- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

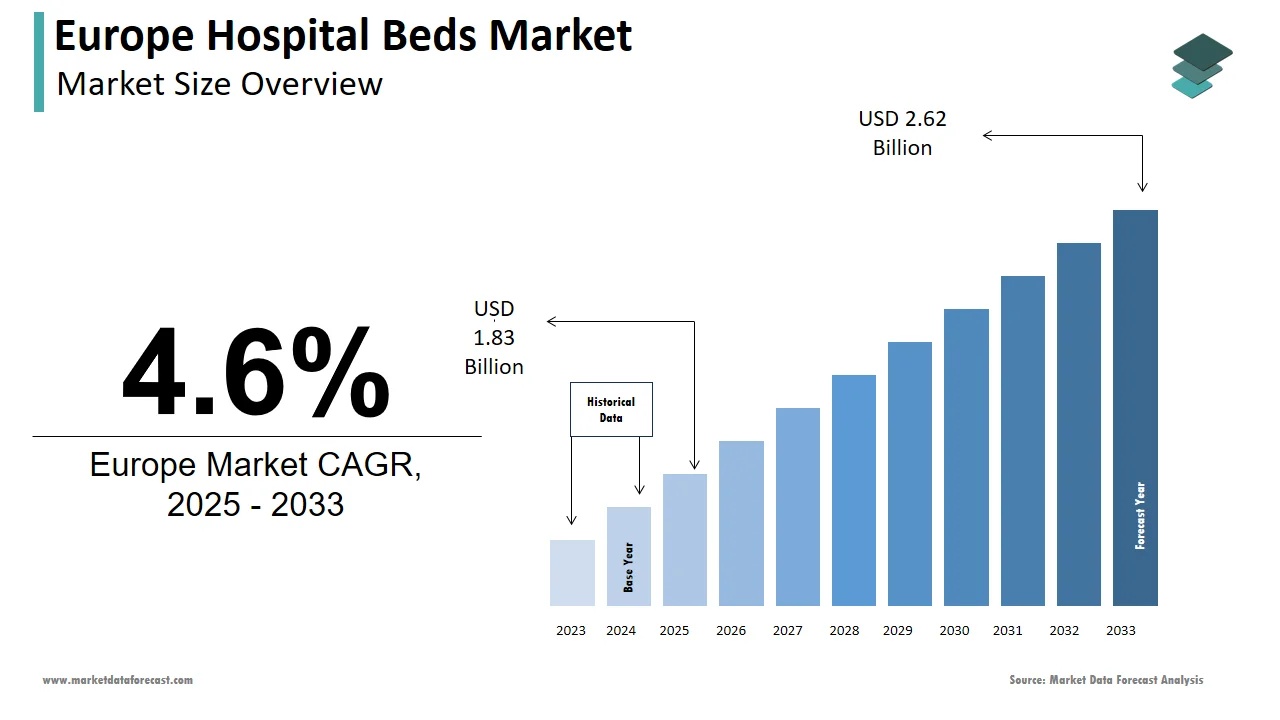

Market Size, 2025

$1.83 BnMarket Estimate, 2026

$1.91 BnMarket Forecast, 2034

$2.74 BnCAGR, 2026–2034

4.6%Europe Hospital Beds Market Size

The hospital beds market size in Europe was valued at USD 1.83 billion in 2025. The European market is estimated to be worth USD 2.74 billion by 2034 from USD 1.91 billion in 2026, growing at a CAGR of 4.6% from 2026 to 2034.

The Hospital Beds are specialized medical support systems designed for patient care in acute, long-term, and rehabilitative healthcare settings. These include manual, semi-electric, and fully electric beds equipped with features such as pressure redistribution support, patient monitoring integration, and infection-resistant surfaces. As per the World Health Organization, the average hospital occupancy rate in the WHO European Region, with countries like Germany and Belgium exceeding 80% indicates capacity strain.

