Europe Infant Incubator Market Size, Share, Trends & Growth Forecast Report By Product, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Europe Infant Incubator Market Size

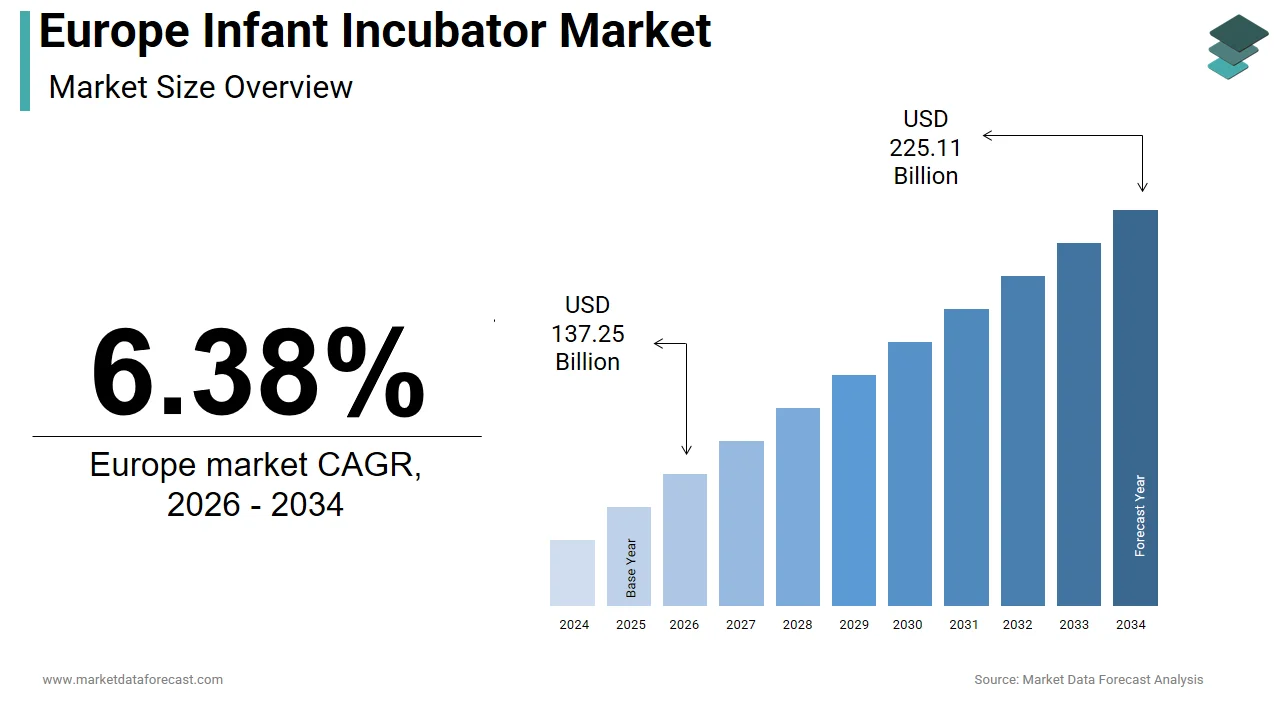

The size of the Europe infant incubator market was valued at USD 129.02 million in 2025. This market is expected to grow at a CAGR of 6.38% from 2026 to 2034 and be worth USD 225.11 million by 2034 from USD 137.25 million in 2026.

Infant incubators are specialized medical devices designed to provide a controlled thermal, humidified, and protected environment for premature and critically ill newborns, particularly those with low birth weight or underdeveloped organ systems. In Europe, these life-sustaining systems are integral to neonatal intensive care units and are subject to stringent regulatory oversight under the European Union Medical Device Regulation. The clinical necessity of incubators is underscored by persistent rates of preterm birth across the region. According to the World Health Organization’s European Regional Office, approximately 500,000 infants are born preterm each year in the European Union, which represents nearly 7% of all live births. Furthermore, according to Eurostat, 6.8% of newborns in the EU weigh less than 2500 grams at birth, which is a key criterion for incubator admission. These demographic and clinical realities establish a continuous and non-discretionary demand for advanced neonatal care infrastructure, positioning infant incubators not as elective equipment but as essential components of perinatal survival protocols across both urban and rural healthcare settings.

MARKET DRIVERS

Persistent Preterm Birth Rates Sustain Clinical Need for Advanced Neonatal Support

Preterm birth remains a leading cause of neonatal morbidity and mortality in Europe, which is creating an enduring requirement for high acuity infant incubators equipped with precise environmental control, and is one of the major factors propelling the European infant incubator market growth. As per the European Perinatal Health Report published in 2024 by the Euro-Peristat network, the preterm birth rate across 25 EU countries averaged 7.1% with countries like Greece and Portugal exceeding 8%. Infants born before 37 weeks of gestation lack sufficient subcutaneous fat and thermoregulatory capacity, which requires immediate placement in servo-controlled incubators. According to the European Society for Neonatology, the vast majority of neonates weighing less than 1,500 grams at birth require incubator care for an extended period. This clinical imperative is further amplified by rising maternal age. According to Eurostat, 22% of births in the EU in 2023 were to women aged 35 or older, which is a demographic associated with higher preterm risk. Consequently, even in high-income nations with advanced obstetric care, the biological vulnerability of preterm infants ensures consistent and non-negotiable demand for reliable, technologically advanced incubation systems.

Modernization of Neonatal Intensive Care Infrastructure Across Public Hospitals

European healthcare systems are undergoing systematic upgrades of neonatal care units to align with evolving standards of care and digital health integration, which is directly stimulating demand for next-generation incubators and is further contributing to the regional market expansion. The European Commission’s 2023 Hospital Infrastructure Modernization Fund allocated over 2.3 billion euros to renovate critical care facilities in member states, with neonatal units prioritized in countries like Romania, Bulgaria, and Italy. In Germany, the Federal Ministry of Health mandated in 2024 that all level three NICUs must replace incubators older than ten years with models featuring integrated monitoring and data export capabilities. Similarly, France’s National Health Agency requires all public maternity hospitals to adopt incubators compliant with the latest IEC 60601-2-19 safety standard by 2026. These policy-driven renewal cycles are reinforced by hospital accreditation frameworks. According to the European Association of Hospital Managers, a majority of tertiary maternity hospitals in Western Europe have active capital budgets dedicated to neonatal equipment replacement. This institutional commitment to infrastructure quality ensures sustained procurement momentum beyond new birth volumes.

MARKET RESTRAINTS

High Capital Cost and Budget Constraints in Public Health Systems Limit Procurement Flexibility

Despite clinical necessity, the acquisition of advanced infant incubators faces significant financial barriers due to their high upfront cost and competing budget priorities within publicly funded healthcare systems, which is a key restraint for the European infant incubator market. A modern servo-controlled incubator with integrated monitoring and remote access capabilities can cost between 30,000 and 50,000 euros per unit as per pricing data from hospital procurement tenders in 2024. In Southern and Eastern European countries, fiscal austerity continues to constrain medical equipment budgets, with public health expenditure in Italy and Spain still facing long-term financial pressures. Consequently, many hospitals operate incubators beyond their recommended service life, which increases maintenance costs and downtime. According to Romania’s Ministry of Health, a significant share of NICU incubators in public hospitals were more than 12 years old in 2024, which is failing to meet current safety and performance benchmarks. This financial pressure delays adoption of energy-efficient, digitally enabled models and perpetuates reliance on outdated technology, which is undermining optimal neonatal outcomes.

Stringent Regulatory Requirements Prolong Certification and Market Entry Timelines

The European Union Medical Device Regulation imposes rigorous clinical evidence and post-market surveillance obligations that significantly extend the time required to introduce new infant incubator models to the market, which is further hindering the growth of the European market. As per the European Commission, the average conformity assessment process for Class IIb medical devices such as infant incubators now exceeds 14 months, which is up from 8 months under the former Medical Devices Directive. Notified bodies responsible for certification remain limited in capacity, with backlogs for technical documentation review extending several months. These delays are particularly burdensome for small and medium-sized manufacturers seeking to deploy innovations like low-noise airflow systems or AI-assisted environmental optimization. Furthermore, each software update or hardware modification triggers a new conformity assessment, which discourages iterative improvements. This regulatory friction slows the availability of clinically superior incubators, especially in emerging EU markets where access to cutting-edge neonatal technology is already limited.

MARKET OPPORTUNITIES

Integration of Smart Monitoring and Tele Neonatology Capabilities

The convergence of medical device connectivity and remote care delivery is unlocking promising opportunities for the European infant incubator market. As per the European Health Management Association, many level two and three NICUs in Germany, the Netherlands, and Sweden have implemented digital neonatal dashboards that aggregate data from incubators, ventilators, and monitors into unified clinical workflows. These systems enable early detection of physiological instability and facilitate specialist consultation across regions, which is a critical advantage in rural areas with limited neonatologist coverage. The European Commission’s Digital Europe Programme includes funding to expand telemedicine infrastructure in maternal and child health, which is directly incentivizing the adoption of incubators with HL7 and FHIR-compliant data interfaces. Companies like Dräger and GE Healthcare have responded with incubators featuring embedded sensors that continuously track infant temperature, humidity, and oxygen exposure, which transmit alerts to clinician smartphones. This shift transforms the incubator from a passive enclosure into an active diagnostic and communication node within integrated neonatal care ecosystems.

Expansion of Regional Perinatal Networks to Improve Access in Underserved Areas

Europe is actively restructuring neonatal care through the establishment of regional perinatal networks that centralize high-risk deliveries and expand access to advanced incubation in peripheral settings, which is another notable opportunity for the European infant incubator market. As per the European Reference Network for Rare Diseases with Neonatal Onset, many EU countries have implemented formal perinatal network strategies that include standardized equipment protocols for transport and satellite units. In Poland, the National Perinatal Program, launched in 2023, mandated the deployment of mobile incubation units and transport incubators to district hospitals, which ensures preterm infants can be stabilized before transfer to level three centers. Similarly, the UK’s NHS Long Term Plan requires birthing units to maintain modern incubators, which recognizes that a substantial share of preterm births occur in low-risk settings. These systemic reforms create new demand streams for compact, portable, and ruggedized incubators designed for community hospitals and ambulance services, which are opening avenues for manufacturers offering specialized transport and point-of-care models aligned with decentralized care strategies.

MARKET CHALLENGES

Shortage of Trained Neonatal Staff Impedes Optimal Utilization of Advanced Incubators

The effective operation of modern infant incubators requires specialized training in thermal management, infection control, and integrated monitoring, which are skills increasingly scarce due to a shortage of qualified neonatal nurses and technicians across Europe, and this is one of the major challenges to the European infant incubator market. According to the European Federation of Nurses Associations, the EU faces a significant deficit of specialized nursing staff by 2030, with neonatal units among the hardest hit. In Italy, according to the National Neonatal Network, in 2024 that many NICUs operate below recommended nurse-to-infant ratios, which is leading to delayed responses to incubator alarms and suboptimal environmental adjustments. This human resource gap is particularly acute in Eastern Europe. As per Romania’s College of Nurses, certified neonatal nursing capacity remains limited nationwide. Consequently, even when advanced incubators are procured, their full functionality often remains underutilized. This mismatch between technological capability and workforce competence not only compromises infant outcomes but also reduces the perceived return on investment for high-end incubator procurement.

Lack of Standardized Maintenance and Calibration Protocols Across Countries

The performance and safety of infant incubators depend on regular calibration and preventive maintenance, yet Europe lacks harmonized protocols for servicing this critical equipment, which is leading to variable reliability and safety risks and is further challenging the regional market expansion. As per a 2024 audit by the European Society for Paediatric Research, many EU member states lack national guidelines for incubator calibration frequency, and intervals vary widely between countries. This inconsistency can contribute to performance drift. According to sources, incubators are failing to maintain target temperatures during routine checks. Moreover, spare parts availability is fragmented as manufacturers often discontinue support for older models, leaving hospitals in lower-income countries with non-functional units. Without EU-wide standards for maintenance, training, and parts logistics, the clinical efficacy of incubators remains uneven, which is undermining the goal of equitable neonatal care across the region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | GE Healthcare, Drägerwerk AG, Novos Medical Systems, Atom Medical Corporation, Ningbo David Medical Device Co., Ltd, Natus Medical Incorporated, Fanem Ltd, Cobams SRL, AVI Healthcare Private Limited, Gammer International, and Ardo. |

SEGMENTAL ANALYSIS

By Product Insights

The neonatal intensive care unit (NICU) incubator segment dominated the Europe infant incubator market, holding the largest share of the European market in 2024. The dominance of the NICU incubator segment is driven by its critical role as the primary life support system for preterm and critically ill newborns in hospital settings. Unlike transport units used episodically, NICU incubators serve as long-controlled environments in level two and three neonatal facilities across the continent. NICU incubators are indispensable in Europe’s network of specialized perinatal centers, where they support the majority of preterm and low birth weight infants requiring extended thermal and respiratory stabilization. According to the European Perinatal Health Report 2024, a large majority of infants born before 32 weeks of gestation are admitted directly to NICUs equipped with servo-controlled incubators. Germany operates a substantial number of level three NICUs, with each maintaining multiple incubators in continuous use. The European Society for Paediatric Research emphasizes that stable thermal regulation in the first 72 hours reduces mortality in very low birth weight infants. Given that the EU records approximately 500,000 preterm births annually as per the World Health Organization’s European Office, the clinical necessity for high acuity, stationary incubation remains non-negotiable and structurally embedded in neonatal care pathways.

The transport infant incubator segment is projected to grow at a promising CAGR of 8.84% over the forecast period, owing to the expansion of regional perinatal networks and the need for safe interfacility transfers of critically ill newborns. European health systems are increasingly adopting hub and spoke perinatal networks that centralize high-risk deliveries in level three centers while stabilizing infants at local hospitals before transfer. As per the European Reference Network for Neonatal and Pediatric Intensive Care, many EU countries have formalized transport protocols requiring mobile incubators for preterm transfers under 32 weeks. In Poland, the National Perinatal Program 2023 to 2027 funded the deployment of transport incubators to district hospitals, which ensures preterm infants can be stabilized before transfer to level three centers. Similarly, Italy’s Ministry of Health reported in 2024 that multiple regions now mandate transport incubators with extended battery autonomy and integrated monitoring. These systemic reforms transform transport incubators from optional accessories into essential components of equitable neonatal care, particularly in geographically dispersed regions like Scandinavia and the Balkans.

By Application Insights

The lower birth weight segment accounted for the largest share of the Europe infant incubator market in 2024, as infants weighing less than 2500 grams at birth universally require external thermal support due to underdeveloped thermoregulatory systems. This category includes both preterm and small for gestational age term infants, which creates a broad and consistent clinical indication for incubator use. Low birth weight remains a persistent public health indicator across Europe with significant variation but universal clinical implications. According to Eurostat, 6.8% of all live births in the European Union in 2023 were classified as low birth weight, which translates to roughly 250,000 infants annually. Southern and Eastern European countries report higher rates driven by socioeconomic and maternal health factors. The World Health Organization’s European Office confirms that infants below 2,500 grams face a substantially higher risk of neonatal death without thermal support, making incubator admission standard protocol. Furthermore, even late preterm infants (34 to 36 weeks) often fall into this weight category and require short-term incubation for stabilization. This demographic reality ensures that low birth weight remains the primary and most predictable driver of incubator utilization across urban and rural maternity units alike.

The neonatal hypothermia segment is estimated to record a CAGR of 8.78% over the forecast period in the European market, owing to the clinical awareness, screening mandates, and therapeutic innovation in temperature management. Neonatal hypothermia is now recognized as a critical and preventable contributor to morbidity, which is prompting systematic screening at birth across Europe. Many EU countries have integrated auxiliary temperature checks into the first minutes of life as part of national delivery room protocols. Delays can be severe as lower admission temperatures in preterm infants are associated with increased risks of sepsis and mortality. In response, countries like Sweden and the Netherlands have implemented “warm chain” initiatives that include immediate placement in prewarmed incubators for any infant showing signs of thermal instability, regardless of gestational age. This proactive stance transforms incubator use from a reactive to a preventive measure, which is broadening its application beyond traditional preterm indications.

COUNTRY LEVEL ANALYSIS

Germany Infant Incubator Market Analysis

Germany led the infant incubator market in Europe in 2024 by accounting for 22.8% of the regional market share. The growth of Germany in the European market is attributed to its dense network of high-level neonatal intensive care units and robust public investment in perinatal infrastructure. Germany operates 43 level three NICUs as part of the German Neonatal Network, each equipped with advanced incubators. Germany’s federal health policy emphasizes early intervention for preterm infants, with premature births accounting for around 8–9% of all births nationally. The Federal Ministry of Health, through the Hospital Future Act, has committed more than four billion euros to the digitization and modernization of hospital infrastructure, including neonatal care. Additionally, Germany’s aging obstetric workforce has accelerated automation investments, which are favoring smart incubators that reduce manual monitoring burden. These structural, policy, and demographic factors consolidate Germany’s status as Europe’s largest and most technologically advanced neonatal care market.

France Infant Incubator Market Analysis

France is projected to witness a promising CAGR in the European infant incubator market over the forecast period, owing to the centralized perinatal planning and universal access to high-quality maternity care. France maintains a nationally coordinated network of 320 maternities classified by neonatal care level, ensuring that even rural regions have access to incubator-equipped units. According to the French National Institute of Health Data, 7.4% of births in 2023 were preterm, generating consistent demand for both NICU and transport incubators. The 2024 National Perinatal Plan mandates that all level one maternity units must maintain at least two modern incubators for stabilization before transfer. Moreover, France leads in therapeutic hypothermia adoption, with a majority of eligible term infants receiving cooling therapy in certified centers. This combination of geographic equity, clinical protocol standardization, and investment in neuroprotective care sustains France’s strong market position.

United Kingdom Infant Incubator Market Analysis

The United Kingdom is predicted to command a prominent share of the European infant incubator market during the forecast period, owing to the National Health Service’s standardized neonatal critical care framework and high preterm birth rates in urban centers. The NHS Neonatal Critical Care Transformation Programme requires all neonatal networks to maintain minimum equipment standards, including incubators with integrated monitoring for all intensive care cots. According to the Office for National Statistics, 7.8% of UK births in 2023 were preterm. The NHS Long Term Plan also prioritized reducing neonatal mortality through early thermal stabilization, which is leading to the rollout of pre-warmed incubator protocols across maternity units. Additionally, the UK is a pioneer in tele-neonatology, with many district hospitals now using incubators linked to regional specialist centers for remote consultation. These systemic and technological initiatives ensure continued demand for advanced incubation solutions across public healthcare settings.

Italy Infant Incubator Market Analysis

Italy is expected to account for a considerable share of the European market over the forecast period, owing to the regional disparities and recent national efforts to standardize neonatal care. While northern regions like Lombardy and Emilia Romagna operate world-class NICUs, southern areas historically faced equipment shortages. The 2023 National Recovery and Resilience Plan allocated significant funding to reduce this gap, supporting new NICU incubators and transport units for underserved provinces. Italy’s preterm birth rate stands at 7.6% as per ISTAT, with over 45,000 infants annually requiring thermal support. The Italian Society of Neonatology launched the “Warm Start” initiative in 2024 to ensure immediate incubator access in all birthing rooms, regardless of facility level. These reforms, combined with EU cohesion funds targeting healthcare modernization, are driving rapid market expansion in previously lagging regions and creating a more unified national demand profile.

Spain Infant Incubator Market Analysis

Spain is also a prominent market for infant incubators in Europe. The universal healthcare coverage, a growing focus on maternal health, and the expansion of regional perinatal networks are a few factors contributing to the Spanish market growth. Spain’s preterm birth rate of 7.1% in 2023, as reported by the National Statistics Institute, translates to over 30,000 infants needing incubator care annually. The Ministry of Health’s 2024 Neonatal Equity Strategy mandates that all 225 public maternity hospitals maintain at least one modern incubator and establish transfer agreements with level three centers. Additionally, Spain is integrating incubators into its national telemedicine platform, allowing real-time data sharing between rural birthing units and urban NICUs. Catalonia and Andalusia have piloted AI-assisted incubators that predict thermal instability, reducing nurse workload. These digital health initiatives, coupled with consistent public funding, position Spain as a stable and evolving market within the European landscape.

COMPETITIVE LANDSCAPE

The Europe Infant Incubator Market is characterized by competition among established global innovators and specialized regional manufacturers vying for influence through clinical efficacy, regulatory adherence, and service excellence. Incumbents like Dräger and GE Healthcare leverage deep hospital relationships and integrated care ecosystems while newer entrants compete on cost efficiency and rapid regulatory compliance. The enforcement of the EU Medical Device Regulation has raised technical and documentation barriers, favoring companies with mature quality management systems. Public procurement processes further intensify competition as national and regional tenders emphasize lifecycle cost over initial price. Differentiation increasingly hinges on digital capabilities such as data interoperability, remote diagnostics, and AI-assisted environmental control. Meanwhile, transport incubator innovation is opening opportunities for agile firms offering ruggedized portable solutions aligned with decentralized perinatal networks. This multifaceted competitive landscape rewards both technological leadership and operational responsiveness.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe infant incubator market include

- GE Healthcare

- Drägerwerk AG

- Novos Medical Systems

- Atom Medical Corporation

- Ningbo David Medical Device Co., Ltd

- Natus Medical Incorporated

- Fanem Ltd

- Cobams SRL

- AVI Healthcare Private Limited

- Gammer International

- Ardo

TOP PLAYERS IN THE MARKET

- Drägerwerk AG is a German-based global leader in medical and safety technology with a longstanding presence in the Europe Infant Incubator Market. The company designs and manufactures advanced NICU and transport incubators known for precision thermal control, low noise operation, and integrated monitoring capabilities. Dräger’s products are widely used in level two and three neonatal units across Germany, France, and Scandinavia. In 2024, the company enhanced its BabyLux incubator series with real-time humidity feedback and wireless data transmission compliant with European Hospital Federation interoperability standards. It also partnered with several European university hospitals to develop AI-driven thermal instability prediction algorithms, reinforcing its reputation for clinical innovation and regulatory compliance in high acuity neonatal care.

- GE Healthcare is a major global provider of neonatal care solutions with a robust footprint in the Europe Infant Incubator Market. The company offers a comprehensive portfolio, including the Giraffe and Panda lines of incubators and warmers tailored for both NICU and transport settings. GE Healthcare leverages its global R&D network to integrate advanced features such as therapeutic hypothermia support and remote diagnostics into its European offerings. In early 2024, the company received CE certification for its updated Giraffe OmniBed Carestation featuring enhanced infection control surfaces and reduced power consumption. It also expanded its service network across Southern and Eastern Europe to ensure rapid maintenance and calibration, addressing a key operational challenge in public hospital systems.

- Atom Medical Corporation is a Japanese multinational with growing influence in the Europe Infant Incubator Market through its high reliability and cost-effective neonatal care devices. The company supplies compact NICU and transport incubators that meet stringent European safety and performance standards while offering lower total cost of ownership. Atom’s products are particularly popular in mid-tier hospitals and emerging EU markets seeking modern yet affordable solutions. In 2024, the company launched its upgraded C2000 Neo incubator across the UK, Spain, and Poland, featuring extended battery life for transport and intuitive touchscreen controls. It also achieved full compliance with the EU Medical Device Regulation ahead of schedule, demonstrating its commitment to regulatory diligence and long-term market access in Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Infant Incubator Market focus on regulatory compliance, clinical integration, and service reliability to maintain a competitive advantage. Companies prioritize full alignment with the European Union Medical Device Regulation through rigorous documentation and post-market surveillance. They invest in smart features such as remote monitoring, predictive analytics, and therapeutic hypothermia support to meet evolving clinical standards. Strategic partnerships with academic hospitals enable real-world validation and rapid feedback for product refinement. Expansion of local service and calibration networks addresses maintenance challenges in public health systems. Additionally, firms develop energy-efficient and infection-resistant designs to support sustainability and patient safety goals in European NICUs.

MARKET SEGMENTATION

This Europe infant incubator market research report is segmented and sub-segmented into the following categories.

By Product

- Transport Infant Incubator

- Neonatal Intensive Care Unit (NICU) Incubator

By Application

- Neonatal Hypothermia

- Lower Birth Weight

- Genetic Defects

- Others

By End User

- Birthing Centers

- Neonatal Intensive Care Units

- Pediatric Hospitals

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the current size of the Europe infant incubator market?

The Europe infant incubator market was valued at approximately USD 137.25 million in 2026 reflecting growth in NICU installations and neonatal care awareness

2. What is the growth forecast for the Europe infant incubator market?

The Europe infant incubator market is projected to grow at a CAGR of 6.38% from 2026 to 2034, reaching around USD 225.11 million due to rising premature births

3. Which countries lead the Europe infant incubator market?

Germany, France, Italy, and the UK dominate the Europe infant incubator market with advanced neonatal care infrastructure and high NICU coverage

4. What drives demand in the Europe infant incubator market?

Increasing premature births, advancements in neonatal technology, and rising healthcare investments boost the Europe infant incubator market growth

5. How do NICU installations affect the Europe infant incubator market?

The rise in NICU units with advanced incubators drives demand in the Europe infant incubator market to improve newborn survival

6. What role do technological innovations play in the Europe infant incubator market?

Smart temperature control, oxygen therapy integration, and AI-based monitoring enhance the Europe infant incubator market offerings

7. What challenges does the Europe infant incubator market face?

High costs and alternatives like baby warmers, along with limited access in some regions, constrain the Europe infant incubator market growth

8. How is premature birth rate influencing the Europe infant incubator market?

Rising premature births across Europe notably increase demand in the Europe infant incubator market for specialized infant care

9. What are the common applications in the Europe infant incubator market?

Neonatal intensive care, respiratory support, and infant warming are major applications driving the Europe infant incubator market

10. How important is regulatory compliance in the Europe infant incubator market?

Strict EU medical device regulations ensure safety, driving product innovation and growth in the Europe infant incubator market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com