Europe Intraocular Lens Market Size, Share, Trends & Growth Forecast Report By Material (Polymethylmethacrylate (PMMA), Silicone, Hydrophobic Acrylic), Type, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Intraocular Lens Market Size

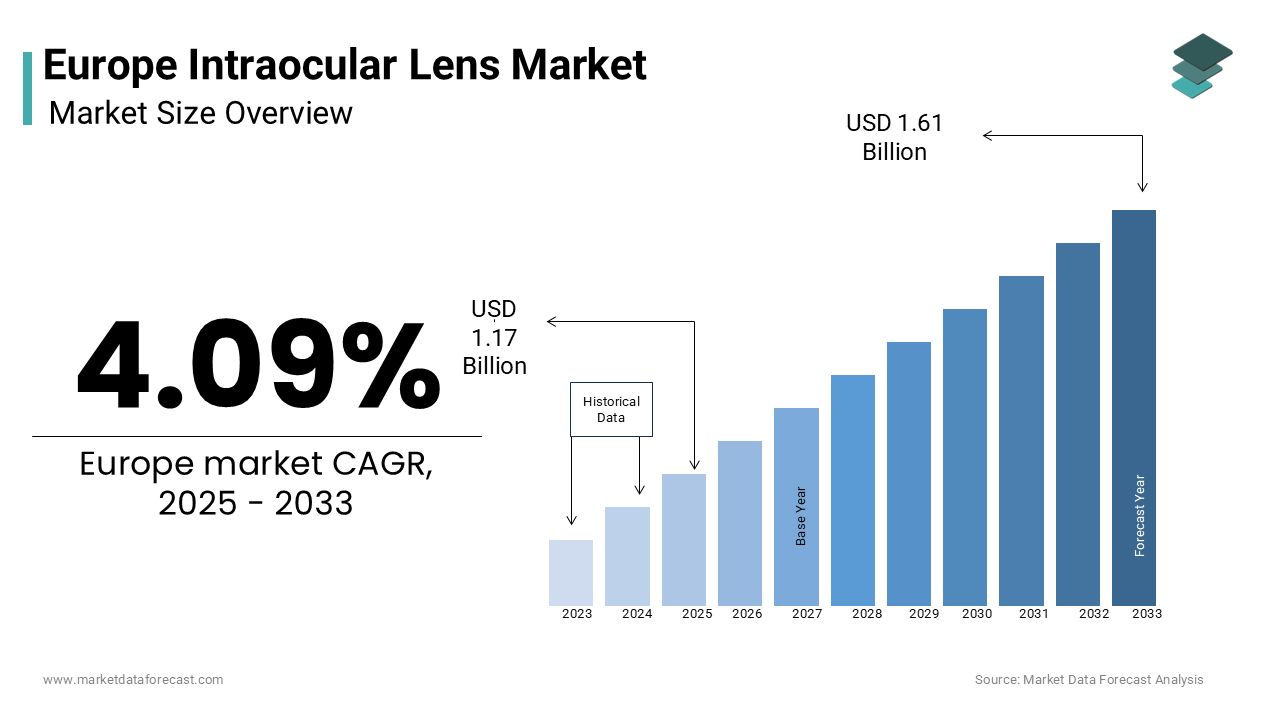

The intraocular lens market size in Europe was valued at USD 1.17 billion in 2025. The European market is estimated to be valued at USD 1.22 billion in 2026 and USD 1.61 billion by 2034, forecasted to grow at a steady CAGR of 4.09% between 2026 to 2034.

The intraocular lens are artificial lenses implanted during cataract extraction or refractive lens exchange procedures, across European countries. These medical devices restore visual acuity by replacing the eye's natural crystalline lens when compromised by opacity or refractive error. The demographic trajectory underpinning this clinical activity is profound. Eurostat data indicates that 21.6% of Europeans were aged 65 years or older in 2024, a proportion projected to reach 29% by 2050. This aging cohort inherently elevates the prevalence of age related cataracts, which account for approximately 51% of global blindness cases according to World Health Organization assessments. Furthermore, as per Eurostat statistics, only 6.4% of cataract surgery patients across the EU required overnight hospital admission in 2023, with the majority treated as day patients or outpatients.

MARKET DRIVERS

Aging Population And Rising Cataract Burden Drive Procedural Volume

The demographic transformation is levelling up the growth of the Europe intraocular lens market. According to Eurostat, the median age in the European Union reached 44.7 years in 2024, with the population aged 65 and above comprising 21.6% of the total. This aging trajectory mechanically expands the pool of individuals susceptible to age related cataracts, the predominant indication for intraocular lens implantation. As per Eurostat surgical statistics, cataract procedures increased in all 26 European countries with available data between 2013 and 2023, with Croatia, Lithuania, Poland and Portugal reporting frequency increases of 1.6 to 2.0 times over the decade. As per World Health Organization estimates, cataracts account for 51% of blindness worldwide, creating sustained pressure on European healthcare systems to maintain surgical capacity. The rebound in procedural volumes following pandemic related backlogs further underscores latent demand. Eurostat recorded 4.73 million cataract surgeries in the EU during 2022, recovering toward pre pandemic levels.

Premium Lens Adoption Accelerates Driven By Patient Expectations And Clinical Outcomes

The growing patient demand for spectacle independence and enhanced visual quality fuels adoption of premium designs is additionally promoting the growth of the Europe intraocular lens market. Multifocal and extended depth of focus platforms address presbyopia concerns by attracting younger refractive lens exchange candidates. Johnson and Johnson Vision's TECNIS Odyssey platform that launched across Europe in 2025, targets dysphotopsia reduction to broaden candidacy for premium optics. Germany's supplemental insurance ecosystem and Spain's competitive medical tourism infrastructure create early adoption pockets for advanced designs. This demographic exhibits higher willingness to self-fund premium options, decoupling adoption from public reimbursement constraints.

MARKET RESTRAINTS

High Cost Of Premium Intraocular Lenses Constrains Broad Patient Access

The substantial out of pocket expenditure required for premium intraocular lenses is hampering the growth of the Europe intraocular lens market. VAT disparities across jurisdictions compound access inequities, with 0% rates in the United Kingdom contrasting with 23% in Portugal by creating potential for cross border arbitrage and market fragmentation. The multifocal intraocular lens procedures are not comprehensively covered under most European insurance policies by requiring patients to sign private pay agreements that introduce friction into the adoption pathway. Manufacturers face a strategic dilemma, while reducing prices to widen access may compromise research and development funding for next generation optics, while maintaining premium pricing perpetuates socioeconomic disparities in visual outcomes. Health technology assessment agencies across Europe increasingly demand real world effectiveness data to justify reimbursement expansions, yet the self pay model for premium lenses generates limited post market evidence, creating a circular constraint on broader adoption.

Reimbursement Limitations Restrict Advanced Technology Adoption Across Public Systems

The public reimbursement frameworks, predominantly cover only basic monofocal intraocular lenses by creating a structural restraint on premium technology diffusion. This factor is attributed in hampering the growth of the Europe intraocular lens market. French, German and United Kingdom payers classify toric and multifocal lenses as discretionary upgrades requiring patient co-payment by limiting adoption to affluent urban cohorts with supplemental insurance or self-pay capacity. England clinical commissioning policy documentation, advanced technology intraocular lenses are not routinely funded within the National Health Service, placing the financial burden directly on patients seeking enhanced visual outcomes. Health technology assessment bodies, such as Germany's Institute for Quality and Efficiency in Health Care. This evidentiary requirement perpetuates a cycle, wherein limited reimbursement restricts patient access, which in turn constrains the generation of post effectiveness data needed to support broader coverage decisions. This reimbursement gap, particularly impacts Eastern European member states, where public healthcare budgets face greater fiscal pressure, delaying adoption of advanced optics despite rising cataract prevalence. The regulatory complexity introduced by the European Union Medical Device Regulation further elevates post market surveillance obligations, favoring incumbent manufacturers with established quality management systems while raising barriers for emerging innovators seeking market entry with novel optical designs.

MARKET OPPORTUNITIES

Ambulatory Surgery Center Expansion Creates Efficient Procurement Pathways

The rapid proliferation of ambulatory surgery centers to optimize distribution and capture premium product adoption is majorly to promote new opportunities for the growth of the Europe intraocular lens makret. This operational shift reduces procedural costs by up to 40%, freeing capital for investment in premium intraocular lens inventory and advanced surgical equipment. EU structural funds earmarked for outpatient infrastructure development in Poland, Romania and Bulgaria, promise fresh greenfield opportunities for distributors able to supply turnkey ophthalmic suites. Spain's private clinic ecosystem exemplifies this opportunity with competitive package pricing attracting cross border patients from Northern Europe, seeking lower costs and warmer climates for refractive lens exchange procedures. Manufacturers can secure loyalty through service-based contracts that include biometer leasing, staff training and guaranteed consumable deliveries.

Technological Innovation In Optical Materials Enhances Clinical Differentiation

Advances in aspheric optics and blue light filtering materials to demonstrate clinical superiority and command premium pricing is also fuelling the growth of the Europe intraocular lens market. The aspheric lens designs flatten curvature to reduce spherical aberration, thereby sharpening contrast sensitivity for night driving scenarios that matter to active European patients. Embedded chromophores that absorb sub 450 nanometer wavelengths address emerging concerns about retinal phototoxicity from prolonged digital screen exposure. The European Union Medical Device Regulation heightens post evidence requirements, favoring incumbents that maintain robust quality management systems, while creating barriers for low cost entrants lacking clinical data infrastructure. The second generation diffractive optics resolve earlier halo and glare complaints by improving satisfaction rates and widening the candidate pool to exacting younger refractive lens exchange patients. Bundled service contracts that include biometry calibration and surgeon education further differentiate premium offerings in competitive tender environments.

MARKET CHALLENGES

Rural Surgical Capacity Shortages Limit Market Penetration In Eastern Europe

The geographic disparities in ophthalmic workforce distribution, across rural and Eastern European countries is a challenge for the growth of the Europe intraocular lens market. As per Eurostat surgical statistics, Romania performed only 389.4 cataract surgeries per 100000 inhabitants in 2023 compared to Luxembourg's 1627.3, revealing a substantial capacity gap that device manufacturers cannot address through product supply alone. This workforce shortage particularly impacts rural regions where patient travel distances to specialized ophthalmic centers create access barriers. Training pipeline constraints exacerbate the challenge, as per European ophthalmology training assessments noting significant transformation in curricula over two decades yet persistent national variations in specialist output. Public hospital networks in underserved regions often lack capital for advanced phacoemulsification equipment required for premium intraocular lens implantation, further concentrating procedural volume in urban centers. Manufacturers seeking to expand market share in these regions must invest in surgeon education programs, equipment financing partnerships and teleophthalmology support infrastructure, strategies that elevate customer acquisition costs and extend return on investment timelines.

Supply Chain Fragility For Specialized Polymers Introduces Production Risk

Dependence on specialized hydrophobic acrylic polymers for foldable intraocular lens manufacturing introduces supply chain vulnerability is to limit the growth of the Europe intraocular lens market. The hydrophobic acrylic monomers require precise polymerization processes and stringent quality controls to meet European Union Medical Device Regulation requirements by limiting the number of qualified global suppliers. Geopolitical tensions, energy price volatility and transportation disruptions can delay raw material deliveries by forcing manufacturers to maintain elevated inventory levels that increase working capital requirements. Brexit induced certification duality between CE marking and United Kingdom Conformity Assessed status further complicates supply chain logistics for manufacturers serving both European Union and United Kingdom markets. The concentration of polymer production among a limited number of chemical manufacturers creates single point of failure risks, as demonstrated during pandemic related manufacturing shutdowns. Manufacturers must invest in dual sourcing strategies, regional inventory hubs and alternative material qualification programs to mitigate these risks, strategies that elevate operational complexity and cost structures.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.09% |

| Segments Covered | By Material, Type, End-User and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Johnson & Johnson, Valeant, Carl Zeiss Meditec AG, Rayner, Alcon, Inc. (a division of Novartis AG), EyeKon Medical, Inc., Lenstec, Inc., HumanOptics AG, STAAR Surgical, PhysIOL s.a., Calhoun Vision Center, and Oculentis GmBH. |

SEGMENTAL ANALYSIS

By Material Insights

The hydrophobic acrylic material segment was the largest by holding a dominant share of the Europe Intraocular Lens Market in 2025 with its superior biocompatibility and foldability which facilitate minimally invasive surgical procedures. The primary driver for this segment is the material's ability to be inserted through incisions smaller than 2.4 millimeters, which significantly reduces surgically induced astigmatism and accelerates patient recovery times. This clinical advantage drives surgeon preference in high volume ambulatory settings across Germany and France. Furthermore, the material’s stability ensures long term optical performance without significant refractive shift. The production scalability of hydrophobic acrylic polymers allows for cost effective mass production, while maintaining strict quality control standards required by the European Union Medical Device Regulation.

The silicone material segment is esteemed to grow at a fastest CAGR of 7.8% throughout the forecast period owing to the recent advancements in silicone formulation that enhance lens flexibility and reduce the risk of glistenings, which are microscopic fluid filled vacuoles that can scatter light. The increasing utilization of silicone in specific premium applications, such as accommodating intraocular lenses where high elasticity is for mimicking natural lens movement. The newer generation silicone materials exhibit improved haptic design stability, which supports better centration in the capsular bag. This technical improvement appeals to surgeons performing complex refractive lens exchanges in younger presbyopic patients. Additionally, silicone lenses offer excellent transparency and UV protection properties, which align with patient demands for long term retinal health.

By Type Insights

The monofocal segment was the largest by accounting for a dominant share of the Europe Intraocular Lens Market in 2025 with the comprehensive public reimbursement policies across major European healthcare systems, which fully cover the cost of standard monofocal implants. The sheer volume of cataract surgeries performed annually, where cost containment remains a priority for national health services. In countries like the United Kingdom and Sweden, the National Health Service mandates monofocal lenses, as the default option unless patients opt for private payment. This structural reimbursement framework ensures consistent demand regardless of economic fluctuations. Furthermore, monofocal lenses provide reliable distance vision with minimal visual disturbances, such as halos or glare, which makes them suitable for the oldest demographic cohorts, who may have reduced neural adaptation capacity.

The toric segment is likely to grow at a fastest CAGR of 8.5% throughout the forecast period with the high prevalence of corneal astigmatism among cataract patients and the growing clinical emphasis on achieving complete refractive correction. The increasing integration of toric lenses into standard surgical workflows supported by advanced preoperative biometry technologies. The availability of precise digital marking systems and intraoperative guidance tools has reduced the complexity of toric alignment encouraging broader surgeon adoption. The willingness of patients to pay out of pocket for astigmatism correction is rising particularly in Western European nations, where disposable income levels support elective enhancements. Additionally, the launch of extended depth of focus toric combinations offers dual benefits of astigmatism correction and presbyopia management creating a compelling value proposition.

By End User Insights

The hospitals segment was the largest by holding 45.3% of the Europe Intraocular Lens Market share in 2025 with the capacity of large hospital networks to handle high volumes of complex cataract cases, including those with comorbidities, such as glaucoma or diabetic retinopathy. The centralized procurement power of hospital groups, which negotiate bulk purchasing agreements for intraocular lenses by ensuring steady supply chains and standardized clinical protocols. The public hospitals in Germany, France, and Italy, perform the majority of cataract surgeries due to their extensive surgical suites and specialized ophthalmology departments. These institutions benefit from integrated care pathways that allow for seamless management of preoperative diagnostics and postoperative follow up. Furthermore, hospitals serve as training centers for resident surgeons fostering early brand loyalty to specific intraocular lens platforms. The presence of advanced imaging equipment and multidisciplinary teams in hospitals also supports the adoption of premium lenses for complex cases requiring customized solutions.

The ambulatory surgical centers segment is expected to grow at a fastest CAGR of 9.1% throughout the forecast period with the strategic shift toward day case surgery models, which offer significant cost efficiencies and enhanced patient convenience. The favorable reimbursement environment for ambulatory procedures in many European countries, which incentivizes providers to move cataract surgery out of inpatient settings. Ambulatory centers feature streamlined workflows with shorter turnover times allowing for higher surgical throughput and reduced overhead costs. The expansion of private equity backed eye care chains in Spain and the United Kingdom has accelerated the establishment of new ambulatory facilities equipped with state of the art phacoemulsification technology.

REGIONAL ANALYSIS

Germany Intraocular Lens Market Analysis

Germany was the largest contributor in the Europe Intraocular Lens Market by holding 18.3% of share in 2025 owing to the high procedural volumes and strong adoption of premium technologies driven by a robust supplemental insurance ecosystem. The presence of leading ophthalmic device manufacturers and research institutions fosters innovation and early access to new intraocular lens designs. Patients with private health insurance or supplemental coverage frequently opt for multifocal and toric lenses enhancing the value mix. Germany spends significantly on outpatient eye care services supporting the proliferation of specialized clinics. The country’s stringent regulatory framework ensures high quality standards, which builds trust in domestic and international brands. Furthermore, the integration of digital health records facilitates efficient patient management and follow up care reinforcing the efficiency of the surgical pathway.

France Intraocular Lens Market Analysis

France intraocular lens market was positioned next by capturing 14.3% of share in 2025 with the highly centralized healthcare system that emphasizes equitable access to cataract surgery, while gradually integrating premium options. According to national health data, France performs over 1 million cataract operations annually reflecting the high prevalence of age related eye disease. The French National Authority for Health actively evaluates new intraocular lens technologies influencing reimbursement decisions and clinical adoption patterns. Recent updates to coding systems have improved transparency in pricing allowing for better comparison of premium lens costs. As per demographic projections the number of individuals aged 75 and above is expected to double by 2050 ensuring long term demand growth. The presence of renowned ophthalmology centers in Paris and Lyon attracts international patients seeking advanced refractive solutions. Additionally, the government’s investment in modernizing hospital infrastructure supports the adoption of latest surgical technologies including femtosecond laser assisted procedures.

United Kingdom Intraocular Lens Market Analysis

The United Kingdom intraocular lens market is expected to grow with the dual system where the National Health Service provides basic care, while a vibrant private sector drives premium lens adoption. The significant backlog of cataract surgeries accumulated during the pandemic, which is now being addressed through increased surgical capacity. The private sector complements this by offering advanced intraocular lenses to self-pay patients with estimates suggesting 15 to 20% of patients choose premium options. The aging population continues to expand with life expectancy improvements increasing the window for elective eye surgery. The introduction of new service frameworks encourages collaboration between public hospitals and independent treatment centers.

Spain Intraocular Lens Market Analysis

Spain intraocular lens market growth is driven by the thriving medical tourism industry and high penetration of private ophthalmology clinics. The country’s reputation for high quality affordable eye care, which attracts patients from Northern Europe and beyond. The warm climate and lifestyle appeal enhance the attractiveness of combining surgery with leisure travel boosting demand for premium intraocular lenses. The private healthcare sector in Spain has grown steadily with increased investment in advanced surgical equipment. The prevalence of myopia and astigmatism among younger demographics drives interest in refractive lens exchange procedures. Additionally, Spanish ophthalmologists are early adopters of new technologies contributing to high clinical standards.

Italy Intraocular Lens Market Analysis

Italy intraocular lens market growth is to grow with the regional disparities in healthcare access but overall high clinical expertise in ophthalmology. The large elderly population with over 23% of Italians aged 65 or older by creating substantial baseline demand for cataract surgery. The northern regions exhibit higher adoption rates of premium intraocular lenses due to greater economic prosperity and private insurance coverage. The aging process is accelerating in Italy requiring sustained investment in eye care services. The presence of leading university hospitals fosters research and development in novel lens materials and designs. Additionally, the Italian Society of Ophthalmology promotes continuous medical education ensuring surgeons remain updated on best practices.

COMPETITIVE LANDSCAPE

The competition in the Europe Intraocular Lens Market is intense and characterized by the dominance of multinational corporations alongside specialized regional players. Major entities, such as Alcon Johnson and Johnson Vision and Bausch + Lomb leverage their extensive research and development capabilities to introduce innovative premium lenses that address presbyopia and astigmatism. These companies benefit from established distribution networks and strong relationships with key opinion leaders which facilitate rapid adoption of new technologies. Smaller competitors focus on niche segments such as customized toric lenses or specific material advantages to carve out market share. Price competition is moderate in the premium segment where clinical differentiation drives value but remains significant in the monofocal category where public reimbursement limits pricing power. Strategic collaborations with ambulatory surgery centers and hospital groups are common tactics to secure volume commitments. The shift toward outpatient care favors providers who can offer comprehensive solutions including surgical equipment and consumables. Innovation in digital surgical planning tools further intensifies rivalry as companies seek to create integrated ecosystems that enhance surgical precision and patient outcomes

KEY MARKET PLAYERS

Some of the notable companies operating in the Europe intraocular lens market include

- Johnson & Johnson

- Valeant

- Carl Zeiss Meditec AG

- Rayner

- Alcon, Inc. (a division of Novartis AG)

- EyeKon Medical, Inc.

- Lenstec, Inc.

- HumanOptics AG

- STAAR Surgical

- PhysIOL s.a.

- Calhoun Vision Center

- Oculentis GmBH.

Top Players in the Market

Alcon Inc

Alcon Inc maintains a formidable presence in the Europe Intraocular Lens Market through its extensive portfolio of monofocal and premium lenses. The company leverages its global manufacturing scale to ensure consistent supply across European distribution networks. Alcon, recently launched the Clareon intraocular lens platform in Europe featuring improved material stability and reduced glistenings. This innovation strengthens its competitive edge by addressing long term clarity concerns. The company invests heavily in surgeon education programs and digital surgical ecosystems integrating biometry and planning software. These initiatives enhance clinical outcomes and foster brand loyalty among ophthalmologists. Alcon’s strategic partnerships with ambulatory surgery centers facilitate direct access to high volume providers.

Johnson and Johnson

Johnson and Johnson Vision is a key contributor to the Europe Intraocular Lens Market with its TECNIS family of lenses. The company focuses on delivering high quality visual outcomes through advanced diffractive and aspheric designs. Johnson and Johnson recently introduced the TECNIS Odyssey lens in Europe, which aims to minimize dysphotopsia and improve contrast sensitivity. This launch expands its premium offerings and addresses unmet patient needs for night vision clarity. The company utilizes robust clinical data to support reimbursement discussions and surgeon adoption. Its integrated approach combines lenses with surgical consumables and visualization systems creating comprehensive solutions. Johnson and Johnson actively engages in post market surveillance to refine product performance. Strategic acquisitions and collaborations enhance its technological capabilities and market reach across diverse European healthcare settings.

Bausch + Lomb

Bausch + Lomb plays a significant role in the Europe Intraocular Lens Market with its enVista and Akreos lens platforms. The company emphasizes versatility and ease of use catering to a broad range of surgical preferences. Bausch + Lomb recently expanded its premium portfolio with new toric and multifocal options designed for enhanced stability. These additions strengthen its position in the growing refractive lens exchange segment. The company supports surgeons through comprehensive training resources and technical assistance programs. Its focus on hydrophobic acrylic materials aligns with market trends favoring biocompatibility and durability. Bausch + Lomb collaborates with key opinion leaders to generate real world evidence supporting clinical efficacy. Continuous innovation in lens design and packaging improves operational efficiency for healthcare providers.

Top Strategies Used by the Key Market Participants

Key players in the Europe Intraocular Lens Market primarily employ product innovation strategies to differentiate their offerings through advanced optical designs and material science improvements. Companies frequently launch new premium lenses featuring extended depth of focus and reduced dysphotopsia to capture higher margin segments. Strategic partnerships with ambulatory surgery centers and hospital networks enable direct distribution channels and bundled service contracts that enhance customer retention. Manufacturers invest extensively in surgeon education and training programs to build brand loyalty and ensure proper utilization of complex premium devices. Regulatory compliance with the European Union Medical Device Regulation is prioritized to maintain market access and trust. Pricing strategies vary by region with tiered approaches addressing reimbursement constraints in public systems while maximizing revenue from private pay patients. Digital integration of biometry and surgical planning software creates ecosystem lock in effects. Mergers and acquisitions are utilized to expand product portfolios and enter new geographic markets efficiently.

MARKET SEGMENTATION

This research report on the Europe intraocular lens market is segmented and sub-segmented into the following categories.

By Material

- Polymethylmethacrylate (PMMA)

- Silicone

- Hydrophobic Acrylic

By Type

- Monofocal Intraocular Lens

- Premium Intraocular Lens

- Toric Intraocular Lens

- Multifocal Intraocular Lens

- Accommodating Intraocular Lens

By End User

- Hospitals

- Ophthalmology Clinics

- Eye Research Institutes

- Ambulatory Surgical Centers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the size of the Europe intraocular lens market?

The European intraocular lens market was worth USD 1.12 billion in 2024.

What are the factors driving the growth of the Europe intraocular lens market?

The growing aging population, increasing prevalence of cataracts, advancements in surgical techniques, and increasing demand for premium intraocular lenses are some of the major factors driving the intraocular lens market in Europe.

Who are the key players in the Europe intraocular lens market?

Alcon Inc., Carl Zeiss Meditec AG, Bausch & Lomb Inc., and Johnson & Johnson Vision are some of the notable companies in the European intraocular lens market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com