- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Europe Health Information Exchange Market Summary

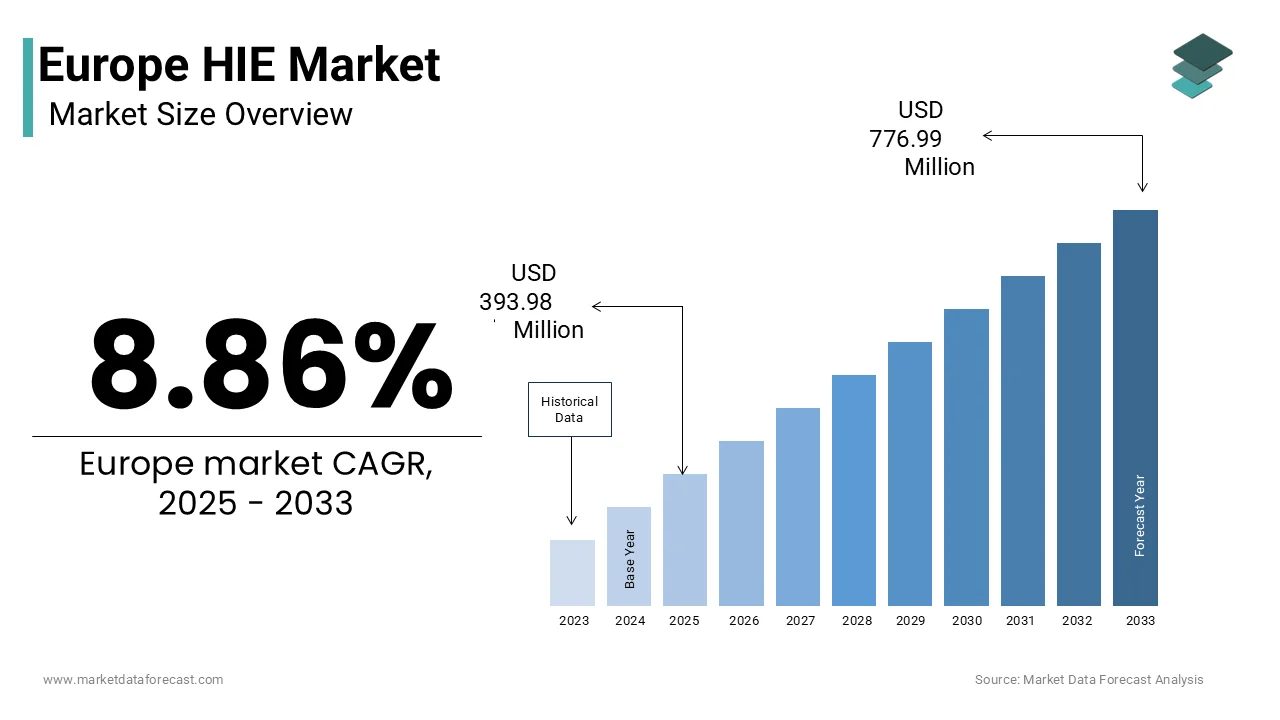

Europe health information exchange market was valued at USD 361.91 million in 2024, estimated at USD 393.98 million in 2025, and is projected to reach USD 776.99 million by 2033 (CAGR 8.86%, 2025–2033), driven by national digital health strategies, rising chronic disease burden, and the rollout of the European Health Data Space enabling secure cross-border clinical data exchange.

Market Highlights

- 2024 (actual): USD 361.91 million

- 2025 (est): USD 393.98 million

- 2033 (forecast): USD 776.99 million

- CAGR (2025–2033): 8.86%

Quick growth drivers

- National digital health strategies are accelerating interoperable EHR adoption across Europe.

- European Health Data Space (EHDS) mandates cross-border exchange of patient summaries, prescriptions, and diagnostics by 2027.

- Rising chronic disease prevalence is increasing demand for longitudinal, coordinated care.

- An ageing population requiring multi-provider data continuity across care settings.

- Value-based care models linking outcomes to timely clinical data access.

Principal restraints

- Fragmented interoperability standards across EU member states and regions.

- Strict GDPR and national privacy enforcement are increasing compliance complexity.

- Inconsistent consent frameworks limit secondary data use and research exchange.

- High integration costs for providers operating legacy health IT systems.

High-value opportunities

- Cross-border care enablement under EHDS, unlocking pan-European patient mobility.

- Consumer-mediated exchange models empower patients to control and share health data.

- AI-driven clinical decision support requires real-time, high-quality data pipelines.

- Federated research environments enabling secure data reuse without centralisation.

