Europe IQF Fruits and Vegetables Market segmented By Types (Fruits Which Include Berries, Bananas, Mango, Apple, Papaya, Pineapple, Kiwi And Others And Vegetables Which Include Carrots, Beans, Peas, Corn, Potato, Broccoli, Cauliflower And Others), By Distribution Channel (Online Stores, Retail Outlets and Hypermarkets), End-Users (Food Manufacturers and Hotels/Catering), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) – Size, Share, Trends, Growth, Forecast (2026 to 2034)

Europe IQF Fruits and Vegetables Market Size

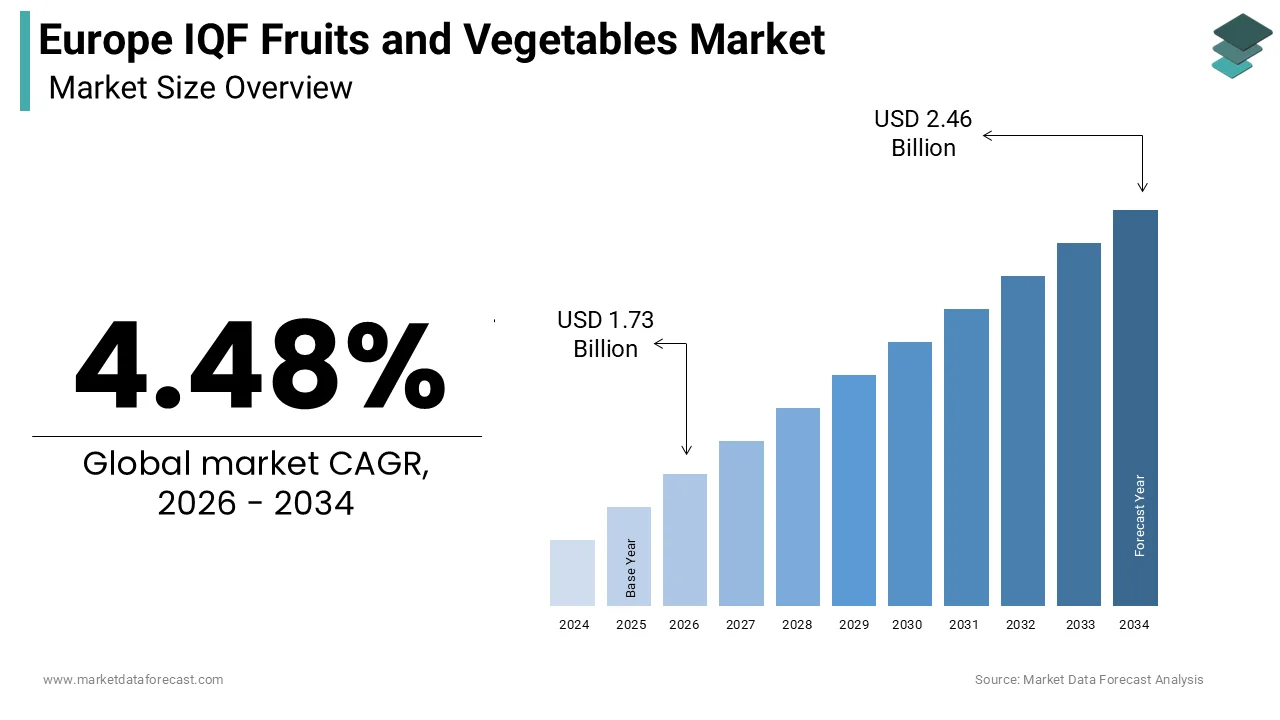

The Europe IQF Fruits and Vegetables Market size was calculated to be USD 1.66 billion in 2025 and is anticipated to be worth USD 2.46 billion by 2034, from USD 1.73 billion in 2026, growing at a CAGR of 4.48% during the forecast period.

Individually Quick Frozen (IQF) fruits and vegetables are fresh produce items that are frozen rapidly soon after harvest using cryogenic or blast freezing technologies to ensure each piece remains separate, retains its shape, and preserves nutritional and sensory qualities. In Europe, IQF products serve as a critical link between seasonal agricultural output and year-round consumer demand, offering convenience without significant compromise on quality. According to the European Commission’s Directorate‑General for Agriculture, the European Union produces tens of millions of metric tons of fruits and vegetables annually, with post‑harvest losses estimated at around 20% without proper cold chain intervention. The European Food Safety Authority recognizes Individual Quick Freezing (IQF) as an effective method to inhibit microbial growth and enzymatic degradation, thereby extending shelf life while maintaining vitamin C and polyphenol content close to fresh levels. According to Eurostat data, a large majority of European households purchased frozen fruits or vegetables in 2023, which reflects deep market penetration. The EU’s Farm to Fork Strategy further endorses IQF as a sustainable preservation technique that reduces food waste and supports seasonal labor optimization. With stringent hygiene regulations under Regulation (EC) No 852/2004 governing frozen food processing, the Europe IQF fruits and vegetables market operates at the intersection of food safety, nutritional integrity, seasonal logistics, and consumer convenience.

MARKET DRIVERS

Consumer Demand for Year‑Round Nutritional Convenience Drives IQF Adoption

European consumers increasingly prioritize health, convenience, and consistent availability of fruits and vegetables regardless of seasonality, which is fuelling sustained demand for IQF products and is one of the major factors driving the growth of the European IQF fruits and vegetables market. According to the European Food Information Council, a majority of adults in Western Europe cite “ease of use” and “no preparation needed” as key reasons for purchasing frozen produce, while many believe IQF items are as nutritious as fresh. According to the European Commission’s 2023 Special Eurobarometer on Food Safety, most respondents trust frozen fruits and vegetables as safe and healthy options. This perception is reinforced by scientific validation. As per a 2024 study by the German Institute of Human Nutrition, IQF blueberries retained over 90% of their anthocyanin content after six months of storage, compared to a much greater loss in refrigerated fresh counterparts. Retailers have responded by expanding IQF offerings as Tesco in the UK and Carrefour in France now stock over a hundred IQF SKUs each, including smoothie mixes and stir‑fry blends. With dual‑income households and urban lifestyles limiting time for produce preparation, IQF’s ready‑to‑cook or eat format aligns perfectly with modern European dietary patterns.

EU Policies on Food Waste Reduction and Seasonal Labor Optimization Support IQF Expansion

The European Union’s commitment to reducing food loss and stabilizing agricultural labor markets has elevated IQF processing as a strategic component of sustainable food systems, which is further boosting the expansion of the European IQF fruits and vegetables market. According to the European Commission’s Food Loss and Waste Prevention Framework, tens of millions of tons of edible food are wasted annually in the EU, with fruits and vegetables representing the largest category. IQF technology mitigates this by preserving surplus or cosmetically imperfect harvests at peak ripeness. In 2023, the EU funded multiple IQF infrastructure projects under the Common Agricultural Policy, including a facility in Poland dedicated to berry freezing. IQF processing also smooths labor demand. As per Eurofound, seasonal agricultural work peaks cause workforce strain in Southern Europe, but IQF plants extend harvesting windows and stabilize employment. According to Spain’s Ministry of Agriculture, IQF contracts now cover a significant share of strawberry and peach output, reducing on‑farm waste. By aligning with the Farm to Fork Strategy’s goal of halving food waste by 2030, IQF has transitioned from a commercial convenience to a policy‑endorsed sustainability tool.

MARKET RESTRAINTS

High Energy Consumption and Carbon Footprint of Freezing Operations Raise Environmental Concerns

The IQF process, while effective for preservation, demands significant energy input during blast or cryogenic freezing, drawing scrutiny under Europe’s climate mandates, which is a major factor hampering the European IQF fruits and vegetables market growth. According to the European Environment Agency, industrial freezing accounts for a notable share of total energy use in the EU food processing sector, with IQF lines consuming more energy than standard block freezing due to rapid air circulation and low temperature requirements. As per a 2023 life‑cycle assessment by the Joint Research Centre, the carbon footprint of IQF blueberries was higher than chilled fresh equivalents, primarily due to electricity use in freezing and cold chain logistics. Countries such as Sweden and Denmark, which enforce strict green manufacturing standards, now require IQF facilities to source renewable energy or face carbon taxes. The EU’s Energy Efficiency Directive also mandates regular audits for high‑consumption plants, increasing operational costs. While IQF reduces food waste, its energy intensity creates a trade‑off with those challenges to net‑zero goals, pressuring producers to invest in costly efficiency upgrades.