MARKET DRIVERS

Aging Population Intensifies Demand for Geriatric and Long-Term Care Beds

The progressive aging of Europe’s population is a fundamental driver of hospital bed demand, particularly for models designed to manage chronic conditions, immobility, and fall prevention. The growing elderly population is elevating the growth of the hospital beds market. According to Eurostat, 102 million people in the European Union were aged 65 or older in 2024, representing 20.2% of the total population, with a figure projected to reach 24% by 2035. Consequently, healthcare systems are prioritizing beds with low height entry, lateral rotation, and integrated pressure ulcer prevention technologies. In countries like Italy and Portugal, where over 23% of the population is elderly, national health strategies now mandate minimum standards for bed functionality in public geriatric wards. Additionally, the rise of intermediate care facilities bridging hospital and home care has created demand for hybrid beds supporting both clinical monitoring and comfort over extended stays.

Hospital Infrastructure Modernization Programs Drive Capital Equipment Upgrades

The Nationwide initiatives to replace outdated medical infrastructure are accelerating the growth of hospital beds in Europe. Over 120 public hospital modernization projects were approved in 2023, totaling 8.4 billion euros in funding, with bed system upgrades listed as a core component in 78% of cases. Countries like France and Spain have launched decade-long facility renewal plans under their National Recovery and Resilience Frameworks, explicitly allocating funds for smart beds with integrated sensors and remote adjustability. These capital-intensive programs transform hospital bed acquisition from reactive maintenance to strategic investment in care quality and operational efficiency.

MARKET RESTRAINTS

Stringent Regulatory Standards Increase Time to Market and Compliance Costs

The rigorous regulatory oversight, primarily governed by the European Medical Device Regulation 2017 745, which classifies most hospital beds as Class IIa or IIb medical devices, is additionally to further enhance the growth of the Europe hospital beds market. As per the European Commission’s 2024 implementation review, over 60% of legacy bed models required extensive redesign to meet new requirements for clinical evaluation, usability engineering, and post-market surveillance. This regulatory recalibration has extended certification timelines from an average of 9 months to over 18 months, significantly delaying product launches. Manufacturers must now conduct extensive human factors testing to demonstrate that bed controls prevent accidental adjustments by patients with cognitive impairment, with a common concern in dementia. Additionally, the regulation mandates unique device identification UDI implementation, increasing administrative burden and software integration costs. Smaller European manufacturers lacking in-house regulatory expertise face disproportionate challenges, with the European Association of Medical Device Manufacturers estimating that compliance costs rose by 35% between 2021 and 2024.

Budget Constraints in Public Healthcare Systems Limit Procurement Volumes

The persistent fiscal pressures on national health services restrict large-scale hospital bed investments, despite clinical need is also impeding the growth of the Europe hospital beds market. According to the European Observatory on Health Systems and Policies, public health expenditure as a share of GDP declined or stagnated in 14 EU member states between 2022 and 2024 due to inflationary cost pressures and competing priorities, such as workforce retention. A 2023 survey by the European Hospital Association found that 41% of public hospitals delayed bed replacements due to budget freezes, with many resorting to third-party leasing or refurbished equipment. These financial realities fragment the market toward lower-tier segments and discourage manufacturers from investing in high-end innovations without guaranteed returns.

MARKET OPPORTUNITIES

Integration of Smart Beds with Hospital Digital Ecosystems Creates New Value Propositions

The emergence of hospital beds with digital health infrastructure that enhanced data capture and workflow integration is majorly promoting new opportunities for the expansion of the Europe hospital bed market. Smart beds equipped with load cells and occupancy sensors can automatically alert nursing staff to fall risks or prolonged immobility, reducing adverse events. The national pilot programs have demonstrated that connected beds reduce nurse documentation time by 18 minutes per shift. Furthermore, the European Commission’s Digital Europe Programme has allocated 220 million euros to support interoperability standards enabling bed data to feed into centralized clinical dashboards. Manufacturers who embed open architecture communication protocols, such as HL7 and FHIR, into bed control units position themselves as enablers of predictive care rather than just hardware suppliers.

Expansion of Home-Based and Intermediate Care Models Drives Demand for Hybrid Beds

The policy-driven shift toward decentralized care is creating opportunities for the growth of the Europe hospital beds market. As per the European Commission’s 2024 Action Plan on Home Care, over 28% of post-surgical and palliative care episodes are now delivered in home or community-based facilities, requiring medical equipment that balances clinical functionality with domestic usability. As per the World Health Organization, home-based hospitalization models can reduce readmission rates by up to 22% when supported by appropriate equipment. Manufacturers are responding with modular designs that offer hospital-level support yet fit through standard doorways and operate on residential power circuits. Additionally, rental and subscription models are emerging, allowing families to access high-end beds for short durations without capital outlay.

