Europe Hospital Lighting Market Size, Share, Trends & Growth Forecast Report By Technology, Application, Product and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Europe Hospital Lighting Market Summary

The Europe Hospital Lighting Market is witnessing steady growth, driven by strict energy-efficiency regulations, hospital infrastructure modernization, and rising adoption of human-centric lighting to improve patient outcomes and staff performance. Increasing focus on sustainability under the European Green Deal, combined with the need for infection-control-compliant and digitally integrated lighting systems, is accelerating market demand. LED technology, smart lighting controls, and circadian-aligned illumination are reshaping hospital environments across the region.

Market Size & Growth

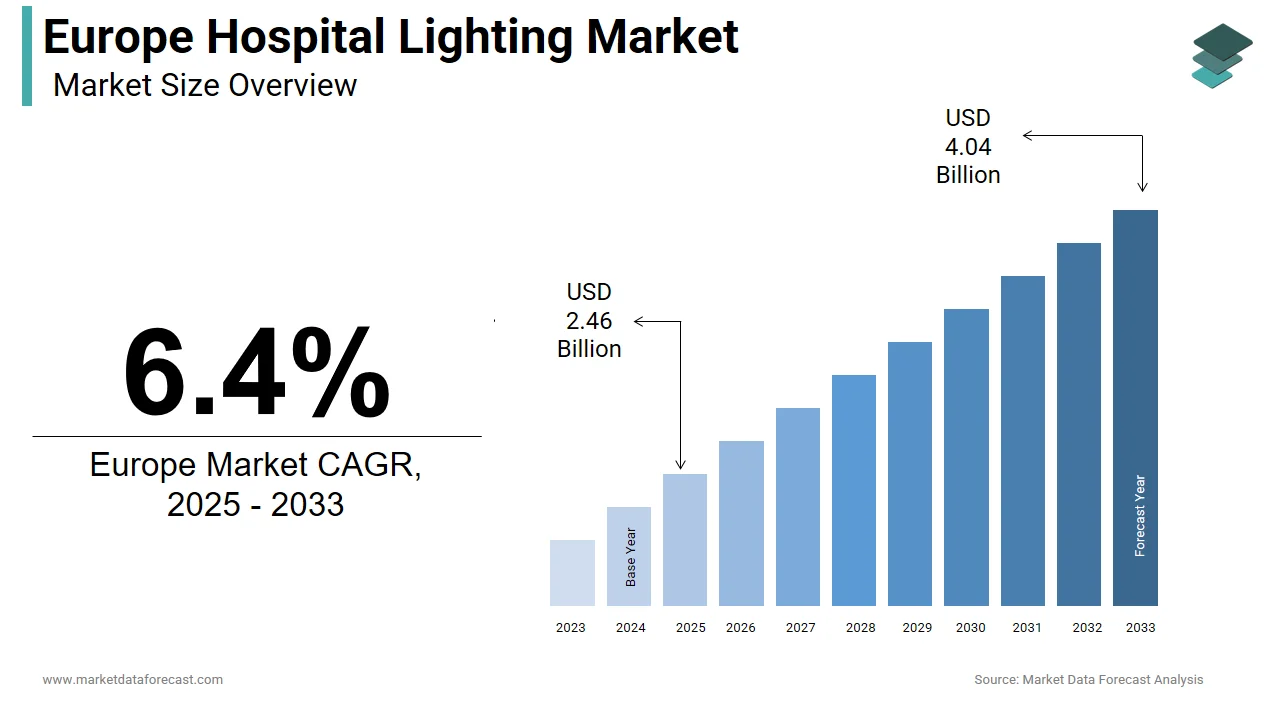

- Valued at USD 2.31 billion in 2025, the market is expected to reach USD 2.62 billion in 2026 and USD 4.30 billion by 2034, growing at a CAGR of 6.4% from 2026 to 2034.

Key Drivers

- Energy Efficiency Regulations: EU Energy Efficiency Directive and national laws pushing LED retrofits in hospitals.

- Human-Centric Lighting: Growing use of circadian lighting to improve patient recovery and staff alertness.