- Public–private digital health partnerships modernising national exchange infrastructure.

Key operational challenges

- Legacy IT infrastructure in public healthcare systems is slowing scalability.

- Shortage of health informatics and digital health professionals across Europe.

- Complex vendor integration across regional health systems.

- Balancing data sovereignty with innovation in analytics and AI deployment.

Fastest-growing segments

- Consumer-mediated exchange: 18.3% CAGR — patient empowerment and portal adoption.

- Hybrid implementation models: 16.7% CAGR — federated care with analytics capability.

- Medical research institutions (end users): 21% CAGR — EHDS-driven data reuse.

- Private HIE setups: 19% CAGR — research, speciality care, and medical tourism.

Regional leadership & dynamics

Germany (lead, 22.3%)

- Telematics Infrastructure with near-universal provider participation.

- Strong statutory mandates and reimbursement-linked interoperability compliance.

France (16.8%)

- Centralised Health Data Hub and nationwide patient portal adoption.

- Strong focus on research-oriented data reuse.

United Kingdom (13.1%)

- Mature NHS Spine and large-scale patient-facing exchange services.

- Continued alignment with HL7 FHIR and EU interoperability norms.

Netherlands & Nordics

- High interoperability maturity and privacy-preserving federated models.

- Benchmarks for cross-border exchange efficiency.

What wins commercially

- Federated, privacy-first exchange architectures aligned with GDPR and EHDS.

- HL7 FHIR–native platforms enabling seamless cross-border interoperability.

- Patient-centric consent and data access tools.

- Scalable APIs supporting AI and analytics integration.

- Strong public-sector alignment with national health authorities.

Top strategic ask for executives

- Align product roadmaps with EHDS interoperability and governance requirements.

- Invest in FHIR-based, AI-ready exchange infrastructure.

- Support patient-mediated data sharing alongside provider networks.

- Build local compliance expertise across key European markets.

Leading players

Cerner · Epic Systems · Philips Healthcare · InterSystems · Orion Health · Optum · Allscripts · Infor · NextGen Healthcare · Covisint · RelayHealth · eClinicalWorks · Medecision

Europe HIE Market Size

The europe health information exchange market was valued at USD 361.91 million in 2024. is expected to have an 8.86 % CAGR from 2025 to 2033 and be worth USD 776.99 million by 2033 from USD 393.98 million in 2025.

The Europe Health Information Exchange market comprises interoperable digital infrastructures designed to enable secure, real-time sharing of clinical and administrative health data among hospitals, general practitioners, laboratories, pharmacies, and public health agencies across national and regional boundaries. These systems are central to the European Union’s vision of a unified digital health ecosystem under the European Health Data Space initiative. As per Eurostat, over sixty-five per cent of general practitioners in the European Union used electronic health record systems in 2023, yet cross-institutional data sharing remains limited. According to the Organisation for Economic Co-operation and Development, only about forty-two per cent of European hospitals could electronically exchange patient summaries with external providers in 2022. The European Commission estimates that seamless health data exchange could reduce avoidable hospital admissions by up to fifteen per cent annually, highlighting the strategic urgency of robust exchange mechanisms in Europe’s increasingly integrated yet fragmented healthcare landscape.

MARKET DRIVERS

Accelerated Adoption of National Digital Health Strategies Fuels Demand

European nations have intensified investments in integrated health data ecosystems as part of broader digital transformation agendas. Germany’s Telematics Infrastructure, for instance, connected over forty-five million insured individuals to a unified health data network by early 2024, as per the German Federal Ministry of Health. Similarly, France’s Health Data Hub, launched in 2020, now aggregates anonymised records from more than seventy million citizens to support clinical research and public health surveillance, according to France’s Ministry of Solidarity and Health. The Nordic countries exemplify regional leadership, with Sweden achieving near universal adoption of national electronic health records among primary care providers, as confirmed by the Swedish eHealth Agency. These national programs create a fertile environment for health information exchange by establishing standardised data formats, consent management protocols, and secure messaging gateways. The European Commission’s 2023 Digital Health and Care Strategy further reinforces this momentum by mandating that all member states implement cross-border health data exchange capabilities under the European Health Data Space by 2027. Such policy-driven digitisation not only expands the addressable scope for interoperable platforms but also cultivates user readiness among both providers and patients, driving consistent demand for scalable exchange solutions tailored to Europe’s fragmented yet converging regulatory landscape.