MARKET CHALLENGES

Supply Chain Fragmentation and Component Shortages Disrupt Production Continuity

The recurrent disruptions due to reliance on global supply chains for critical components, such as electric actuators, sensors, and specialty foam, are acting as a barrier for the growth of the Europe hospital beds market. According to the European Association of Medical Technology Industries, over 70% of motion control systems used in European hospital beds are sourced from Asia, primarily China and Taiwan. Additionally, the war in Ukraine impacted the supply of steel tubing and electronic subassemblies from Eastern Europe, further straining just-in-time manufacturing models. These supply vulnerabilities delay delivery schedules, inflate costs, and force hospitals to accept substitute models that may not meet clinical specifications, thereby compromising care continuity and equipment standardization across health networks.

Workforce Shortages Limit Effective Utilization of Advanced Bed Features

The shortage of workforce is additionally inhibiting the growth of the Europe hospital beds market. According to the European Federation of Public Service Unions, the EU faces a deficit of over 2 million healthcare workers, with nursing vacancies exceeding 15% in countries like the UK, France, and Italy. This shortage means that even when hospitals invest in smart beds with features like automatic repositioning or integrated vital sign monitoring, staff often lack the time or training to activate or interpret these functions. A 2024 study by the European Agency for Safety and Health at Work found that only 38% of nurses in multi-bed wards consistently used advanced pressure ulcer prevention protocols embedded in modern beds due to overwhelming patient loads. Consequently, the return on investment for high-end beds diminishes as sophisticated features remain underutilized. This misalignment discourages procurement committees from selecting premium models and reinforces a cycle of under specification that ultimately impacts patient outcomes and caregiver injury rates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Usage, Power, End-user, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Invacare Corporation, Paramount Bed Holdings Co. Ltd., Gendron Inc., Medline Industries Inc., LINET spol. S r.o., Arjo AB, Savaria Corporation, Savion Industries, Hill-Rom Holdings Inc., Stryker Corporation, and Getinge Group. |

SEGMENTAL ANALYSIS

By Usage Insights

The acute care beds segment was the largest and held 52.3% of the Europe Hospital Beds Market share in 2024, with the high volume of emergency surgeries, trauma admissions, and intensive care interventions across national health systems. As per the World Health Organization European Region, over 45 million inpatient surgical procedures were performed in 2023, necessitating beds equipped with rapid adjustability infection infection-resistant surfaces, and compatibility with life support equipment. Countries like Germany and France maintain acute bed densities exceeding 270 beds per 100000 inhabitants, far above the EU average of 210. Furthermore, the European Commission’s 2024 Hospital Resilience Framework mandates that acute care units upgrade to beds with integrated patient monitoring and fall prevention capabilities following post-pandemic reviews of care safety.

The long-term care beds segment is likely to register an anticipated CAGR of 7.9% during the forecast period, with Europe’s aging demographics and policy shifts toward extended care infrastructure. According to Eurostat, 20.2% of the EU population was aged 65 or older in 2024, with projections indicating this will reach 24% by 2035. The European Centre for Disease Prevention and Control estimates that 38% of adults over 75 live with three or more chronic conditions requiring prolonged bed-based care. Additionally, the European Investment Bank approved 3.4 billion euros in 2023 for long-term care infrastructure projects across Southern Europe, explicitly prioritizing beds with low height entry lateral rotation and bariatric support. These investments reflect a systemic transition from reactive hospitalization to proactive chronic care management, reinforcing demand for specialized long-stay beds.

By Power Type Insights

The electric segment was the largest by occupying 48.7% of the Europe hospital beds market share in 2024, owing to the stringent occupational safety mandates aimed at reducing caregiver injuries during patient handling. Electric beds enable precise control of head, knee, and Trendelenburg positions without physical strain, enhancing both staff safety and patient comfort. Additionally, integration with digital health systems such as automatic weight recording and movement alerts has made electric beds essential in smart hospital initiatives funded under the Digital Europe Programme. These regulatory, technological, and ergonomic advantages solidify their market leadership.

