Europe Healthcare IT Market Size, Share, Trends & Growth Forecast Report By Type and Country (Germany, UK, France, Italy, Rest of Europe) – Industry Analysis From 2026 to 2034.

Europe Healthcare IT Market Size

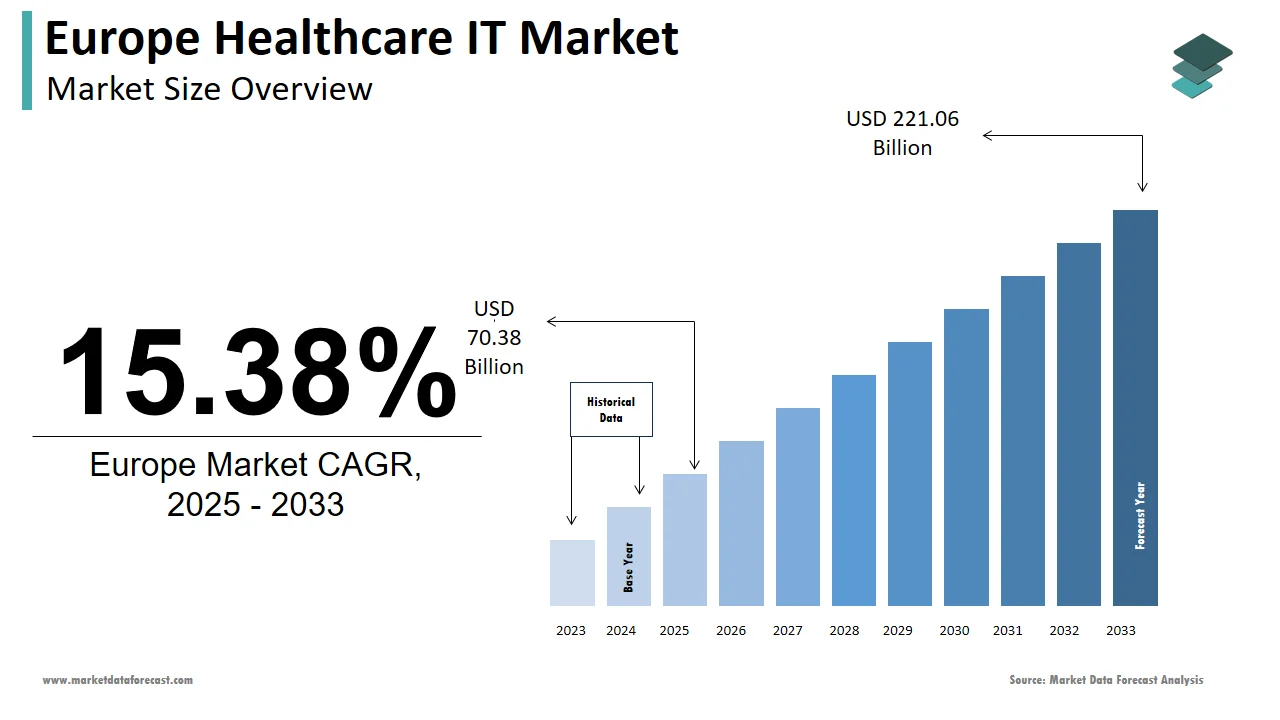

The healthcare IT market size in Europe was valued at USD 70.38 billion in 2025. The European market is estimated to be worth USD 255.05 billion by 2034 from USD 81.20 billion in 2026, growing at a CAGR of 15.38% from 2026 to 2034.

Healthcare IT refers to the digital technologies engineered to manage clinical information, optimize administrative operations, and elevate the quality and efficiency of patient care across hospitals, outpatient clinics, and long-term care institutions. Core components include electronic health records, health information exchanges, telehealth infrastructures, clinical decision support systems, and cybersecurity frameworks tailored specifically for healthcare environments.

As of early 2025, the urgency for digital transformation in European healthcare is intensifying, propelled by demographic and workforce pressures. According to Eurostat, individuals aged 65 years or older constituted more than 21 percent of the European Union’s population in 2024, significantly increasing demand for chronic disease management and coordinated care. As per research, the majority of European Union member states have developed national digital health strategies that align with broader EU policy goals for 2030. Europe is also experiencing a significant shortage of healthcare professionals, which is driving increased adoption of automation, remote monitoring, and data-driven care models, according to sources. These structural dynamics emphasize the critical need for secure, interoperable, and scalable health IT infrastructure across the region.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Fuels Demand for Integrated Health IT Systems

Chronic non-communicable diseases drive the growth of the Europe healthcare IT market. According to the World Health Organization, chronic conditions continue to be the leading cause of mortality in Europe, with diseases like diabetes affecting a large segment of the population. This epidemiological reality necessitates continuous monitoring, multidisciplinary coordination, and longitudinal data sharing, functions that integrated health IT platforms are uniquely positioned to deliver. Germany has developed comprehensive national registries linking electronic health records to improve early intervention and disease management, according to sources. The United Kingdom is advancing digital health initiatives through the NHS Long Term Plan, aiming to cover all chronic disease patients with digital care records soon, as per research. These initiatives illustrate how population health imperatives are directly translating into institutional demand for interoperable, analytics-driven health IT solutions that support proactive and preventive care models across fragmented care settings.

EU Regulatory Frameworks Mandate Digital Health Infrastructure Modernization

Legislative action at the European Union level is accelerating the expansion of the Europe healthcare IT market. The European Health Data Space Regulation has introduced a unified legal framework to promote cross-border health data exchange, with member states required to standardize electronic health records, as per research. According to sources, hospitals and general practices across Europe are working to reach interoperability targets ahead of schedule to comply with this regulation. Cybersecurity is also a growing focus, with new legislation imposing strict requirements on digital health software and connected medical devices, as per research. France’s Health Data Hub is leading by example, integrating millions of patient records in alignment with these standards in preparation for a full national rollout, according to sources. These regulatory instruments not only generate compliance-driven investment but also foster public and professional trust in data sharing, enabling secondary uses of health data for research, policy, and innovation, and thereby supporting the structural necessity for advanced health IT infrastructure.

MARKET RESTRAINTS

Fragmented Health Data Ecosystems Impede Interoperability and Scale

Systemic fragmentation in data standards and legacy infrastructure restricts the growth of the Europe healthcare IT market. As per research, only a portion of European hospitals utilize electronic health record systems that fully comply with the latest EU interoperability standards. National health systems often operate on mutually incompatible platforms. Germany alone hosts numerous distinct hospital information systems with limited data exchange capabilities. This fragmentation inflates integration costs and disrupts care coordination, especially in cross-border contexts. According to a study, A significant challenge for multi-country and cross-border referral networks is the lack of standardized health data, which requires clinicians to spend extra time reconciling disparate electronic health records (EHRs) and other data formats. Moreover, smaller practices in Southern and Eastern Europe frequently rely on paper-based or obsolete digital systems due to budgetary constraints. As per research, digital record-keeping infrastructure remains underdeveloped in many primary care facilities in Romania, Bulgaria, and Greece, which showcases regional disparities in digital health adoption across Europe. These incompatibilities not only reduce clinical efficiency but also obstruct the realization of a truly unified European health data space.

Persistent Cybersecurity Vulnerabilities Affect Stakeholder Confidence

The rapid digitization of healthcare has exposed the sector to escalating cyber threats, which constrain the expansion of the Europe healthcare IT market. This erodes confidence among patients, providers, and policymakers. According to ENISA, the European Union Agency for Cybersecurity, healthcare was one of the key sectors for ransomware attacks in 2024, with a year-on-year increase in incidents. Many breaches originate from outdated software, insufficient staff training, and underinvestment in cyber resilience. As per research, cybersecurity practices such as regular penetration testing and off-site encrypted data backups are not yet widely implemented across European hospitals by indicating ongoing vulnerabilities in healthcare cybersecurity. The General Data Protection Regulation (GDPR) offers a robust privacy framework; however, without specialized enforcement for healthcare, its implementation remains inconsistent. The 2021 cyberattack on Ireland’s Health Service Executive serves as a significant example of the potential consequences of such systemic weaknesses, according to sources. Greater adoption of health IT depends on shifting from a bolted-on security model to one where cybersecurity is foundational to the architecture, thereby lowering perceived risks.

MARKET OPPORTUNITIES

Expansion of AI-Enabled Clinical Decision Support Systems

Artificial intelligence is setting up new opportunities for the growth of the Europe healthcare IT market. Namely, through clinical decision support tools that enhance diagnostic precision and therapeutic planning. As per studies, AI has shown the ability to improve the accuracy and efficiency of medical image analysis, reduce diagnostic errors from human fatigue, and decrease misdiagnosis risks. The EU's AI Act came into force in 2024, with its requirements for high-risk AI medical devices phasing in over the next several years. This regulatory change marks a significant trend towards stricter governance for AI systems in healthcare. Clinical trials and real-world studies of AI sepsis prediction systems, such as the TREWS model, have demonstrated improved patient outcomes, including reduced time to treatment and lower mortality rates in some cohorts.. These innovations thrive on Europe’s expanding pool of standardized health data, accelerated by the European Health Data Space. Furthermore, the EU’s Horizon Europe program allocated funds for trustworthy AI in healthcare, causing public-private research consortia. Europe's digital health future will rely on AI augmentation to sustain care quality as clinician shortages are expected to increase.

Growth of Remote Patient Monitoring in Post-Acute and Home Care Settings

Remote patient monitoring is gaining momentum as European health systems shift care delivery from institutions to homes, which creates fresh opportunities for the expansion of the Europe healthcare IT market. This growth is driven by cost efficiency and patient preference. According to research, a share of EU member states expanded reimbursement for remote monitoring services, covering chronic conditions such as heart failure, COPD, and post-surgical recovery. As per research, Italy’s national telehealth program for elderly patients has gained significant adoption, resulting in reduced hospital readmissions and improved care continuity. Connected biosensors transmit real-time physiological data to integrated platforms, enabling timely interventions. According to sources, Spain’s regional health services have also achieved positive outcomes through remote monitoring programs that lower emergency visits for chronic disease patients. These models align with the EU’s integrated care agenda. The European Union continues to support the expansion of home-based digital health solutions through dedicated funding initiatives like the Digital Europe Programme, as per research. Based on a study showing notable household broadband penetration across the EU, the technical foundation for large-scale remote monitoring is now well-established.

MARKET CHALLENGES

Workforce Resistance to Digital Workflow Transformation

Resistance from healthcare professionals remains a barrier to the Europe healthcare IT market growth. As per research, a significant portion of nurses feel that electronic health records increase their administrative workload, which can affect job satisfaction.

According to sources, many physicians in France show reluctance or delay in adopting new digital prescribing systems, impacting digital health progress. This resistance often stems from inadequate frontline involvement during system design and insufficient change management. Research indicates that newly implemented health IT modules in Germany often require extensive customization, which emphasizes challenges with system integration. Generational divides further complicate adoption. According to sources, older healthcare practitioners tend to express greater dissatisfaction with digital tools compared to their younger colleagues, reflecting generational differences in technology adoption. The effectiveness of any advanced system depends on a human-centered design and continuous user engagement, without which it will remain underutilized.

Inconsistent Reimbursement Policies Across Member States

The lack of harmonized reimbursement frameworks for digital health services continues to impede the expansion of the Europe healthcare IT market. As per the European Health Management Association, only a few EU member states had established clear billing codes for telehealth and remote monitoring by the end of 2024. In some countries, digital consultations remain largely out of pocket, limiting both patient access and provider incentives. Even in mature markets, reimbursement remains selective. According to research, Germany’s policy framework for digital healthcare has encouraged the inclusion of digital therapeutics in national coverage, though research suggests that the overall adoption and reimbursement approvals remain limited. This regulatory fragmentation discourages cross-border innovation and complicates market entry for health IT vendors. As per research, a recent analysis by industry groups indicates that digital health startups in Europe often face lengthy and complex processes while securing reimbursement approvals across different countries, according to research. Failure to implement coordinated payment reform that values modern care models will prevent Europe's health IT market from achieving its full potential.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type and Country. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Cerner Corporation, Oracle Corporation, Mckesson Corporation, Philips Healthcare, Novarad Corporation, GE Healthcare, Carestream Health, eClinicalworks, EPIC Systems Corporation, Siemens Healthcare (Siemens AG), Athenahealth Inc. and Allscripts Healthcare Solutions, Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The electronic health records segment dominated the Europe healthcare IT market by accounting for 28.4% share in 2024. The dominance of the electronic health records segment is primarily driven by binding national mandates that require the digitization of patient data. According to research, most European countries have implemented policies mandating hospitals and primary care providers to adopt certified electronic health record systems, as per by research. As per the study, Germany’s healthcare policies continue to push hospitals toward achieving higher levels of digital interoperability, with provisions linking compliance to reimbursement outcomes, according to research. According to studies, France has steadily expanded its national digital health platform, with strong participation from citizens and healthcare providers, as supported by research. These policy-driven rollouts create structural demand that far exceeds voluntary adoption. The United Kingdom’s NHS continues to enforce its Digital Aspirations Framework, which mandates real-time EHR access across all trusts. This regulatory compulsion, combined with EU level alignment under the European Health Data Space, ensures sustained investment in EHR infrastructure, which cements its position as the market’s largest segment. Electronic Health Records serve as the foundational layer for managing Europe’s growing burden of chronic conditions. According to the World Health Organization, a portion of adults in the European Region live with at least one chronic disease, necessitating longitudinal data capture and care coordination. In Sweden, the national EHR system integrates with regional disease registries covering a portion of diabetic and cardiovascular patients, which enables predictive analytics, as per sources. These use cases demonstrate how EHRs transcend administrative digitization to become clinical decision engines, directly enhancing outcomes while aligning with EU priorities for value-based care.

The telemedicine segment is predicted to witness the highest CAGR of 18.7% from 2026 to 2034. The growth of the telemedicine segment is fuelled by the institutionalization of temporary pandemic-era policies into permanent reimbursement structures. According to research, many EU countries have been increasingly adopting sustainable payment models for virtual consultations, reflecting a growing trend toward integrating telehealth into routine care, as indicated by research. As per research, the Netherlands has formalized reimbursement structures for video-based primary care, which has contributed to a significant rise in teleconsultation usage, according to research. According to research, Spain has expanded telemedicine reimbursement across multiple care areas at the regional level, leading to widespread adoption of virtual healthcare services in public clinics, as observed in research. This shift from emergency response to routine care modality has unlocked consistent provider adoption and patient engagement, which transforms telemedicine from a contingency tool into a core service line. Telemedicine’s growth is further amplified by convergence with remote patient monitoring and artificial intelligence. According to research, Denmark’s national digital health strategy is increasingly integrating teleconsultations with wearable health data, which enhances real-time clinician support and improves patient outcomes, as reflected in research. As per research, Switzerland is leveraging AI-powered tools in healthcare to efficiently direct patient inquiries to virtual care services, which is helping to reduce wait times and improve access, according to research. These integrations enhance clinical utility beyond simple video calls, positioning telemedicine as a gateway to comprehensive digital care ecosystems. Supported by EU funding under the Digital Europe Programme and rising broadband access, telemedicine is poised for sustained high-velocity expansion.

COUNTRY LEVEL ANALYSIS

Germany Healthcare IT Market Analysis

Germany outperformed other regions in the Europe Healthcare IT Market and captured a 22.3% share in 2024. The domination of Germany is because to its advanced digital infrastructure, robust public investment, and stringent regulatory enforcement. The country’s dominance is anchored in the Hospital Future Act, which allocated notable funds to modernize IT systems in hospitals. As per studies, a share of acute care facilities had implemented certified EHR systems, with a portion achieving interoperability with regional health information exchanges. Besides, Germany hosts Europe’s largest health data research ecosystem, with the Medical Informatics Initiative connecting university hospitals and processing over millions of anonymized patient records annually. The nation’s dual focus on clinical digitization and data-driven innovation, strengthened by mandatory cybersecurity upgrades, ensures continued dominance in both public and private health IT procurement.

United Kingdom Healthcare IT Market Analysis

The United Kingdom was the second largest region in the Europe healthcare IT market by occupying 17.8% share in 2024. The growth of the United Kingdom is attributed to centralized digital transformation under the NHS Long Term Plan. According to research, the NHS has made significant progress in implementing interoperable electronic health records across its acute care trusts, enhancing patient data accessibility as supported by research. As per research, the national health IT infrastructure in the UK is handling a very high volume of secure health transactions, demonstrating the scale and integration of digital health services according to research. The UK also leads in AI adoption, with a portion of hospitals piloting clinical decision support tools, as per sources. Post-Brexit regulatory autonomy has enabled faster approval of digital therapeutics, with products receiving National Health Service reimbursement. Despite workforce challenges, the UK’s integrated architecture and national data strategy sustain its position as a high-intensity adopter of health IT.

France Healthcare IT Market Analysis

France remains a key region in the Europe healthcare IT market, with its citizen-centric Mon Espace Santé digital health platform. According to research, the NHS has achieved widespread deployment of interoperable electronic health records across its acute care trusts, improving patient data access and integration, as indicated by research. It integrates EHRs, ePrescriptions, teleconsultation records, and preventive care plans into a single portal accessible by patients and authorized providers. France also leads in cross-border data exchange. As per research, France’s national digital health platform has seen significant user enrollment since its launch, demonstrating strong adoption of digital health services, according to research. Strong public investment and strict interoperability deadlines for private clinics further accelerate adoption, which strengthens France’s role as a policy-driven digital health leader.

Italy Healthcare IT Market Analysis

Italy is moving ahead gradually in the Europe healthcare IT market due to regional decentralization and rapid catch-up in digital maturity. It has successfully implemented a nationwide electronic health record system that connects a large network of general practitioners and hospitals, enhancing healthcare data integration. As per research, there is a notable increase in the volume of secure health data exchanges facilitated by Italy’s digital health system, reflecting growing digital health activity. Southern regions such as Sicily and Campania saw the fastest adoption, supported by a notable amount in EU Recovery Fund allocations dedicated to digital health infrastructure. Italy also leads in telemedicine utilization for elderly care, with a portion of long-term care facilities offering remote monitoring, as per sources. This blend of national coordination and EU-funded regional modernization has elevated Italy into the top tier of European health IT markets.

Spain Healthcare IT Market Analysis

Spain is anticipated to grow in the Europe healthcare IT market during the forecast period, owing to its agile integration of telehealth and primary care digitization. According to research, Spain's national digital health platform connects a vast network of primary care centers and hospitals, enhancing healthcare accessibility for millions, supported by research. As per research, there is strong adoption of electronic prescriptions and digital referral pathways in Spain, reflecting growing digital integration in healthcare services, according to research. According to research, virtual consultations for mental health conditions like depression and anxiety have significantly increased, indicating rising acceptance of telehealth in Spain, as observed in research. Furthermore, Catalonia and Andalusia operate advanced health data lakes that support real-time public health surveillance and clinical research. A combination of robust political support and advanced digital skills among citizens ensures Spain's steady progress as a dynamic and responsive health IT market.

COMPETITIVE LANDSCAPE

The Europe Healthcare IT Market features intense competition among multinational vendors and agile regional specialists. Global leaders such as Cerner, Epic, and Philips compete on interoperability, regulatory compliance, and clinical depth, while European firms like Dedalus and CompuGroup Medical emphasize localized workflows and legacy system integration. The market is characterized by high entry barriers due to stringent data governance requirements and complex procurement processes in public health systems. Differentiation hinges on the ability to deliver secure, scalable, and user-centric platforms that align with national digital health roadmaps. Continuous innovation in AI-driven analytics, telehealth, and cybersecurity further intensifies rivalry as vendors strive to capture strategic partnerships with governments and integrated care networks across diverse healthcare landscapes.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe healthcare IT market include

- Cerner Corporation

- Oracle Corporation

- McKesson Corporation

- Koninklijke Philips NV

- Novarad Corporation

- GE Healthcare

- Carestream Health

- eClinicalWorks

- EPIC Systems Corporation

- Siemens Healthcare (Siemens AG)

- Athenahealth Inc.

- Allscripts Healthcare Solutions, Inc.

TOP 3 PLAYERS IN THE EUROPE HEALTHCARE IT MARKET

- Cerner Corporation maintains a significant footprint in the Europe Healthcare IT Market through its integrated electronic health record platforms and health data analytics solutions. The company supports national digital transformation programs in the United Kingdom and Ireland by delivering interoperable clinical systems aligned with NHS Digital standards. This initiative strengthens its commitment to scalable and compliant health IT infrastructure across the region while enhancing its global portfolio of public sector health solutions.

- Epic Systems Corporation has deepened its presence in Europe by partnering with leading academic medical centers in the Netherlands, Sweden, and Denmark. The company provides highly customizable electronic health record systems that comply with the European Health Data Space framework. This technical alignment with EU interoperability mandates strengthens its value proposition for large integrated delivery networks and positions Epic as a key enabler of cross-border care continuity in high-maturity health systems.

- Koninklijke Philips NV leverages its dual expertise in medical devices and health informatics to offer end-to-end digital care pathways across Europe. The company’s IntelliSpace Enterprise Imaging and HealthSuite platforms support radiology, cardiology, and telehealth workflows in many European countries. This clinical integration strategy underscores Philips' commitment to outcome-driven digital health solutions and supports its role as a convergent technology leader in the global healthcare IT ecosystem.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Healthcare IT Market prioritize strategic alignment with evolving EU regulatory frameworks such as the European Health Data Space and Cyber Resilience Act. They invest heavily in cloud native and interoperable architectures to meet national digitization mandates. Companies actively pursue partnerships with public health systems to embed their platforms into the national infrastructure. Innovation in artificial intelligence and remote monitoring is accelerated through joint ventures with academic and research institutions. Furthermore, firms localize their solutions to address language clinical workflow and reimbursement variations across member states, ensuring sustainable adoption and long-term market relevance.

MARKET SEGMENTATION

This Europe healthcare IT market research report is segmented and sub-segmented into the following categories.

By Type

- Electronic Health Records

- Computerized Provider Order Entry Systems

- Electronic Prescribing Systems

- PACS

- Lab Information Systems

- Clinical Information Systems

- Telemedicine

- Other Healthcare IT Services

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Healthcare IT Market?

Growth is driven by digital health transformation, telemedicine adoption, EHR expansions, big data use, and increasing government and private investments in healthcare technology

2. What are the main segments in the Europe Healthcare IT Market?

Key segments include electronic health records, telemedicine platforms, healthcare analytics, cloud computing, and mobile health apps that drive demand

3. How does telemedicine influence the Europe Healthcare IT Market?

Telemedicine enhances healthcare access and efficiency, especially in rural areas, reducing costs and enabling remote patient monitoring and consultations

4. What role do electronic health records (EHRs) play in the market?

EHRs improve patient care by streamlining clinical workflows, reducing errors, and enabling data sharing between healthcare stakeholders

5. Which countries lead the Europe Healthcare IT Market?

Germany, the UK, France, and Italy lead due to advanced digital infrastructure and supportive government policies encouraging healthcare IT adoption

6. How does cloud computing impact the Europe Healthcare IT Market?

Cloud services provide scalability, cost savings, remote access, and support for digital health innovations in patient data management and care delivery

7. What are the challenges in Europe Healthcare IT Market growth?

Challenges include interoperability gaps, cybersecurity risks, strict data privacy laws, and shortages in skilled IT healthcare professionals

8. How is artificial intelligence influencing the market?

AI enables predictive analytics, clinical decision support, personalized treatment plans, and automated workflows in hospitals and clinics across Europe

9. What is the role of healthcare data analytics?

Healthcare analytics supports patient outcome improvement, resource optimization, and population health management with real-time insights

10. Who are major players in the Europe Healthcare IT Market?

Leading providers include Veradigm, Epic Systems, Siemens Healthineers, Oracle, and Philips Healthcare offering diverse IT healthcare solutions

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com