millions of hectares of soybeans, reducing yields without glufosinate intervention. Argentina follows with large acres of glufosinate-tolerant soybeans, while Paraguay and Uruguay show accelerating adoption. Aerial application dominates. Regulatory frameworks are pragmatic. Import dependency remains high, but local formulation plants by BASF and Bayer are expanding to reduce logistics costs. Latin America’s growth is fueled by biological necessity, scale, and regulatory pragmatism, which makes it the most dynamic and volume-expansive region globally.

Asia Pacific Market Analysis

Asia Pacific is an attractive region in the global glufosinate market due to herbicide resistance in rice and wheat systems, expansion of vegetable exports, and limited adoption of genetically modified crops outside of India and the Philippines. As per sources, increasing adoption in Vietnam and Thailand for stale seedbed preparation in rice by reducing labor costs compared to manual weeding. China restricts glufosinate to non-food industrial uses but permits its application in orchards and tea plantations. Japan and South Korea approve glufosinate in conventional vegetables and fruits, where residue tolerances are strictly enforced. Australia’s grains sector is a bright spot. The region’s diversity in regulation, crop systems, and farm size creates a mosaic of demand drivers rather than a unified market.

Europe Market Analysis

Europe grew moderately in the global glufosinate market. Agricultural use is minimal due to political restrictions on genetically modified crops, but non-crop and specialty horticulture applications sustain demand. France, Spain, and Italy permit directed spraying in vineyards, orchards, and olive groves. Germany suspended agricultural authorizations in 2020 but allows non-crop use, which creates a regulatory patchwork. The European Food Safety Authority continues evaluating reapproval dossiers, delaying investment but not eliminating demand. Organic transition farms increasingly use glufosinate for burndown before certification, as permitted under EU transitional rules. Eastern European nations, including Poland and Romania, as shown adoption in conventional sunflower and rapeseed. Europe’s market is defined by regulatory fragmentation, niche horticultural value, and institutional vegetation management, which makes it low volume but high value per liter.

Middle East and Africa Market Analysis

The Middle East and Africa region is likely to expand in the glufosinate market from 2025 to 2033. Demand is concentrated in commercial export agriculture and infrastructure maintenance rather than subsistence farming. South Africa leads adoption, with the Agricultural Research Council documenting increased use of siglufosinate-tolerant maize and soybeans to combat glyphosate-resistant weeds in the Highveld region. Egypt permits glufosinate in cotton and vegetables under strict supervision. Kenya and Tanzania are emerging markets, where development agencies promote water-soluble powder formulations for smallholder vegetable production, reaching a large number of farmers, as per studies. Gulf Cooperation Council nations use glufosinate for airport runways, pipelines, and roadside maintenance, valuing its rapid degradation in high-temperature environments. Saudi Arabia’s Ministry of Environment, Water, and Agriculture includes glufosinate in its approved list for date palm orchards and alfalfa fields.

COMPETITIVE LANDSCAPE

The gasoline fuel additives market is characterized by oligopolistic competition among global chemical conglomerates and specialized formulation houses vying for refinery and aftermarket channel dominance. Major players differentiate through proprietary detergent, corrosion inhibitor, and octane booster chemistries tailored to regional fuel specifications and engine technologies. Strategic acquisitions of regional blenders and distribution networks consolidate market access while reducing logistics costs. Innovation cycles are dictated by tightening emissions regulations and automaker fuel performance standards demanding cleaner combustion and reduced intake valve deposits. Joint ventures with national oil companies embed additives into fuel streams at source, locking out independent suppliers. Price competition is intense in commoditized segments like metal deactivators, while premium margins are preserved in performance and multifunctional additives. Market leaders invest in real-time refinery analytics to align additive dosing with crude feedstock variability. Emerging economies witness aggressive penetration pricing to capture volume before regulatory harmonization. Sustainability narratives drive bio-based additive development.

KEY MARKET PLAYERS

A few of the market players in the global glufosinate market include

- Bayer

- Syngenta

- BASF

- Dow AgroSciences

- Monsanto (acquired by Bayer)

- Adama Agricultural Solutions

- Nufarm

- FMC Corporation

- UPL Limited

- Corteva Agriscience

- Sipcam-Oxon

- Jiangsu Huangma Agrochemicals

- Zhejiang YongNong BioSciences

- Nanjing Red Sun Co., Ltd.

- Zhejiang Wynca Chemical Industrial Group Co., Ltd.

- Nantong Jiangshan Agrochemical & Chemicals

- Shandong Weifang Rainbow Chemical Co., Ltd

- Rainbow Chemical

- Lianyungang Liben Crop Science and Technology Co., Ltd

Top Players in the Market

- BASF is a global leader in glufosinate manufacturing and innovation, supplying both technical grade active ingredient and formulated end-use products under its Liberty and Basta brands. The company operates proprietary production facilities in Europe and North America, ensuring supply chain resilience and quality control. It also launched a next-generation low-drift formulation and is co-developed with local agronomists. BASF continues to invest in stewardship programs by partnering with universities to promote resistance management and proper application techniques across major cropping regions.

- Bayer plays a pivotal role in the glufosinate market through its LibertyLink genetically modified trait platform and complementary herbicide formulations. The company integrates glufosinate into its digital farming ecosystem, enabling precision application recommendations via its Climate FieldView platform. It also strengthened its regulatory dossier in key Asian markets by securing approvals for expanded use in vegetables and orchards. Bayer’s strategy centers on trait herbicide bundling, which ensures recurring demand through seed technology adoption rather than standalone chemical sales.

- UPL is a major global supplier of glufosinate formulations, particularly in price-sensitive and emerging markets across Asia, Africa, and Latin America. The company leverages its extensive distribution network and localized manufacturing to offer cost-effective, region-specific product formats, including water-dispersible granules and soluble powders. It also secured regulatory registration for glufosinate in three new African countries and partnered with national agricultural extension services to train farmers on resistance management. UPL’s strength lies in accessibility, formulation flexibility, and grassroots education in underserved markets.

Top Strategies Used By Key Market Participants

Leading participants in the glufosinate market prioritize backward integration into active ingredient manufacturing to ensure cost control and supply security amid volatile raw material markets. They invest heavily in formulation science to develop low-drift, rainfast, and tank-mix compatible products tailored to regional application methods. Strategic bundling with genetically modified seed traits creates recurring, non-substitutable demand tied to planting decisions. Companies expand regulatory footprints aggressively, securing approvals in emerging economies where herbicide resistance is escalating. Digital agriculture integration enables precision recommendation engines that drive product adoption through farm management platforms. Stewardship programs in partnership with universities and extension services support proper use and delay resistance evolution. Geographic diversification reduces dependency on politically volatile regions such as Europe. Partnerships with aerial applicators and equipment manufacturers optimize delivery systems. Product line extensions into non-crop and specialty segments capture premium pricing. Sustainability narratives emphasize rapid degradation and low environmental persistence to counter activist narratives.

MARKET SEGMENTATION

This research report on the global glufosinate market is segmented and sub-segmented into the following categories.

By Crop

- Genetically Modified Crop

- Conventional Crop

By Form

- Liquids

- Dry forms

By Application

- Agriculture

- Non-agriculture

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

Which regions are leading in terms of market share for glufosinate herbicides?

North America and Europe currently hold the largest market share for glufosinate herbicides, driven by extensive use in agricultural and non-agricultural applications.

What factors are hindering the growth of the glufosinate market in Asia Pacific?

In Asia Pacific, factors such as stringent regulatory requirements, increasing awareness about environmental and health concerns, and competition from other herbicides are hindering the growth of the glufosinate market.

Who are the key players dominating the glufosinate market in Europe?

Companies such as Bayer AG, Syngenta AG, and UPL Limited are among the key players dominating the glufosinate market in Europe.

How is the adoption of glufosinate-tolerant crops influencing the glufosinate market in North America?

The adoption of glufosinate-tolerant crops such as soybeans, corn, and cotton is driving the demand for glufosinate herbicides in North America to control weeds effectively.

What are the emerging opportunities for glufosinate herbicides in Africa's agriculture sector?

The emerging opportunities for glufosinate herbicides in Africa's agriculture sector include increasing adoption of GM crops, expansion of commercial farming operations, and rising demand for herbicides to combat resistant weeds.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com