The semi-electric beds segment is expected to grow at a CAGR of 8.2% in next coming years, as healthcare systems seek cost-effective alternatives that retain core functionality. According to the European Hospital Association, 63% of smaller public hospitals in Eastern and Southern Europe operate under constrained capital budgets yet must comply with minimum safety standards. Semi-electric models, which automate critical adjustments like backrest and leg elevation while using manual height control, offer a balanced solution, reducing purchase costs by 25 to 30% compared to fully electric variants as noted in a 2024 procurement analysis by the Organisation for Economic Co-operation and Development. Countries like Portugal and Greece have adopted semi-electric beds as the standard for rural and district hospitals through centralized tendering. Moreover, modular designs now allow future retrofitting of height actuators, enabling phased upgrades.

By End User Insights

The hospitals segment accounted in holding a significant share of the Europe Hospital Beds Market in 2024, with their role as primary providers of inpatient and critical care across publicly funded systems. Additionally, hospitals serve as hubs for high acuity procedures, where the WHO European Region records over 300 million outpatient visits annually that often escalate to inpatient admission requiring immediate bed availability. This operational centrality, combined with centralized procurement authority, ensures hospitals remain the primary demand driver for advanced bed systems across all usage and power categories.

The ambulatory care centers segment is anticipated to register the fastest CAGR of 9.1% with the expansion of same-day surgery and chronic disease monitoring outside traditional hospitals. This shift is driven by cost containment strategies, where the Organisation for Economic Co-operation and Development estimates that ambulatory care reduces per procedure costs by 35 to 50% compared to inpatient admission. Consequently, these facilities require specialized beds that support rapid turnover, infection control, and patient comfort during short stays.

COUNTRY LEVEL ANALYSIS

Germany Hospital Beds Market Analysis

Germany was the top performer of the Europe Hospital Beds Market by holding 19.8% of the share in 2024, with its dense hospital network, robust public funding, and stringent safety regulations. According to the German Federal Statistical Office, the country operates over 480000 hospital beds with an average occupancy rate of 79% in 2024. Furthermore, Germany enforces strict ergonomic standards under the DGUV Rule 112 106, requiring all new beds in public hospitals to feature electric height adjustment to protect nursing staff. These policies, combined with a high density of academic medical centers in cities like Berlin, Munich, and Heidelberg, drive continuous demand for advanced acute and ICU beds with integrated monitoring capabilities, positioning Germany as both a consumption leader and regulatory benchmark for the region.

France Hospital Beds Market Analysis

France hospital beds market held 14.3% of the share in 2024, with its centralized healthcare system and large-scale modernization agenda. As per France’s Ministry of Health, the country maintains approximately 370000 hospital beds, with over 60% located in public institutions undergoing renewal under the Plan Hôpital 2030 initiative. The French High Authority for Health issued updated guidelines in 2024 mandating that all geriatric and post-surgical units use beds with integrated weighing and movement sensors. Additionally, France operates one of Europe’s largest psychiatric care networks with over 25000 dedicated psychiatric beds requiring specialized restraint-free designs.

United Kingdom Hospital Beds Market Analysis

The United Kingdom Hospital Beds Market growth is expected to register the highest CAGR throughout the forecast period, with demand shaped by National Health Service modernization and workforce safety mandates. The UK Health and Safety Executive enforces the Manual Handling Operations Regulations, which effectively require powered beds in all new acute and elderly care procurements to reduce staff injury rates. A 2024 NHS Supply Chain review showed that electric bed adoption in district hospitals rose by 22% year on year. Furthermore, the UK’s devolved administrations have launched pilot programs in Scotland and Wales, integrating smart beds with remote patient monitoring platforms to support early discharge. These initiatives reflect a strategic shift toward technology-enabled care pathways that position beds as data collection nodes rather than passive support systems.

Italy Hospital Beds Market Analysis

Italy hospital beds market growth is propelled by its dynamics, influenced by an aging population and regional healthcare disparities. This has intensified demand for long-term and geriatric beds, particularly in the North, where regional governments like Lombardy and Emilia Romagna have invested over 600 million euros since 2023 in elderly care infrastructure. However, Southern regions face budget constraints, leading to reliance on refurbished equipment, creating a dual market dynamic.

