Europe Smart Hospitals Market Size, Share, Trends & Growth Forecast Report By Component, Technology, Application, Connectivity and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Europe Smart Hospitals Market Report Summary

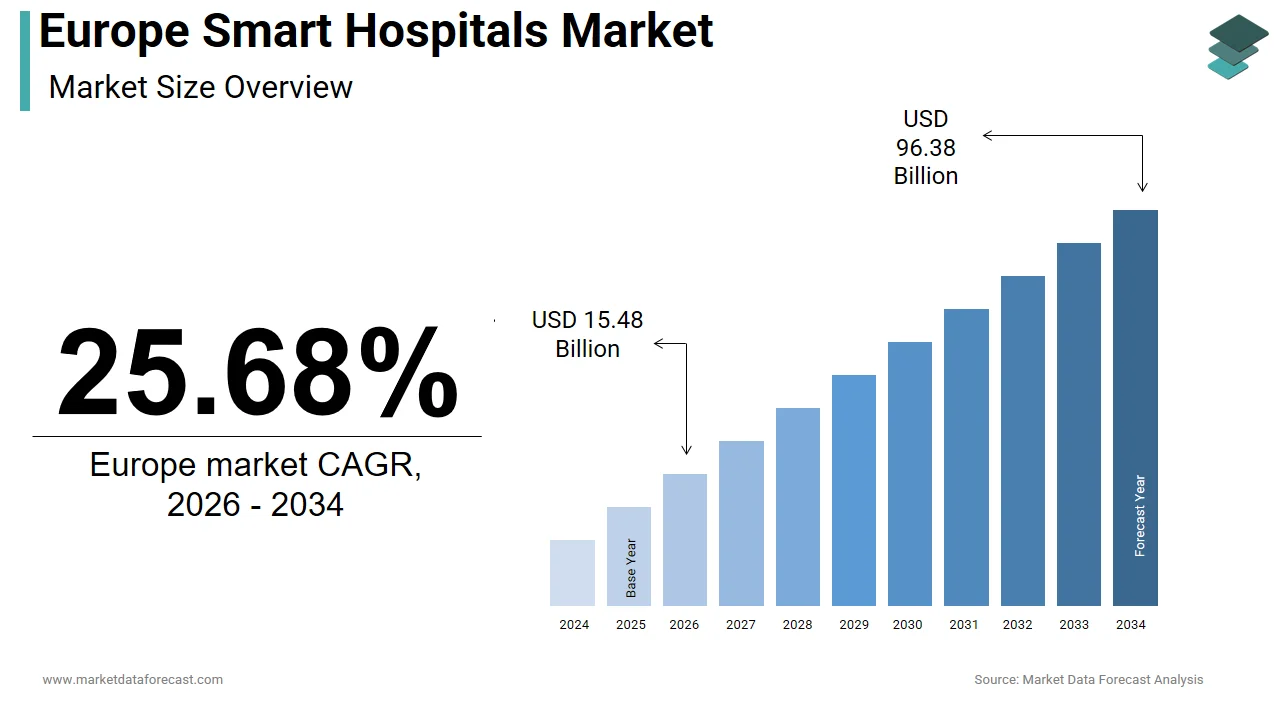

The Europe smart hospitals market was valued at USD 12.32 billion in 2025, is estimated to reach USD 15.48 billion in 2026, and is projected to grow to USD 96.38 billion by 2034, reflecting a CAGR of 25.68% (2026 to 2034). Market expansion is driven by AI-enabled clinical decision support, IoT-connected medical device deployments, rising remote-monitoring and hospital-at-home models for ageing populations, and initiatives to standardize cross-border health data exchange. Workforce shortages and pressure to reduce readmissions are accelerating investments in automation, predictive analytics, and interoperable clinical platforms across Europe.

Market Snapshot

| Metric | Value (USD) |

| 2025 | USD 12.32 billion |

| 2026 (projection) | USD 15.48 billion |

| 2034 (forecast) | USD 96.38 billion |

| CAGR (2026 to 2034) | 25.68% |

Key Market Trends

- AI-driven clinical workflows: Rapid adoption of AI for diagnostics, triage, sepsis prediction, and predictive deterioration alerts.

- Interoperability & data standardization push: Momentum behind EU-level frameworks (EHDS) and national EHR programs to enable cross-institution data flows.

- Shift to remote & decentralized care: Expansion of remote medicine management, telespecialty networks, and hospital-at-home models.

- Cloud-first infrastructure & sovereign clouds: Growing use of cloud platforms for scalable analytics while addressing data sovereignty.

- Cybersecurity & regulation focus: Strong emphasis on NIS2, GDPR compliance, and embedded security for medical device ecosystems.

- Service-led deployments: Rise in managed services, cyber-audits, and training as hospitals outsource complex digital transformation tasks.

Segmental Insights

- By Component: Software led in 2024 (~42.6% share) as unified EHRs, clinical decision support, and command-center platforms form the integration backbone.

- By Services: Services are the fastest-growing subsegment (projected CAGR ~14.8%) — implementation, managed security, and training drive recurring revenue.

- By Application: EHR & clinical workflow solutions dominated (38.2% share) as they underpin interoperability and AI pipelines; remote medicine management is one of the fastest-growing applications (CAGR ~18.3%) driven by chronic-care monitoring and teleconsultations.

- By Technology: Cloud computing was the largest technology segment (35.1% share) for scalable storage/analytics; AI is the high-growth tech vector (CAGR ~22.1%) powering diagnostics and operational optimization.

Regional Insights

- Germany: Market leader (~23.6% share) — strong public funding, Telematics Infrastructure, rigorous IT-security standards, and extensive university hospital networks.

- United Kingdom: Significant adopter (~17.8% share) — centralized NHS data assets and pioneering AI deployments in imaging and genomics.

- France: Large market with strong national EHR programs, dedicated funding, and regulated health-data sandbox environments for innovation.

- Netherlands & Sweden: Benchmarks for interoperable, patient-centric systems, telemonitoring scale-up, and national digital health platforms.

- Rest of Europe: Heterogeneous adoption—Western/Nordic markets lead on digital maturity; Southern & Eastern countries show growing interest but face funding and interoperability constraints.

Competitive Landscape

The market is fragmented and competitive, featuring global cloud/tech giants, legacy medical device firms, health-IT specialists, and local system integrators. Differentiation centers on: regulatory compliance (GDPR, NIS2), interoperability (FHIR/EHDS readiness), demonstrable clinical outcomes, cybersecurity resilience, and managed services capabilities. Public procurement and evidence of real-world impact increasingly drive vendor selection.

Key Market Players

IBM · Medtronic · Philips · Microsoft · GE Healthcare · Qualcomm · SAP · Stanley Healthcare · Cerner Corporation · McKesson · Siemens

Europe Smart Hospitals Market Size

The size of the Europe smart hospitals market was valued at USD 12.32 billion in 2025. This market is expected to grow at a CAGR of 25.68% from 2026 to 2034 and be worth USD 96.38 billion by 2034 from USD 15.48 billion in 2026.

Smart Hospitals are healthcare facilities that integrate interconnected digital infrastructure, artificial intelligence-driven diagnostics, real-time data analytics, and automated operational systems to enhance clinical outcomes, patient safety, and resource efficiency. Unlike conventional hospitals, smart hospitals leverage Internet of Things-enabled medical devices, centralized command centers, and interoperable electronic health records to enable predictive care and seamless care coordination. Most hospitals are implementing advanced information systems. An initiative is in place to standardize the sharing of health data across borders. A shortage of healthcare professionals is increasing the demand for automated and remote monitoring solutions. Besides, the aging population underscores the need for scalable care models that reduce hospital readmissions and support the management of chronic diseases.

MARKET DRIVERS

Integration of Artificial Intelligence for Clinical Decision Support

Artificial intelligence is rapidly transforming diagnostic and therapeutic workflows in European hospitals by enabling real-time data interpretation and evidence-based recommendations, which propels the growth of the Europe smart hospitals market. According to a study, the implementation of artificial intelligence algorithms in European radiology departments for tasks such as chest X-ray analysis and mammography screening is increasing, to enhance efficiency and optimize workflow. Research initiatives, such as projects funded by the German Federal Ministry of Health, are focused on developing and evaluating AI-assisted clinical decision support systems to improve early detection and treatment strategies for critical conditions like sepsis. Furthermore, Regulatory bodies in the European Union are actively developing frameworks and guidance for artificial intelligence and machine learning applications in medical devices, focusing on safety, ethics, and performance validation. The integration of AI systems in healthcare aims to support clinical staff and alleviate workload pressures amidst significant concerns regarding physician burnout and workforce strain in the medical field. Hospitals are increasingly embedding AI into electronic health records to generate personalized treatment pathways aligning with the European Commission’s vision for data-driven precision medicine.

Rising Prevalence of Chronic Diseases and Aging Population Demographics

The region’s demographic shift toward an older population is intensifying demand for smart hospital solutions capable of managing complex long-term conditions efficiently, which in turn boosts the expansion of the Europe smart hospitals market. Health statistics indicate that the vast majority of older adults in Europe and globally live with at least one chronic health condition. The prevalence of having multiple chronic conditions among adults aged 65 and over is significant across European nations. Population projections by Eurostat consistently show a significant and sustained increase in the number and proportion of very old individuals in the European population. This demographic shift is leading to a growing demand for healthcare services and placing a greater burden on existing acute care infrastructure. Europe, including in countries like Italy and Portugal, remote patient monitoring platforms are increasingly used to manage chronic conditions and support home-based care. These digital health technologies are a key component in efforts to improve care efficiency and minimize avoidable hospital admissions. These systems also support the EU’s Strategic Agenda for Healthy Aging, which prioritizes technology-enabled independent living and hospital-at-home services to maintain care continuity while optimizing bed utilization.

MARKET RESTRAINTS

High Capital Expenditure and Fragmented Healthcare Funding Mechanisms

The deployment of smart hospital infrastructure requires substantial upfront investment in connectivity hardware, cybersecurity protocols, and staff training, which poses a significant barrier to the Europe smart hospitals market. This is particularly true in publicly funded systems with constrained budgets. The initial capital investment required for comprehensive hospital digitalization is substantial and often requires significant governmental or EU-level funding support. Countries with lower overall health spending as a proportion of their economic output face challenges in allocating substantial capital specifically for non-urgent digital health infrastructure upgrades. Additionally, procurement rules under national health services often delay technology adoption due to multiyear tender cycles and a lack of interoperability standards across legacy systems. Funding uncertainty and the lack of clear reimbursement models often impede the widespread implementation of innovative smart hospital technologies across European health systems. This financial fragmentation impedes scalable innovation and widens the digital divide between Western and Eastern European healthcare institutions.

Data Privacy Regulations and Interoperability Compliance Complexities

Strict data governance frameworks such as the General Data Protection Regulation pose operational challenges for smart hospital implementations that rely on continuous data aggregation from diverse sources, and thereby restrain the expansion of the Europe smart hospitals market. Data protection authorities across the EU processed a high volume of GDPR complaints in 2023, with the healthcare sector continuing to face significant scrutiny regarding data security and unauthorized data processing, often involving third-party vendor risks. Achieving compliance requires hospitals to implement granular consent management, encryption, and audit trails, which increase system complexity and integration costs. Furthermore, the lack of uniform technical standards for health data exchange hinders interoperability even among certified systems. Interoperability challenges remain prevalent in the EU healthcare sector, with a general trend toward the development and adoption of new, harmonized EU-wide technical specifications for electronic health record exchange under the European Health Data Space (EHDS) regulation, which aims to improve data sharing beyond current varied compliance levels. These regulatory and technical hurdles slow down real-time data utilization and limit the scalability of AI-driven care models across regional networks.

MARKET OPPORTUNITIES

Expansion of 5G-Enabled Remote Surgery and Telespecialty Networks

The rollout of dedicated 5G health networks is opening new capabilities in real-time remote clinical interventions and specialist collaboration across the region, which is predicted to drive the growth of the Europe smart hospitals market. Hospitals in several European nations are incorporating ultra-low latency 5G private networks to facilitate advanced medical applications like robotic-assisted telesurgery and immersive teleconsultations. Medical professionals have utilized 5G connectivity for remote neurosurgery simulations, demonstrating precise instrument control from a distance, while initiatives support pilot corridors connecting rural and urban centers using holographic imaging and haptic feedback systems. Hospitals are also leveraging 5G to stream high-resolution intraoperative video for real-time peer review and surgical training, thereby improving procedural standardization and patient safety outcomes across the continent.

Adoption of Predictive Analytics for Hospital Resource Optimization

The increased deployment of machine learning models in the field to forecast bed occupancy, staff requirements, and equipment utilization thereby enhances operational resilience and generates fresh prospects for the expansion of the Europe smart hospitals market. Hospitals using predictive bed management systems have reduced emergency department boarding times. Dynamic discharge planning and capacity alerts contribute to more efficient patient flow. Implementation of AI-driven staffing algorithms in acute care wards has decreased nurse overtime hours. These staffing changes were achieved while consistently maintaining patient safety indicators. These systems analyze historical admission patterns, seasonal disease outbreaks, and real-time ambulance telemetry to generate actionable insights. Such capabilities are especially vital as European hospitals face persistent workforce shortages and rising patient volumes, making data-driven resource orchestration a cornerstone of sustainable smart hospital transformation.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Interconnected Medical Ecosystems

The proliferation of connected devices in these healthcare facilities has exponentially expanded the attack surface for cyber threats targeting patient data and clinical operations, which constrains the growth of the Europe smart hospitals market. The European Union Agency for Cybersecurity (ENISA) reports that healthcare institutions continue to be a prime target for a significant number of cybersecurity incidents, with ransomware remaining one of the primary threats. A prevalent challenge across the healthcare sector involves the use of medical equipment running on legacy operating systems that lack current security patches, creating significant vulnerabilities due to manufacturer support limitations. A large-scale ransomware attack severely disrupted Ireland's National Health Service in 2021, leading to widespread cancellations of appointments and critical service outages in facilities like radiology and laboratories. The EU’s NIS2 Directive mandates stricter incident reporting and resilience measures, yet many hospitals lack dedicated cybersecurity teams or real-time threat monitoring capabilities. This exposure not only endangers patient safety but also undermines trust in digital health transformation efforts across the region.

Workforce Resistance and Insufficient Digital Literacy Among Clinical Staff

The successful deployment of smart hospital systems is often hindered by inadequate digital competencies and cultural resistance among healthcare professionals, despite technological advancements, which in turn holds back the expansion of the Europe smart hospitals market. The European Foundation for the Improvement of Living and Working Conditions and related research indicate that a significant portion of healthcare professionals across Europe perceive their training to operate new digital systems as inadequate to perform effectively in evolving work environments. Studies on the healthcare sector's digitalisation, which are relevant to the European Federation of Public Service Unions, emphasize concerns among clinical staff that new digital systems may contribute to administrative burden rather than leading directly to improved patient care outcomes. In Italy, pilot implementations of AI triage tools were delayed due to skepticism about algorithmic bias and lack of transparency in decision logic. Furthermore, medical curricula across many EU countries have not yet integrated health informatics as a core competency, resulting in generational gaps in technology adoption. Failure to integrate continuous education and end-user co-design into change management means even advanced smart hospital platforms may suffer from low utilization and workflow disruptions, jeopardizing both ROI and quality of care.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Application, Technology, Connectivity, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | IBM, Medtronic, Philips, Microsoft, GE Healthcare, Qualcomm, SAP, Stanley Healthcare, Cerner Corporation, McKesson, and Siemens. |

SEGMENTAL ANALYSIS

By Component Insights

The software segment held the leading share of 42.6% of the Europe smart hospitals market in 2024. The leading position of the software segment is attributed to the central role of integrated clinical platforms in enabling data interoperability, real-time analytics, and regulatory compliance across hospital departments. Hospitals increasingly rely on unified software ecosystems such as enterprise resource planning, electronic health records, and clinical decision support systems to streamline operations and meet EU mandates like the European Health Data Space. Besides, the European Medicines Agency’s push for real-world evidence generation has accelerated the adoption of software tools that aggregate patient data from wearables, imaging devices, and laboratory systems into longitudinal health profiles supporting precision medicine initiatives across the region.

The services segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 14.8% from 2025 to 2033 due to the increasing complexity of smart hospital ecosystems, which require specialized implementation, training, cybersecurity auditing, and managed support beyond initial deployment. Hospitals across several European countries are increasingly engaging external service providers to manage digital transformation initiatives. Internal resource limitations within the health informatics and IT security sectors are a primary driver for this shift. Demand for services relating to compliance advisory and penetration testing has become more intense. Healthcare facilities across the region are under mandate to complete regular cyber resilience assessments. Additionally, the shift toward outcome-based care models has spurred demand for data analytics as a service, enabling hospitals to monitor readmission rates, treatment efficacy, and patient satisfaction in real time. Companies offering 24/7 remote monitoring of connected medical devices have also seen contracts grow year on year.

By Application Insights

The Electronic Health Records and Clinical Workflow segment led the Europe smart hospitals market by capturing a 38.2% share in 2024. The supremacy of the electronic health records and clinical workflow segment is credited to stringent regulatory requirements under the EU Cross-Border Healthcare Directive, which mandates structured digital documentation for patient referrals and reimbursements. Public hospitals in Germany are using certified Electronic Health Record (EHR) systems that enable secure data exchange among various healthcare providers. Hospitals in the Netherlands have widely adopted a national EHR system that integrates essential patient information, such as medication histories, allergy alerts, and diagnostic reports, into a unified interface for clinicians. Funding has been provided to support the modernization of EHR interoperability using established data standards, which helps improve efficiency and patient safety. These systems also serve as foundational data pipelines for AI-driven applications, reinforcing their strategic centrality in smart hospital architecture.

The Remote Medicine Management segment is expected to exhibit a noteworthy CAGR of 18.3% during the forecast period, owing to policy shifts toward decentralized care and rising demand for chronic disease monitoring outside acute settings. Across Europe, many patients managing conditions like heart failure, diabetes, or respiratory issues are participating in national remote monitoring programs. These programs have shown positive results in reducing hospital admissions in various regions. In Sweden, the national “Digital First” strategy mandates that all primary care consultations begin with a digital triage option, accelerating adoption of remote symptom assessment platforms. The use of reimbursed remote medical consultations has seen a significant increase in France in recent years. These consultations now cover a wide range of medical services, including follow-up care after surgery and mental health support sessions. Besides, the integration of home-based biosensors with hospital command centers enables real-time alerts for physiological deterioration, enhancing preventive care while aligning with the EU’s vision for integrated community-based health ecosystems.

By Technology Insights

The cloud computing segment was the largest in the Europe smart hospitals market by occupying a share of 35.1% in 2024. The dominance of the cloud computing segment is driven by the need for scalable, secure, and cost-efficient data storage that supports interoperability across disparate hospital systems and regulatory compliance with the European Health Data Space. New electronic health record (EHR) deployments are increasingly using sovereign cloud platforms that are hosted locally. This approach helps ensure that data management practices align with regional data protection regulations. The adoption of cloud technology in healthcare is associated with operational benefits. These include a potential reduction in the ongoing cost of maintaining physical, on-site server infrastructure. Cloud platforms help streamline system management. Specific advantages involve enabling more efficient software updates and enhancing capabilities for disaster recovery. This infrastructure is critical for enabling real-time analytics, AI training, and cross-institutional collaboration while maintaining strict data sovereignty.

The Artificial Intelligence segment is predicted to witness the highest CAGR of 22.1% from 2025 to 2033. The rapid expansion of the artificial intelligence segment is fuelled by regulatory validation, clinical efficacy, and urgent workforce constraints across the continent. Artificial intelligence (AI) based software applications for medical devices are actively receiving certification, with tools developed for applications such as early sepsis prediction, stroke lesion segmentation, and antimicrobial resistance forecasting. AI programs in hospitals are deploying real-time patient deterioration algorithms, and AI-powered triage systems are being integrated into emergency departments. Significant funding is being directed toward AI projects focused on rare disease diagnosis and surgical robotics, reinforcing the growing role of AI in next-generation smart hospitals.

COUNTRY-LEVEL ANALYSIS

Germany Smart Hospitals Market Analysis

Germany was the top performer in the Europe smart hospitals market and accounted for a 23.6% share in 2024. The domination of the German market is driven by robust public investment, strong data governance frameworks, and a dense network of university-affiliated medical centers. A national Telematics Infrastructure platform has been established to connect many medical practices and hospitals. This platform facilitates secure electronic prescriptions, emergency data sets, and electronic patient records. Government funding was allocated to support hospital digitization efforts. A key aspect of this initiative includes a requirement for electronic health record certification. Major hospitals have implemented artificial intelligence technologies in clinical settings. The use of technology in surgical and patient management systems has shown an impact on the duration of patient stays. Germany’s stringent IT security standards under the KRITIS regulation also compel hospitals to adopt advanced cybersecurity services, making it a benchmark for resilient smart healthcare deployment across the EU.

United Kingdom Smart Hospitals Market Analysis

The United Kingdom was the second-largest country in the European smart hospitals market and captured a share of 17.8% in 2024. The growth of the UK market is due to its centralized National Health Service data infrastructure and pioneering adoption of AI in clinical workflows. Integrated health datasets in the health service provide a foundation for AI development in medical imaging and genetics areas. A federated data platform initiative connects numerous acute healthcare facilities, enabling current data analytics for managing operational aspects like patient lists, infection trends, and resource distribution. AI algorithms are utilized in many hospitals for medical image interpretation and predicting certain patient conditions, with studies indicating efficiency improvements in diagnostic processes. Government strategies support the integration and expansion of validated AI tools across different levels of patient care, fostering an environment for ongoing innovation in digital health.

France Smart Hospitals Market Analysis

France is another key player in the Europe smart hospitals market because of aggressive national digital strategies and universal EHR implementation. There has been a significant increase in the integration of national electronic health record systems across hospitals. A large number of citizens are enrolled in these systems, and many healthcare professionals are authorized to use the records. Substantial funding has been dedicated to modernizing hospital technology, including areas such as artificial intelligence, remote monitoring, and advanced command centers. The use of artificial intelligence in healthcare settings is expanding, with specific applications in clinical decision support systems integrated with various data sources like imaging and laboratory information. Additionally, the French data protection authority CNIL has approved health data sandbox environments enabling startups to develop and test smart hospital applications under strict ethical oversight, fostering a dynamic innovation ecosystem aligned with public health priorities.

Netherlands Smart Hospitals Market Analysis

The Netherlands occupies a noteworthy position in the Europe smart hospitals market as a model for interoperable and patient-centric smart healthcare systems in the region. A national platform allows for the smooth flow of patient data between many hospitals, general practitioners, and pharmacies, with access rights managed by the patient. Most hospitals utilize integrated clinical workflow systems that feature decision support alerts for medication issues and preventative care. The health care inspectorate has mandated the real-time digital tracking of high-risk medication administration. Remote care is prevalent, with numerous patients enrolled in telemonitoring programs for long-term conditions, supported by existing reimbursement structures. This systemic integration of data automation and patient engagement makes the Netherlands a benchmark for scalable smart hospital implementation in small, high-income European nations.

Sweden Smart Hospitals Market Analysis

Sweden is predicted to grow in the Europe smart hospitals market from 2025 to 2033. It emerges as a Nordic pioneer in smart hospital innovation, characterized by advanced digital literacy, universal health data standards, and strong public tech investment. The national Inera platform provides every citizen with a digital health portal that aggregates records from all care providers, enabling seamless referrals and patient-reported outcome tracking. Hospitals are utilizing AI-enabled predictive analytics for managing emergency department needs and forecasting bed availability. One university hospital has observed improvements related to managing intensive care unit capacity. National technology testbeds are facilitating connectivity between different types of healthcare facilities using advanced technologies such as augmented reality and real-time data sharing capabilities. This forward-looking ecosystem positions Sweden as a leader in human-centered smart hospital design with a focus on equity, efficiency, and clinician usability.

COMPETITIVE LANDSCAPE

Competition in the Europe Smart Hospitals Market is characterized by a dynamic interplay between global technology giants, specialized health IT vendors, and local system integrators, all striving to deliver compliant, secure, and clinically relevant solutions. The landscape is highly fragmented due to national differences in healthcare financing, data governance, and digital maturity, yet leading players differentiate through regulatory expertise, interoperability certification, and evidence-based clinical outcomes. Large vendors such as Siemens, Philips, and IBM compete on end-to-end platform capabilities while niche firms focus on vertical applications like AI radiology or remote ICU monitoring. The European Commission’s push for health data standardization through the European Health Data Space is intensifying pressure to adopt open architectures, thereby reducing vendor lock-in. Simultaneously, cybersecurity resilience has become a decisive competitive factor as hospitals prioritize solutions that withstand ransomware and ensure continuity of care. Innovation cycles are accelerating with real-world validation and public procurement frameworks increasingly favoring vendors that demonstrate measurable improvements in patient safety, operational efficiency, and equity of access.

KEY MARKET PLAYERS

The leading companies operating in the Europe smart hospitals market include:

- IBM

- Medtronic

- Philips

- Microsoft

- GE Healthcare

- Qualcomm

- SAP

- Stanley Healthcare

- Cerner Corporation

- McKesson

- Siemens

TOP 3 PLAYERS IN THE MARKET

- Siemens Healthineers is a pivotal contributor to the Europe Smart Hospitals Market through its integrated digital health platforms and AI-driven imaging solutions. The company supports hospitals across Germany, France, and the Nordic countries with its Teamplay digital health ecosystem, which connects medical devices, data analytics, and clinical workflows into unified command centers. Globally, Siemens Healthineers enables predictive maintenance, remote diagnostics, and dose optimization across multiple hospitals. It also expanded its cloud-based data lake infrastructure in partnership with European health authorities to facilitate compliant cross-institutional research while reinforcing its position as a leader in interoperable smart hospital infrastructure.

- Philips Healthcare plays a central role in advancing smart hospital transformation in Europe through its integrated patient monitoring, clinical informatics, and telehealth solutions. The company’s IntelliSpace Enterprise Imaging and HealthSuite platforms are deployed in numerous European hospitals, enabling real-time data aggregation from operating rooms, intensive care units, and outpatient clinics. Globally, Philips contributes to connected care innovation by developing open architecture systems that support third-party AI integration and longitudinal health tracking. The company also launched a cybersecurity-hardened version of its medical device operating system in compliance with EU NIS2 requirements, further solidifying trust among European healthcare providers.

- IBM strengthens the Europe Smart Hospitals Market through its Watson Health data analytics and hybrid cloud infrastructure tailored for clinical and operational intelligence. Although it divested parts of Watson Health in 2022, IBM continues to support European hospitals via its consulting arm and Red Hat OpenShift platform, which underpins secure health data exchange networks in France, Italy, and the Netherlands. Globally, IBM enables health systems to build AI models on de-identified patient data while maintaining strict governance through its data fabric architecture. This initiative leverages federated learning to train models across institutions without sharing raw data, aligning with EU data sovereignty principles and advancing ethical AI adoption in clinical settings.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Smart Hospitals Market focus on developing interoperable and secure digital ecosystems that align with stringent EU regulations and clinical workflows. They prioritize strategic partnerships with public health systems to co-design solutions that address workforce shortages and aging population demands. Investment in cloud native and AI-enabled platforms allows for scalable deployment of predictive analytics and remote monitoring capabilities. Companies emphasize compliance with the General Data Protection Regulation and NIS2 by embedding end-to-end encryption, zero-trust architecture, and audit trails into their products. Open application programming interfaces and adherence to HL7 FHIR standards ensure seamless integration with legacy hospital information systems. Additionally, they offer managed services, including cybersecurity monitoring, staff training, and continuous system optimization to reduce implementation barriers for public hospitals with limited internal IT capacity.

MARKET SEGMENTATION

This Europe smart hospitals market research report is segmented and sub-segmented into the following categories.

By Component

- Software

- Hardware

- Services

By Application

- Remote Medicine Management

- Medical Connected Imaging

- Medical Assistance

- Electronic Health Records & Clinical Workflow

- Outpatient Vigilance

By Technology

- Cloud Computing

- Artificial Intelligence

- Wearable Technologies

- Radio Frequency Identification

By Connectivity

- Wired

- Wireless

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the size of the Europe smart hospitals market?

The Europe smart hospitals market is valued at USD 12.32 billion in 2025, driven by digital health adoption across major countries.

2. What drives growth in the Europe smart hospitals market?

Aging populations, chronic disease rise, and EU digital health initiatives propel the Europe smart hospitals market transformation.

3. Which countries lead the Europe smart hospitals market?

Germany, UK, France, and Netherlands dominate the Europe smart hospitals market with advanced infrastructure and policies.

4. What technologies rule the Europe smart hospitals market?

IoT and AI systems hold major shares in the Europe smart hospitals market for real-time monitoring and analytics.

5. How does 5G impact the Europe smart hospitals market?

5G enables seamless connectivity in the Europe smart hospitals market for remote monitoring and data transfer.

6. What trends shape the Europe smart hospitals market?

Interoperable platforms and patient-centric apps define trends in the Europe smart hospitals market evolution.

7. Which components dominate the Europe smart hospitals market?

Hardware like sensors leads the Europe smart hospitals market, followed by software for data management.

8. Who are key players in the Europe smart hospitals market?

Philips, Siemens Healthineers, and Medtronic compete in the Europe smart hospitals market innovations.

9. Why is Germany key in the Europe smart hospitals market?

Germany's Industry 4.0 healthcare initiatives position it as leader in the Europe smart hospitals market.

10. What challenges face the Europe smart hospitals market?

Data privacy and cybersecurity concerns challenge scalability in the Europe smart hospitals market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com