Europe Green Tea Market Research Report Segmented By Container Type (Plastic Bottles, Bags, Cans, And Others), Product Type (Flavored And Unflavored), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Market Size, 2025

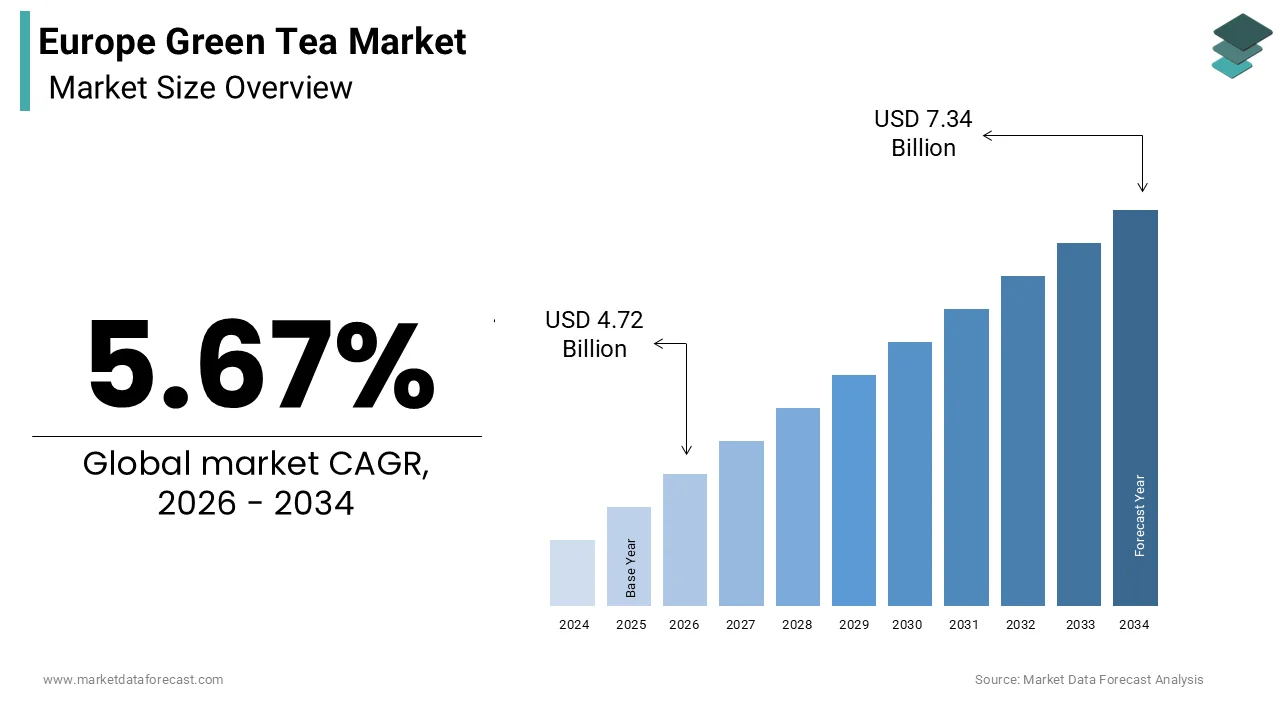

$4.47 BnMarket Estimate, 2026

$4.72 BnMarket Forecast, 2034

$7.34 BnCAGR, 2026–2034

5.67%Europe Green Tea Market Size

The European green tea market size was calculated to be USD 4.47 billion in 2025 and is anticipated to be worth USD 7.34 billion by 2034, from USD 4.72 billion in 2026, growing at a CAGR of 5.67% during the forecast period.

Green tea is a mainstream functional beverage deeply embedded in evolving dietary and wellness paradigms. Sourced from the unfermented leaves of Camellia sinensis, green tea preserves a high concentration of catechins, particularly epigallocatechin gallate, which form the scientific basis for its health positioning. Unlike black tea, which remains culturally entrenched, green tea’s appeal stems from its alignment with preventive nutrition, clean label preferences, and plant-based lifestyles. Tea consumption in the European Union is a substantial market, and preferences are evolving towards healthier options. The popularity and market share of green tea are expanding, especially in countries like Germany, the Netherlands, and the Nordic nations, driven by increasing health consciousness among consumers. Germany maintains substantial per capita tea consumption, yet its market is marking a clear transition: consumers are increasingly choosing specialty and green tea variants, found in traditional stores and niche specialty retailers alike. This growth is not merely commercial but cultural, reflecting a wider European shift toward mindful consumption and botanical authenticity in daily nutrition.

MARKET DRIVERS

Elevated Public Awareness of Preventive Health Fuels Consumption Patterns

European consumers are increasingly adopting dietary strategies to mitigate chronic disease risks, which is among the key factors driving the growth of the Europe green tea market. Green tea is emerging as a scientifically endorsed component of this preventive approach. Peer-reviewed studies have reinforced its role in cardiovascular and metabolic health. Large-scale prospective studies within Europe and Asia have consistently indicated that regular consumption of green or black tea is associated with a reduced risk of experiencing cardiovascular events. As per, there is a growing consumer interest across the European Union in functional and herbal beverages, driven by increasing health and wellness awareness. National regulatory bodies have also contributed to its credibility; Scientific literature suggests that the moderate intake of green tea may be linked to improvements in lipid profiles among adults. Retail evidence further validates this trend. This health-led demand is particularly strong among urban millennials and aging populations by creating resilient and recurring consumption patterns that transcend seasonal or promotional influences.

Expansion of Plant-Based and Clean Label Food Trends Reinforces Product Integration

Green tea’s versatility has enabled its integration far beyond traditional infusion formats by embedding it into the broader plant-based and clean label food movement sweeping the region, which further propels the expansion of the Europe green tea market. Consumers now encounter green tea in energy bars, snack blends, frozen desserts, and even savory culinary products, driven by demand for recognizable ingredients and functional benefits. Consumers are showing a preference for food items with simpler ingredient lists. Shoppers appear to favor products with a limited number of recognizable components. Major retailers have responded accordingly. The market is seeing an expansion in the range of store-brand offerings in the green tea segment. This cross-category adoption is facilitated by green tea’s mild flavor and thermal stability during processing, allowing manufacturers to enhance product functionality without artificial additives. As a result, green tea has evolved from a standalone beverage into a foundational botanical ingredient across Europe’s clean-label innovation ecosystem.

MARKET RESTRAINTS

Limited Domestic Cultivation Constrains Supply Chain Autonomy

The region lacks commercial-scale green tea cultivation, which renders the market almost entirely import-dependent, and ultimately restricts the growth of the Europe green tea market. The European Union is a significant global importer of green tea, sourcing a large proportion of its volume from China. This reliance introduces significant vulnerabilities related to trade policy climate variability and food safety compliance. For instance, European food safety authorities consistently monitor for pesticide residues in all imported food products, including tea from China, and take appropriate action when residue levels exceed permitted limits. Commercial green tea cultivation within the European Union is limited in scale and area compared to major global producers, with production governed by the general framework of the EU's Common Agricultural Policy and environmental standards. This structural import dependency not only limits freshness and traceability but also complicates efforts to meet growing consumer demand for locally sourced or low-carbon products. European brands must strategically invest in regional agro-climatic adaptation to build supply chain resilience and support their sustainability goals.

Inconsistent Regulatory Classification Across Member States Creates Market Fragmentation

The absence of a unified EU regulatory stance on green tea, particularly when marketed for functional benefits, results in significant market fragmentation and thereby hinders the expansion of the Europe green tea market. The lack of authorised specific health claims for green tea components under EU regulation contributes to ongoing uncertainty for businesses regarding product positioning. Moreover, the status of green tea extracts varies significantly across the European Union, being treated as a general food product in some nations while classified as a regulated medicinal item in others, creating barriers to consistent market access. Additionally, caffeine limits in ready-to-drink green tea beverages vary widely. Member states maintain different maximum recommended intake levels for specific green tea components, creating regulatory inconsistency across national borders. This regulatory patchwork increases compliance complexity, especially for small and medium enterprises. European food and drink industry associations consistently highlight significant product launch delays for smaller companies, primarily caused by varied national interpretations of unified EU food regulations.

MARKET OPPORTUNITIES

Premiumization Through Organic and Single Origin Offerings Captures High Margin Segments

European consumers are increasingly willing to pay significant premiums for green tea that emphasizes origin, authenticity, ethical sourcing, and artisanal processing. This premiumization is expected to boost the growth of the Europe green tea market. The organic green tea segment experienced significant growth in recent years, reflecting a broader increase in demand for organic products across Europe. Single-origin green teas are increasingly positioned as a premium product in European specialty markets, commanding high retail prices. European consumers are increasingly placing importance on the geographical origin of green tea as a key factor in their purchasing decisions. Brands are capitalizing on this by highlighting traditional methods such as shade growing for matcha or stone grinding for ceremonial grades, which resonate with culturally literate urban consumers. The presence of the European Union’s organic logo on green tea products has increased significantly in Germany and the Netherlands since 2020, indicating a rising availability of certified organic options. This premium trajectory not only enhances profitability but also builds defensible brand equity in a category increasingly defined by provenance and craftsmanship rather than price alone.

Integration Into Workplace Wellness and Corporate Sustainability Programs Drives B2B Demand

Green tea is being strategically adopted by European corporations as part of workplace wellness and environmental sustainability initiatives, which is likely to generate fresh expansion possibilities for the Europe green tea market. Its low caffeine content, cognitive benefits, and minimal environmental footprint align with corporate health and ESG goals. The provision of diverse beverage options, including a greater variety of teas, is a growing trend among multinational employers across the EU. Procurement data suggests a notable increase in demand for green tea in corporate catering services in several European countries, including France, Germany, and the Nordic countries. Environmental metrics further support this shift. Life cycle assessments consistently highlight that packaging-free brewing methods, such as loose-leaf tea, generally produce less packaging waste than single-serve convenience formats like coffee pods. The environmental impact, including greenhouse gas emissions, is often lower for traditional, minimally processed products like loose-leaf tea when compared to some highly processed, single-serving alternatives. Public institutions are following suit. This institutional channel provides stable, recurring demand insulated from retail volatility and opens new revenue streams for specialty tea suppliers.

MARKET CHALLENGES

Climate Change Induces Volatility in Key Exporting Regions

Climate instability in major green tea-producing nations is disrupting supply reliability and quality consistency for the Europe green tea market. Climatic variations during essential growth periods have been observed to impact the visual and structural characteristics of tea leaves in certain major Asian growing regions. Fluctuating weather patterns, particularly unseasonable temperature shifts, are associated with a perceived reduction in the overall quality markers of harvested foliage. Extreme cold events occurring early in the growing season have been noted to physically damage tea plants, leading to a decrease in the volume of successful initial harvests. Primary tea-producing provinces and prefectures appear increasingly vulnerable to atmospheric instabilities that disrupt traditional harvest cycles. The consistency of high-grade tea production is facing challenges attributed to the rising frequency of environmental anomalies during sensitive developmental stages. These disruptions directly impact European importers. Such volatility complicates forecasting inventory management and pricing strategies, particularly for premium segments reliant on seasonal flushes. Without diversified sourcing or climate-resilient cultivation partnerships, European brands remain exposed to escalating supply risks that could intensify with projected global warming trends.

Consumer Confusion Over Product Authenticity and Processing Methods Undermines Trust

Widespread consumer misconceptions about green tea’s composition and processing erode trust and hinder category maturation, despite rising interest, which limits the expansion of the Europe green tea market. Consumer understanding of specific tea production methods, such as the difference between green and black tea processing, often appears limited across various markets. Furthermore, a common perception exists among a significant number of consumers that all green teas are inherently free of caffeine. This knowledge gap is exploited by ambiguous labeling; many “green tea” blends contain fewer actual Camellia sinensis leaves. Official food monitoring agencies in Germany occasionally uncover instances of non-compliance and misbranding in various food products, including items like tea. These findings highlight an ongoing trend of consumer protection authorities addressing issues of undeclared ingredients and misleading origin claims within the marketplace. Additionally, the proliferation of high sugar-ready-to-drink green teas contradicts the health image of traditional infusions. This dissonance fosters consumer skepticism, drives demand for costly third-party certifications, and fragments brand loyalty. The market risks commoditization and a diluted reputation, which would impede long-term growth if comprehensive industry education efforts are not implemented.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.67% |

| Segments Covered | By Container Type, Product Type, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | AMORE Pacific Corp, Arizona Beverage Company, Associated British Foods LLC, Cape Natural Tea Products, Celestial Seasonings, Finlays Beverages Ltd., Frontier Natural Products Co-Op., Hambleden Herbs, Hankook Tea, and Honest Tea, Inc. |

SEGMENTAL ANALYSIS

By Container Type Insights

The tea bags segment was the largest in the Europe green tea market by holding a 62.1% share in 2025. The dominance of the tea bags segment is primarily driven by convenience, standardized dosing, and compatibility with fast-paced urban lifestyles across Western and Northern Europe. The format’s popularity is further amplified by innovations such as biodegradable pyramid bags and oxygen barrier packaging that preserve catechin integrity, features increasingly demanded by eco-conscious consumers. Additionally, major tea brands have optimized supply chains around bagged formats, achieving economies of scale that keep prices lower than loose leaf equivalents. This affordability, combined with consistent brew strength and minimal preparation time, solidifies tea bags as the default choice for mainstream European consumers who prioritize efficiency without sacrificing perceived health benefits.

The canned green tea segment is predicted to witness the highest CAGR of 11.4% between 2026 and 2034 due to the convergence of on-the-go consumption trends, rising demand for functional ready-to-drink beverages, and aggressive product innovation by both global and regional players. The demand for canned green tea in major European urban centers has been on the rise, driven by increasing consumer health consciousness. Major beverage producers are increasingly introducing premium, health-focused green tea products featuring a variety of natural and functional infusions, such as ginger or vitamin C, to cater to wellness-minded consumers. The European market for functional beverages is experiencing substantial expansion as consumers increasingly seek drinks offering added health benefits like energy and immunity boosts. The aluminum can itself offers logistical advantages—lightweight recyclability and superior light barrier properties that protect sensitive polyphenols from degradation. Moreover, the aluminum beverage can recycling rate across Europe has remained high and stable in recent years, with ongoing industry efforts aimed at achieving near-total circularity. These factors position canned green tea as a high velocity channel for brand trial and urban penetration.

By Product Type Insights

The unflavoured green tea segment held the majority share of 58.6% of the Europe green tea market in 2025. The leading position of the unflavoured green tea segment is attributed to consumer preference for purity and perceived authenticity. European buyers, particularly in Germany and the Nordic countries, associate unflavored variants with higher concentrations of natural antioxidants and fewer processing additives. Health-conscious tea consumers across Europe are increasingly moving towards products with a focus on natural ingredients, purity, and the absence of artificial flavors or sweeteners. Sales data from the German market indicate a strong consumer preference for unflavored organic green tea options, particularly within specialist retail channels like pharmacies and health food stores. Moreover, traditional preparation methods, such as Japanese Sencha or Chinese Longjing, are increasingly promoted through culinary media and wellness platforms, reinforcing the cultural credibility of unadulterated tea. Reports on European consumer food trends show that regular tea drinkers frequently associate unflavored green tea with greater health benefits and a higher degree of trustworthiness compared to their flavored counterparts.

The flavoured green tea segment is estimated to register the fastest CAGR of 10.2% over the forecast period, owing to sensory innovation, cross-cultural flavour fusion, and strategic targeting of younger, experience-driven consumers. Social media and foodservice trends have amplified this shift. Leading coffeehouse chains have introduced new limited-edition green tea latte options. The launch of these specific new flavors increased consumer interest in flavored green tea product variations within a key demographic segment. Flavored green tea drinks generally have a lower sugar content compared to many other soft drinks in the region. This characteristic makes the product category align well with current national health-focused sugar reduction goals. This health-aligned indulgence is redefining flavored tea as a gateway to sustained green tea consumption.

REGIONAL ANALYSIS

Germany Green Tea Market Analysis

Germany dominated the Europe green tea market by accounting for 22.7% share in 2025. The supremacy of the German market is credited to a deeply rooted health culture, robust pharmacy distribution networks, and high consumer literacy around botanical efficacy. There is sustained demand for green tea, with unflavored options being particularly popular, indicating a preference for traditional varieties. Consumer interest is significant, with a notable portion of adults integrating it into their regular weekly routine for general well-being. Consumption habits are often linked to a belief in specific health benefits, such as supporting metabolism and digestion. The regulatory framework in the region is supportive of market expansion, as the classification of high-grade green tea extracts allows them to be marketed through established health-focused retail channels and associated with certain wellness claims. Retailers like dm Drogerie and Rossmann dedicate entire shelves to green tea, with private-label organic SKUs growing year on year. Germany’s emphasis on scientific validation and clean label integrity continues to anchor its dominant position in the European landscape.

United Kingdom Green Tea Market Analysis

The United Kingdom was the next prominent country in the Europe green tea market by holding a 17.5% share in 2025. The growth of the UK market is fuelled by rapid innovation in ready-to-drink formats and strong influence from Asian culinary trends. London’s diverse food scene has normalized matcha lattes, bubble tea, and cold brew green tea, with chains like Itsu and Bubbleology driving mainstream adoption. The UK’s departure from the EU has also accelerated direct sourcing from Japan and Taiwan, improving freshness and enabling premium single-origin offerings. Tesco and Sainsbury’s reported a percentage increase in chilled green tea sales, highlighting the shift toward convenience without compromising perceived health value.

France Green Tea Market Analysis

France is another key player in the Europe green tea market due to its integration of green tea into gastronomy and beauty wellness ecosystems. French green tea imports constitute a notable volume within the national market, and the tea market in general is experiencing an upward trend in consumption. The French market shows a significant and consistent increase in the general consumption and market share of organic products, including organic tea. French consumers increasingly view green tea not just as a beverage but as a lifestyle symbol, evident in collaborations between tea houses and luxury brands like L’Occitane and Guerlain, which use green tea extracts in skincare. In France, green tea and other plant-based foods are increasingly associated with health and well-being, particularly among urban, health-conscious consumers who value natural and organic cosmetics and food supplements. Carrefour and Monoprix have expanded their green tea selections to include Japanese Gyokuro and flavored blends with lavender or verbena, blending tradition with local terroir. This cultural repositioning, from medicinal infusion to aesthetic ritual, has elevated green tea’s perceived value and sustained its premium pricing.

Netherlands Green Tea Market Analysis

The Netherlands is moving ahead steadfastly in the Europe green tea market, owing to progressive sustainability policies and a highly informed consumer base. Dutch per capita green tea consumption has experienced an ongoing, long-term upward trend, driven by growing health awareness. Also, Dutch retailers like Albert Heijn and Jumbo lead in offering plastic-free packaging and Fair Trade-certified green teas, aligning with the national circular economy agenda. There is a significant and growing interest among Dutch green tea buyers in ethically sourced products with transparent supply chains. The country also serves as a key logistical hub. The Port of Rotterdam is a primary entry point and a major logistics hub for a large volume of tea imported into the European Union from global suppliers. Moreover, workplace wellness programs in Amsterdam’s tech and finance sectors have institutionalized green tea as a default office beverage by reinforcing habitual consumption. This combination of ethical commerce and infrastructural advantage solidifies the Netherlands as a strong influence in the market.

Sweden Green Tea Market Analysis

Sweden is likely to expand in the Europe green tea market from 2026 to 2034 due to strong public health initiatives and climate-conscious consumption patterns. Observations indicate an increase in the volume of green tea imports, with organic varieties constituting a considerable portion. This proportion of organic green tea within the overall imports is notably high compared to other regions. Official dietary guidelines recommend daily consumption of unsweetened plant-based beverages, including green tea, for their antioxidant benefits. Sales growth of green tea in a specific sustainable category appears linked to environmentally certified packaging and the introduction of local flavors. Additionally, Sweden’s high digital literacy enables direct-to-consumer subscription models, and companies like Tealet and Pukka Herbs saw growth in Nordic online tea sales. The nation’s alignment of personal wellness with planetary health makes it a bellwether for future green tea trends across Northern Europe.

COMPETITION OVERVIEW

The Europe green tea market features intense competition among multinational corporations, regional specialty brands, and private label retailers. Global players leverage extensive distribution networks, branding power, and R&D capabilities to dominate shelf space in supermarkets and pharmacies. Simultaneously, niche artisanal brands gain traction by emphasizing single-origin sourcing, organic certification, and traditional processing methods that appeal to discerning consumers. Private labels exert pricing pressure, particularly in Western Europe, where retailers like Carrefour and Aldi offer cost-effective green tea alternatives with clean label positioning. Innovation remains a critical battleground with companies competing on flavor profile,s functional benefits, and sustainability credentials. Regulatory complexity across EU member states adds another layer of competitive differentiation as brands navigate varied health claim permissions and packaging mandates. This dynamic landscape fosters continuous adaptation with market leaders investing in consumer education, supply chain transparency, and digital engagement to maintain relevance and drive loyalty in a rapidly maturing category.

KEY MARKET PLAYERS

A few major players of the Europe green tea market include

- AMORE Pacific Corp

- Arizona Beverage Company

- Associated British Foods LLC

- Cape Natural Tea Products

- Celestial Seasonings

- Finlays Beverages Ltd

- Frontier Natural Products Co-Op

- Hambleden Herbs

- Hankook Tea

- Honest Tea, Inc

Top Strategies Used by the Key Market Participants

Key players in the Europe green tea market prioritize product innovation through flavor diversification and functional enhancement to meet evolving health demands. They invest heavily in sustainable packaging, including compostable tea bags and recyclable containers, to align with EU environmental regulations. Companies are expanding ready-to-drink formats with cold brew and low sugar variants to capitalize on the go consumption trends. Strategic partnerships with wellness platforms and retail chains enhance visibility and trial among urban consumers. Geographic expansion into Northern and Eastern Europe focuses on premium organic offerings tailored to local taste preferences. Digital marketing and direct-to-consumer subscription models further strengthen brand loyalty and data-driven personalization across the region.

Leading Players in the Market

- Unilever plays a pivotal role in the Europe green tea market through its Lipton and PG Tips brands, which offer a wide range of green tea variants, including organic and flavored options. The company has intensified its focus on sustainability by committing to recyclable packaging for all tea products. In recent years, Unilever has expanded its ready-to-drink green tea portfolio across Western Europe with low-sugar formulations tailored to health-conscious consumers. It has also partnered with European farmers to trial climate-resilient tea cultivation methods. These initiatives reinforce its commitment to both market relevance and environmental responsibility while enhancing product authenticity and supply chain transparency across the region.

- Nestlé contributes significantly to the Europe green tea landscape primarily through its NesTea and ready-to-drink green tea lines, which emphasize functional ingredients and premium positioning. The company has invested in cold brew technology to preserve catechin integrity and improve flavor profiles in bottled formats. It also strengthened its digital engagement through personalized nutrition apps that recommend green tea based on lifestyle data. These actions reflect Nestlé’s strategy to align green tea with holistic wellness trends and capture urban millennial consumers seeking convenience without compromising health values.

- TAZO Tea Company has established a distinctive presence in Europe by blending traditional green tea with bold global flavor profiles such as ginger lime and passionfruit. Owned by LIPTON Teas and Infusions, the brand targets younger demographics through vibrant packaging and ethical sourcing narratives. The company also collaborated with European wellness festivals to promote mindful consumption experiences. These efforts position TAZO as an innovator that bridges cultural authenticity with contemporary lifestyle values, thereby deepening consumer engagement beyond conventional tea categories.

MARKET SEGMENTATION

This research report on the Europe green tea market has been segmented and sub-segmented based on container type, product type, and region.

By Container Type

- Packaging in plastic bottles

- Packaging in Bags

- Packaging in cans

- Packaging in other containers

By Product Type

- Flavored green tea

- Unflavored green tea

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe green tea market?

The market is driven by increasing health consciousness, rising demand for antioxidant-rich beverages, and growing consumer preference for natural and functional drinks.

2. What are the major types of green tea available in Europe?

Popular varieties include matcha, sencha, jasmine green tea, flavored green tea, organic green tea, and ready-to-drink green tea products.

3. What are the health benefits associated with green tea consumption?

Green tea is known for its antioxidant properties and is often associated with supporting metabolism, heart health, immune function, and overall wellness.

4. Which distribution channels are important in the Europe green tea market?

Supermarkets, hypermarkets, specialty tea stores, convenience stores, online retail platforms, and foodservice outlets are key distribution channels.

5. What challenges does the Europe green tea market face?

Challenges include competition from other healthy beverages, fluctuating raw material prices, supply chain issues, and regulatory requirements related to health claims.

6. What opportunities exist in the Europe green tea market?

Opportunities include product innovation, premium tea offerings, expansion of ready-to-drink green tea products, and increasing demand for functional beverages.

7. Who are the key players operating in the Europe green tea market?

Major companies include Unilever, Tata Consumer Products, Twinings, ITO EN, Ltd., and Associated British Foods plc.

8. How is the ready-to-drink (RTD) segment impacting the market?

The growing demand for convenient and healthy beverage options is driving the popularity of ready-to-drink green tea products.

9. What role do antioxidants play in green tea demand?

Consumers increasingly seek antioxidant-rich beverages to support healthy lifestyles, making green tea a preferred choice.

10. What is the future outlook for the Europe green tea market?

The market is expected to witness steady growth due to rising health awareness, growing demand for functional beverages, premium product innovations, and expanding retail availability.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com