- Hospital Modernization: Large-scale renovation of aging healthcare infrastructure across Europe.

- Public Procurement Policies: Preference for high-efficacy, compliant lighting systems in public hospitals.

Leading Segments

- Technology: LED Lighting.

- Application: Patient Wards & ICUs, Surgical Suites.

- Product: Troffers and Surgical Lamps.

Key Trends

- Smart Lighting Integration: IoT-enabled lighting connected to hospital building management systems.

- Sustainability Focus: Use of energy-efficient, recyclable, and low-carbon lighting solutions.

- Infection-Control Design: Seamless, easy-to-clean luminaires for clinical environments.

- Digital OR Lighting: Surgical lamps synchronized with imaging and robotic systems.

Major Players

- Signify, OSRAM, Zumtobel Group AG, General Electric Company, Eaton Corporation, Cree Inc., Trilux, Herbert Waldmann, Koninklijke Philips N.V., Acuity Brands.

Europe Hospital Lighting Market Size

The size of the Europe hospital lighting market was valued at USD 2.46 billion in 2025. This market is expected to grow at a CAGR of 6.4% from 2026 to 2034 and be worth USD 4.30 billion by 2034 from USD 2.62 billion in 2026.

Hospital lighting includes specialized illumination systems designed to support clinical accuracy, patient well-being, and operational efficiency across healthcare environments. Unlike conventional architectural lighting, these solutions integrate photometric precision, circadian rhythm alignment, infection control compliance, and energy performance tailored to distinct zones from operating theaters and intensive care units to patient rooms and corridors. The Europe hospital lighting market operates within a regulatory and sustainability framework shaped by the European Green Deal, Energy Efficiency Directive, and stringent building codes such as the German EnEV and French RT 2012. As per the European Commission, public and private healthcare facilities in the European Union account for approximately 8% of total non‑residential energy consumption, with lighting representing nearly 25% of on‑site electricity use. According to the World Health Organization European Office, over 7,000 hospitals underwent infrastructure modernization between 2020 and 2024, with lighting upgrades cited as a priority in 63% of renovation projects. These upgrades increasingly focus on human‑centric lighting that mimics natural daylight patterns to reduce patient stress and improve staff alertness. Consequently, the market reflects a convergence of clinical necessity, environmental policy, and advancing LED and smart control technologies, positioning lighting as a critical enabler of next‑generation European healthcare delivery.

MARKET DRIVERS

Mandatory Energy Efficiency Standards and Public Procurement Policies

Europe’s stringent energy regulations and green public procurement directives are compelling hospitals to replace outdated lighting with high‑efficiency LED systems, which is a major factor driving the European hospital lighting market growth. The European Union’s Energy Efficiency Directive mandates that public buildings, including hospitals, pursue significant energy savings through retrofitting and modernization. According to official EU and national energy assessments, lighting retrofits in healthcare facilities can reduce electricity consumption substantially compared with conventional fluorescent systems. National policies amplify this requirement. For instance, France’s Multiannual Energy Program targets large reductions in public‑sector energy use by 2030, with hospital lighting identified as a high‑impact intervention. Similarly, Germany’s Hospital Future Act allocated multi‑billion-euro funding for infrastructure upgrades, with lighting modernization eligible for substantial subsidy coverage. Public procurement guidelines in Sweden and the Netherlands explicitly prioritize luminaires with high efficacy ratings, dimming capabilities, and compliance with Ecodesign regulations. These policy levers not only accelerate adoption but also ensure that new installations meet minimum performance thresholds for color rendering and glare control, directly linking energy savings to clinical functionality and patient comfort in European healthcare settings.

Integration of Human‑Centric Lighting to Enhance Patient Outcomes

Human‑centric lighting dynamically adjusts color temperature and intensity to support circadian biology, which is gaining clinical validation and institutional adoption across European hospitals and is further propelling the European hospital lighting market expansion. Research demonstrates that exposure to properly tuned light cycles improves sleep quality, reduces delirium in elderly patients, and accelerates postoperative recovery. For instance, wards equipped with circadian lighting report measurable improvements in sleep quality and reductions in medication use and nighttime agitation. The European Society of Intensive Care Medicine includes lighting parameters in its environmental care guidance, recommending morning exposure to higher‑intensity cool white light to help synchronize circadian rhythms. Moreover, several national healthcare design standards now recommend or mandate circadian lighting in specific facility types such as psychiatric and neonatal units. This fusion of evidence‑based design and therapeutic intent is transforming hospital lighting from a utility into a non‑pharmacological care modality, driving demand for advanced, tunable LED systems across the continent.

MARKET RESTRAINTS

High Upfront Investment and Budget Constraints in Public Healthcare Systems

Despite long‑term savings, the initial capital required for advanced hospital lighting systems remains a significant barrier, particularly in publicly funded healthcare networks facing fiscal pressure, which is a key restraint to the growth of the European hospital lighting market. Modern LED and human‑centric lighting installations often entail higher upfront costs than basic retrofit solutions due to smart controls, tunable drivers, and architectural integration. For instance, constrained capital envelopes for non‑clinical upgrades limit the pace of comprehensive lighting overhauls in many countries. Consequently, many hospitals delay comprehensive lighting upgrades, opting instead for piecemeal replacements that fail to deliver system‑wide benefits. Even in wealthier systems, procurement decisions are subject to multi‑year budgeting cycles and competitive tendering that prioritize lowest cost over lifecycle value. These financial realities slow the adoption of high‑performance lighting, especially in aging facilities where wiring and ceiling infrastructure may require concurrent upgrades, compounding total project costs and implementation complexity.

Lack of Standardized Clinical Lighting Guidelines Across Europe

The absence of harmonized clinical lighting standards across Europe creates ambiguity in design specifications and inhibits scalable deployment of advanced systems, which is further impeding the growth of the European hospital lighting market. While some countries have adopted detailed lighting criteria for patient rooms and operating theatres, others rely on generic building codes that do not address healthcare‑specific needs such as shadow reduction, color fidelity for wound assessment, or glare control for bedridden patients. For instance, only a minority of member states explicitly reference international hospital‑lighting guidance in national regulations, which is resulting in wide national variation. This fragmentation forces manufacturers to customize solutions per country, increasing development costs and delaying market entry. Regional differences in lux and technical requirements across member states complicate multinational hospital groups’ procurement strategies. Without pan‑European clinical lighting benchmarks, hospitals struggle to justify premium investments, and suppliers face inconsistent technical and regulatory expectations, ultimately constraining innovation diffusion.

MARKET OPPORTUNITIES

Retrofitting Aging Hospital Infrastructure Under EU Green Transition Funding

Europe’s vast stock of aging hospital buildings presents a major opportunity for lighting modernization, catalyzed by dedicated funding from the European Union’s Green Transition initiatives. According to EU recovery and green‑transition program summaries, substantial funding has been allocated for public building energy‑efficiency upgrades, with healthcare facilities explicitly eligible. As per the European Investment Bank, a large share of hospitals in Southern and Central Europe were constructed before 1990 and rely on obsolete T8 or halogen lighting with poor efficacy and high maintenance burdens. In Portugal, the National Recovery Plan included targeted funding for hospital retrofits in 2023 with performance requirements for lighting systems in retrofit projects. Similarly, Greece launched national upgrade programs mandating LED conversion and daylight‑harvesting measures in state‑owned medical centers. These programs not only cover hardware costs but also fund energy‑performance contracting, allowing hospitals to repay investments through verified savings. This policy‑driven retrofit wave enables lighting providers to deploy integrated solutions at scale, transforming outdated facilities into energy‑efficient, patient‑centered care environments aligned with Europe’s decarbonization goals.

Expansion of Smart Lighting Integration with Hospital Building Management Systems

The convergence of Internet‑of‑Things‑enabled lighting with hospital building‑management systems is a strategic opportunity for the European hospital lighting market. Modern LED luminaires equipped with sensors and connectivity can feed real‑time data on occupancy, ambient light, and room usage into centralized platforms that enable dynamic resource allocation. For instance, smart lighting systems have delivered substantial reductions in unoccupied‑room energy waste and enabled operational optimizations such as usage‑based cleaning schedules. In the Netherlands, hospital projects have integrated lighting controls with clinical workflows to automatically adjust light scenes during night rounds, minimizing sleep disruption. The European Standard EN 15232 recognizes lighting as a key subsystem in building automation, which is facilitating interoperability with HVAC and security networks. Furthermore, cybersecurity‑certified lighting gateways compliant with industrial IT standards address hospital IT concerns, accelerating adoption. As European hospitals digitize operations, lighting evolves from passive illumination to an active data layer, unlocking efficiencies in energy, staffing, and patient flow that justify premium system investments.

MARKET CHALLENGES

Stringent Infection Control and Maintenance Requirements Limit Fixture Design Flexibility

Hospital lighting must comply with rigorous hygiene standards that restrict fixture geometry, material selection, and accessibility, which is posing significant engineering challenges to the growth of the European hospital lighting market. Smooth, seamless surfaces without crevices are mandated to prevent microbial accumulation, particularly in operating rooms and isolation units. For instance, luminaires in high‑risk zones must be cleanable with hospital‑grade disinfectants without degradation of optical or electrical components. This requirement eliminates many standard commercial LED designs that feature grilles, diffusers, or exposed drivers. Additionally, maintenance protocols demand that fixtures allow tool‑free access for lamp or driver replacement to minimize downtime in critical areas. In some national hospital design guidelines, ceiling‑mounted luminaires are required to withstand repeated cleaning cycles with common disinfectants. These constraints limit the use of complex optical systems or integrated sensors that could compromise cleanability. Consequently, manufacturers must invest in specialized housings that increase production costs and extend development timelines, slowing the introduction of innovative features in clinical environments.

Complex Stakeholder Decision Making and Long Procurement Cycles

Hospital lighting projects in Europe involve multidisciplinary stakeholders whose competing priorities delay approvals and complicate specifications, which is also challenging the expansion of the European hospital lighting market. Unlike commercial or residential lighting, hospital decisions require consensus on clinical impact, energy performance, maintenance burden, and aesthetic integration, often spanning 18–36 months from concept to installation. For instance, a large share of hospital lighting tenders are revised multiple times due to conflicting input from clinical and technical teams. In public systems, procurement must follow EU public‑tender rules that emphasize transparency and competition, which can discourage lifecycle cost analysis. Even when budgets are approved, administrative bottlenecks are common; some regional permitting regimes require separate environmental and electrical approvals for lighting upgrades, adding months to project timelines. This fragmented governance model impedes the rapid adoption of advanced systems, as suppliers must navigate inconsistent evaluation criteria and prolonged validation processes, reducing agility in responding to emerging clinical or sustainability needs across Europe’s diverse healthcare landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Application, Product, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | General Electric Company, Eaton Corporation PLC, Cree Inc., Herbert Waldmann GmbH & Co. KG, Trilux GmbH & Co. KG, Signify, Zumtobel Group AG, KLS Martin GmbH + Co. KG, Koninklijke Philips N.V., Hill-Rom Holdings Inc., OSRAM, and Acuity Brands. |

SEGMENTAL ANALYSIS

By Technology Insights

The LED technology segment commanded the highest share of 71.4% of the European hospital lighting market in 2024. The dominance of the LED technology segment in this regional market is driven by its unmatched energy efficiency, extended service life, and compatibility with advanced clinical lighting requirements. Unlike legacy fluorescent systems, LEDs offer precise chromatic control, high color rendering indices above 90, and flicker‑free operation, which is critical for accurate visual diagnosis and surgical precision. According to the European Commission’s 2023 Energy Efficiency Report, LED retrofits in public healthcare facilities reduce lighting energy consumption by more than half, with payback periods under four years when supported by EU green funding. National policies further accelerate adoption. Germany’s Hospital Future Act mandates that all lighting upgrades funded under the program utilize LED technology with a minimum efficacy threshold. Additionally, LEDs support human‑centric lighting through tunable white systems that adjust correlated color temperature from 2700K to 6500K, which aligns with circadian health protocols endorsed by the European Society of Intensive Care Medicine. The absence of mercury also simplifies disposal and enhances compliance with the EU’s Waste Electrical and Electronic Equipment Directive. These combined technical, regulatory, and clinical advantages have cemented LED as the de facto standard across Europe’s modernizing healthcare infrastructure.

By Application Insights

The patient wards and intensive care units (ICU) segment held the 44.6% of the European hospital lighting market share in 2024. The dominance of the patient wards and ICUs segment in this regional market is attributed to the critical role of lighting in supporting patient recovery, circadian regulation, and staff vigilance in prolonged care environments. Modern ward lighting must balance clinical functionality with therapeutic comfort that provides adequate illumination for monitoring while minimizing sleep disruption through low blue‑light emission at night. According to a 2023 multicenter study published by the University Medical Center Hamburg, patients exposed to circadian‑tuned LED lighting in German ICUs experienced fewer episodes of delirium and shorter hospital stays compared to those under static lighting. National design guidelines reinforce this trend. Denmark’s Health Building Authority requires all new ICU rooms to incorporate tunable white lighting with automated day‑night cycles. Additionally, the spatial scale of wards creates high‑volume demand for standardized, maintainable luminaires. The European Hospital Association reports that a majority of hospital bed capacity in Western Europe underwent lighting modernization between 2021 and 2024, primarily to comply with energy efficiency and patient well‑being mandates. This combination of clinical evidence, regulatory push, and infrastructure scale solidifies wards and ICUs as the cornerstone application for advanced hospital lighting in Europe.

The surgical suites segment is the fastest-growing application segment in the Europe hospital lighting market and is expected to register a CAGR of 12.04% over the forecast period, owing to the rising volume of minimally invasive and robotic procedures that demand ultra‑precise, shadow‑free illumination with exceptional color fidelity. According to Eurostat, surgical interventions in EU hospitals increased significantly between 2019 and 2023, with laparoscopic and endoscopic surgeries accounting for most of the growth. These procedures require surgical lamps with high color rendering indices above 95 and correlated color temperatures near 4500K to accurately distinguish tissue types and vascular structures. Regulatory standards are tightening accordingly. The European Committee for Electrotechnical Standardization updated EN 60601‑2‑41 in 2022 to mandate integrated light‑field monitoring and thermal management in surgical luminaires. Leading hospitals are also adopting hybrid systems that combine overhead surgical LED troffers with articulated shadow‑reducing lamps, enabling seamless transitions between general and task lighting. In the Netherlands, the Erasmus Medical Center installed a fully digital operating room suite in 2023 featuring surgical lights synchronized with imaging systems to auto‑adjust intensity during endoscopic feed capture. As Europe’s surgical caseload grows and precision medicine advances, lighting becomes an integral component of procedural safety and efficiency, driving premium adoption in this high‑value segment.

By Product Insights

The troffers segment accounted for 50.9% of the regional market share in 2024. These recessed or surface‑mounted luminaires are the backbone of general illumination in corridors, wards, and administrative zones due to their uniform light distribution, modular design, and seamless integration into suspended ceiling grids. In European hospitals, troffers offer plug‑and‑play replacement for legacy fluorescent fixtures without structural modifications. According to the European Lighting Association, a large majority of hospital lighting retrofits in France, Germany, and the Netherlands between 2022 and 2024 utilized LED troffers with integrated drivers and emergency backup. Their flat, smooth surfaces align with infection control protocols by eliminating dust traps and enabling easy disinfection with hospital‑grade agents. Additionally, modern troffers support daylight harvesting and occupancy sensing through embedded controls compliant with the EU’s Ecodesign Directive. The Charité Berlin’s 2023 infrastructure upgrade replaced thousands of fluorescent troffers with high‑efficacy LED versions, achieving a substantial reduction in lighting energy use. This blend of hygiene compliance, energy performance, and architectural adaptability makes troffers the default choice for large‑scale, code‑compliant hospital lighting across Europe.

The surgical lamps segment is the fastest-growing product segment in the Europe hospital lighting market and is expected to register a CAGR of 10.6% over the forecast period, owing to the technological advancements that merge optical precision with digital integration to meet the demands of modern operating theaters. Contemporary surgical lamps now feature multi‑source LED arrays that eliminate shadows, maintain stable color temperature under prolonged use, and project light fields exceeding 160,000 lux, which is critical for deep cavity procedures. According to the European Society of Surgical Oncology, most new operating rooms commissioned in Western Europe since 2022 specify surgical lamps with integrated cameras and data interfaces for recording and teleconsultation. Manufacturers are also addressing thermal management. The latest models limit surface temperature rise to under 10 degrees Celsius to prevent tissue desiccation, a requirement codified in Germany’s Medical Devices Directive. In Sweden, Karolinska University Hospital’s 2023 operating suite deployed surgical lamps with real‑time spectral tuning that adapts to tissue reflectance during robotic prostatectomies. Furthermore, the EU Medical Device Regulation 2017/745 now classifies high‑end surgical lamps as Class IIa devices, necessitating rigorous clinical validation that favors innovative suppliers. These clinical, regulatory, and technological drivers position surgical lamps as a high‑value, high‑innovation frontier in Europe’s hospital lighting ecosystem.

COUNTRY-LEVEL ANALYSIS

Germany Hospital Lighting Market Analysis

Germany occupied 20.9% of the European hospital lighting market share in 2024 and is likely to remain the regional leader in hospital lighting over the coming years, owing to the high retrofit and new‑build activity, extensive public healthcare infrastructure, stringent energy laws, and targeted hospital modernization funding. The federal Hospital Future Act has catalyzed widescale retrofits, with funded projects required to meet minimum LED efficacy thresholds and incorporate human‑centric design in patient areas. EnEV energy regulations and national lighting power density limits push new hospital builds toward low‑wattage, high‑efficacy solutions. Clinical pioneers such as Charité Berlin and University Hospital Heidelberg have implemented circadian lighting in intensive care and recovery wards, reporting measurable benefits for patient sleep and staff alertness. A strong domestic lighting industry, including global innovators, accelerates deployment of advanced clinical fixtures and integrated control systems, reinforcing Germany’s role as the market’s technical and commercial hub.

United Kingdom Hospital Lighting Market Analysis

The United Kingdom is expected to see sustained smart‑lighting adoption as decarbonization and integrated care programs continue to prioritize energy and clinical outcomes. The UK market is characterized by system‑wide modernization under Integrated Care Systems and a Net Zero agenda that identifies lighting retrofits as a high‑impact intervention. Large‑scale LED and IoT upgrades across acute and community facilities are supported by public decarbonization funding, while evidence‑based design studies are driving clinical use cases for tunable and tunable‑white systems in psychiatric, surgical, and inpatient settings. New hospital projects increasingly integrate lighting into building management and clinical workflows, and regulatory alignment with ecodesign standards, plus agile device approvals, sustain a favorable environment for innovative medical lighting solutions.

France Hospital Lighting Market Analysis

France is likely to accelerate LED transition and sustainable fixture adoption as national renovation programs and circular‑economy rules continue to shape procurement. The French market is driven by a major National Hospital Renovation Plan that mandates high‑efficacy LEDs, occupancy/daylight controls, and minimum color rendering performance for public hospitals. Human‑centric lighting is prioritized in sensitive units such as neonatal and geriatric care, and surgical suites are moving toward digitally synchronized lighting and imaging integration. Circular‑economy requirements for recycled content in luminaires and forthcoming thermal‑performance regulations further stimulate demand for energy‑efficient, sustainably manufactured hospital lighting systems.

Italy Hospital Lighting Market Analysis

Italy is expected to register a rapid retrofit wave as EU recovery funding and national modernization plans accelerate the replacement of legacy fluorescent systems. The Italian market’s large stock of aging hospitals creates immediate retrofit opportunities, with regional authorities and national programs tying lighting upgrades to mandated energy‑savings targets. Pilot deployments of circadian lighting in critical care have shown clinical benefits and are informing broader rollouts, while hygiene and material standards for clinical luminaires shape product specifications. These combined drivers, urgent infrastructure needs, EU financing, and clinical innovation are propelling Italy’s transition to modern hospital lighting at scale.

Netherlands Hospital Lighting Market Analysis

The Netherlands is projected to consolidate its role as a technical benchmark for human‑centric and digitally integrated hospital lighting solutions. Dutch policy and professional guidance mandate circadian and evidence‑based lighting in key clinical areas, and a high share of recent projects already specify tunable‑white systems with automated day/night cycles. Leading hospitals integrate lighting telemetry into digital twins and building management platforms to optimize energy use and patient flow, while stringent procurement criteria emphasize ecolabels, low embedded carbon, and glare control. This combination of clinical focus, digital integration, and sustainability standards positions the Netherlands as a reference market for next‑generation hospital lighting across Europe.

COMPETITIVE LANDSCAPE

Competition in the Europe hospital lighting market is characterized by a convergence of clinical expertise, regulatory agility, and sustainable innovation. While global lighting specialists dominate, the market rewards deep understanding of healthcare workflows, infection control protocols, and human factors design. Differentiation arises not from luminous output alone but from integration with hospital digital ecosystems, compliance with medical device classifications, and evidence-based health outcomes. The phase out of fluorescent technology under EU Ecodesign rules has intensified focus on high-performance LED retrofits, yet price competition is tempered by the premium placed on reliability, color fidelity, and circadian functionality. National hospital modernization funds create large-scale opportunities, but winning requires navigating complex public procurement rules and multidisciplinary stakeholder input. Emerging players face high barriers due to certification costs and the need for clinical validation, while incumbents leverage existing relationships and proven installations. The market increasingly favors solutions that merge lighting with data intelligence, transforming luminaires into nodes of operational insight. This sophisticated landscape favors companies that balance engineering excellence with empathetic design and policy alignment across Europe’s diverse healthcare systems.

KEY MARKET PLAYERS

The leading companies operating in the Europe hospital lighting market include:

- General Electric Company

- Eaton Corporation PLC

- Cree Inc.

- Herbert Waldmann GmbH & Co. KG

- Trilux GmbH & Co. KG

- Signify

- Zumtobel Group AG

- KLS Martin GmbH & Co. KG

- Koninklijke Philips N.V.

- Hill-Rom Holdings Inc.

- OSRAM

- Acuity Brands

TOP PLAYERS IN THE MARKET

- Signify is a leading force in the Europe hospital lighting market through its comprehensive portfolio of connected LED systems and human-centric lighting solutions. The company supplies advanced tunable white troffers, surgical lamps, and IoT-enabled luminaires to major healthcare institutions across Germany, the Netherlands, and the United Kingdom. Signify integrates its Interact Healthcare platform to enable data-driven lighting control that enhances patient well-being and operational efficiency. In 2023, the company launched its new surgical lighting family compliant with the updated EN 60601 2 41 standard, featuring shadow-free illumination and thermal management for prolonged procedures. Its collaboration with university hospitals on circadian lighting studies has generated clinical evidence supporting recovery outcomes. Signify’s global reach, regulatory expertise, and deep integration with building management systems solidify its influence in advancing clinical lighting standards worldwide.

- OSRAM contributes significantly to the Europe hospital lighting market through its precision optical components and integrated lighting systems tailored for surgical and diagnostic applications. The company leverages its expertise in high flux LEDs and thermal management to deliver surgical luminaires that maintain stable color temperature and luminance during complex procedures. OSRAM’s solutions are embedded in operating rooms across Germany, France, and Switzerland, where reliability and photometric accuracy are non-negotiable. In 2024, the company introduced a new generation of medical-grade LED modules with enhanced color rendering above 95 CRI, specifically designed for wound assessment and tissue differentiation. It also partnered with European medical device manufacturers to co-develop hybrid lighting imaging systems for robotic surgery. Through its focus on clinical-grade performance and regulatory compliance, OSRAM plays a pivotal role in shaping the technological frontier of surgical and critical care lighting globally.

- Zumtobel Group holds a strong position in the Europe hospital lighting market by offering architecturally integrated, infection control-compliant luminaires for patient wards, corridors, and examination rooms. The company’s Litecom lighting control system enables seamless integration of daylight harvesting, occupancy sensing, and circadian tuning in accordance with European hospital design standards. Zumtobel has executed large-scale retrofits in public hospitals across Austria, Italy, and Sweden, aligning with national decarbonization mandates. In 2023, it launched the Tecton Continuous lighting system with smooth, seamless surfaces and tool-free maintenance, meeting the stringent hygiene requirements of the Robert Koch Institute. The company also emphasizes sustainability, ensuring all new luminaires contain recycled aluminum and comply with EU Ecolabel criteria. By combining clinical functionality, aesthetic design, and environmental responsibility, Zumtobel strengthens healthcare environments across Europe and influences global best practices in institutional lighting.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe hospital lighting market prioritize human-centric lighting integration to support circadian health and improve patient outcomes through tunable white LED systems. They align product development with stringent European regulatory standards, including EN 60601 for surgical lamps and Ecodesign Directive requirements for energy efficiency. Companies invest in IoT-enabled luminaires that feed occupancy and ambient data into hospital building management systems to optimize energy use and space utilization. Strategic partnerships with university hospitals generate clinical evidence on lighting’s impact on recovery, delirium reduction, and staff alertness. Retrofit solutions are engineered for seamless compatibility with existing ceiling grids and electrical infrastructure to minimize installation disruption. Infection control compliance drives fixture design with smooth non-porous surfaces and tool-free maintenance access. Participation in EU-funded hospital modernization programs ensures alignment with public procurement priorities. Emphasis on sustainability includes the use of recycled materials and compliance with circular economy principles. These multifaceted strategies collectively reinforce technological leadership and market relevance in Europe’s evolving healthcare infrastructure landscape.

MARKET SEGMENTATION

This Europe hospital lighting market research report is segmented and sub-segmented into the following categories.

By Technology

- Renewable Energy

- LED

- Fluorescent lights

By Application

- Surgical Suites

- Patient wards & ICUs

- Examination Rooms

By Product

- Surface Lamps

- Troffers

- Surgical Lamps

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe hospital lighting market?

The Europe hospital lighting market supplies specialized fixtures for surgical suites, patient rooms, and clinics. LED solutions dominate due to energy efficiency regulations across EU facilities.

Why is the Europe hospital lighting market growing?

The Europe hospital lighting market expands through EU energy directives and healthcare infrastructure upgrades. Sustainability mandates drive LED retrofitting in aging hospital buildings.

What segments define the Europe hospital lighting market?

Segments in the Europe hospital lighting market include surgical lights, troffers, and pendants. Operating theater lighting leads due to precision requirements in procedures.

Who leads the Europe hospital lighting market?

Leaders in the Europe hospital lighting market engineer high-CRI LEDs for surgical clarity. German manufacturers dominate with advanced human-centric lighting solutions.

What drives innovation in the Europe hospital lighting market?

Innovation in the Europe hospital lighting market features circadian lighting and IoT controls. Tunable white LEDs support patient recovery through natural light simulation.

How do regulations shape the Europe hospital lighting market?

Regulations in the Europe hospital lighting market enforce Ecodesign standards and RoHS compliance. EU Green Deal accelerates energy-efficient retrofits across healthcare facilities.

What trends influence the Europe hospital lighting market?

Trends in the Europe hospital lighting market emphasize wireless controls and antimicrobial coatings. Human-centric lighting improves patient outcomes through biological rhythm alignment.

What challenges face the Europe hospital lighting market?

Challenges in the Europe hospital lighting market include legacy fluorescent replacement costs. Retrofitting programs address budget constraints in public healthcare systems effectively.

How does technology advance the Europe hospital lighting market?

Technology advances the Europe hospital lighting market with shadowless surgical LEDs and smart sensors. Occupancy detection optimizes energy use in underutilized clinical spaces.

What role does the Europe hospital lighting market play in surgery?

The Europe hospital lighting market supports surgery through high-intensity focusable lights. Adjustable color temperatures enhance tissue contrast during complex procedures.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com