Europe Glycolic Acid Market Size, Share, Trends & Growth Forecast Report By Grade, Application, and By Country (Germany, France, Italy, United Kingdom, Spain & Rest of Europe) – Industry Analysis and Forecast, 2025 to 2033

Europe Glycolic Acid Market Summary

Market Highlights

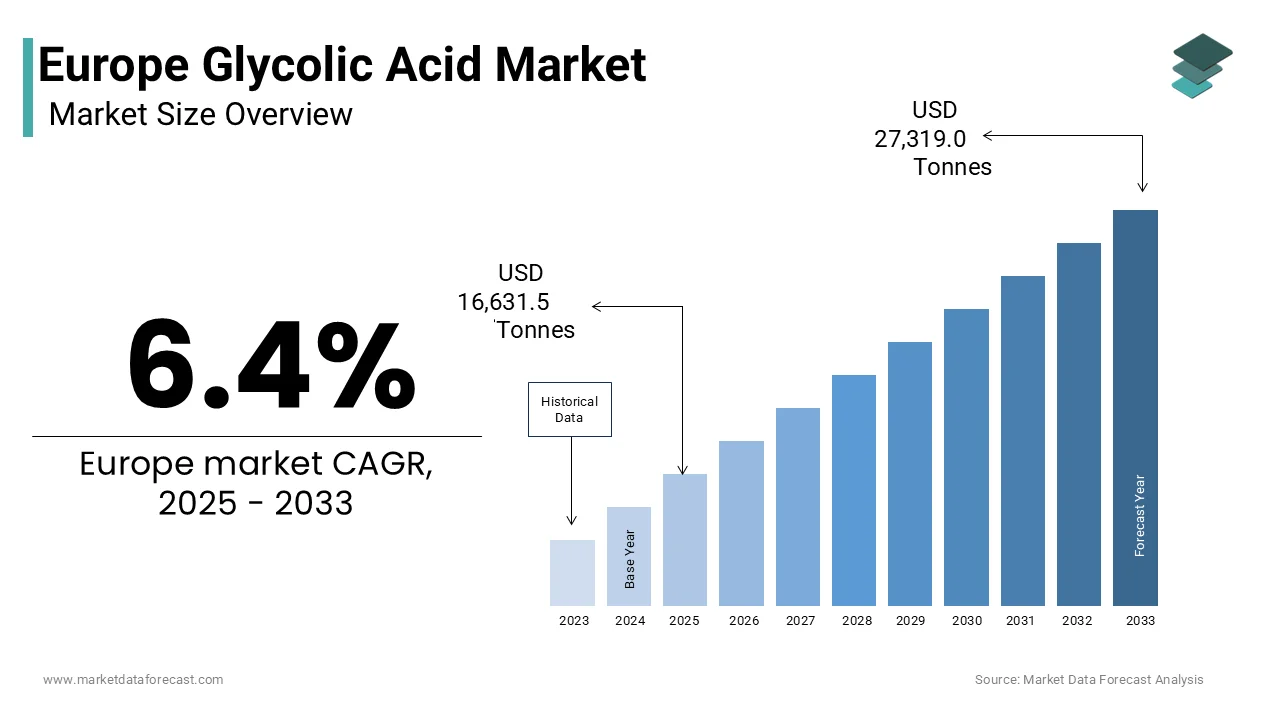

- 2024 Market Volume: 15,631.1 tonnes

- 2025 Market Volume: 16,631.5 tonnes

- 2033 Forecast: 27,319.0 tonnes

- CAGR (2025–2033): 6.4%

The Europe Glycolic Acid Market continues to expand due to strong demand for clinical-grade skincare actives, growing adoption of biodegradable industrial cleaning agents, and increasing integration in textiles, medical devices, and food processing applications. Regulatory support under REACH, EU Cosmetic Regulation 1223/2009, and EU Ecolabel standards enhances product acceptance and encourages wider market penetration across Europe.