Stringent Cold Chain Integrity Requirements Increase Logistics Complexity and Cost

Maintaining an unbroken cold chain from IQF processing to retail freezer is essential to preserve quality and safety, yet this requirement imposes significant logistical and financial burdens, which further impede the European IQF fruits and vegetables market growth. According to the European Food Safety Authority, temperature fluctuations above –18 °C during transport or storage can trigger ice recrystallization, leading to cellular damage and reduced sensory quality. EU Regulation (EC) No 852/2004 mandates continuous temperature monitoring and documentation for all frozen foods, necessitating investment in telematics and data loggers. In 2023, the French Directorate General for Competition Policy reported that a portion of IQF shipments failed temperature compliance checks during cross‑border transit, often due to refrigeration unit failures or loading delays. Small and medium producers in Eastern Europe struggle to afford certified refrigerated transport, limiting their reach. The rise of e‑grocery delivery introduces new risks; a 2024 study by Wageningen University found that a notable share of home‑delivered IQF orders experienced temperature excursions during last‑mile transit. These vulnerabilities increase waste, compliance costs, and consumer dissatisfaction, acting as a structural restraint on market scalability.

MARKET OPPORTUNITIES

Growth of Plant‑Based and Clean Label Food Manufacturing Creates Premium IQF Demand

The rapid expansion of plant‑based food production in Europe is generating robust demand for high-quality IQF fruits and vegetables as clean-label ingredients in meat analogs, dairy alternatives, and ready meals, which is a major opportunity in the European IQF fruits and vegetables market. According to the European Plant‑Based Foods Association, the EU plant‑based market grew by over 20% in 2023, reaching billions of euros in retail sales, with IQF berries, spinach, and peas serving as key components for color, flavor, and nutrition. Companies such as Oatly and Beyond Meat source IQF produce to ensure a consistent year‑round supply without artificial additives. The European Commission’s 2024 guidance on clean label claims favours frozen over dried or powdered ingredients due to minimal processing. In Germany, a majority of new vegan product launches in 2023 listed “IQF fruits” on packaging to signal freshness and naturalness. IQF’s ability to deliver microbiologically safe, pre‑cleaned ingredients reduces processing steps for manufacturers, aligning with efficiency and food safety goals.

Expansion of Retail Private Label IQF Lines Enhances Market Accessibility and Volume

Major European supermarket chains are aggressively expanding their private label IQF portfolios, democratizing access and driving volume through competitive pricing and quality assurance, which is another prominent opportunity in the regional market. According to the European Private Label Association, private label IQF fruits and vegetables now account for more than half of frozen produce sales in Western Europe, up significantly since 2020. Retailers such as Edeka in Germany, Sainsbury’s in the UK, and Auchan in France enforce strict supplier standards, ensuring consistent quality while offering lower prices than branded alternatives. In 2023, Carrefour launched a “Farm to Freezer” transparency initiative, showcasing IQF sourcing regions and freezing times on packaging to build consumer trust. Retailers are also innovating with portion‑controlled and recipe‑specific IQF blends, boosting frequency of purchase. This retail‑led strategy increases household penetration and stabilizes demand for growers and processors through long‑term contracts.

MARKET CHALLENGES

Seasonal and Geopolitical Volatility Disrupts Raw Material Sourcing Consistency

The Europe IQF fruits and vegetables market faces recurring supply instability due to climate variability, labor shortages, and geopolitical disruptions affecting key sourcing regions. According to the European Commission’s 2023 Crop Monitoring Report, extreme weather events—including droughts in Spain and floods in Poland—reduced berry and pea harvests compared to the five‑year average, directly limiting IQF feedstock availability. Additionally, a significant share of European IQF production relies on labor from Eastern Europe and North Africa, where migration policy changes and visa restrictions have caused harvesting delays. Geopolitical tensions further compound risk; the war in Ukraine disrupted sunflower and berry supplies to Central European processors, forcing reformulation or price hikes. As per a 2024 survey by FoodDrinkEurope, a majority of IQF manufacturers experienced raw material shortages in the past year, leading to extended lead times and contract renegotiations. Unlike canned or dried alternatives, IQF requires immediate post‑harvest processing, leaving little buffer for supply chain shocks.

Consumer Misconceptions About Nutritional Quality Undermine Premium Positioning

Despite scientific evidence supporting the nutritional parity of IQF produce, persistent consumer myths equating frozen with “inferior” continue to limit willingness to pay premium prices in certain European markets, which is further challenging the European IQF fruits and vegetables market expansion. According to the European Consumer Organisation’s 2024 survey, a significant share of respondents in Southern Europe still believe fresh fruits and vegetables are more nutritious than frozen, even when stored for days. This perception is reinforced by retail placement—many supermarkets relegate IQF sections to less prominent freezer aisles, which signals lower status compared to fresh produce displays. In Italy and Greece, where culinary traditions emphasize “from the garden” freshness, IQF adoption lags despite high food waste rates; Eurostat data shows that less than half of households regularly purchase frozen vegetables. Marketing efforts by industry groups have struggled to overcome cultural biases, and price promotions often reinforce the notion of IQF as a budget option rather than a premium choice. Until coordinated education campaigns shift cultural narratives, the market will face headwinds in achieving value‑based pricing across all European regions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.48% |

| Segments Covered | By Type, Distribution Channel, End User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Alasko Foods Inc, SunOpta Inc, Fruktana Ltd, Nimeks Organics, AXUS International LLC, Breukers Schamp Foods, and Rasanco Ltd. |

SEGMENTAL ANALYSIS

By Type Insights

The vegetables segment dominated the market by holding 56.5% of the European market share in 2025. The dominance of vegetables segment in this regional market is driven by their widespread use in ready meals, institutional catering, and household cooking. IQF vegetables such as peas, carrots, corn, and broccoli offer consistent quality, year‑round availability, and reduced preparation time—critical attributes for both consumers and food service operators. According to the European Commission’s Food Consumption Database, a majority of European households consume frozen vegetables weekly, with pea and carrot blends being the most common. The European School Fruit Scheme further institutionalizes demand, as national programs in Germany, Poland, and the Netherlands include IQF vegetables in meal preparations for millions of children annually. Food manufacturers also rely heavily on IQF vegetables for soups, sauces, and plant‑based products. According to FoodDrinkEurope, most new frozen ready meal launches contained IQF broccoli, peas, or corn due to their texture retention and visual appeal in 2023.

The berries segment represents the fastest-growing segment and is estimated to grow at a promising CAGR of 11.5% over the forecast period, owing to the rising health consciousness, smoothie innovation, and strong seasonal supply from Nordic and Eastern European growers. According to the European Berry Association, EU berry production exceeded over a million metric tons in 2023, with a large share processed as IQF to preserve anthocyanins and vitamin C. In Sweden and Finland, government‑supported berry collection programs channel wild‑harvested bilberries and lingonberries directly into IQF supply chains. EFSA’s 2023 opinion recognized berries as high in antioxidants, reinforcing their inclusion in functional food formulations. Major brands such as Innocent (UK) and Bjorg (France) now use IQF blueberries and raspberries in dairy alternatives and breakfast bowls. E‑commerce platforms highlight “no sugar added” IQF berry packs as clean-label superfoods, appealing to wellness‑focused consumers.

By Distribution Channel Insights

The retail outlets and hypermarkets segment dominated the market in 2025 with 61.6% of the regional market share. The retail outlets and hypermarkets segment is serving as the primary access point for household consumption. Supermarkets such as Edeka (Germany), Carrefour (France), and Tesco (UK) allocate significant freezer space to IQF produce, offering both branded and private label options. According to the European Private Label Association, private label IQF products grew by over 20% in 2023, driven by demand for value without quality compromise. Retailers enforce strict supplier standards such as BRCGS certification and pesticide residue testing, ensuring consistency. In the Netherlands, as per Statistics Netherlands, a large majority of households purchase IQF vegetables monthly, supported by recipe integration in weekly flyers. Seasonal promotions like “summer berry packs” or “winter vegetable blends” further boost trial and volume.

The online stores segment is estimated to witness a promising CAGR of 13.5% over the forecast period, owing to the growing popularity of e‑grocery platforms, subscription meal kits, and demand for transparent sourcing. According to Eurostat, a majority of European households made at least one online grocery purchase in 2023, with frozen produce among the top categories. Platforms such as Picnic (Netherlands) and Ocado (UK) now offer dedicated “frozen fruit and veg” filters. Meal kit companies like HelloFresh and Marley Spoon incorporate IQF berries and vegetables into pre‑portioned recipes, reaching millions of subscribers. Specialty e‑retailers such as Bio c’Bon (France) highlight organic IQF produce with farm origin stories, appealing to ethically conscious shoppers.

By End User Insights

The food manufacturers segment accounted for the largest share of 55.7% of the European market in 2025. The food manufacturers leverage IQF produce as consistent, safe, and clean-label ingredients in processed foods. IQF vegetables like peas, corn, and broccoli are essential in frozen ready meals, soups, and sauces, while IQF fruits such as berries and mangoes feature prominently in yogurts, desserts, and plant‑based beverages. According to FoodDrinkEurope, most new frozen food launches in 2023 included IQF ingredients due to their microbiological safety and color retention. Companies such as Nestlé, Unilever, and Dr Oetker rely on long‑term contracts with IQF processors to secure supply stability. The European Commission’s 2024 Clean Label Guidelines favor IQF over powders or concentrates, reinforcing its role in “free from” formulations.

The hotels and catering segment is the fastest-growing end-user segment and is anticipated to expand at a CAGR of 10.3% over the forecast period due to the hospitality recovery, contract catering expansion, and the need for kitchen efficiency. According to the European Hospitality Association, hundreds of thousands of hotels and institutional kitchens in the EU now use IQF vegetables as standard prep items. In Germany, the Federal Ministry of Food and Agriculture reported that a majority of school meal providers switched to IQF broccoli and peas in 2023 to meet nutritional standards. High‑end restaurants in Paris and Copenhagen increasingly use IQF wild berries for desserts and sauces. The EU’s Sustainable Public Procurement criteria further encourage IQF adoption by recognizing its role in reducing food waste.

REGIONAL ANALYSIS

Germany IQF Fruits and Vegetables Market Analysis

Germany led the IQF fruits and vegetables market in Europe in 2025 with 23.3% of the regional market share. The dominance of Germany in the European market is driven by its large population, advanced cold chain infrastructure, and strong frozen food culture. According to the German Frozen Food Association, a large majority of households purchase IQF produce regularly, with peas, carrots, and berries among the top sellers. The country hosts major food manufacturers such as Dr Oetker and Nestlé Deutschland that rely on IQF ingredients for frozen meals and desserts, driving industrial demand. Germany’s stringent food safety laws under the LFGB ensure high-quality standards, while government initiatives like the National Reduction and Recycling Strategy promote IQF as a tool to cut household food waste. Additionally, the rise of plant‑based diets has boosted demand for IQF berries and vegetables in alternative protein products.

UK IQF Fruits and Vegetables Market Analysis

The UK held the second-largest share of the European IQF fruits and vegetables market in 2025. The growth of the UK in the European market can be credited to the high retail penetration, meal kit adoption, and post‑Brexit supply chain localization. According to the British Frozen Food Federation, frozen fruit and vegetable sales grew by double digits in 2023, with IQF berries and broccoli leading household purchases. Major retailers such as Tesco and Sainsbury’s allocate prominent freezer space to IQF produce, while private labels now account for the majority of volume. The UK’s meal kit sector is among Europe’s largest, with HelloFresh and Gousto using IQF vegetables in most of their recipes to ensure consistency and reduce spoilage. NHS catering guidelines for hospitals and schools mandate frozen vegetables when fresh is unavailable, institutionalizing demand. Consumer trust is strong—most UK consumers believe IQF is as healthy as fresh, according to the Food Standards Agency.

France IQF Fruits and Vegetables Market Analysis

France is estimated to account for a promising share of the regional market during the forecast period, owing to its culinary integration of IQF produce and strong agricultural processing base. According to FranceAgriMer, hundreds of thousands of metric tons of fruits and vegetables are IQF processed annually, with peas, green beans, and berries sourced from Brittany and the Loire Valley. French consumers value convenience without compromising gastronomy; a 2024 CREDOC survey found that a majority of households use IQF vegetables in traditional dishes such as pot au feu and ratatouille. Major brands like Marie and Picard Surgelés have built national loyalty through high-quality IQF offerings, with Picard operating hundreds of dedicated frozen food stores. France’s anti‑food waste law mandates supermarkets to donate unsold fresh produce or convert it to frozen, indirectly supporting IQF infrastructure.

Spain IQF Fruits and Vegetables Market Analysis

Spain is expected to register a healthy CAGR in the European IQF fruits and vegetables market during the forecast period. Spain is a key production and export hub due to its favorable climate and large horticultural sector. According to the Spanish Ministry of Agriculture, Spain is the EU’s largest producer of IQF strawberries, peaches, and artichokes, with a significant share exported to Northern Europe. Intensive farming in Andalusia and Murcia enables year‑round harvesting, feeding a dense network of IQF processing plants that comply with EU hygiene regulations. Domestic consumption is rising; the Spanish Food Consumption Survey 2023 reported growth in household IQF vegetable purchases, driven by urbanization and dual‑income households. Spain’s tourism sector fuels demand from hotels and catering services for consistent, ready‑to‑use IQF produce.

Italy IQF Fruits and Vegetables Market Analysis

Italy is projected to account for a notable share of the European market over the forecast period. Italy is experiencing accelerated growth due to shifting dietary habits and institutional procurement reforms. According to ISTAT, IQF vegetable consumption rose by over 20% between 2021 and 2023, particularly among young urban families seeking convenience without processed additives. Italy’s school meal programs are increasingly using IQF peas, broccoli, and spinach to meet nutritional mandates while managing seasonal gaps. The country is also a major processor of IQF tomatoes and artichokes for sauce and ready meal manufacturers such as Barilla and Conad. Despite traditional emphasis on fresh ingredients, rising food costs and labor shortages are driving professional kitchens to adopt IQF as a reliable backup. The Ministry of Agricultural Policies’ 2023 Food Waste Prevention Plan further endorses IQF as a sustainable solution.

COMPETITION OVERVIEW

The Europe IQF fruits and vegetables market features a competitive landscape characterized by a mix of large integrated agro processors and specialized regional players. Competition is driven by raw material access, processing efficiency, and brand reputation rather than price alone. Major companies like Nomad Foods and Südzucker benefit from scale backward integration and established retail relationships, enabling consistent supply and innovation. Smaller processors compete through niche offerings such as wild berries, organic certification, or regional specialties. The market is highly regulated under EU hygiene and food safety laws, requiring strict cold chain control and microbiological testing, which creates barriers for new entrants. Sustainability has become a key differentiator, with consumers and retailers favoring suppliers with low carbon footprints and zero waste commitments. Geopolitical and climatic volatility in sourcing regions adds risk, requiring diversified supply strategies. As demand grows from food manufacturing, meal kits, and institutional catering, competition increasingly centers on reliability, quality, transparency, and environmental stewardship across the IQF value chain.

KEY MARKET PLAYERS

A few major players of the Europe IQF fruits and vegetables market include

- Alasko Foods Inc

- SunOpta Inc

- Fruktana Ltd

- Nimeks Organics

- AXUS International LLC

- Breukers Schamp Foods

- Rasanco Ltd

Top Strategies Used by the Key Market Participants

Key players in the Europe IQF fruits and vegetables market focus on vertical integration, sustainability innovation, and retail collaboration to strengthen competitiveness. Companies invest in energy-efficient freezing technologies and renewable energy to align with EU climate goals and reduce operational costs. They source directly from contracted farms to ensure quality, consistency, supply security, and traceability. Product portfolios are expanded to include organic clean-label and region-specific blends such as Mediterranean or Nordic berry mixes. Strategic partnerships with retailers enable private label development and prominent shelf placement in frozen aisles. Digital tools like blockchain and QR codes are increasingly used to provide transparency on origin and freezing time. Additionally, firms diversify into plant-based and meal kit channels to capture emerging demand streams. These strategies collectively address Europe’s dual priorities of food quality, sustainability, and convenience.

Leading Players in the Europe IQF Fruits and Vegetables Market

- Nomad Foods Limited is a leading European frozen food company with a substantial presence in the IQF fruits and vegetables segment through its iconic brands Birds Eye and Findus. The company sources IQF produce from a network of certified farms across Eastern and Southern Europe, ensuring a year-round supply of peas, broccoli, berries, and mixed vegetable blends. In 2024, Nomad enhanced its sustainability credentials by achieving zero food waste to landfill across all its European IQF processing facilities and committing to 100 percent renewable electricity by 2025. The company also launched a new line of organic IQF berry packs with blockchain-enabled traceability for retail consumers. Through brand trust, product innovation, and vertical integration from farm to freezer, Nomad continues to shape consumer expectations and industry standards for IQF quality and transparency across Europe.

- Südzucker AG operates one of Europe’s largest IQF fruit and vegetable processing networks under its Toorank and Raffo brands, serving both retail and food manufacturing customers. Headquartered in Germany, the company leverages its agricultural cooperatives to source raw materials directly from growers, ensuring freshness and supply stability. In 2023, Südzucker invested 25 million euros in upgrading IQF freezing lines at its Polish and Italian facilities to improve energy efficiency and reduce carbon emissions per ton of frozen produce. The firm also expanded its portfolio of IQF pulses and Mediterranean vegetables to meet demand from plant-based food manufacturers. By combining agricultural integration, technological modernization, and sustainability initiatives, Südzucker reinforces its role as a reliable and forward-looking supplier in the European IQF ecosystem.

- Agrana Beteiligungs AG is an Austrian based agro industrial group with a focused IQF fruits business that supplies berries app,les and tropical fruits to food service and ingredient markets across Europe. The company operates state-of-the-art IQF plants in Hungary, Romania, and Serbia strategically located near key berry harvest zones. In early 2024, Agrana launched aclean-labell IQF fruit platform free from anti-caking agents and glazes, targeting premium yogurt and smoothie manufacturers. The firm also strengthened partnerships with Nordic wild berry collectors to secure sustainable supplies of bilberries and cloudberries. Through geographic proximity to raw material,s technological precision, acustomer-centricric formulation, Agrana has established itself as a niche yet influential player in the high-quality IQF fruit segment of the European market.

MARKET SEGMENTATION

This research report on the Europe IQF Fruits and Vegetables market has been segmented and sub-segmented based on type, distribution channel, end user, and region.

By Type

- Fruits

- Berries

- Bananas

- Mango

- Apple

- Papaya

- Pineapple

- Kiwi

- Others

- Vegetables

- Carrots

- Beans

- Peas

- Corn

- Potato

- Broccoli

- Cauliflower

- Others

By Distribution Channel

- Online stores

- Retail stores

- Hypermarkets

By End User

- Food Manufacturers

- Hotel / Catering

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe IQF fruits and vegetables market?

Market growth is driven by rising demand for convenient food options, increasing consumption of frozen ready meals, expanding foodservice industries, and growing awareness of reduced food waste.

2. What does IQF mean in food processing?

IQF stands for Individually Quick Frozen, a freezing method that rapidly freezes individual pieces of fruits or vegetables to prevent clumping and maintain quality.

3. Which fruits are most commonly sold in IQF format in Europe?

Popular IQF fruits include strawberries, raspberries, blueberries, mangoes, peaches, and mixed berries, widely used in dairy, bakery, and beverage applications.

4. Which vegetables dominate the Europe IQF vegetables segment?

Peas, sweet corn, green beans, carrots, broccoli, and mixed vegetables are among the most commonly consumed IQF vegetables in Europe.

5. Which industries use IQF fruits and vegetables the most?

The food processing industry, including bakery, dairy, ready meals, soups, sauces, and foodservice sectors, represents the largest consumer base for IQF products.

6. How does IQF technology benefit manufacturers?

IQF technology ensures extended shelf life, minimal nutrient loss, portion control flexibility, and improved supply chain efficiency compared to fresh produce.

7. How is sustainability influencing the Europe IQF fruits and vegetables market?

Sustainability initiatives such as energy-efficient freezing systems, recyclable packaging, and food waste reduction are increasingly shaping market strategies.

8. What distribution channels are important for IQF fruits and vegetables?

Supermarkets, hypermarkets, foodservice distributors, specialty frozen food retailers, and industrial bulk supply chains are key distribution channels.

9. What challenges does the Europe IQF fruits and vegetables market face?

Challenges include fluctuating raw material supply due to climate conditions, high energy costs for freezing and storage, and strict food safety regulations.

10. What is the future outlook for the Europe IQF fruits and vegetables market?

The market is expected to grow steadily, supported by rising demand for convenient, healthy frozen foods, innovation in freezing technologies, and expansion of ready-to-eat and plant-based product categories.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com