Rising Burden of Chronic Diseases Intensifies Need for Coordinated Care

The growing prevalence of chronic conditions across Europe has amplified demand for health information exchange systems that enable longitudinal care management. According to the World Health Organisation, non-communicable diseases account for approximately eighty-six per cent of all deaths in the European Region, with cardiovascular disorders, diabetes, and respiratory illnesses representing the leading causes. In 2023, the European Centre for Disease Prevention and Control reported that over one hundred seventy million Europeans live with at least one chronic condition, often requiring input from multiple specialists over extended periods. This complexity necessitates seamless data flow between primary, secondary, and community care settings to avoid treatment fragmentation. For example, in the Netherlands, integrated care pathways for diabetes patients that leverage shared digital records have demonstrated a twenty-two per cent reduction in emergency department visits, as per the Dutch National Institute for Public Health and the Environment. Likewise, Spain’s Andalusian Regional Health Service attributes a fifteen per cent improvement in hypertension control rates to its interconnected clinical data platform, according to its 2022 performance review. These outcomes validate health information exchange as a critical enabler of value-based care, where timely access to comprehensive patient histories directly influences clinical efficacy, patient safety, and system efficiency across Europe’s ageing populations.

MARKET RESTRAINTS

Persistent Fragmentation in Data Standards Hinders Interoperability

Despite policy harmonisation efforts, Europe continues to grapple with divergent technical and semantic standards across national health information systems, significantly impeding seamless data exchange. While the European Committee for Standardisation has endorsed the use of HL7 FHIR and SNOMED CT as baseline interoperability frameworks, actual implementation varies widely. As per a 2023 assessment by the European Institute for Health Records, only eleven of the twenty-seven European Union member states have fully adopted SNOMED CT for clinical documentation, while others rely on legacy coding systems such as ICD-10 or local terminologies. This inconsistency creates barriers when attempting to aggregate or interpret data across borders. For instance, a patient’s medication list recorded in Germany’s ePrescription system may not be machine-readable in a Polish hospital due to incompatible data models, as noted in a joint study by the European Health Management Association and the Technical University of Berlin. Furthermore, regional disparities within countries exacerbate the issue. Italy’s twenty-one regional health systems operate under distinct IT architectures, according to Italy’s National Agency for Regional Health Services, complicating nationwide data integration. Such fragmentation not only increases implementation costs for vendors but also delays the realisation of cross-border care coordination envisioned under the European Health Data Space, thereby constraining market scalability and uniform adoption.

Stringent and Evolving Data Privacy Regulations Create Compliance Complexity

The regulatory environment governing health data in Europe remains one of the most rigorous globally, with the General Data Protection Regulation establishing strict conditions for processing personal health information. While essential for protecting patient rights, these provisions impose significant operational burdens on health information exchange initiatives. According to the European Data Protection Board, health data qualifies as a special category under Article 9 of the General Data Protection Regulation, requiring explicit consent or a specific legal basis for each data sharing instance. In practice, this complicates secondary uses of data for research or public health monitoring. A 2024 survey by the European Federation of Pharmaceutical Industries and Associations found that seventy-three per cent of clinical trial sponsors reported delays in accessing real-world patient data due to inconsistent interpretations of consent requirements across member states. Moreover, the upcoming European Health Data Space Regulation, while promoting data reuse, introduces additional governance layers, including the mandatory appointment of data altruism coordinators and strict audit trails, as outlined by the European Commission. National data protection authorities further diverge in enforcement; for example, France’s CNIL has issued detailed guidance on anonymisation thresholds, whereas Germany’s Federal Commissioner for Data Protection maintains stricter pseudonymization standards, according to comparative analyses by the Centre for Information Policy Leadership. This regulatory heterogeneity increases legal uncertainty and implementation costs, deterring smaller healthcare providers from participating in exchange networks.

MARKET OPPORTUNITIES

Expansion of Cross-Border Care Under the EHDS Unlocks New Data Flows

The European Health Data Space represents a transformative opportunity by institutionalising cross-border access to electronic health records for both patients and providers. As per the European Commission, over two million European citizens seek medical care in another member state annually, yet until recently, clinical information often remained siloed within national systems. The European Health Data Space Regulation, adopted in 2024, mandates that by 2027 all member states enable the exchange of key documents such as discharge summaries, prescriptions, and diagnostic reports across borders using standardised digital formats. Pilot projects under the Connecting Europe Facility for Health have already demonstrated feasibility in the Baltic region, Estonia, Latvia, and Lithuania, achieving interoperable exchange of patient summaries in 2023, allowing over one hundred fifty thousand cross-border consultations to be supported with shared clinical data, according to the European Health Telematics Observatory. This regulatory push is catalysing demand for exchange platforms capable of multilingual, multi-jurisdictional data handling. Furthermore, it incentivises national health authorities to modernise legacy infrastructures to comply with pan-European standards, thereby expanding the technical and operational footprint of health information exchange vendors. The initiative not only enhances patient mobility but also generates rich, anonymised datasets for health technology assessment and policy modelling, positioning Europe as a global leader in federated health data governance.