Spain Hospital Beds Market Analysis

Spain Hospital Beds Market growth is likely to grow with post-pandemic infrastructure renewal and decentralized procurement. The National Recovery and Resilience Plan has allocated 2.1 billion euros through 2026 for hospital modernization, with 40% earmarked for medical equipment, including beds with smart features. Regional governments such as Catalonia and Andalusia lead procurement through centralized tenders, favoring semi-electric models that balance cost and functionality. The warm climate and urban density also support the expansion of ambulatory surgery centers requiring compact recovery beds, further diversifying demand beyond traditional hospital settings.

COMPETITIVE LANDSCAPE

The Europe Hospital Beds Market features a competitive landscape shaped by a mix of global medtech giants, European specialists, and regional manufacturers. Competition is primarily driven by regulatory compliance, technological integration, and alignment with public procurement frameworks rather than price alone. Incumbents leverage decades of clinical validation and service infrastructure to maintain strong relationships with national health systems, while newer entrants focus on niche segments such as bariatric, psychiatric, or home care beds. The stringent requirements of the EU Medical Device Regulation have raised entry barriers favoring established players with robust quality management systems.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe carbon steel market include

- Invacare Corporation

- Paramount Bed Holdings Co. Ltd.

- Gendron Inc.

- Medline Industries Inc.

- LINET spol. s r.o.

- Arjo AB

- Savaria Corporation

- Savion Industries

- Hill-Rom Holdings Inc.

- Stryker Corporation

- Getinge Group

TOP PLAYERS IN THE MARKET

- Stryker Corporation is a prominent participant in the Europe hospital beds market, offering a comprehensive portfolio of electric and smart hospital beds under its InTouch and XT lines. The company focuses on integrating advanced safety features such as predictive fall alerts and pressure injury prevention technologies. In recent years, Stryker has strengthened its European footprint by expanding its service and training centers in Germany and the Netherlands to support rapid deployment and clinical onboarding. It also launched a cloud-connected bed platform in early 2024, enabling real-time data exchange with hospital electronic health records across EU member states. These initiatives align with Europe’s digital health transformation goals and reinforce Stryker’s role as a technology-driven solutions provider in both regional and global acute care environments.

- Hill Rom remains a key force in the Europe Hospital Beds Market through its legacy of innovation in patient safety and care workflow integration. Its VersaCare and Progressa bed systems are widely deployed in public hospitals across France, the UK, and Scandinavia. Following its acquisition by Baxter International, the business has accelerated R&D in connected care solutions, including beds with embedded biometric sensors. The company also enhanced its sustainability program by launching a bed refurbishment and recycling initiative in partnership with European healthcare systems, reducing equipment lifecycle emissions and supporting circular economy principles.

- Arjo AB is a leading European-origin player specializing in patient handling, mobility, and therapeutic surfaces, including advanced hospital beds for long-term and geriatric care. Headquartered in Sweden, the company leverages deep regional clinical insights to develop beds focused on pressure ulcer prevention, safe patient handling, and dignified care. Arjo has recently expanded its manufacturing capacity in Malmö to meet growing demand from Southern and Eastern European health ministries, modernizing aging infrastructure.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Hospital Beds Market emphasize compliance with the European Medical Device Regulation through rigorous clinical validation and technical documentation. They invest heavily in smart bed technologies that integrate with hospital information systems to support predictive care and workflow efficiency. Strategic partnerships with national health services and group purchasing organizations facilitate large-scale public tenders and standardization across regions. Companies also prioritize ergonomic design to reduce caregiver injuries, aligning with EU occupational safety directives. Additionally, sustainability initiatives, including take-back programs, modular component design, and energy-efficient actuators, are increasingly central to product development and public procurement criteria across Western and Northern Europe.

MARKET SEGMENTATION

This research report on the Europe hospital beds market has been segmented and sub-segmented into the following categories.

By Usage

- Acute care beds

- Long-term care beds

- Psychiatric care beds

- Others (maternity, etc.)

By Power

- Electric Bed

- Semi-Electric Bed

- Manual Bed

By End-User

- Hospitals

- Clinics

- Ambulatory services

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe