Europe Hospital Information System Market Size, Share, Trends & Growth Forecast Report By Type, Component, Deployment and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) – Industry Analysis From 2026 to 2034.

Europe Hospital Information System Market Report Summary

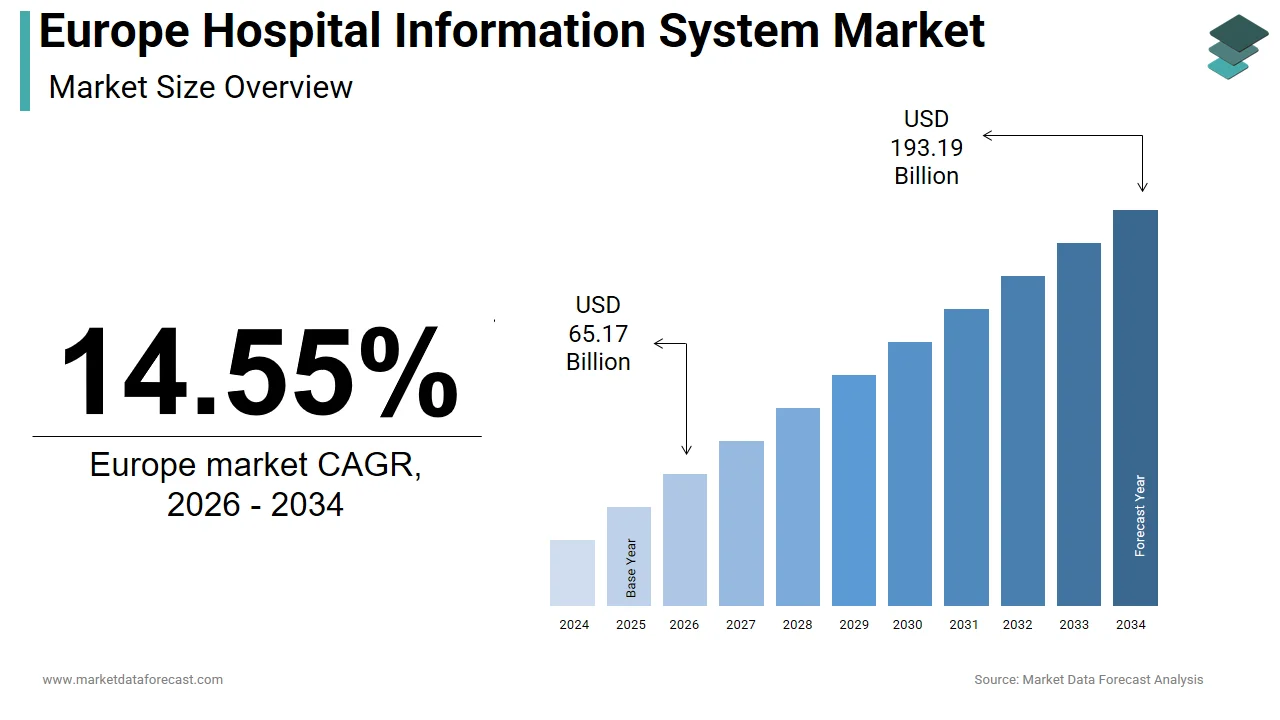

The Europe hospital information system (HIS) market was valued at USD 56.89 billion in 2025, is anticipated to reach USD 65.17 billion in 2026, and is projected to reach USD 193.19 billion by 2034, growing at a strong CAGR of 14.55% from 2026 to 2034. Market growth is driven by accelerating digital transformation in healthcare, increasing adoption of electronic health records (EHRs), and rising demand for integrated patient data management systems. Hospitals across Europe are modernizing IT infrastructure to improve operational efficiency, enhance patient outcomes, and comply with national digital health regulations. Integration of cloud computing, interoperability frameworks, and AI-powered clinical decision support tools is further fueling market expansion.

Key Market Trends

- Rising adoption of electronic health records (EHRs) across public and private hospitals.

- Increasing focus on interoperability and cross-border health data exchange.

- Growing integration of AI-driven clinical decision support systems.

- Expansion of digital patient engagement and telehealth platforms.

- Strengthening regulatory push for data security and healthcare digitization.

Segmental Insights

- Based on type, the Electronic Health Record (EHR) segment dominated the market in 2025 by holding 38.5% share, driven by regulatory mandates and increasing need for centralized patient data management.

- Based on deployment, the on-premises segment led the market by capturing 45.6% share in 2025, supported by concerns over data sovereignty, security compliance, and legacy infrastructure compatibility.

- Based on component, the software segment accounted for 52.7% share in 2025, driven by continuous upgrades, system integrations, and customization requirements across hospital networks.

Regional Insights

The Europe hospital information system market is witnessing rapid growth across major economies, supported by national digital health strategies and expanding hospital IT investments.

- Germany led the regional market in 2025 with 23.1% share, driven by federal digital healthcare initiatives and structured hospital modernization programs.

- The United Kingdom followed with 17.2% share in 2025, supported by NHS digital transformation programs and interoperability initiatives.

- France maintains a significant position, supported by its national “Ma Santé 2022” strategy and the rollout of the Dossier Médical Partagé (DMP), a shared electronic health record accessible to citizens.

Competitive Landscape

The Europe hospital information system market is characterized by strong competition among global healthcare IT providers and regional software vendors. Market players are focusing on interoperability, cybersecurity, AI-enabled analytics, and cloud integration to strengthen their competitive positioning. Strategic partnerships with public healthcare systems and cross-border digital health collaborations are shaping competitive dynamics across the region.

Prominent companies operating in the Europe hospital information system market include Cerner Corporation, Dedalus Group, Epic Systems Corporation, Siemens Healthineers, CompuGroup Medical, MEDITECH, and McKesson Corporation.

Europe Hospital Information System Market Size

The size of the Europe hospital information system market was valued at USD 56.89 billion in 2025. This market is expected to grow at a CAGR of 14.55% from 2026 to 2034 and be worth USD 193.19 billion by 2034 from USD 65.17 billion in 2026.

A Hospital Information System (HIS) refers to an integrated digital infrastructure that manages clinical, administrative, and financial operations across healthcare facilities, encompassing electronic health records (EHR), laboratory information systems, pharmacy management, and patient scheduling modules. These systems are critical enablers of the EU’s digital health transformation, operating under stringent data protection frameworks such as the General Data Protection Regulation (GDPR) and the emerging European Health Data Space (EHDS) initiative. Unlike fragmented legacy setups, modern HIS platforms emphasize interoperability, allowing seamless data exchange between primary care, hospitals, and public health agencies. According to the Digital Decade 2025: eHealth Indicator Study, the composite eHealth score for the EU-27 reached 83% in 2024. This reflects a steady increase in healthcare providers connecting to sharing networks rather than just raw hospital adoption percentages. National strategies further accelerate adoption. Germany’s Hospital Future Act allocated 4.3 billion euros to digitize hospital infrastructure by 2025, while France’s “Ma Santé 2022” plan mandates nationwide EHR integration. France continues its "Ma Santé 2022" goals through Mon espace santé, which provides every citizen with a secure digital health space to foster nationwide interoperability. Strong public alignment persists, with 88% of EU citizens supporting electronic access to their health data, a core driver for the European Health Data Space (EHDS) framework. This convergence of policy, infrastructure investment, and societal readiness defines the structural evolution of the Europe Hospital Information System Market.

MARKET DRIVERS

Mandated Interoperability and Cross-Border Health Data Exchange Under EU Policy

The European Union’s strategic push for a unified digital health ecosystem drives the growth of the Europe hospital information system market. The European Union has formally adopted the EHDS regulation to create a unified, secure, and standardized framework for sharing electronic health information across borders. This mandate requires EU Member States to gradually implement interoperable health information systems to facilitate the exchange of patient data, with compliance deadlines phased over the coming years rather than a single deadline. This mandate compels hospitals to upgrade legacy systems to comply with technical specifications like the FHIR (Fast Healthcare Interoperability Resources) standard. According to research, the vast majority of EU countries have launched national services allowing citizens to access their health records, with several nations achieving comprehensive coverage. Within this, Denmark and Estonia are recognized for establishing near-universal adoption of digital health records, setting the standard for nationwide patient access. Additionally, the EU’s Cross-Border Healthcare Directive enables patients to access treatment in other member states, necessitating real-time data portability. Hospitals in border regions, such as those in the Greater Region spanning Germany, France, and Belgium, are prioritizing HIS integration to facilitate seamless care coordination. This top-down regulatory impetus transforms HIS from an operational tool into a compliance necessity, driving urgent investment across public and private healthcare institutions.

Aging Population and Escalating Demand for Integrated Chronic Disease Management

The region’s rapidly aging demographic is intensifying pressure on healthcare systems to manage complex, long-term conditions efficiently, which creates a compelling need for robust HIS, and thereby propels the expansion of the Europe hospital information system market. According to Eurostat, 21.6% of the EU population was aged 65 or older in 2024, a figure projected to reach approximately 30.6% by 2050. Older adults typically suffer from multiple chronic diseases, such as diabetes, cardiovascular disorders, and COPD, requiring coordinated care across specialists, pharmacies, and home health services. HIS platforms enable holistic patient views by integrating data from wearables, primary care visits, and hospital admissions, facilitating proactive interventions. In Germany, where approximately 40% of adults have two or more chronic conditions according to the Robert Koch Institute, the use of digital health interventions and structured follow-up care has shown potential to reduce 30-day readmission rates, which currently stand at about 18.4% for heart failure patients. Similarly, in Sweden's Västra Götaland region, the implementation of electronic medication reporting and automated alerts has been shown to reduce medication errors by approximately 50% in clinical intervention groups. This clinical and economic imperative, to deliver coordinated, preventive care amid demographic strain, is accelerating HIS deployment as a cornerstone of sustainable health system design.

MARKET RESTRAINTS

Fragmented National Regulatory Landscapes and Certification Delays

Significant disparities in national certification processes for health IT systems create implementation barriers across the region, despite EU-level harmonization efforts, which restrict the growth of the Europe hospital information system market. Each member state maintains its own conformity assessment bodies and technical requirements for EHR and HIS certification, leading to prolonged approval timelines and increased compliance costs for vendors. In France, obtaining health data hosting certification is a rigorous and lengthy process, while Germany’s Gematik agency mandates independent, specialized certification for each digital component within its infrastructure framework. Across Europe, a significant majority of hospital IT leaders identify the lack of unified regulatory standards as a major impediment to procuring and implementing digital health technologies. Furthermore, the lack of mutual recognition between national certifications forces multinational vendors to undergo redundant testing, delaying market entry. This patchwork regulatory environment stifles innovation, discourages SME participation, and impedes the very interoperability the EU seeks to achieve, ultimately slowing the pace of digital transformation in critical care settings.

Persistent Workforce Shortages and Digital Literacy Gaps Among Clinical Staff

The successful deployment of HISs hinges not only on technology but on human capacity, and the region faces a critical deficit in both IT-savvy clinicians and trained health informaticians, which hampers the expansion of the Europe hospital information system market. The World Health Organization projects a severe, escalating shortage of health personnel across Europe by 2030, exacerbating existing high-pressure, time-constrained work environments for nurses and physicians. Introducing complex HIS often increases documentation burden during initial rollout phases, exacerbating burnout. Data suggests that European nurses, particularly in specific regions, frequently encounter inadequate training on new digital technologies, resulting in the adoption of workarounds and a risk to data accuracy. Moreover, medical curricula in many countries still lack robust health informatics components. Despite growing calls from medical authorities to integrate digital skills into medical practice, a minority of European nations currently have fully mandatory, standardized digital competency requirements for initial physician licensure. Advanced HIS systems face underutilization or rejection if not supported by proper change management, user-focused design, and continuous education, ultimately jeopardizing ROI and patient safety.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Predictive Analytics and Operational Efficiency

HISs are evolving into intelligent platforms capable of leveraging artificial intelligence to enhance clinical decision-making and resource optimization, which creates new opportunities for the Europe hospital information system market. AI algorithms embedded within HIS can analyze real-time patient data to predict sepsis onset, forecast ICU bed demand, or optimize surgical scheduling, addressing critical inefficiencies in overstretched systems. In the Netherlands, academic medical centers are increasingly implementing AI-driven early warning systems within their Hospital Information Systems, leading to improved, timely detection of sepsis and a subsequent decrease in mortality rates among patients. Similarly, Spain’s Hospital Clínic de Barcelona uses predictive analytics to anticipate emergency department surges, improving staff allocation and wait times. The European Union's Horizon Europe program is heavily investing in digital transformation, providing substantial funding for AI projects aimed at advancing healthcare, improving medical diagnostics, and personalizing treatment strategies between 2021 and 2027. Privacy-preserving federated learning allows hospitals to collaborate on AI development without moving sensitive patient data, positioning AI-enhanced HIS as a revolutionary, high-value tool for proactive, personalized, and compliant European healthcare.

Expansion of Cloud-Based HIS Solutions for Small and Medium-Sized Hospitals

Cloud computing offers a scalable, cost-effective pathway for smaller hospitals, particularly in rural areas and Eastern Europe, to access enterprise-grade HISs without massive upfront capital expenditure, thereby providing fresh prospects for the European hospital information system market. Traditional on-premise HIS deployments can cost millions and require dedicated IT teams, placing them out of reach for many community hospitals. Cloud-based models, offered via subscription, reduce the total cost of ownership while ensuring automatic updates and disaster recovery. According to a study, small European hospitals are increasingly adopting cloud-based health information systems to modernize technology, with major regional vendors supporting this shift toward digital, flexible infrastructures. The EU’s Cybersecurity Act and ENISA certification now provide trusted frameworks for secure health data hosting, alleviating privacy concerns. In countries like Poland and Romania, where public hospital budgets are constrained, cloud HIS enables rapid digitization aligned with EU interoperability standards. This democratization of advanced digital infrastructure ensures equitable access to modern health IT, bridging the urban-rural digital divide and strengthening regional healthcare resilience.

MARKET CHALLENGES

Cybersecurity Vulnerabilities and Rising Threat of Ransomware Attacks

HISs are becoming high-value targets due to their reliance on interconnected and cloud-based technology, which places patient safety and data privacy at serious risk. This poses a serious challenge to the Europe hospital information system market. The European healthcare sector is experiencing a surge in ransomware incidents, consistently ranking as a prime target for cybercriminals seeking to disrupt services and steal sensitive patient data. In 2023, major hospitals in Ireland, Finland, and the Czech Republic suffered debilitating breaches that forced the cancellation of surgeries and the diversion of ambulances. Legacy HIS modules, often running on outdated operating systems, contain unpatched vulnerabilities that attackers exploit through phishing or remote desktop protocols. The imposition of stringent cybersecurity standards via the NIS2 Directive presents significant compliance challenges for many hospitals, primarily driven by budgetary constraints and a lack of specialized technical staff. The tension between open data sharing for care coordination and robust security creates a persistent dilemma, where a single breach can erode public trust and trigger regulatory penalties, making cybersecurity not just a technical issue but a foundational challenge to digital health sustainability.

Data Silos and Lack of True Semantic Interoperability Across Systems

Meaningful data exchange remains hampered by inconsistent coding standards, proprietary data formats, and semantic mismatches between HISs, despite advances in technical connectivity, which in turn hinders the expansion of the Europe hospital information system market. Two hospitals may both use FHIR APIs, yet one records “myocardial infarction” using ICD-10 codes while another uses SNOMED CT, rendering automated analysis impossible without manual mapping. Despite widespread adoption of digital record systems, most European healthcare facilities still struggle to share information in a way that allows different systems to automatically understand and process the data's meaning without manual corrections. True semantic interoperability across the EU remains a significant challenge due to a lack of uniform national strategies and standardized clinical adherence. This fragmentation impedes large-scale research, real-world evidence generation, and pan-European disease surveillance. Even within single institutions, radiology, pathology, and EHR systems often operate as isolated islands, forcing clinicians to toggle between interfaces. While the EHDS promotes common data models, adoption is voluntary and uneven. The promise of a unified European health data ecosystem is destined to fail, undermining HIS investment value, unless semantic standards are universally enforced in procurement.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Deployment, Component, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Cerner Corporation, Dedalus Group, Epic Systems Corporation, Siemens Healthineers, CompuGroup Medical, MEDITECH, and McKesson Corporation. |

SEGMENTAL ANALYSIS

By Type Insights

The Electronic Health Record (EHR) segment dominated the Europe Hospital Information System Market by accounting for a 38.5% share in 2025. The dominance of the EHR segment is driven by its role as the foundational digital backbone of modern healthcare delivery, mandated by national digitization strategies across the EU. EHR systems consolidate patient data from multiple care settings, including primary care, hospitals, and pharmacies, enabling longitudinal health management and regulatory compliance. According to the European Commission's 2024 studies, a significant majority of acute care hospitals across the EU have accelerated the adoption of certified electronic health record systems, driven by increased digital infrastructure support. Concurrently, Germany is investing heavily in hospital digital tools and infrastructure, while France is expanding its national digital health strategy to provide widespread access to personal health records. The European Health Data Space regulation further cements EHRs as essential infrastructure by requiring standardized, interoperable records for cross-border care. This confluence of policy mandates, clinical necessity, and funding ensures EHRs remain the cornerstone of hospital digital transformation across Europe.

The Population Health Management (PHM) segment is predicted to witness the highest CAGR of 14.2% from 2026 to 2034 due to the EU’s strategic shift from reactive treatment to proactive, value-based care models that emphasize prevention and cost efficiency. PHM platforms aggregate and analyze data from EHRs, wearables, and social determinants to identify at-risk cohorts, predict disease outbreaks, and optimize resource allocation. The Swedish Västra Götaland region is leveraging population health management (PHM) analytics to better monitor heart failure patient care and optimize resources, although specific, uniform readmission reductions in 2024 are still under evaluation. Similarly, the UK National Health Service is implementing population health management tools to monitor and manage diabetes across a large population, aiming to improve glycemic control rates and enhance long-term health outcomes. Horizon Europe is investing substantial funding into real-world evidence and predictive analytics projects to drive innovation in healthcare and enhance the use of digital technology in clinical settings. Population health management (PHM) is positioned as the vanguard of future healthcare strategies, offering a scalable, data-driven, and equitable solution to address the strain placed on health budgets by aging populations and chronic diseases.

By Deployment Insights

The on-premises deployment segment led the Europe Hospital Information System Market by capturing a 45.6% share in 2025. The leading position of the on-premises deployment segment is attributed to historical investment patterns, stringent data sovereignty requirements, and institutional risk aversion, particularly in large university hospitals and public health systems. Many legacy HIS were built decades ago with on-premises architecture, and migration costs, coupled with concerns over cloud security, have slowed the transition. German cybersecurity authorities continue to mandate that highly sensitive medical information be processed within specific geographic and high-security boundaries to protect patient privacy. According to the German Hospital Institute, a majority of medical facilities still maintain their digital records on physical servers located within their own buildings rather than utilizing external cloud storage. Similarly, France’s ASIP Santé initially prioritized on-premises solutions to maintain control over the national health data infrastructure. Despite rising cloud adoption and new EU regulations, on-premises systems remain strong in public healthcare due to existing infrastructure and slow procurement cycles.

The cloud-based deployment segment is estimated to register the fastest CAGR of 16.8% during the forecast period, owing to the need for scalability, cost efficiency, and rapid innovation, especially among small and medium-sized hospitals lacking dedicated IT resources. Cloud HIS eliminates upfront capital expenditure, offering subscription-based access to enterprise-grade functionality with automatic updates and disaster recovery. European hospitals, including smaller facilities, are increasingly moving toward cloud-based solutions to enhance digital infrastructure, with major European health IT suppliers like Dedalus and CompuGroup Medical facilitating this transition. The EU’s Cybersecurity Act and ENISA certification now provide trusted frameworks for secure health data hosting, alleviating privacy concerns. In Eastern Europe, where public hospital budgets are constrained, cloud solutions enable rapid compliance with EU interoperability standards without massive infrastructure overhaul. This democratization of advanced digital capabilities positions cloud deployment as the primary engine of inclusive, future-ready healthcare digitization across the continent.

By Component Insights

The software component segment held the majority share of 52.7% of the Europe Hospital Information System Market in 2025. The supremacy of the software component segment is credited to the core value of HIS as intelligent platforms that orchestrate clinical workflows, data integration, and decision support, not merely hardware infrastructure. Modern HIS software includes modules for EHR, laboratory information, pharmacy management, and analytics, all requiring continuous updates to comply with evolving regulations like GDPR and the European Health Data Space. The majority of long-term expenses for Hospital Information Systems (HIS) stem from ongoing software licensing and maintenance rather than initial acquisition, according to various sources. National digital health initiatives, specifically Germany’s Hospital Future Act, prioritize funding for the acquisition, customization, and implementation of digital tools to enhance hospital infrastructure. Additionally, the shift toward modular, API-driven architectures increases demand for specialized software components that can interoperate across vendor ecosystems. In a healthcare landscape increasingly defined by data, intelligent and adaptable software solutions offer greater strategic value than physical assets, driving their dominance in the sector.

The services segment is anticipated to witness the fastest CAGR of 13.5% over the forecast period. This rapid growth is propelled by the increasing complexity of HIS implementation, optimization, and cybersecurity management in an era of interoperability and AI integration. Hospitals require expert consulting for system selection, data migration, staff training, and regulatory compliance, tasks that internal teams often lack the capacity to handle. European hospitals are increasingly relying on third-party specialists to manage and deploy their health information systems to address operational complexity and skill gaps. Cybersecurity services are particularly critical. Driven by a significant rise in ransomware incidents targeting the European healthcare sector, hospitals are increasingly adopting managed detection and response services to strengthen their cybersecurity defenses. Additionally, as AI-powered analytics enter clinical workflows, hospitals seek ongoing support for model validation and bias monitoring. This shift from product-centric to service-centric engagement reflects the maturation of the HIS market, where long-term success depends not on installation but on continuous adaptation and support.

COUNTRY LEVEL ANALYSIS

Germany Hospital Information System Market Analysis

Germany was the top performer in the Europe Hospital Information System Market by accounting for a 23.1% share in 2025. The prominence of the German market is driven by its landmark Hospital Future Act, which committed funds to digitize hospital infrastructure by 2025. The law mandates EHR adoption, interoperability, and telemedicine capabilities, creating unprecedented demand for integrated HIS solutions. According to reports on the German Hospital Future Act, a vast majority of German hospitals have received funding to modernize their digital infrastructure, with a primary focus on strengthening cybersecurity and enhancing secure, inter-sectoral data exchange via the national Telematics Infrastructure. Germany’s strong industrial base, home to Siemens Healthineers and SAP, further accelerates innovation in AI-driven clinical decision support. Additionally, the country’s aging population intensifies the need for coordinated chronic disease management through advanced HIS. This combination of policy ambition, technological capability, and demographic pressure solidifies Germany’s position as the continent’s most dynamic and influential HIS market.

United Kingdom Hospital Information System Market Analysis

The United Kingdom was the second largest country in the Europe hospital information system market by holding a 17.2% share in 2025. The demand for HIS in the UK is supported by its centralized National Health Service (NHS) and ambitious digital transformation agenda. NHS England is driving a near-universal, mandated shift toward fully digital, interoperable electronic patient record systems for all hospital trusts, heavily supported by substantial national funding, aiming for comprehensive, standardized digital maturity within the decade. The vast majority of acute NHS trusts have now adopted electronic patient record systems, with major global technology providers, such as Epic and Oracle Health, playing a significant role in improving, though not yet entirely perfecting, data exchange across primary and secondary care. The UK also pioneers AI integration. The National Pathology Exchange uses HIS-linked algorithms to reduce diagnostic turnaround. Post-Brexit, the UK maintains alignment with EU data standards while accelerating its own initiatives like the Federated Data Platform. The UK's health IT landscape is a top-tier, high-impact market for interoperable and scalable tools, heavily supported by government investment, centralized purchasing, and a focus on data-driven, improved patient outcomes.

France Hospital Information System Market Analysis

France occupied a promising share of the Europe hospital information system market due to its national “Ma Santé 2022” strategy and the rollout of the Dossier Médical Partagé (DMP), a shared electronic health record accessible to all citizens. The French health authority (via the digital health platform "Mon Espace Santé") has rapidly expanded the adoption of digital shared medical records (DMPs), making their integration into hospital and ambulatory information systems a central, ongoing requirement for care coordination, with increasing pressure to ensure seamless data exchange by healthcare professionals. The Agence du Numérique en Santé (ANS) certifies all health IT systems, ensuring compliance with interoperability and security standards. France’s hospital landscape, comprising a large number of public and private facilities, relies heavily on domestic vendors like Cegedim and Dedalus for tailored solutions. Additionally, the country’s emphasis on preventive care fuels the adoption of population health modules to manage chronic diseases like diabetes and hypertension. This blend of top-down policy, national infrastructure, and local innovation sustains France’s role as a pivotal market for standardized, citizen-centric health information systems.

Netherlands Hospital Information System Market Analysis

The Netherlands is expected to be the most lucrative region in the Europe hospital information system market by emerging as a leader in interoperability and data-driven care. The country’s national LSP (Landelijk Schakelpunt) enables secure, consent-based exchange of medical records among a substantial share of general practitioners and all hospitals. Dutch hospitals prioritize open-platform HIS that integrates with regional health networks and wearable data streams. Erasmus University Medical Center, for instance, uses AI-enhanced HIS to predict sepsis onset with significant accuracy. The government’s “Digital Health Action Plan” allocates sustained funding for innovation, while strict GDPR enforcement builds public trust. The Netherlands acts as a premier testbed for advanced European health IT, driven by nearly universal electronic health record (EHR) adoption, sophisticated data analytics, and a collaborative environment.

Sweden Hospital Information System Market Analysis

Sweden is predicted to register a notable CAGR in the Europe Hospital Information System Market over the forecast period, owing to its mature, decentralized yet interoperable digital health ecosystem. Each of the regions manages its own HIS, but all adhere to national standards set by the Swedish eHealth Agency, ensuring cross-regional data exchange. The comprehensive regional Health Information System in Västra Götaland, which connects hospital and primary care data, is improving patient safety by lowering medication-related errors. According to a study, a significant majority of citizens utilize digital services to interact with healthcare providers, highlighting high public adoption of eHealth solutions. Sweden’s participation in EU projects like EHDS and its strong focus on preventive analytics position it as a benchmark for citizen-centric, outcome-oriented health IT. This balance of regional autonomy and national coherence makes Sweden a model for scalable, sustainable digital health infrastructure.

COMPETITIVE LANDSCAPE

Competition in the Europe Hospital Information System Market is characterized by a dynamic interplay between global technology giants, specialized European vendors, and emerging cloud-native startups. Incumbents like Siemens Healthineers leverage scale and integration with medical devices, while regional leaders such as Dedalus and CompuGroup Medical thrive on deep regulatory knowledge and localized customization. The market is highly fragmented due to divergent national standards, creating both barriers and opportunities for global players to adapt to local certification regimes, whereas agile regional firms can rapidly deploy compliant solutions. Differentiation increasingly hinges on interoperability, AI capabilities, and cybersecurity resilience rather than core functionality alone. Public funding programs like Germany’s Hospital Future Act intensify demand but also raise procurement complexity. Ultimately, success depends on balancing pan-European scalability with national specificity, all while navigating stringent data protection laws and rising expectations for real-time, intelligent healthcare delivery.

KEY MARKET PLAYERS

The leading companies operating in the Europe hospital information system market include:

- Cerner Corporation

- Dedalus Group

- Epic Systems Corporation

- Siemens Healthineers

- CompuGroup Medical

- MEDITECH

- McKesson Corporation

TOP PLAYERS IN THE MARKET

- Siemens Healthineers is a pivotal force in the Europe Hospital Information System Market through its Teamplay digital health platform and advanced hospital IT solutions. The company integrates imaging, laboratory, and clinical data into unified workflows, enabling real-time decision support across care settings. In Europe, Siemens leverages its deep ties with public healthcare systems to deploy scalable, interoperable HIS architectures compliant with GDPR and the European Health Data Space. Recently, it enhanced its AI-powered analytics suite to predict patient deterioration and optimize resource allocation in intensive care units. It also expanded cloud-based hosting options certified under ENISA standards to address data sovereignty concerns. These initiatives reinforce Siemens Healthineers’ role as a trusted partner in Europe’s transition toward intelligent, data-driven hospital operations.

- Dedalus Group stands as a leading European-born provider of integrated Hospital Information Systems, serving thousands of healthcare facilities across the continent. Headquartered in Italy, the company specializes in modular EHR, laboratory, and pharmacy management solutions tailored to national regulatory frameworks in France, Germany, Spain, and the UK. Dedalus has strengthened its position by acquiring regional players like Medasys in France and expanding its cloud-native platform, OpenHealth, which supports FHIR-based interoperability and population health analytics. It actively participates in EU-funded projects on cross-border health data exchange and has aligned its systems with the European Health Data Space specifications. Dedalus enables seamless digital transformation for diverse healthcare ecosystems by combining local compliance expertise with pan-European scalability.

- CompuGroup Medical plays a critical role in the Europe Hospital Information System Market through its comprehensive digital health platforms that connect hospitals, physicians, and patients. The company’s CGM HOSPITAL suite offers end-to-end HIS functionality, including EHR, scheduling, and billing, with strong adoption in Germany, the Netherlands, and Eastern Europe. CompuGroup has recently accelerated its cloud migration strategy, launching secure, GDPR-compliant hosting environments certified under the EU Cloud Rulebook. It also integrated AI-driven clinical documentation tools to reduce physician burnout and improve coding accuracy. CompuGroup Medical is reinforcing its commitment to establishing robust, future-ready digital infrastructure across Europe’s fragmented landscape through strategic partnerships with national eHealth agencies and continuous investments in semantic interoperability.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Hospital Information System Market are prioritizing cloud native deployments with ENISA and EU Cloud Rulebook-certified infrastructure to address data sovereignty and cybersecurity concerns. They are embedding artificial intelligence for predictive analytics and clinical decision support to enhance patient outcomes and operational efficiency. Companies are aligning their systems with FHIR standards and European Health Data Space requirements to ensure cross-border interoperability and regulatory compliance. Strategic acquisitions of regional vendors are being pursued to strengthen local market presence and integrate legacy systems into modern platforms. Additionally, firms are expanding professional services, including cybersecurity, managed detection response, and change management training to support complex hospital digitization journeys.

MARKET SEGMENTATION

This research report on the Europe hospital information system market has been segmented and sub-segmented into the following categories.

By Type

- Electronic Health Record

- Electronic Medical Record

- Real-time Healthcare

- Patient Engagement Solution

- Population Health Management

By Deployment

- Web-based

- On-premises

- Cloud-based

By Component

- Software

- Hardware

- Services

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe hospital information system market?

The Europe hospital information system market provides integrated software managing patient records, workflows, and hospital operations digitally.

Why is the Europe hospital information system market growing?

The Europe hospital information system market expands through digital health mandates and integrated care delivery requirements.

What modules comprise the Europe hospital information system market?

EHR, PACS, LIS, and pharmacy systems lead the Europe hospital information system market comprehensive functionality.

Who leads the Europe hospital information system market?

Cerner, Epic, and Philips dominate the Europe hospital information system market enterprise solutions.

What trends shape the Europe hospital information system market?

Trends feature cloud migration in the Europe hospital information system market scalability advantages.

How does EHR integration benefit the Europe hospital information system market?

EHR enables seamless data sharing in the Europe hospital information system market care coordination improvements.

What role does interoperability play in the Europe hospital information system market?

HL7 FHIR standards ensure connectivity in the Europe hospital information system market cross-facility data exchange.

Which countries lead the Europe hospital information system market?

Germany, UK, and Netherlands pioneer the Europe hospital information system market advanced digital health infrastructures.

What challenges face the Europe hospital information system market?

Legacy system migration challenges adoption in the Europe hospital information system market modernization efforts.

How does cloud deployment impact the Europe hospital information system market?

Cloud HIS reduces infrastructure costs in the Europe hospital information system market smaller facilities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com