Integration of Artificial Intelligence in Clinical Workflows Demands Robust Data Pipelines

The rapid integration of artificial intelligence into European healthcare systems is creating a compelling opportunity for health information exchange platforms to serve as foundational data enablers. As per the European Artificial Intelligence Office, over sixty per cent of EU-based hospitals piloted at least one artificial intelligence application in 2024, ranging from radiology image analysis to predictive risk stratification for sepsis. However, these algorithms require high-quality, standardised, and continuously updated clinical data to function effectively. Health information exchange systems that provide real-time access to comprehensive patient records, including lab results, medication histories, and vital signs, become indispensable for training and deploying such models. For example, the United Kingdom’s National Health Service reported in 2023 that its AI-enabled diabetic retinopathy screening program achieved ninety-eight per cent diagnostic accuracy only after integration with national primary care data via the NHS Spine, according to NHS Digital. Similarly, Finland’s Kanta Services platform, which aggregates data from over five million citizens, has been instrumental in supporting artificial intelligence-driven oncology decision support tools, as confirmed by the Finnish Institute for Health and Welfare. These implementations underscore a strategic shift: health information exchange is no longer just a record-sharing utility but a critical data infrastructure layer for next-generation clinical intelligence. Vendors that embed application programming interfaces compatible with artificial intelligence development environments stand to gain significant traction as European healthcare digitisation converges with intelligent analytics.

MARKET CHALLENGES

Legacy Infrastructure in Public Health Systems Limits Scalability

Many European countries continue to rely on outdated information technology systems within their publicly funded healthcare networks, creating substantial technical debt that impedes the deployment of modern health information exchange solutions. In Greece, for instance, over sixty per cent of public hospitals still operate on electronic medical record systems developed before 2010, lacking application programming interfaces or standardised data export functions, as per the Hellenic Ministry of Health’s 2023 Digital Transformation Audit. Similar constraints exist in parts of Eastern Europe; Romania’s public hospitals use more than fifteen different electronic health record vendors, none of which natively support HL7 FHIR, according to the Romanian National Authority for Digital Transformation. Even in more advanced systems, legacy components persist. Germany’s early telematics modules, rolled out between 2019 and 2021, require middleware upgrades to support real-time data streaming, as noted in a 2024 technical assessment by the German Association of Health IT Vendors. These infrastructural limitations increase integration costs, extend implementation timelines, and often necessitate parallel system maintenance. Consequently, healthcare providers face budgetary and operational barriers to adopting comprehensive exchange platforms, particularly when national reimbursement schemes do not cover modernisation expenses. This technological inertia slows the pace of interoperability across Europe and creates a fragmented adoption curve that complicates vendor scalability and standardisation efforts.

Workforce Shortages Exacerbate Implementation and Maintenance Gaps

Europe’s critical shortage of health information technology professionals significantly undermines the operational viability of health information exchange initiatives. According to the World Health Organisation’s 2024 European Health Workforce Report, the region faces a deficit of over three hundred thousand digital health specialists, including clinical informaticians, health data architects, and cybersecurity analysts. This scarcity is particularly acute in rural and underserved areas; in Portugal, only twenty-eight per cent of regional health centres employ dedicated health IT staff, as per the Portuguese Directorate General of Health. The consequences are that tangible healthcare facilities without in-house expertise struggle to configure, troubleshoot, or optimise exchange platforms, leading to underutilization. A 2023 study by the European Health Management Association found that hospitals with fewer than two full-time informatics personnel were three times more likely to report incomplete data synchronisation and user dissatisfaction with exchange tools. Moreover, the burden often falls on clinical staff, who lack training in data governance or interface management, further reducing system adoption. Compounding the issue, academic pipelines remain insufficient; the European Union’s Digital Education Action Plan acknowledges that fewer than fifteen universities across the bloc offer accredited degrees in health informatics. Without a robust talent base to support deployment, customisation, and ongoing maintenance, even the most advanced exchange platforms risk becoming shelfware, thereby stifling market growth and equitable digital health access across Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Implementation mode, Setup Type, Application, End-User Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Aetna Medcity, eClinical Works, RelayHealth, Medecision, Epic Corporation Inc., Cerner Corporation, RelayHealth Corporation, Infor Inc., Intersystems, Optum Inc., Alere Wellogic, NextGen Healthcare Information Systems, LLC, Covisint Corporation, Allscripts Healthcare Solutions Inc., and Orion Health. |

SEGMENTAL ANALYSIS

By Type Insights

Query-Based Exchange holds the largest share of the European Health Information Exchange market, estimated at approximately forty-eight per cent in 2024. This model enables authorised providers to search for and retrieve patient data from other entities at the point of care, aligning closely with Europe’s emphasis on data minimisation and on-demand access under the General Data Protection Regulation. According to the European Institute for Health Records, over sixty per cent of cross-institutional clinical data requests in Germany, France, and the Netherlands in 2023 were fulfilled through query-based mechanisms, primarily due to their ability to preserve data sovereignty while supporting urgent care coordination. A key driver is the integration of this model into national eHealth gateways. Sweden’s National Patient Overview, for instance, processes more than two million clinical data queries annually, as per the Swedish eHealth Agency. Unlike direct messaging, which relies on re-established workflows, query-based exchange offers dynamic, context-relevant access without requiring full data replication, making it particularly suitable for Europe’s decentralised healthcare systems, where patient records remain institutionally anchored yet must be accessible on demand.

Consumer Mediated Exchange is the fastest-growing segment in the European Health Information Exchange market, projected to expand at a compound annual growth rate of 18.3 per cent from 2024 to 2030. This acceleration stems from rising patient empowerment initiatives and regulatory shifts enabling individuals to control and share their own health data. As per the European Commission’s 2024 Digital Rights Survey, seventy-one per cent of EU citizens expressed a desire to access and manage their electronic health records directly, with over half willing to share data with secondary care providers. National programs are responding. Finland’s Kanta Patient Portal allows over four million users to view lab results, prescriptions, and care summaries, and in 2023 recorded a thirty-two per cent year-on-year increase in active users, according to the Finnish Institute for Health and Welfare. Similarly, the UK’s NHS App now serves more than thirty-five million users, with personal health record exports increasing by forty per cent in 2024, as reported by NHS Digital. These platforms are evolving beyond passive viewing to active data brokering, where patients authorise third-party apps or researchers to access curated datasets, aligning with the European Health Data Space’s vision of data altruism and participatory health governance.

By Implementation Model Insights

Decentralised or federated models dominate the European Health Information Exchange market with an estimated fifty-two per cent share in 2024. This architecture, where data remains stored locally at source institutions and is accessed via secure queries without central aggregation, resonates deeply with Europe’s legal and cultural emphasis on data localisation and institutional autonomy. According to a 2023 interoperability benchmark by the European Health Telematics Observatory, seventeen of the twenty-seven EU member states have adopted federated models as their national standard, citing compliance with Article 7 of the cross-border Healthcare Directive, which mandates that health data not be stored outside the originating country without explicit consent. Germany’s Telematics Infrastructure exemplifies this approach, linking over one hundred thousand healthcare sites while keeping all clinical records within local practice servers, as confirmed by the German Federal Ministry of Health. Likewise, Estonia’s X Road platform, used across the Baltic states, enables real-time cross-border data exchange without central storage, supporting over two hundred million secure transactions annually, according to the Estonian Health and Development Institute. This model minimises cybersecurity risks, reduces migration costs, and aligns with the principle of subsidiarity that underpins European health policy.

The Hybrid Model is emerging as the fastest-growing implementation approach, projected to grow at a compound annual growth rate of 16.7 per cent through 2030. It combines the security and control of federated architectures with the analytical power of centralised data lakes for specific use cases such as public health surveillance or clinical trials. The European Commission’s 2024 European Health Data Space rollout has accelerated this trend by requiring member states to establish trusted research environments that can temporarily consolidate anonymised datasets under strict governance. France’s Health Data Hub operates under this logic, while clinical records remain with providers, de-identified data is aggregated into a national analytics platform that now supports over four hundred fifty research projects, as per France’s Ministry of Solidarity and Health. Similarly, the Netherlands’ Health Data Network uses a hybrid architecture to enable both real-time clinical exchange and retrospective cohort studies, processing over five billion data points annually, according to the Dutch National Institute for Public Health and the Environment. This duality meets Europe’s dual mandate: protecting individual privacy while unlocking data for innovation, making hybrid systems increasingly indispensable for health systems, and balancing care delivery with evidence generation.

By Setup Type Insights

Publicly deployed health information exchange systems command the majority share of the European market, estimated at sixty per cent in 2024. This dominance reflects Europe’s predominantly publicly funded healthcare systems, where national or regional governments act as both regulator and infrastructure provider. According to the Organisation for Economic Co-operation and Development, twenty-one of the twenty-seven EU countries operate national or regionally mandated health information exchange platforms under public stewardship. In Sweden, the national patient overview system is fully funded and managed by the Swedish eHealth Agency, achieving near universal coverage across all counties by 2023, as confirmed by the Swedish National Board of Health and Welfare. Similarly, Spain’s Diraya platform in Andalusia, a publicly run system, connects all public hospitals and primary care centres, serving over nine million residents with integrated records, according to the Andalusian Ministry of Health. These systems benefit from sustained budgetary support, legal mandates for provider participation, and alignment with broader digital public service strategies, ensuring long-term sustainability and scale that private models struggle to match in Europe’s highly regulated environment.

The Private Setup segment is the fastest growing, with a projected compound annual growth rate of 19 per cent from 2024 to 2030. This surge is driven by the expansion of private healthcare networks, cross-border medical tourism, and specialised digital health vendors offering interoperability as a service. In Germany, where over thirty per cent of outpatient care is delivered by private practices, proprietary exchange platforms like CompuGroup Medical’s CGM LINK now connect more than twenty-five thousand physicians, as per the company’s 2024 operational report validated by Germany’s Federal Association of Statutory Health Insurance Physicians. Similarly, in Switzerland, a country with a highly privatised health system, private hospital groups such as Hirslanden and Genolier have deployed internal exchange ecosystems that also interface with public registries, supporting over one hundred fifty thousand patient records annually, according to the Swiss Medical Informatics Association. Additionally, private setups are gaining traction in clinical research, where contract research organisations require fast, compliant data pipelines; IQVIA’s European Trial Exchange reported a forty-five per cent increase in private health data onboarding in 2023, as per its annual transparency review. This agility customisation and responsiveness to niche needs position private models as critical complements to public infrastructure.

By End User Insights

Healthcare providers constitute the largest end-user segment in the European Health Information Exchange market, accounting for an estimated fifty-seventeenth share in 2024. Hospitals, clinics, and general practices are the primary generators and consumers of clinical data, making them natural anchor points for exchange adoption. According to the European Commission’s 2023 Digital Health Survey, eighty-four per cent of European hospitals with more than two hundred beds had implemented at least one form of health information exchange by 2023, primarily to reduce duplicate testing and streamline referrals. In Denmark, the national MedCom infrastructure enables over nine hundred thousand clinical messages per day between providers, reducing average referral processing time from fourteen days to under forty-eight hours, as per the Danish Health Authority. Germany’s hospital sector has integrated exchange into routine workflows, with ninety per cent of acute care facilities using the Telematics Infrastructure for ePrescriptions and discharge summaries, according to the German Hospital Federation. This dominance is sustained by clinical necessity, regulatory incentives, and reimbursement policies that increasingly tie payment to interoperability compliance, ensuring continued investment from provider organisations across the continent.

Medical Research Institutions represent the fastest growing end user segment, projected to expand at a compound annual growth rate of 21.per cent through 2030. This growth is fueled by the European Union’s strategic push to position health data as a public good for scientific advancement under the European Health Data Space. As per the European Medicines Agency, over two hundred eighty clinical trial sponsors accessed federated research data environments in Europe in 2024, a six per cent increase from 2022. The Swedish National Pandemic Centre, for example, leverages real-time exchange data from primary care and hospitals to model vaccine effectiveness, publishing findings in The Lancet based on records from over three million citizens, according to the Karolinska Institute. Likewise, the French National Institute of Health and Medical Research now coordinates a pan-European oncology data network that aggregates de-identified records from twelve countries, supporting over sixty active trials, as confirmed by its 2024 research impact report. With the European Commission allocating over one billion euros to health data research infrastructure under Horizon Europe, academic and research entities are rapidly scaling their exchange capabilities not to deliver care, but to generate it through evidence, making this segment the most dynamic in the ecosystem.

COUNTRY LEVEL ANALYSIS

Germany Health Information Exchange Market Analysis

Germany holds the largest national share of the European Health Information Exchange market at 22.3 per cent in 2024, driven by its comprehensive Telematics Infrastructure and statutory mandates. The country operates one of the most advanced nationwide exchange ecosystems, connecting over one hundred thousand healthcare sites, including all statutory health insurance providers, pharmacies, and hospitals. As per the German Federal Ministry of Health, more than ninety-five per cent of insured citizens were issued electronic health cards by early 2024, enabling secure authentication for data exchange. The system processed over five hundred million ePrescriptions in 2023 alone, according to the German National Association of Statutory Health Insurance Physicians. Regulatory enforcement through the E-Health Act, coupled with financial incentives for provider adoption, has ensured near universal participation. Germany’s leadership is further reinforced by its role in shaping EU interoperability standards, positioning it not only as a market leader but also as a technical and policy trendsetter for the region.

France Health Information Exchange Market Analysis

France commands the second largest market share at 16.8 per cent, underpinned by a centralised yet privacy-compliant Health Data Hub and an aggressive digital health roadmap. Launched in 2020, the Health Data Hub now integrates data from over seventy million citizens across public hospitals, primary care, and medico administrative databases. According to France’s Ministry of Solidarity and Health, the platform supported more than four hundred fifty research projects in 2023, including national studies on long COVID and cardiovascular risk. The Mon Espace Santé patient portal, rolled out to all citizens by 2024, has achieved over forty million registered users, enabling personal data sharing and access to medical records. France’s 2023 Digital Health Act mandates all healthcare professionals to connect to the national exchange infrastructure by 2026, accelerating adoption. This blend of state-driven coordination, public trust, and research orientation has solidified France’s position as a pivotal market in Europe’s health data landscape.

United Kingdom Health Information Exchange Market Analysis

The United Kingdom holds the third largest market share at 13.1 per cent, distinguished by its mature NHS Spine and rapidly expanding patient-facing services. Despite Brexit, the UK remains deeply integrated into European health data norms through its Global Digital Exemplar program and interoperability standards aligned with HL7 FHIR. As per NHS Digital, the NHS App reached thirty-five million active users in 2024, with over six million patients viewing their full medical records monthly. The national Summary Care Record, accessible by authorised clinicians across England, contains data for more than sixty million individuals and was accessed over two hundred million times in 2023, according to the Department of Health and Social Care. Recent investments in cloud-based exchange infrastructure and AI-driven analytics have further modernised the ecosystem. While devolved administrations in Scotland and Wales maintain separate systems, cross-border data protocols with the EU under the UK Health Data Strategy ensure continued relevance in the broader European context.

Netherlands Health Information Exchange Market Analysis

The Netherlands ranks fourth with an 8.7 per cent market share, recognised for its highly interoperable and privacy-preserving national infrastructure. The country’s Health Information Exchange network, coordinated by Nictiz, links all hospitals, general practices, and pharmacies through standardised messaging and document sharing. According to the Dutch National Institute for Public Health and the Environment, over ninety eight cent of Dutch general practitioners exchanged clinical data electronically in 2023, with patient summaries shared across institutions more than ten million times annually. The Netherlands was among the first EU members to implement the International Patient Summary under the Cross-Border Directive, facilitating care for over three hundred thousand mobile patients each year, as per the Dutch Ministry of Health. Strong collaboration between public agencies, professional associations, and vendors under the Dutch Digital Health Pact has created a harmonised ecosystem where technical, legal, and cultural barriers to exchange are systematically addressed, making it a benchmark for small but high-performing health data markets.

Sweden Health Information Exchange Market Analysis

Sweden holds the fifth largest market share at 7.2 per cent, distinguished by its citizen-centric and seamlessly integrated national system. The Swedish National Patient Overview, managed by the Swedish eHealth Agency, provides real-time access to medical records across all twenty-one counties, with participation from virtually all public healthcare providers. As per the Swedish National Board of Health and Welfare, the system processed over two million clinical data queries in 2023, reducing duplicate diagnostics by an estimated eighteen per cent. Sweden’s success stems from early digitisation, electronic health records have been mandatory in primary care since 2009, and a strong legal framework that balances data access with privacy, including patient rights to see who accessed their records. Additionally, Sweden actively contributes to EU interoperability initiatives, hosting the European Institute for Health Records and piloting cross-border exchange with Norway and Denmark. This combination of technical maturity, public trust, and regional leadership ensures Sweden remains a key player despite its modest population size.

COMPETITIVE LANDSCAPE

Competition in the European Health Information Exchange market is characterised by a blend of global technology leaders and specialised regional vendors vying for influence amid fragmented regulatory and technical landscapes. Global players bring mature interoperability engines and cloud scale, but must adapt to Europe’s stringent data sovereignty norms and decentralised care models. Meanwhile, local firms leverage deep knowledge of national health systems and legacy integration pathways to maintain strong footholds. Innovationcentress on balancing real-time clinical exchange with research-oriented data reuse under the European Health Data Space. Differentiation arises through compliance agility, patient empowerment features, and public sector collaboration. As cross-border care and AI-driven analytics gain traction, the competitive arena is shifting from mere data transfer toward intelligent, governance-aware data ecosystems that serve both care delivery and public health missions across the continent.

KEY MARKET PLAYERS

Companies playing an influential role in the europe health information exchange market are

- Aetna Medcity

- eClinical Works

- RelayHealth

- Medecision

- Epic Corporation Inc.

- Cerner Corporation

- RelayHealth Corporation

- Infor Inc.

- Intersystems

- Optum Inc.

- Alere Wellogic

- NextGen Healthcare Information Systems, LLC

- Covisint Corporation

- Allscripts Healthcare Solutions Inc.

- Orion Health

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Health Information Exchange market prioritise strategic alignment with national digital health roadmaps by tailoring their platforms to meet country-specific regulatory and technical standards. They invest heavily in HL7 FHIR and open API development to ensure compatibility with the European Health Data Space framework. Companies actively form public-private partnerships with ministries of health and regional agencies to co-develop secure, scalable exchange infrastructures. They also embed patient-centric functionalities such as portal integration and data donation consent mechanisms to comply with evolving privacy norms. Additionally, vendors expand their presence through localised cloud deployments that address data residency requirements while enabling cross-border interoperability for research and emergency care coordination.

TOP LEADING PLAYERS IN THE MARKET

- Cerner Corporation plays a pivotal role in the European Health Information Exchange market through its integrated electronic health record platforms and interoperability frameworks. The company supports national digital health programs across several European countries by enabling seamless data exchange between hospitals, laboratories, and public health agencies. In 2024, Cerner expanded its collaboration with the Danish Health Authority to enhance real-time clinical data sharing across regional health systems. It also launched a federated data query module compliant with the European Health Data Space standards, reinforcing its commitment to privacy-preserving exchange architectures and strengthening its footprint in value-based care ecosystems throughout Europe.

- Epic Systems Corporation contributes significantly to the European health information landscape by deploying its proprietary interoperability engine, Care Everywhere, in academic medical centres and integrated care networks. Although historically US-focused, Epic has deepened its European presence by partnering with University Hospital Zurich and Oslo University Hospital to implement cross-border data sharing capabilities. In 2024, the company integrated HL7 FHIR APIs aligned with EU standards, enabling patients to access and share records via national portals. These strategic adaptations demonstrate Epic’s responsiveness to European regulatory expectations and its growing influence in enabling secure, patient-centred data liquidity across high complexity health systems.

- Philips Healthcare leverages its deep integration with hospital infrastructure to advance health information exchange across Europe. The company’s HealthSuite Digital Platform serves as a neutral data aggregation layer that connects disparate clinical systems while supporting analytics and remote monitoring. In 2024, Philips collaborated with France’s AP HP hospital group to deploy a unified exchange gateway across thirteen teaching hospitals, enabling real-time access to imaging, lab, and vital signs data. It also enhanced its platform with consumer-mediated data-sharing features compatible with national patient portals. These initiatives underscore Philips’ focus on embedding interoperability within clinical workflows rather than as a standalone IT function, positioning it as a key enabler of connected care in Europe.

EUROPE HEALTH INFORMATION EXCHANGE MARKET NEWS

- In March 2024, Cerner Corporation partnered with the Swedish eHealth Agency to enhance the National Patient Overview with real-time medication reconciliation capabilities across all twenty-one counties.

- In May 2024, Philips Healthcare launched a hybrid exchange gateway with AP HP in France,ce enabling federated data access for over thirteen university hospitals while supporting anonymised data pooling for clinical research.rch

- In February 2024, Epic Systems Corporation completed the integration of its Care Everywhere platform with Norway’s national health portal, allowing cross-border patient record access between Oslo University Hospital and Swedish providers.

- In June 2024, Cerner Corporation introduced a General Data Protection consumer-mediated exchange module compatible with Germany’s Telematics Infrastructure for use by over twenty-five thousand private practices.

- In April 2024, Philips Healthcare collaborated with the Dutch National Institute for Public Health to deploy a secure data pipeline linking hospital discharge summaries to municipal home care systems across the Netherlands.ds.

MARKET SEGMENTATION

This research report on the europe health information exchange market is segmented and sub-segmented into the following categories.

By Type

- Direct Exchange

- Query-Based Exchange

- Consumer Mediated Exchange

By Implementation mode

- Centralised

- ed/Consolidated Models

- Decentralised/Federated Models

- Hybrid Model

By Setup Type

- Private

- Public

By Application

- Internal Interfacing

- Secure Messaging

- Workflow management

- Web Portal Development

- Patient Safety

By Component-based

- Enterprise Master Person Index (EMPI)

- Healthcare Provider Directory (HPD)

- Record Locator Service (RLS)

- Clinical Data Repository

By End-User

- Healthcare provider

- Public Health Agency

- Medical Research Institution

- Medical Professional

- Patient

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland,

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe