Europe Hysteroscopy Instruments Market Size, Share, Trends & Growth Forecast Report By Product, By Usability, By Application, By End User, and By Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

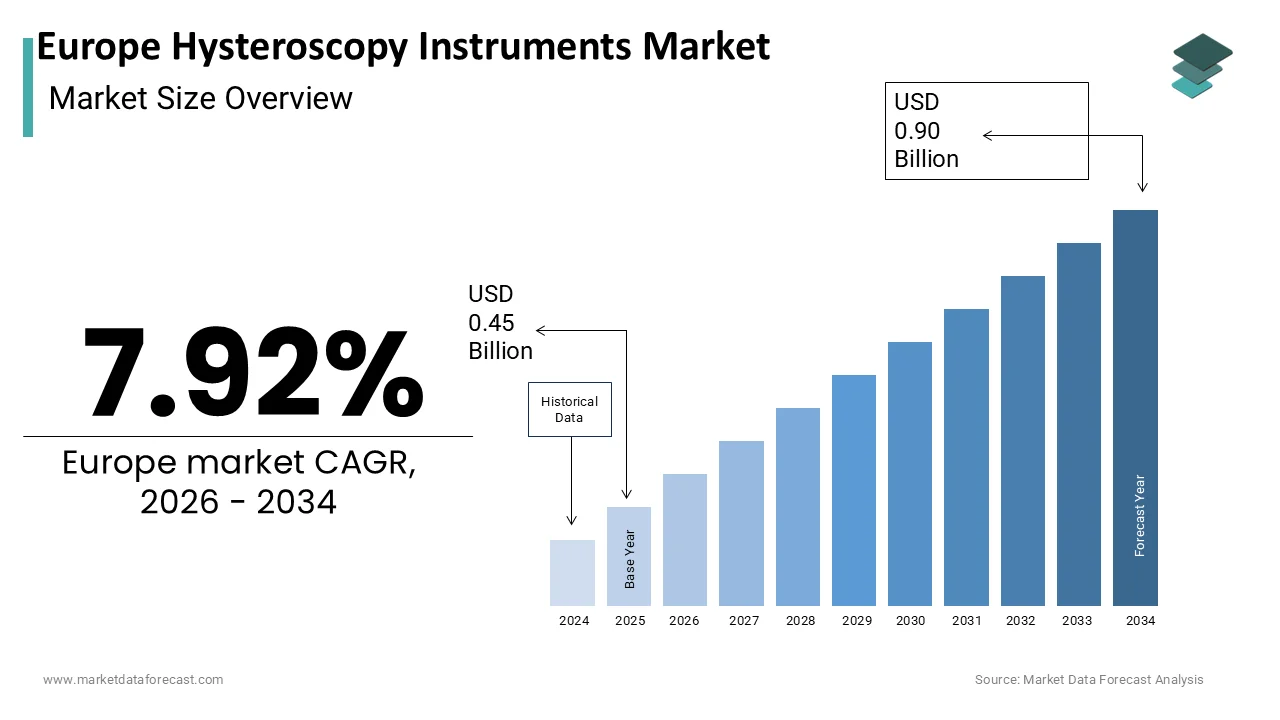

$0.45 BnMarket Estimate, 2026

$0.49 BnMarket Forecast, 2034

$0.90 BnCAGR, 2026–2034

7.92%Europe Hysteroscopy Instruments Market Size

The europe hysteroscopy instruments market size was valued at USD 0.45 billion in 2025, is expected to have a 7.92% CAGR from 2026 to 2034 and be worth USD 0.90 billion by 2034 from USD 0.49 billion in 2026.

Hysteroscopy Instruments are medical devices used to visualize and operate within the uterine cavity for diagnostic and therapeutic gynecological procedures. These instruments include rigid and flexible hysteroscopes, operative sheaths, resectoscopes, fluid management systems, and accessory tools designed for minimally invasive interventions such as polypectomy, myomectomy, and endometrial ablation. According to studie a significant number of hysteroscopic procedures were performed across the European Union in 2023, which reflects widespread clinical adoption. Furthermore, national health technology assessment bodies in Germany, France, and the Netherlands now prioritize hysteroscopy over blind dilation and curettage due to superior diagnostic accuracy and reduced complication rates. These clinical, regulatory, and epidemiological factors collectively define a market driven by precision medicine, patient safety, and procedural efficacy rather than volume alone.

MARKET DRIVERS

Rising Prevalence of Gynecological Disorders Requiring Minimally Invasive Diagnosis

The increasing incidence of uterine pathologies such as polyps, fibroids, and intrauterine adhesions continues to be a major driver of the Europe hysteroscopy instruments market. According to sources, a portion of women of reproductive age experience a gynecological condition during their lifetime, with abnormal uterine bleeding affecting a portion of this cohort. The European Society of Human Reproduction and Embryology reports that uterine polyps are detected in 24 percent of women undergoing infertility evaluation,n and hysteroscopy remains the gold standard for both diagnosis and removal. This shift toward early and accurate diagnosis aligns with EU healthcare policies emphasizing ambulatory care and reduced hospital stays, thereby sustaining consistent demand for advanced hysteroscopic instrumentation.

Integration of Hysteroscopy into Fertility and Reproductive Health Pathways

Hysteroscopy has become an indispensable component of modern fertility workups and assisted reproductive technology protocols, which propels the expansion of the Europe Hysteroscopy instruments market. The European Society of Gynaecological Endoscopy recommends routine hysteroscopy for all patients with recurrent implantation failure, a condition affecting a share of IVF patients, as undetected intrauterine abnormalities reduce pregnancy rates. Similarly, the UK’s National Institute for Health and Care Excellence includes hysteroscopy in its fertility pathway for women with two or more miscarriages. This institutional embedding within reproductive care ensures recurring demand for both diagnostic and operative hysteroscopy systems across public and private fertility clinics.

MARKET RESTRAINTS

Stringent Regulatory Compliance Under the EU Medical Devices Regulation

The implementation of the European Union Medical Devices Regulation has significantly increased the regulatory burden, which obstructs the growth of the Europe hyperoscopy instruments market. According to sources, Class IIa and higher devices, including operative hysteroscopes, demonstrate clinical performance through robust post-market clinical follow-up studies and maintain comprehensive technical documentation. Compliance costs have risen substantially, with small and medium enterprises reporting notable expenditures per product line to meet new requirements, as per research. Apart from these, the Unique Device Identification system requires full traceability from production to patient implantation, increasing software and labeling complexity. These hurdles delay time to market by several months for new instruments and deter innovation among smaller players lacking regulatory infrastructure, thereby constraining market dynamism despite strong clinical demand.

Limited Reimbursement Office-Based Hysteroscopy in Several Member States

Inconsistent reimbursement across European healthcare systems limits its adoption and utilization, and as a result hampers the expansion of the Europe hysteroscopy instruments market. According to sources, only a few European countries have separate reimbursement systems for outpatient hysteroscopy, while many still include it within general gynecological consultation fees. Many healthcare professionals in parts of Southern and Eastern Europe continue to avoid outpatient hysteroscopy because of insufficient financial incentives despite its clinical advantages, according to sources. The economic incentive to adopt modern hysteroscopy systems remains weak in several key markets. This is without a harmonized valuation that reflects the diagnostic precision and cost savings of office procedures.

MARKET OPPORTUNITIES

Advancement of Miniaturized and Flexible Hysteroscopes for Office Use

The development of ultra-thin flexible hysteroscopes with integrated imaging and fluid management is generating new opportunities for the growth of the Europe hysteroscopy instruments market. According to the European Society of Gynaecological Endoscopy, instruments with diameters under 3 millimeters now enable diagnostic procedures without cervical dilation or anesthesia, reducing patient discomfort and enabling same-day return to work. These next-generation devices incorporate chip-on-tip technology and smartphone connectivity, allowing image capture and teleconsultation, which is particularly valuable in rural areas with limited specialist access. These innovations are poised to expand procedural volume and instrument adoption beyond traditional hospital settings, as a Eurobarometer survey found that a portion of European women prefer office-based diagnostics.

Expansion of Training Programs and Standardized Certification Frameworks

The establishment of structured hysteroscopy training and credentialing systems across Europe is creating fresh prospects for the expansion of the Europe hysteroscopy instruments market. As per research, multiple gynecologists completed their accredited hysteroscopy certification program in recent years, with mandatory simulation and live case requirements. National societies in Germany, Spain,n and Sweden now require hysteroscopy competency for hospital privileges, driving demand for training compatible instrument sets. Furthermore, the EU’s program funded to development of virtual reality simulators that replicate tissue resistance and fluid dynamics, enhancing skill acquisition. These educational and quality assurance initiatives not only improve patient safety but also increase clinician confidence in adopting advanced operative hysteroscopy techniques, thereby expanding the addressable market for sophisticated instrumentation.

MARKET CHALLENGES

High Cost of Advanced Hysteroscopy Systems and Budget Constraints in Public Hospitals

The significant capital investment required for integrated hysteroscopy towers with high definition imaging, fluid control, and electrosurgical capabilities poses a major impediment to the growth of the Europe hysteroscopy market. According to research, the cost of a full operative hysteroscopy suite exceeds ds notable amount, with annual maintenance costing a significant amount, which further strains hospital budgets. These limitations force clinicians to rely on older, rigid scopes with inferior optics or refer patients to centralized centers, causing delays. The diffusion of advanced hysteroscopy technology will remain uneven across Europe. This is because there are no dedicated funding streams or leasing models that are tailored to public procurement cycles.

Shortage of Trained Personnel for Operative Hysteroscopy Procedures

There is a vital gap in gynecologists proficient in advanced operative hysteroscopy across many European countries, which in turn hinders the expansion of the Europe hysteroscopy instruments market. The learning curve for operative hysteroscopy is steep, requiring supervised cases to achieve competency, as per the Cochrane Database of Systematic Reviews. Furthermore, the retirement of experienced practitioners without adequate succession planning exacerbates the deficit, with Germany projecting a shortfall of skilled hysteroscopists by 2030, as per research. This human capital constraint limits the utilization of available instrumentation and restricts patient access to minimally invasive alternatives to hysterectomy. The full potential of hysteroscopy technology will remain unrealized in significant parts of Europe until training capacity expands through simulation centers and cross-border fellowships.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Usability Application, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | KARL STORZ, Olympus, Richard Wolf, Stryker, Hologic, Medtronic, Ethicon, B. Braun, Boston Scientific, MedGyn Products, CooperSurgical, Cook Medical, Medicon, Maxer Medizintechnik, Hospiline Equipment |

SEGMENTAL ANALYSIS

By Product Insights

The hysteroscope segment dominated the Europe Hysteroscopy Instruments Market by accounting for 38.2% share in 2025. The dominance of the hysteroscope segment is fuelled by its role as the foundational visualization tool without which no hysteroscopic procedure, diagnostic or operative, can be performed. Technological advancements such as 4K imaging, integrated light sources, and narrow band imaging have enhanced diagnostic accuracy for subtle endometrial lesions with an improvement in polyp detection rates. National clinical guidelines in some countries require hysteroscopic visualization before any intrauterine intervention, reducing reliance on blind techniques. Furthermore, the shift toward office-based diagnostics has spurred demand for miniaturized scopes under 3 millimeters in diameter, which account for a portion of new hysteroscope sales in Western Europe, as per studies. These clinical and technological imperatives ensure the hysteroscope remains the indispensable core of the procedural ecosystem.

The hysteroscopic tissue removal systems segment is predicted to witness the highest CAGR of 12.6% from 2025 to 2033. The rapid growth of the hysteroscopic tissue removal systems segment is driven by the rising preference for one-step hysteroscopic polypectomy and myomectomy that combine visualization and resection in a single outpatient visit. According to sources, many fertility clinics in Europe have adopted advanced tissue removal systems for treating endometrial polyps to improve safety and procedural accuracy. In France, the national health authority has endorsed mechanical extraction technologies for their efficiency in reducing operation time and enhancing patient outcomes, as per research. Besides, these systems eliminate the need for electrosurgical energy, reducing fluid absorption risks and enabling use under local anesthesia.

By Usability Insights

In 2025, the reusable instruments segment held a substantial share of the Europe Hysteroscopy Instruments Market 2025. The prominence of the reusable instruments segment is driven by the prevalence is rooted in the cost efficiency and durability of high-quality stainless steel and optical components used in hysteroscope sheaths and operative tools. National health systems in Germany, France, and Italy prioritize capital investment in reusable systems due to long-term budget constraints. Furthermore stringent EU Medical Devices Regulation requires rigorous validation of reprocessing protocols, ensuring patient safety. These institutional and regulatory factors sustain the dominance of reusable instrumentation despite growing interest in disposables.

The disposable hysteroscopy instruments segment is estimated to register the fastest CAGR of 14.3% from 2025 to 203,3, owing to the elimination of reprocessing risks, cross-contamination concerns, and operational barriers in sterile services. The European Commission’s guidance on infection prevention in outpatient settings drew attention to disposables as a strategy to reduce healthcare-associated infections, with pilot programs in Spain reporting a 22 percent decline in post-procedure endometritis. According to sources, the European Union’s circular economy policies include programs that promote the collection and recycling of medical devices to minimize environmental impact. Some companies have launched CE-marked disposable hysteroscopes with integrated fluid management, further accelerating adoption. Hence, the disposable segment is capturing a growing share of decentralized care.

BY Application Insights

The diagnostic applications segment was the largest region of the Europe Hysteroscopy Instruments Market by capturing 61.8% share in 2025. The dominance of the diagnostic applications segment is because of the widespread use of hysteroscopy as the gold standard for evaluating abnormal uterine bleeding, infertility, and postmenopausal bleeding. As per sources, a significant number of diagnostic hysteroscopies were performed across the EU in 2023, with office-based procedures comprising a portion of the total. National guidelines in some countries require hysteroscopic evaluation before any surgical intervention for suspected intrauterine pathology, reducing unnecessary hospital admissions. These clinical imperatives ensure diagnostics remain the primary driver of instrument utilization.

The operative segment is anticipated to witness the fastest CAGR of 11.9% during the forecast period due to the increasing adoption of minimally invasive alternatives to hysterectomy for benign uterine conditions. Standardized training frameworks developed by European medical societies are enhancing surgeon proficiency and procedural outcomes. Advanced tissue removal systems are also supporting same-day patient discharge and expanding the adoption of outpatient procedures, according to sources. These clinical and economic advantages are shifting care paradigms toward uterus-preserving interventions.

By End User Insights

The hospitals segment led the Europe Hysteroscopy Instruments Market by occupying a significant share in 2025. Their role as primary centers for complex operative hysteroscopy, including myomectomy, adhesiolysis, and septum resection, which require advanced imaging, fluid management, and anesthesia support, rt significantly contributed to the rise of the hospitals segment. Public healthcare networks are also prioritizing collective procurement of reusable surgical instruments to optimize costs. The European Commission is supporting the digital integration of hysteroscopy units with electronic health record systems across multiple countries to improve documentation and oversight, as per research. These structural and clinical factors ensure hospitals remain the cornerstone of hysteroscopy service delivery.

The clinics segment is likely to experience the fastest CAGR of 13.1% from 2025 to 2033. The rapid growth of the clinics segment is due to the decentralization of gynecological care and the rise of specialized outpatient centers offering office hysteroscopy under local anesthesia. Private fertility and women’s health clinics across Western Europe are increasingly providing same-day diagnostic hysteroscopy services to improve patient access, according to sources. In the United Kingdom, many private centers have transitioned to using disposable hysteroscopes to streamline procedures and reduce equipment handling time, as per research. National policies in Sweden and the Netherlands reimburse office procedures at parity with hospital care, incentivizing private investment. Besides, telemedicine integration allows real-time image sharing with specialists for second opinions, expanding access in rural areas. These operational and policy enablers position clinics as the highest growth channel for hysteroscopy instrumentation.

COUNTRY LEVEL ANALYSIS

Germany Hysteroscopy Instruments Market Analysis

Germany was the top performer in the Europe Hysteroscopy Instruments Market in 2025 by accounting for 24.7% share in 2025. Advanced healthcare infrastructure and strong clinical guidelines are largely contributing to the domination of Germany in the regional market. The country performs a large number of hysteroscopies annually, with a portion conducted in hospital settings equipped with high-definition imaging and integrated fluid management systems, as per sources. Public hospitals benefit from centralized procurement through regional alliances, reducing instrument costs by 18 percent. Furthermore, Germany leads in training. The Medical Devices Regulation enforcement is strict, with all instruments requiring notified body certification through TÜV agencies, ensuring high safety standards. These systemic strengths sustain Germany’s prominence in both adoption and innovation.

France Hysteroscopy Instruments Market Analysis

France was the second largest region in the Europe Hysteroscopy Instruments Market and held 18.3% of the regional market share in 2025, with demand driven by national fertility policies and outpatient care expansion. The country has pioneered office hysteroscopy. A large proportion of gynecologists in France now prefer using advanced miniaturized scopes that help improve the precision of procedures, as per research. The country’s healthcare policy ensures standardized coverage for both diagnostic and operative hysteroscopy, which makes these treatments more accessible for patients. In addition, France is known for some of the most innovative medical device companies that often work with leading hospitals to develop the next generation of gynecological instruments. These clinical policies and industrial factors create a robust and growing market environment.

United Kingdom Hysteroscopy Instruments Market Analysis

The United Kingdom saw consistent growth in the Europe Hysteroscopy Instruments Market due to the integration into national clinical pathways and private sector innovation. As per research, hysteroscopy is widely recommended in the United Kingdom for women with certain reproductive health conditions to ensure proper medical evaluation and follow-up. The country’s public healthcare system now conducts a large number of these procedures each year, with a growing emphasis on convenient office-based diagnostic services, according to sources. Private women’s health clinics in London and Manchester have driven the adoption of disposable hysteroscopes. The UK also leads in registry development. Post Brexit, the Medicines and Healthcare products Regulatory Agency maintains alignment with the EU MDR, ensuring continued device availability. These clinical governance and market dynamics support sustained instrument utilization across public and private settings.

Italy Hysteroscopy Instruments Market Analysis

Italy expanded gradually in the Europe Hysteroscopy Instruments Market owing to the high prevalence of uterine pathologies and regional specialization. The country performs a notable number of hysteroscopies annually, with Lombardy and Emilia Romagna serving as hubs for advanced operative procedures, including hysteroscopic sterilization reversal. National guidelines from the Italian Society of Gynaecology mandate hysteroscopy before any endometrial ablation, ensuring procedural standardization. Italy also leads in academic research. Regional health authorities have invested in modernizing equipment. These epidemiological and institutional factors emphasize Italy’s strong market position.

Netherlands Hysteroscopy Instruments Market Analysis

The Netherlands is predicted to grow in the Europe Hysteroscopy Instruments Market during the forecast period due to its dominance in outpatient gynecology and digital integration. As per research, the Netherlands has one of the most advanced uses of hysteroscopy among European countries, showing a strong emphasis on women’s diagnostic care. The healthcare system fully supports both diagnostic and operative hysteroscopy procedures, making them easily accessible for patients. These policies, technological, and educational enablers position the Netherlands as a model for efficient and accessible hysteroscopic care.

COMPETITIVE LANDSCAPE

The competition in the Europe Hysteroscopy Instruments Market is characterized by a mix of established multinational corporations and specialized medical device firms vying for clinical adoption across hospital and outpatient settings. Differentiation occurs through optical quality system, ease of use, and compliance with stringent EU regulatory standards rather than price alone. Leading players compete by offering comprehensive ecosystems thatinclude opticale imaging, towers fluid, control, and ac,ce, and ssories ensuring seamless interoperability. The shioffice-basedfice based diagnostics has intensified rivalry in miniaturized and disposable segments where innovation in ergonomics and workflow efficiency is important. Regulatory barriers under the EU Medical Devices Regulation favor companies with robust quality management systems and clinical evidence capabilities, limiting new entrants. Training and education have become competitive, with manufacturers sponsoring simulation labs and certification programs to build clinician loyalty. Despite the moderate pricing burden, the market remains innovation-driven with competition centered on clinical outcomes, process safety, and alignment with European healthcare policies promoting minimally invasive care.

KEY MARKET PLAYERS

A few of the promising companies operating in the europe hysteroscopy instruments Market Profiled in the report are

- KARL STORZ

- Olympus

- Richard Wolf

- Stryker

- Hologic

- Medtronic

- Ethicon

- B. Braun

- Boston Scientific

- MedGyn Products

- CooperSurgical

- Cook Medical

- Medicon

- Maxer Medizintechnik

- Hospiline Equipment.

TOP LEADING PLAYERS IN THE MARKET

- Karl Storz SE & Co KG is a German multinational renowned for its high precision endoscopic systems, including advanced hysteroscopes and operative instrumentation used across European hospitals and clinics. The company contributes significantly to the global market by setting optical and ergonomic standards in minimally invasive gynecology. Karl Storz maintains a strong presence in Europe through direct clinical training programs and partnerships with academic medical centers.

- Boston Scientific Corporation is a global medical technology leader with a robust portfolio in women’s health, including innovative hysteroscopic tissue removal systems widely adopted in Europe. The company plays a pivotal role globally by advancing one-step operative solutions that enable same-day polypectomy and myomectomy in outpatient environments. In Europe, Boston Scientific collaborates with national gynecological societies to support clinical adoption and training. It also achieved CE certification for a fully disposable hysteroscope with integratfluidistensionnio,,n simplifying workflow in clinics and reducing reprocessing burdens. These developments strengthen its position in the growing ambulatory care segment across the continent.

- Olympus Corporation is a Japanese multinational with a substantial footprint in the Europe Hysteroscopy Instruments Market through its advanced visualization and resectoscopic platforms. The company contributes to the global market by integrating artificial intelligence and high-definition imaging into gynecological endoscopy. Olympus supplies hysteroscopy systems to major hospitals in Germany, France, and the United Kingdom, and actively participates in European clinical guidelines development. These initiatives support Olympus’s commitment to clinical excellence and education in minimally invasive gynecology.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Hysteroscopy Instruments Market pursue several strategic imperatives to maintain clinical relevance and regulatory compliance. These include continuous innovation in visualization technologies such as 4K imaging, narrow band imaging, and AI-assisted diagnostics to enhance procedural accuracy. Companies invest heavily in developing integrated systems that combine hysteroscopy fluid management and tissue removal into seamless workflows, reducing procedure time and complexity. Strategic collaborations with professional societies and academic institutions support clinical training and evidence generation. Compliance with the EU Medical Devices Regulation drives rigorous post-market surveillance and quality management upgrades. Apart from these, firms are expanding their portfolios to include both reusable high-end systems for hospitals and cost-effective disposable solutions for outpatient clinics. These strategies collectively address evolving clinical needs, regulatory demand, nd care decentralization trends across Europe.

MARKET SEGMENTATION

This research report on the European hysteroscopy instruments market has been segmented and sub-segmented into the following categories..

By Product

-

Handheld Instruments

- Forceps

- Scissors

- Dilators

- Other Handheld Instruments

- Hysteroscope

- Rigid

- Flexible

- Resectoscope

- Unipolar

- Bipolar

- Hysterosheaths

- Hysteroscopic Tissue Removal Systems

By Usability

- Reusable Instruments

- Disposable Instruments

By Application

- Diagnostics

- Operative

- Myomectomy

- Polypectomy

- Endometrial Ablation

- Tubal Sterilization

By End-User

- Hospitals

- Clinics

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the Europe Hysteroscopy Instruments Market growth?

Key factors include rising incidence of uterine disorders, advancements in imaging technology, increasing female geriatric population, and strong preference for minimally invasive gynecologic procedures.

2. Which countries lead the Europe Hysteroscopy Instruments Market?

Major markets include the United Kingdom, Germany, France, Italy, and Spain. The UK leads the regionBthanks to advanced healthcare systems, innovation, and supportive government initiatives.

3. Who are the prominent companies in the Europe Hysteroscopy Instruments Market?

Key players include Karl Storz, Olympus, Stryker, Hologic, B. Braun, Medtronic, Ethicon, Boston Scientific, Richard Wolf, and CooperSurgical, all contributing to regional market competitiveness.

4. What are the main product segments within the Europe Hysteroscopy Instruments Market?

The market consists of handheld instruments, hysteroscopes, tissue removal systems, fluid managementB systems, and accessories, with forceps and dilators showing rising clinical adoption.

5. How is technology influencing the Europe Hysteroscopy Instruments Market?

Adoption of 3D and 4K imaging, robotic-assisted operations, and sensor-integrated smart devices are improving surgical accuracy, patient outcomes, and infection control standards

6. What role does minimally invasive surgery play in this market?

Minimally invasive gynecologic procedures like hysteroscopic polypectomy and myomectomy are gaining preference for less tissue trauma, faster recovery, and reduced hospital stays.

7. Which end-users contribute most to the Europe Hysteroscopy Instruments Market?

Hospitals and ambulatory surgical centers are the leading end-users, collectively accounting for most device procurement and usage in the region’s gynecology departments.

8. What are the leading trends in Europe’s hysteroscopy segment?

Trends include rising use of disposable hysteroscopy instruments, robotic-assisted procedures, and demand for cost-efficient office-based surgeries that reduce operating room reliance

9. How does the regulatory environment affect the Europe Hysteroscopy Instruments Market?

Strict European medical device regulations ensure high product quality and patient safety, though they also extend approval timelines and increase R&D expenditures for manufacturers.

10. What are the major challenges faced by the Europe Hysteroscopy Instruments Market?

Challenges include high costs of advanced devices, limited trained specialists, and competition from alternative diagnosis methods like laparoscopy and ultrasound imaging.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com