Europe Industrial Centrifuges Market Size, Share, Trends & Growth Forecast Report By Type (Sedimentation, Filtering), Design (Horizontal Centrifuge, Vertical Centrifuge), Operation Mode (Batch, Continuous), Industry (Food and Beverage, Pharmaceutical, Water and Wastewater Treatment, Chemical, Metal and Mining, Power, Pulp and Paper, Other Industries), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) – Industry Analysis From 2026 to 2034.

Market Size, 2025

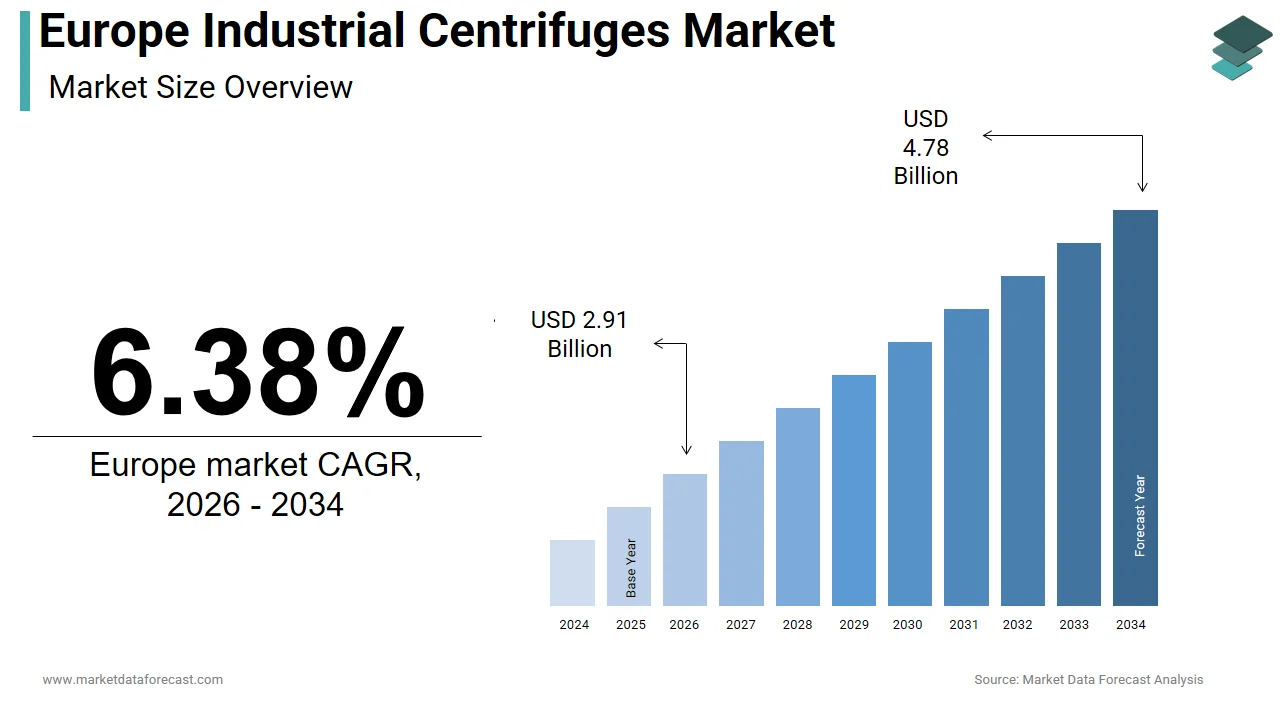

$2.74 BnMarket Estimate, 2026

$2.91 BnMarket Forecast, 2034

$4.78 BnCAGR, 2026–2034

6.38%Europe Industrial Centrifuges Market Size

The size of the Europe industrial centrifuges market was valued at USD 2.74 billion in 2025. This market is expected to grow at a CAGR of 6.38% from 2026 to 2034 and be worth USD 4.78 billion by 2034 from USD 2.91 billion in 2026.

The Europe industrial centrifuge market includes a range of high-performance separation technologies used across multiple sectors, including chemical processing, pharmaceuticals, food and beverage, oil and gas, wastewater treatment, and energy. Industrial centrifuges are critical in separating solids from liquids or different liquid phases based on density differences through high-speed rotational force. These machines vary widely in design, from decanter and disc stack centrifuges to basket and scroll types, each tailored for specific applications such as crude oil purification, dairy processing, biopharmaceutical manufacturing, and sludge dewatering.

According to the European Chemical Industry Council, several manufacturing plants in Western Europe rely highly on continuous phase separation technologies, with centrifuges being the preferred method for high-volume processing. Additionally, the region's commitment to sustainable operations and automation has further reinforced the demand for modern centrifuge systems equipped with digital monitoring and predictive maintenance features.

MARKET DRIVERS

Expansion of the Biopharmaceutical and Healthcare Industries

One of the primary drivers of the Europe industrial centrifuge market is the rapid expansion of the biopharmaceutical and healthcare sectors, particularly in countries like Germany, Switzerland, and the UK. Centrifuges play an essential role in drug development, vaccine production, blood component separation, and diagnostic testing. According to the European Federation of Pharmaceutical Industries and Associations, the EU pharmaceutical sector invested over €37 billion in R&D in 2023, leading to increased demand for high-purity separation equipment in laboratories and large-scale manufacturing units. In particular, the rise in biologics and cell-based therapies has necessitated advanced centrifugation technologies capable of handling delicate biological materials without compromising integrity. Moreover, the post-pandemic surge in vaccine production has accelerated the deployment of industrial-scale centrifuges in purification lines. Leading pharmaceutical companies such as Roche and Novartis have expanded their bioreactor capacities, directly increasing procurement of high-speed disc stack and tubular bowl centrifuges.

Growth in Wastewater Treatment and Environmental Compliance Initiatives

Another significant driver of the Europe industrial centrifuge market is the increasing focus on wastewater treatment and environmental sustainability, driven by stringent EU regulations on water discharge and pollution control. Centrifuges are extensively used in municipal and industrial wastewater treatment plants for sludge thickening, dewatering, and biosolids management. The implementation of the Urban Waste Water Treatment Directive has compelled local authorities to upgrade aging infrastructure, resulting in higher investments in modern dewatering systems. Additionally, industries such as food processing, pulp and paper, and chemicals generate substantial volumes of organic waste, which require effective separation solutions to meet environmental obligations. A report by the European Commission noted that industrial wastewater reuse targets set under the Circular Economy Action Plan have led to an increase in centrifuge installations in these sectors since 2021.

MARKET RESTRAINTS

High Capital and Maintenance Costs Limiting Adoption Among SMEs

A key restraint affecting the Europe industrial centrifuge market is the high capital expenditure associated with advanced centrifuge systems, particularly those designed for continuous operation in large-scale industrial settings. Premium models equipped with variable speed drives, automated controls, and corrosion-resistant materials often come with high price tags, making them inaccessible for small and medium-sized enterprises (SMEs). According to the study, nearly 40% of surveyed SMEs in the chemical and food processing sectors cited affordability as a primary barrier to upgrading their separation technologies in 2023. Beyond initial costs, ongoing maintenance also poses a financial burden. High-speed industrial centrifuges require regular inspection, lubrication, and component replacement to ensure optimal performance and safety. This economic pressure is especially pronounced in Eastern Europe, where budget constraints and limited access to financing options hinder technology upgrades. Many smaller firms continue to rely on outdated mechanical separators, limiting market penetration despite rising demand for efficient wastewater and product recovery solutions.

Stringent Regulatory Approvals and Certification Requirements

Stringent regulatory approvals and certification requirements present a significant challenge to the Europe industrial centrifuge market, particularly for new entrants and niche manufacturers. Compliance with directives such as the Pressure Equipment Directive (PED), Machinery Directive, and ATEX regulations for explosive environments necessitates rigorous testing, documentation, and third-party verification before market entry. According to the European Committee for Standardization, obtaining CE marking for industrial centrifuges involves extensive conformity assessments, often extending product launch timelines by several months. In the pharmaceutical and food processing sectors, adherence to Good Manufacturing Practice (GMP) and Hygienic Design Standards further complicates the approval process. Manufacturers must demonstrate that their centrifuge designs prevent contamination, facilitate easy cleaning, and meet material compatibility criteria. Furthermore, export-oriented producers face additional hurdles when navigating varying international standards. For instance, centrifuges intended for sale in North America must comply with ASME BPVC and FDA regulations, adding another layer of complexity and cost. These regulatory demands not only slow down innovation but also deter smaller players from entering the market, thereby limiting competition and slowing overall market expansion in certain segments.

MARKET OPPORTUNITIES

Rising Demand for Energy-Efficient and Smart Centrifuge Systems

A major opportunity emerging in the Europe industrial centrifuge market is the growing demand for energy-efficient and smart centrifuge systems that integrate digital monitoring, predictive maintenance, and remote diagnostics. With increasing pressure on industries to reduce carbon footprints and operational costs, manufacturers are shifting toward intelligent centrifuge solutions that optimize energy consumption and enhance process efficiency. Leading centrifuge manufacturers such as GEA Group and Alfa Laval have introduced variable frequency drive (VFD)-enabled models that adjust rotational speeds based on load conditions, reducing energy consumption. Also, IoT-enabled centrifuges equipped with real-time sensors allow operators to monitor vibration levels, temperature fluctuations, and wear indicators, preventing unplanned downtime and improving asset longevity. In the food and beverage sector, where hygiene and process consistency are paramount, companies are increasingly investing in self-diagnosing centrifuges that provide data analytics for quality assurance. As per the European Food Safety Authority, digital integration in food processing machinery has grown in recent years, reflecting broader trends toward automation and sustainability.

Expansion of Renewable Energy and Biofuel Production Facilities

The expansion of renewable energy and biofuel production facilities across Europe presents a significant growth opportunity for the industrial centrifuge market, particularly in biodiesel and ethanol processing. Centrifuges play a crucial role in biomass separation, oil extraction, and fermentation residue management, making them integral to the production chain of biofuels. In response to the Renewable Energy Directive (RED III), which mandates a major share of renewables in transport by 2030, numerous European countries have expanded their bioethanol and biodiesel refining capacities. Countries like France, Sweden, and Finland have ramped up investment in second-generation biofuel plants, where centrifuges are employed for lipid extraction from algae and lignocellulosic feedstocks. Moreover, the European Commission’s Carbon Border Adjustment Mechanism (CBAM) has encouraged biofuel producers to adopt cleaner and more efficient processing methods, including advanced centrifugal separation techniques.

MARKET CHALLENGES

Intense Competition from Asian and North American Centrifuge Manufacturers

One of the foremost challenges facing the Europe industrial centrifuge market is the intensifying competition from centrifuge manufacturers based in Asia and North America. Companies from China, India, and the United States are increasingly capturing market share by offering cost-effective alternatives to European brands, leveraging lower production costs and streamlined supply chains. While European centrifuge manufacturers are known for superior build quality, precision engineering, and compliance with stringent safety standards, their counterparts in Asia are rapidly closing the technological gap. Chinese and Indian firms are now producing high-capacity, digitally enabled centrifuges at competitive prices, attracting budget-conscious buyers in Eastern Europe and small-to-medium industrial operators. Additionally, aggressive marketing strategies and after-sales service packages offered by non-European players are influencing purchasing decisions. Some global end-users are diversifying their supplier base to include low-cost providers, diluting the dominance of established European brands such as Andritz and Flottweg.

Supply Chain Disruptions and Component Shortages

Supply chain disruptions and component shortages represent a significant challenge for the Europe industrial centrifuge market, particularly following the impacts of the pandemic, geopolitical tensions, and semiconductor scarcity. The manufacturing of high-performance centrifuges relies on precision-engineered components such as high-strength alloys, magnetic bearings, and programmable logic controllers, many of which are sourced globally. The war in Ukraine and sanctions on Russia have disrupted raw material supplies, particularly affecting the availability of nickel and stainless steel, key materials in corrosion-resistant centrifuge construction. Besides, freight bottlenecks and rising logistics costs have added pressure on manufacturers' profit margins. A report by the European Logistics Association indicated that shipping costs from Asia to Europe increased in early 2023, impacting procurement strategies. Furthermore, labor shortages in skilled machining and assembly operations have slowed domestic production rates. Several manufacturers have reported difficulties in sourcing qualified technicians to operate advanced CNC machining centers and perform precision balancing of rotating components. These disruptions have led to order backlogs and delayed project executions, challenging the ability of European centrifuge suppliers to meet growing demand across key sectors such as pharmaceuticals, food processing, and energy.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Design, Operation Mode, Industry, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

| Market Leaders Profiled | Alfa Laval AB, GEA Group AG, HAUS Centrifuge Technologies, Andritz AG, and Flottweg SE. |

SEGMENTAL ANALYSIS

By Type Insights

The sedimentation centrifuge segment had the largest share of the Europe industrial centrifuge market by accounting for 57.8% of total revenue in 2024. This dominance is primarily attributed to the widespread application of sedimentation-based separation in wastewater treatment, chemical processing, food and beverage production, and pharmaceutical manufacturing. In Germany alone, where wastewater compliance standards are among the strictest in Europe, a large share of treatment facilities rely on decanter-type sedimentation centrifuges. Additionally, the food and beverage industry extensively employs sedimentation technology for clarification processes in dairy, juice, and edible oil refining. Moreover, biopharmaceutical manufacturers increasingly depend on continuous-flow sedimentation systems for cell harvesting and protein purification.

The segment of filtration centrifuges represented the fastest-growing category in the Europe industrial centrifuge market, projected to expand at a CAGR of 6.3% from 2025 to 2033. This growth is driven by increasing demand from industries requiring precise solid-liquid separation with minimal moisture content in the final cake discharge, particularly in fine chemical synthesis, specialty pharmaceuticals, and advanced material processing. In the pharmaceutical sector, the rise in contract manufacturing organizations (CMOs) has led to increased adoption of automatic filtration centrifuges for active pharmaceutical ingredient (API) isolation. A report by the European Federation of Pharmaceutical Industries and Associations noted that pharmaceutical CMO capacity utilization reached 82% in 2023 , highlighting the need for efficient downstream processing equipment. Furthermore, advancements in filtration media and automation have enhanced throughput and reduced manual intervention, making these centrifuges attractive for continuous operation environments.

COUNTRY-LEVEL ANALYSIS

Germany spearheaded the Europe industrial centrifuge market by accounting for 24.8% of total regional revenue in 2024. The country’s prominence is underpinned by its strong industrial base, particularly in chemical processing, pharmaceuticals, and mechanical engineering, all of which rely heavily on centrifugal separation technologies. According to the German Mechanical Engineering Industry Association (VDMA), over 80% of industrial firms engaged in chemical and pharmaceutical production in 2023 utilized centrifuges for purification and filtration purposes, emphasizing the critical role of these machines in maintaining product quality and operational efficiency. The country is also home to leading centrifuge manufacturers such as GEA Group and Flottweg, which supply both domestic and international markets. Additionally, Germany's commitment to environmental sustainability has spurred investment in advanced wastewater treatment infrastructure.

The United Kingdom saw strong demand amid regulatory shifts in 2024. Despite post-Brexit trade adjustments, the UK remains a major consumer of industrial centrifuge technology due to its well-developed pharmaceutical, food processing, and wastewater treatment sectors. The food and beverage industry also plays a crucial role, with British dairy and brewing companies adopting advanced disc stack centrifuges for product clarification and yeast separation. Post-Brexit regulatory divergence has prompted some firms to invest in dual-certified centrifuge systems to ensure compliance with both UKCA and CE marking standards. With ongoing investments in sustainable water management and life sciences innovation, the UK maintains a robust presence in the European centrifuge market.

France occupies a notable position in the Europe industrial centrifuge market. The country’s market dynamics are shaped by stringent regulatory enforcement, a strong presence of multinational corporations, and increasing focus on sustainability and process efficiency. Moreover, its is also a hub for nuclear energy and biotechnology research, where centrifuges play a vital role in uranium enrichment and cell culture applications. The expansion of renewable energy projects has further influenced centrifuge demand, particularly in biodiesel refining and fermentation residue management. Besides, France’s food processing industry, especially in wine and dairy, relies on high-efficiency centrifuges for clarification and stabilization.

Italy commanded an eye-catching portion of the Europe industrial centrifuge market share in 2024, supported by its vibrant manufacturing sector, growing exports, and increasing emphasis on product quality and environmental compliance. The country’s industrial landscape, particularly in machinery, food processing, and textile dyeing, drives consistent demand for centrifugal separation solutions. Also, the textile industry, concentrated in regions like Lombardy and Veneto, has been particularly active in seeking centrifuges for dye removal and wastewater treatment. The pharmaceutical sector remains another key contributor, with companies such as Alfa Wassermann and Chiesi expanding their biopharmaceutical production capacities. These developments have led to increased procurement of high-speed tubular bowl centrifuges for protein purification and vaccine formulation.

Spain is increasing urbanization and infrastructure development, driving demand which is supported by rising urbanization, infrastructure modernization, and growing awareness of product safety and process efficiency. The country’s economic recovery post-pandemic has spurred investments in transportation, energy, and real estate, all of which rely on extensive centrifuge usage for fluid separation and waste treatment. In addition, the expansion of renewable energy projects, particularly in bioethanol and biodiesel production, has led to increased deployment of centrifuges for biomass dewatering and lipid extraction. The food and beverage industry remains a key user of centrifuges, with Spanish exporters seeking certifications such as BRCGS to ensure compliance with EU and international food safety regulations. Major companies like Mahou San Miguel and Freixenet have incorporated centrifugal clarification into their production workflows. Additionally, the tourism-driven hospitality sector has adopted advanced water treatment systems utilizing centrifugal dewatering to comply with new environmental mandates.

COMPETITIVE LANDSCAPE

The competition in the Europe industrial centrifuge market is characterized by a mix of well-established global leaders and regionally focused manufacturers striving to differentiate themselves through technological innovation, customization, and service excellence. While multinational corporations like GEA Group, Alfa Laval, and Flottweg dominate due to their extensive product lines and engineering expertise, several mid-sized European firms compete effectively by offering specialized solutions tailored to niche applications. The market remains fragmented, with intense rivalry observed particularly in Germany, Sweden, and Italy, where demand for high-performance separation equipment is consistently strong.

A defining feature of this competitive environment is the increasing emphasis on digital transformation, as companies race to integrate smart monitoring, predictive analytics, and remote diagnostics into centrifuge operations. Additionally, growing regulatory pressure around environmental compliance and resource recovery is compelling manufacturers to innovate in areas such as energy efficiency and waste minimization. To maintain relevance and growth, market participants are actively engaging in strategic acquisitions, forming industry partnerships, and investing in R&D to stay ahead of evolving industrial demands. As the need for precise, scalable, and sustainable separation processes expands across sectors, competition is expected to intensify further, driving greater specialization and value addition within the European industrial centrifuge landscape.

KEY MARKET PLAYERS

Companies playing a prominent role in the European industrial centrifuges market profiled in this report are

- Alfa Laval AB

- GEA Group AG

- HAUS Centrifuge Technologies

- Andritz AG

- Flottweg SE

TOP LEADING PLAYERS IN THE MARKET

- GEA Group is a leading global technology provider in the field of industrial centrifuges, with a strong footprint in Europe and beyond. The company offers a comprehensive range of sedimentation and filtration centrifuges tailored for applications in food processing, pharmaceuticals, chemicals, and wastewater treatment. Known for its engineering excellence and innovation, GEA plays a pivotal role in shaping industry standards through advanced separation technologies. Its commitment to sustainability and digitalization has positioned it as a preferred partner for large-scale industrial clients seeking efficient and eco-friendly solutions.

- Alfa Laval is a globally recognized leader in heat transfer, separation, and fluid handling technologies, including a diverse portfolio of industrial centrifuges. With a strong presence in Europe, the company serves key sectors such as dairy, beverage, marine, and biotechnology. Alfa Laval's centrifuge systems are renowned for their reliability, high performance, and adaptability to complex process conditions. The company continues to drive technological advancements, particularly in energy-efficient and automated centrifugation solutions, contributing significantly to both regional and global market development.

- Flottweg is a specialist in centrifuge technology and one of Europe’s most respected manufacturers of decanter, disc stack, and separator centrifuges. The company is known for its custom-engineered solutions that cater to demanding applications in wastewater treatment, chemical processing, food production, and energy. Flottweg emphasizes precision engineering, durability, and process optimization, making it a trusted name among industrial operators across Europe. Its continuous investment in R&D ensures that it remains at the forefront of innovation in the industrial centrifuge sector.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Leading companies in the Europe industrial centrifuge market are heavily investing in research and development to introduce next-generation centrifuge systems that incorporate smart automation, predictive maintenance, and enhanced energy efficiency. By integrating IoT-enabled sensors and real-time monitoring capabilities, manufacturers aim to improve operational transparency and reduce downtime, meeting the evolving needs of industries such as pharmaceuticals, food processing, and renewable energy.

To strengthen their product portfolios and geographic reach, major players are acquiring niche centrifuge specialists and forming strategic alliances with process engineering firms. These moves allow companies to access new markets, diversify offerings, and enhance technical expertise without the need for extensive internal development, thereby accelerating time-to-market and reinforcing competitive positioning.

Industrial centrifuge buyers often require highly specialized configurations based on specific process requirements. In response, key participants are offering tailored solutions along with comprehensive after-sales support, including remote diagnostics, preventive maintenance contracts, and operator training programs. This approach not only enhances customer satisfaction but also fosters long-term client relationships and brand loyalty.

RECENT MARKET DEVELOPMENTS

- In March 2024, GEA Group launched a new line of digitally integrated centrifuges designed for the pharmaceutical and fine chemical sectors, featuring real-time process monitoring and adaptive control systems aimed at improving batch consistency and reducing energy consumption.

- In May 2024, Alfa Laval acquired a Danish manufacturer specializing in compact centrifugal separators for the food and beverage industry, enhancing its ability to serve small and medium-scale processors with modular and hygienic design-compliant equipment.

- In February 2024, Flottweg introduced an AI-driven predictive maintenance solution for its decanter centrifuge series, enabling operators to anticipate wear patterns and schedule servicing proactively, thereby minimizing unplanned downtime in critical applications.

- In August 2023, Andritz AG expanded its centrifuge manufacturing facility in Austria to accommodate rising demand from the biofuels and wastewater sectors, ensuring faster delivery times and localized customization for European clients.

- In October 2023, Kusters Zech GmbH, a German centrifuge manufacturer, partnered with a Swiss automation firm to develop fully autonomous centrifuge lines for continuous operation environments in chemical and biopharmaceutical production facilities.

MARKET SEGMENTATION

This Europe industrial centrifuges market research report is segmented and sub-segmented into the following categories.

By Type

- Sedimentation

- Filtering

By Design

- Horizontal Centrifuge

- Vertical Centrifuge

By Operation Mode

- Batch

- Continuous

By Industry

- Food and Beverage

- Pharmaceutical

- Water and Wastewater Treatment

- Chemical

- Metal and Mining

- Power

- Pulp and Paper

- Other Industries

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com