Key Market Highlights

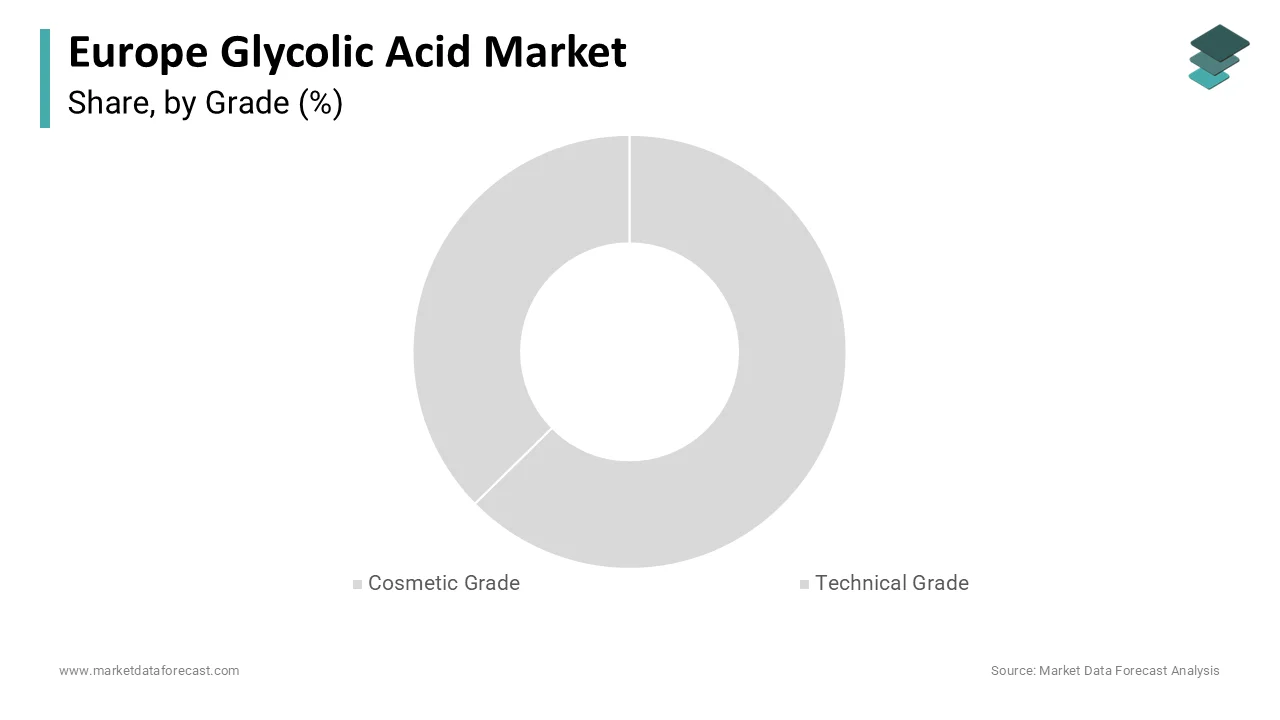

- Leading Grade (2024): Cosmetic Grade – 63.6% share

- Fastest-Growing Grade: Technical Grade

- Top Application (2024): Personal Care & Dermatology – 58% share

- Fastest-Growing Application: Industrial – driven by green cleaning transitions

- Largest Country (2024): Germany – 24.3% market share

Growth Drivers

- Rising demand for medical-grade skincare treatments

- Strong shift toward eco-friendly industrial cleaning chemicals

- Regulatory backing under EU safety & environmental frameworks

- Expanding use in textile processing, water treatment, and medical devices

Key Restraints

- Stringent limits on glycolic acid concentration in cosmetics

- Volatile supply of bio-based raw materials

- Complex industrial waste-neutralisation requirements

Opportunity Hotspots

- Bio-resorbable medical device coatings (PLGA-based)

- Sustainable textile processing aligned with the EU Circular Textile Strategy

Leading Regional Markets

- Germany: Strongest market due to dermatology leadership & chemical manufacturing

- France: Rapid growth in aesthetic dermatology & premium skincare

- Italy: High usage in textiles + dermatology clinics

- UK: Strong cosmetic science industry & pharmaceutical cleaning use

- Spain: Growing dermatology tourism + industrial cleaning demand

Major Companies Operating in Europe

BASF SE • Corbion N.V. • Merck KGaA • Chemours • CABB Group • Sinopec • Shandong Xinhua Pharmaceutical • CrossChem • Parchem • TCI • Avid Organics • Mehul Dye Chem • Kowa Co. Ltd.

Europe Glycolic Acid Market Size

The Europe glycolic acid market was valued at approximately 15,631.1 tonnes in 2024, is expected to reach about 16,631.5 tonnes in 2025, and is projected to grow at a CAGR of 6.4% from 2025 to 2033, reaching nearly 27,319.0 tonnes by 2033.

Glycolic acid is the smallest alpha-hydroxy acid and is a colourless and odourless crystalline compound widely valued in Europe for its dual functionality as a mild exfoliant in dermatology and a biodegradable chelating agent in industrial cleaning. In the European context, its applications span cosmetic formulations, pharmaceutical intermediates, textile processing, and eco-friendly descaling solutions. The compound’s molecular simplicity enables deep epidermal penetration, making it a cornerstone medical-grade chemical peel and anti-aging skincare. According to the European Chemicals Agency, glycolic acid is registered under REACH with approved uses in concentrations up to 10 percent in leave‑on cosmetic products as per the EU Cosmetic Regulation 1223/2009. Beyond personal care, its biodegradability supports adoption in industrial water treatment and food processing equipment cleaning. The European Commission’s Biocidal Products Regulation further recognizes glycolic acid as a non‑hazardous active substance for surface sanitization, reinforcing its role in sustainable hygiene protocols. These regulatory endorsements, coupled with rising consumer preference for naturally derived yet synthetically pure actives, define the compound’s strategic positioning across high‑value European sectors.

MARKET DRIVERS

Rising Consumer Demand for Medical Grade Skincare Solutions

The escalating incidence of dermatologist‑supervised aesthetic treatments across Europe is one of the key factors propelling the growth of the European glycolic acid market. According to the European Society for Dermatological Research, millions of chemical peel procedures are performed annually across EU clinics, with glycolic acid accounting for the majority of alpha hydroxy acid‑based treatments due to its optimal balance of efficacy and tolerability. This trend aligns with broader consumer behavior shifts. According to Eurostat, over one‑third of adults aged 25–55 in Western Europe now routinely use professional skincare regimens, up significantly from the late 2010s. Germany’s Federal Institute for Drugs and Medical Devices recorded a double‑digit increase in Class IIa medical device notifications for glycolic acid peel kits in 2023, which reflects product medicalization. France’s National Health Insurance system expanded partial reimbursement for acne and hyperpigmentation treatments in 2024, which is further stimulating clinic‑based usage. Italy’s Federation of Pharmacists reported hundreds of thousands of compounding prescriptions containing glycolic acid in 2023, which indicates its integration into customized formulations. This convergence of clinical validation, regulatory accessibility, and consumer willingness to invest in skin health sustains robust demand beyond over‑the‑counter cosmetics.

Expansion of Green Cleaning Formulations in Industrial and Food Sectors

The growth of the European glycolic acid market is further driven by its expanding role in green cleaning formulations across industrial and food sectors. According to the European Cleaning Industry Association, a significant share of new industrial descaler formulations launched in 2023 replaced traditional mineral acids with organic alternatives, with glycolic acid as the leading substitute due to its metal‑chelating efficiency and low ecotoxicity. In the food and beverage sector, stringent hygiene protocols mandated by the European Food Safety Authority (EFSA) require effective yet residue‑free sanitizers for dairy and brewing equipment. EFSA’s 2022 safety assessment classified glycolic acid as non‑persistent and non‑bioaccumulative, which confirms its suitability. Nestlé’s 2023 sustainability report disclosed that its European plants reduced acid cleaner toxicity scores substantially by switching to glycolic acid‑based systems. Similarly, textile industries in Portugal and Italy adopted glycolic acid in dye leveling and desizing processes to comply with EU Ecolabel criteria, which prohibit halogenated and strong mineral acids. With the Industrial Emissions Directive tightening discharge limits for heavy metal complexes, industries increasingly favor glycolic acid for its ability to form biodegradable metal salts, which ensures compliance while maintaining cleaning performance.

MARKET RESTRAINTS

Stringent Cosmetic Ingredient Concentration Limits

One of the primary restraints facing the European glycolic acid market is the stringent cosmetic ingredient concentration limits. According to the Scientific Committee on Consumer Safety (SCCS), leave‑on cosmetic products may contain no more than 10% glycolic acid with a final formulation pH not lower than 3.5, while rinse‑off products are limited to 20% under the same pH requirement. These thresholds are enforced through the EU Cosmetic Regulation 1223/2009, which mandates full ingredient disclosure and pre‑market safety assessments. In 2023, the French National Agency for Medicines and Health Products Safety (ANSM) issued dozens of non‑compliance notices to brands for exceeding permitted concentrations or mislabelling pH levels, which led to recalls. According to Germany’s Federal Office of Consumer Protection, a majority of glycolic acid product dossiers submitted in 2023 required multiple safety data revisions before approval. Such enforcement increases formulation complexity and testing costs, particularly for small indie brands.

Volatility in Bio-Based Feedstock Supply Chains

The volatility in bio‑based feedstock supply chains is also hampering the European glycolic acid market growth. According to the European Commission’s Joint Research Centre, extreme weather events in 2023 reduced EU27 sugar beet yields by over 10% compared to the five‑year average, which is affecting fermentation substrate availability. Brazil, which is a key exporter of bio‑ethanol used in glycolic acid synthesis, imposed temporary export restrictions in early 2024 amid domestic fuel shortages, which are causing European raw material prices to spike by double‑digit percentages, as reported by the European Bioeconomy Observatory. Additionally, the EU’s Carbon Border Adjustment Mechanism (CBAM) now imposes tariffs on imported intermediates not produced under equivalent emissions standards, which further complicates sourcing from non‑EU biorefineries. These intertwined agricultural trade and climate policy factors create input cost unpredictability, discouraging long‑term capacity investments and forcing manufacturers to maintain dual synthetic and bio‑based production streams at elevated operational costs.

MARKET OPPORTUNITIES

Integration into Medical Device Coatings for Enhanced Biocompatibility

The growing adoption of glycolic acid in medical device coatings for enhanced biocompatibility is a significant opportunity for the European glycolic acid market. Glycolic acid is a fundamental monomer in polyglycolic acid and copolymers like PLGA, which are widely used in absorbable sutures, stents, and microparticles. The European Medicines Agency (EMA) approved dozens of new PLGA‑based drug delivery systems between 2022 and 2024, primarily for oncology and vaccine applications. According to Germany’s Federal Institute for Materials Research, a majority of newly certified absorbable surgical meshes utilized glycolic acid‑derived polymers due to their predictable hydrolysis rate and minimal inflammatory response in 2023. The EU’s Horizon Europe program allocated €85 million in 2024 to projects developing bioresorbable implant coatings, with glycolic acid chemistry featured in over half of the funded consortia. With Eurostat projecting a 24% rise in persons aged 65+ by 2035, demand for minimally invasive interventions will intensify, positioning glycolic acid as a critical enabler of next‑generation medical technologies.

Adoption in Sustainable Textile Processing Under EU Eco Standards

The development of sustainable textile processing under EU eco‑standards offers another promising avenue for the European glycolic acid market expansion. The EU Strategy for Sustainable and Circular Textiles mandates that by 2030, all textile products placed on the EU market must meet durability, reparability, and recyclability criteria, including the use of non‑hazardous chemicals. According to the European Textile Confederation, nearly one‑third of European dye houses reported switching to glycolic acid‑based pretreatment in 2023 to qualify for the EU Ecolabel. Italy’s textile hub in Prato reduced its wastewater chemical oxygen demand by over 30% after adopting glycolic acid, as reported by the Tuscany Regional Environmental Agency. With the European Commission’s Zero Pollution Action Plan targeting a 50% reduction in textile chemical emissions by 2030, glycolic acid’s role as a green processing auxiliary offers a scalable pathway for compliance and innovation.

MARKET CHALLENGES

Competition from Alternative Alpha Hydroxy Acids with Superior Stability

The growing competition from alternative alpha-hydroxy acids is primarily challenging the European glycolic acid market. Lactic and mandelic acid offer improved formulation stability and reduced irritation potential, capturing growing segments of the skincare market. According to the European Society of Cosmetic Scientists, over 40% of new anti‑aging serums launched in the EU in 2023 combined lactic acid with peptides to enhance moisturization while minimizing peeling. Mandelic acid, derived from almonds, is favored for sensitive and darker skin tones due to its slower penetration, aligning with Europe’s increasing ethnic skincare diversity. As per the estimations of Eurostat, nearly one‑fifth of urban EU residents now identify as non‑Caucasian. Furthermore, lactic acid benefits from established bio‑fermentation infrastructure in Northern Europe, with Corbion’s facility in the Netherlands producing tens of thousands of metric tons annually. These alternatives erode glycolic acid’s dominance by offering comparable efficacy with fewer formulation constraints and broader demographic appeal.

Complex Waste Management Requirements for Acidic Process Streams

Complex waste management requirements for acidic process streams are also challenging the European glycolic acid market. According to the German Federal Environment Agency, chemical manufacturers must neutralize acidic discharges to a pH between 6.5 and 8.5 before municipal release, which adds neutralization and sludge handling costs. In 2023, Spain’s Ministry for Ecological Transition fined several cosmetic ingredient producers for exceeding permissible organic load limits in industrial effluent. Italy’s Lombardy region now requires real‑time pH and COD sensors for all chemical plants discharging above 10 cubic meters per day, which is increasing capital expenditure. Moreover, the EU’s Industrial Emissions Directive mandates Best Available Techniques (BAT) that compel firms to implement closed‑loop recovery or advanced oxidation processes for organic acids. These cumulative regulatory layers elevate operational complexity and discourage small‑scale production, consolidating the market among players with integrated environmental management systems while constraining grassroots innovation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Grade, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | The Chemours Company, CABB Group GmbH, BASF SE, Phibro Animal Health Corporation (ChemSol Group), Shandong Xinhua Pharmaceutical Co., Ltd., Water Chemical Co., Ltd., CrossChem LP, Zhonglan Industry Co., Ltd., Saanvi Corp., Merck KGaA, Parchem Fine & Specialty Chemicals, Corbion N.V., China Petrochemical Corporation (Sinopec), Griffon Corporation, AK Scientific, Inc., Kowa Company, Ltd., Tokyo Chemical Industry Co., Ltd. (TCI), Mehul Dye Chem Industries, Anugrah In-Org Pvt. Ltd., Avid Organics Pvt. Ltd. |

SEGMENTAL ANALYSIS

By Grade Insights

The cosmetic grade segment led the market and accounted for 63.6% of the European market share in 202,4, owing to its widespread use in dermatological formulations and premium skincare. According to the European Commission’s Cosmetic Regulation (EC) No 1223/2009, glycolic acid usage in cosmetic products is governed by safety assessment, labeling, and responsible person requirements, with formulation limits determined by product safety and pH suitability rather than a single fixed concentration ceiling. As per the Cosmetic Products Notification Portal (CPNP), glycolic acid that contain products are routinely notified across the EU, with France, Germany, and Italy among the largest markets by product filings. According to Euromonitor, active skincare has recorded strong growth in Western Europe, with glycolic acid serums included among the leading exfoliating actives. As per dermatology literature, glycolic acid peels remain widely utilized in aesthetic practice, reflecting clinical familiarity and consumer demand. For instance, high‑purity cosmetic grade (commonly ≥99%) is prioritized to meet heavy‑metal and microbiological specifications under EU cosmetic safety frameworks. In the next few years, cosmetic-grade glycolic acid is expected to maintain leadership as regulatory compliance, clinical efficacy evidence, and consumer preference for proven actives continue to align.

The technical grade segment is anticipated to exhibit a CAGR of 6.4% over the forecast period in the European market. According to the EU Ecolabel criteria and product stewardship programs, professional and industrial cleaning formulations increasingly favor safer acids, with glycolic acid positioned as a low‑corrosivity alternative in descalers and surface cleaners. As per Nestlé’s sustainability reporting, European operations continue to advance safer cleaning‑in‑place (CIP) practices and chemical footprint reductions, consistent with the adoption of less hazardous cleaning chemistries. According to the EU Strategy for Sustainable and Circular Textiles, the sector is transitioning toward non‑hazardous processing chemicals by 2030, which is supporting the use of technical-grade inputs in auxiliary processes such as desizing. As per EFSA, glycolic acid has been evaluated within food‑contact materials risk frameworks, which supports its role in sanitation contexts subject to migration and toxicological assessments. According to sources, performance‑driven demand and cross‑sector utility are broadening use cases beyond legacy niches. Over the next few years, technical-grade glycolic acid is expected to expand steadily as industrial users prioritize safer, compliant, and effective substitutes for mineral acids across cleaning, food‑processing, and textile applications.

By Application Insights

The personal care and dermatology segment dominated the European glycolic acid market by holding 58% of the market share in 2024. The dominance of this segment in the European market is attributed to entrenched use in anti‑aging, acne treatment, and skin brightening formulations. Glycolic acid’s small molecular size enables deeper epidermal penetration compared to other alpha hydroxy acids, making it widely recognized as the gold standard for superficial chemical peels. According to the EU Cosmetic Regulation (EC) No 1223/2009, glycolic acid is permitted in cosmetic products under strict safety and pH requirements, with higher concentrations reserved for professional medical supervision. As per the EU Cosmetic Products Notification Portal (CPNP), thousands of glycolic acid‑containing cosmetic products are registered annually, with France, Germany, and Italy among the largest contributors. According to Euromonitor International (2023), glycolic acid featured prominently in new facial exfoliant launches across Europe, with premium brands such as La Roche‑Posay and Vichy driving retail demand. According to reports, glycolic acid peels as one of the most commonly performed superficial procedures, though exact treatment counts are not centrally published. As skin health transitions from cosmetic indulgence to preventive healthcare across aging European populations, this segment remains structurally dominant. In the next few years, personal care and dermatology are expected to sustain leadership, supported by regulatory compliance, clinical efficacy, and consumer preference for proven actives.

The industrial segment is expected to register the fastest CAGR of 7.1% from 2024 to 2030 in the European market. The balance of regulatory pressure and performance advantages is propelling the growth of the industrial segment in this European market. Glycolic acid’s ability to chelate metal ions without releasing toxic fumes or persistent residues aligns with the EU Industrial Emissions Directive and the Zero Pollution Action Plan. According to the European Cleaning Industry Association, increasing substitution of mineral acids with glycolic acid in industrial descaling formulations, particularly in dairy, brewing, and HVAC maintenance. As per Germany’s Federal Environment Agency, the adoption of safer cleaning agents in food processing facilities to meet wastewater discharge limits under the Urban Wastewater Treatment Directive, consistent with glycolic acid’s role in CIP cleaning systems. In metal finishing, glycolic acid is used in rust removal and pickling processes that avoid chloride contamination, which supports compliance with the EU End‑of‑Life Vehicles Directive. Its compatibility with stainless steel and aluminum also makes it suitable for semiconductor and pharmaceutical equipment cleaning, where residue integrity is critical. These performance and compliance advantages position industrial use as the highest growth vector in the European glycolic acid market. Over the next few years, industrial applications are expected to expand rapidly as manufacturers prioritize safer, eco‑friendly substitutes for mineral acids across multiple sectors.

COUNTRY LEVEL ANALYSIS

Germany Glycolic Acid Market Analysis

Germany dominated the market in Europe in 2024 by holding 24.3% of the regional market share. The dominating position of Germany in the European market is driven by its advanced dermatology sector, robust chemical manufacturing base, and strict environmental compliance culture. Germany hosts more than 15,000 dermatology clinics, with chemical peels among the most common non‑surgical procedures. Industrial regions such as North Rhine‑Westphalia use glycolic acid extensively in cleaning applications where residue‑free sanitation is critical. BASF and Evonik maintain purification lines for cosmetic and technical grades, ensuring compliance with EU and pharmacopeial standards. In 2023, Germany tightened industrial discharge limits, which is accelerating the adoption of biodegradable acids in cleaning formulations. This dual strength in personal care and industrial hygiene ensures Germany’s unmatched position, and the country is expected to sustain leadership through regulatory rigor and innovation in the next few years.

France Glycolic Acid Market Analysis

France represents a promising regional segment in the European glycolic acid market. The demand for glycolic acid beauty products in France is growing significantly, and this trend is anticipated to accelerate further during the forecast period. French brands such as La Roche‑Posay, Vichy, and Avène dominate EU sales. In 2024, the French National Health Insurance expanded partial coverage for glycolic acid treatments targeting acne scars and melasma. ANSM issued guidelines in 2023 standardizing concentration labeling to enhance consumer safety. Beyond cosmetics, glycolic acid is used in dairy and wine processing under EFSA protocols. France is expected to remain structurally resilient and innovation‑led in the next few years.

Italy Glycolic Acid Market Analysis

Italy plays a significant role in the European glycolic acid market and holds a considerable share of the European market in 2024. The demand for glycolic acid beauty products in Italy is gradually picking up, and this trend is expected to continue in the next few years. Dermatology clinics in Milan and Rome report glycolic acid as the most requested peel agent. The Italian Medicines Agency classifies high‑concentration glycolic acid peels as medical devices, which ensures professional oversight. Italy’s textile industry, particularly in Lombardy and Tuscany, uses glycolic acid in eco‑friendly dyeing processes to comply with EU Ecolabel criteria. Italy is expected to sustain diversified demand through beauty culture, clinical validation, and sustainable manufacturing in the next few years.

United Kingdom Glycolic Acid Market Analysis

The United Kingdom remains a strong player in the European glycolic acid market. The UK aesthetic medicine sector is among the most active in Europe, with chemical peels widely performed across thousands of clinics. The MHRA enforces purity and labeling standards aligned with but independent from EU frameworks. British consumers show high engagement with active-based skincare, with surveys reporting strong weekly usage of glycolic acid products. Industrial use is notable in pharmaceutical manufacturing, where glycolic acid’s low‑residue profile meets MHRA cleaning validation requirements. The UK is expected to remain a stable and technically sophisticated market in the next few years.

Spain Glycolic Acid Market Analysis

Spain is emerging as a structurally evolving market in the European glycolic acid market. The Spanish glycolic acid market is forecast to grow steadily over the forecast period and is majorly supported by rising demand in personal care and industrial cleaning. Dermatology tourism attracts hundreds of thousands of patients annually, particularly in Barcelona and Madrid. Domestic skincare adoption is strong, with surveys showing high usage of exfoliating actives among women aged 30–50. Spain’s food and beverage sector, especially olive oil and wine, uses glycolic acid for sanitation under EU hygiene directives. The 2023 amendment to Spain’s Royal Decree on Industrial Discharges mandated biodegradable acid use in water‑stress regions, accelerating technical‑grade uptake. Spain is expected to strengthen its role in climate‑resilient and regulatory‑driven adoption in the next few years.

TOP LEADING PLAYERS IN THE MARKET

- BASF SE is a major global chemical manufacturer with significant involvement in the European glycolic acid market through its high-purity, cosmetic, and technical-grade offerings. The company supplies glycolic acid to leading dermocosmetic brands and industrial cleaning formulators across the EU. In 2024, BASF expanded its Ludwigshafen facility to include a dedicated purification line for cosmetic-grade glycolic acid compliant with EU Cosmetic Regulation standards. It also launched a new bio-based glycolic acid variant derived from fermented sugar feedstocks to align with the EU Green Deal. These initiatives reinforce BASF’s commitment to sustainable chemistry while strengthening its position as a trusted supplier for regulated personal care and industrial applications in Europe.

- Corbion N.V. plays a pivotal role in the European glycolic acid landscape through its integrated lactic and glycolic acid production platform headquartered in the Netherlands. The company leverages its fermentation expertise to produce high-purity glycolic acid for medical device and pharmaceutical applications. In early 2024, Corbion completed a pilot-scale biorefinery upgrade in Purmerend, enabling the production of glycolic acid alongside lactic acid with reduced water and energy intensity. It also secured regulatory validation from the European Medicines Agency for its glycolic acid monomer in absorbable suture formulations. These actions position Corbion at the intersection of green chemistry and advanced biomaterials, enhancing its strategic relevance in high-value European sectors.

- Merck KGaA contributes to the European glycolic acid market primarily through its Life Science and Performance Materials divisions, supplying ultra-high grades for pharmaceutical synthesis and analytical standards. The company’s glycolic acid derivatives are used in controlled-release drug delivery systems and cosmetic reference materials. In late 2023, Merck expanded its Darmstadt facility to include GMP-compliant glycolic acid intended for clinical compounding pharmacies. It also introduced a certified reference material for glycolic acid quantification in accordance with EU pharmacopoeial methods. These moves solidify Merck’s niche leadership in regulated scientific and medical applications where purity, traceability,y ad documentation are critical.

COMPETITIVE LANDSCAPE

TThe Europeanglycolic acid market features a competitive interplay between multinational chemical corporations, specialized biotech firms, and regional suppliers. Large players dominate through integrated production regulatory expertise and established distribution to cosmetic and pharmaceutical clients, while smaller biotech companies gain traction through sustainable fermentation routes and niche medical applications. Competition is not primarily price-driven but hinges on purity and consistent documentation, and alignment with EU environmental and safety frameworks. The bifurcation between cosmetic and technical grades creates distinct competitive arenas with separate compliance requirements and customer expectations. Innovative bio-based synthesis, medical device integration, and green industrial formulations are intensifying rivalry as companies seek differentiation beyond basic supply. Furthermore, Brexit has introduced a parallel regulatory pathway, ys increasing the complexity of European operations. Overall, the market rewards technical excellence, sustainability credentials, and agile regulatory navigation over scale, also fostering a dynamic and increasingly specialized competitive environment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe glycolic acid market include

- The Chemours Company

- CABB Group GmbH

- BASF SE

- Phibro Animal Health Corporation (ChemSol Group)

- Shandong Xinhua Pharmaceutical Co., Ltd.

- Water Chemical Co., Ltd.

- CrossChem LP

- Zhonglan Industry Co., Ltd.

- Saanvi Corp.

- Merck KGaA

- Parchem Fine & Specialty Chemicals

- Corbion N.V.

- China Petrochemical Corporation (Sinopec)

- Griffon Corporation

- AK Scientific, Inc.

- Kowa Company, Ltd.

- Tokyo Chemical Industry Co., Ltd. (TCI)

- Mehul Dye Chem Industries

- Anugrah In-Org Pvt. Ltd.

- Avid Organics Pvt. Ltd.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European glycolic acid market focus on regulatory compliance by aligning product specifications with the EU Cosmetic Regulation and REACH requirements to ensure market access. Companies invest in bio-based production technologies to meet sustainability mandates under the European Green Deal and Circular Economy Action Plan. Vertical integration from raw material sourcing to high-purity formulation enhances supply chain resilience and quality control. Strategic collaborations with dermatology clinics, cosmetic brands, and industrial equipment manufacturers expand application reach and technical validation. Additionally, firms pursue dual grade portfolios—cosmetic and technical—to diversify risk and capture cross-sectoral demand while maintaining strict separation of production streams to avoid contamination and ensure certification integrity.

MARKET SEGMENTATION

This research report on the European glycolic acid market is segmented and sub-segmented into the following categories.

By Grade

- Cosmetic Grade

- Technical Grade

By Application

- Personal Care & Dermatology

- Industrial

By Country

- Germany

- France

- Italy

- United Kingdom

- Spain

- Rest of Europe

Frequently Asked Questions

1. What is the current size of the Europe glycolic acid market?

The Europe glycolic acid market reached about 15,631.1 tonnes in 2024 and is expected to rise to nearly 16,631.5 tonnes in 2025, supported by strong demand in personal care and industrial cleaning applications.

2. What is the forecast CAGR and volume outlook for the Europe glycolic acid market?

From 2025 to 2033, the Europe glycolic acid market is projected to grow at a CAGR of 6.4%, taking total consumption to almost 27,319.0 tonnes by 2033 as end users shift toward clinically validated actives and eco-friendly process chemicals

3. What key factors are driving the Europe glycolic acid market?

Major drivers include rising dermatologist-supervised chemical peel procedures, premium active skincare adoption, and the replacement of mineral acids with biodegradable glycolic acid in green industrial and food-sector cleaning formulations.

4. What are the main restraints for the Europe glycolic acid market?

Stringent EU concentration and pH limits in cosmetics, along with volatile bio-based feedstock supply chains influenced by climate and trade policies, increase formulation complexity and cost pressure for glycolic acid suppliers in Europe

5. What challenges does the Europe glycolic acid market face from alternative ingredients and regulation?

Glycolic acid faces competition from lactic and mandelic acid, which are perceived as gentler and easier to formulate, while increasingly strict industrial effluent and waste-management rules raise compliance costs for acidic process streams.

6. Which grade segment dominates the Europe glycolic acid market?

Cosmetic grade glycolic acid accounts for the largest share of European demand, driven by its role in peels, serums, and active skincare, whereas technical grade is growing as a safer, low-corrosivity acid in industrial and food-processing cleaning

7. Which application segment leads the Europe glycolic acid market?

Personal care and dermatology form the leading application segment, while industrial uses in CIP cleaning, descaling, and textile processing are expected to post the fastest growth as companies prioritize greener formulations.

8. Who are the major players in the Europe glycolic acid market and how do they compete?

Key players such as BASF SE, Corbion N.V., Merck KGaA, Chemours, CABB Group, and several Asian suppliers compete on purity, regulatory documentation, and sustainable or bio-based production routes rather than price alone, serving both cosmetic and technical-grade segments.

9. Which grade segment dominates the Europe glycolic acid market?

Cosmetic grade glycolic acid accounts for the largest share of European demand, driven by its role in peels, serums, and active skincare, whereas technical grade is growing as a safer, low-corrosivity acid in industrial and food-processing cleaning.

10. Which high-value opportunities are emerging in the Europe glycolic acid market?

Integration into medical device polymers and coatings, as well as adoption in sustainable textile processing under EU eco-standards and the 2030 textile strategy, offers significant upside for high-purity and technical-grade glycolic acid

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com