Europe LPG Market Size, Share, Trends & Growth Forecast Report By Source (Refinery, Associated Gas, Non-Associated Gas), Application (Residential/Commercial, Chemical, Industrial, Autogas, Refinery, Others), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) – Industry Analysis From 2026 to 2034.

Market Size, 2025

$39.71 BnMarket Estimate, 2026

$40.90 BnMarket Forecast, 2034

$52 BnCAGR, 2026–2034

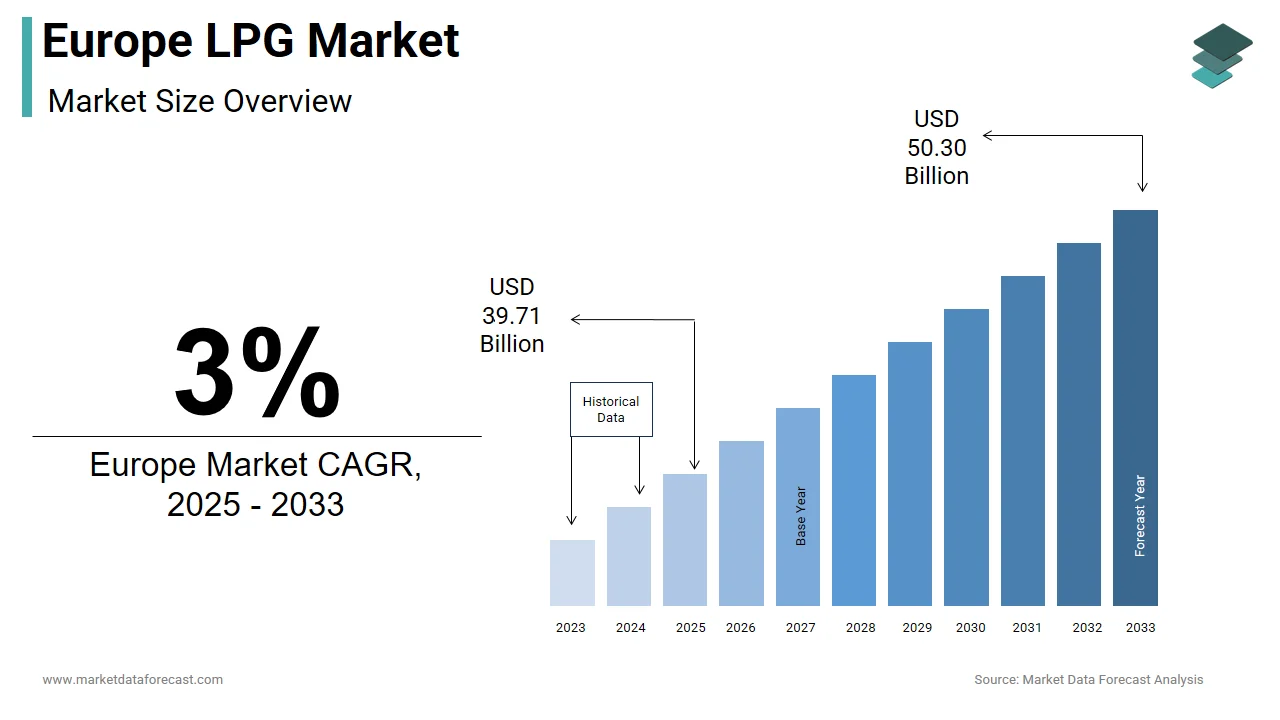

3%Europe LPG Market Size

The size of the Europe LPG (liquefied petroleum gas) market was valued at USD 39.71 billion in 2025. This market is expected to grow at a CAGR of 3% from 2026 to 2034 and be worth USD 52 billion by 2034 from USD 40.90 billion in 2026.

LPG is primarily composed of propane and butane, and serves as a versatile energy source used for heating, cooking, power generation, and as an alternative fuel for vehicles under the name autogas.

According to Eurostat, over 60 million European households rely on LPG for domestic heating and cooking, particularly in rural and off-grid areas where natural gas pipelines are unavailable. LPG plays a crucial role in complementing renewable energy sources, offering a cleaner-burning alternative to coal and oil-based fuels. It is also widely used in industrial processes such as metal cutting, food processing, and agricultural drying, where high-energy density and portability are essential. Furthermore, as per the International Energy Agency, LPG contributes significantly to reducing indoor air pollution and improving energy access in remote communities.

MARKET DRIVERS

Growing Demand for Clean Cooking and Heating Solutions in Off-Grid Areas

One of the primary drivers of the Europe LPG market is the increasing demand for clean cooking and heating solutions in off-grid and semi-urban areas where natural gas infrastructure is limited or absent. According to Eurostat, nearly 30% of EU households lack access to centralized gas networks, which is making LPG a critical alternative for reliable and clean energy use.

In countries like Poland, Greece, and Romania, where large rural populations depend on solid fuels for heating, LPG adoption has been encouraged through government subsidies and awareness campaigns promoting cleaner energy alternatives. According to the European Environment Agency, switching from coal or wood to LPG can reduce particulate matter emissions by up to 90% by contributing to improved public health and environmental outcomes.

Moreover, as per the European LPG Association (AEGPL), LPG usage in residential heating increased by 8% between 2020 and 2023 in Eastern Europe, driven by rising energy poverty concerns and efforts to phase out inefficient and polluting heating systems.

Expansion of Autogas Infrastructure and Vehicle Adoption

Another significant driver of the Europe LPG market is the growth of autogas as a cost-effective and environmentally preferable alternative to gasoline and diesel in the transportation sector. As per the International Association for Liquefied Petroleum Gas (World LPG), more than 10 million autogas vehicles were in operation across Europe in 2023, with Italy, Poland, and Germany leading in fleet numbers. Governments have incentivized the conversion of conventional vehicles to autogas through tax exemptions, reduced fuel prices, and investment in refueling stations. According to ACEA (European Automobile Manufacturers’ Association), autogas fuel costs approximately half as much as petrol, making it an attractive option for cost-conscious consumers and fleet operators alike.

Additionally, as per AEGPL, over 4,500 autogas refueling stations were operational across Europe in 2023, ensuring broader accessibility and convenience for drivers. This expanding infrastructure supports the long-term viability of LPG as a mobility fuel in urban logistics and public transport segments seeking affordable, low-emission solutions.

MARKET RESTRAINTS

Regulatory Push Toward Electrification and Renewable Energy Sources

A major restraint affecting the Europe LPG market is the regulatory push toward full electrification and renewable energy sources, which has led to reduced policy support for LPG in several key markets. The European Green Deal and the Fit for 55 package prioritize direct electrification and hydrogen-based solutions, which is limiting the long-term prospects of LPG as a transitional fuel.

According to the European Commission, several member states have introduced stricter emission standards and financial disincentives for fossil fuels, including LPG, in favor of zero-emission technologies such as battery electric vehicles and heat pumps. Countries like France and the Netherlands have gradually phased out tax benefits for autogas conversions, redirecting subsidies exclusively toward electric mobility. Moreover, as per the International Energy Agency, new building regulations in Germany and Sweden discourage the installation of LPG heating systems in favor of all-electric home solutions powered by renewable electricity.

Volatility in Global LPG Prices and Supply Chain Disruptions

Another critical constraint on the Europe LPG market is the volatility in global LPG prices, which directly affects consumer affordability and industry profitability. LPG prices are closely tied to crude oil markets, making them susceptible to geopolitical tensions, supply chain disruptions, and fluctuations in feedstock availability. According to the UK government’s Department for Business, Energy & Industrial Strategy, LPG prices in Europe saw a 40% increase in early 2023 due to supply bottlenecks and reduced imports from traditional exporters such as the US and Algeria. These price surges disproportionately affected small-scale users, particularly in Southern and Eastern Europe. Additionally, as per the European Chemical Industry Council, logistical challenges such as shipping delays and storage capacity constraints have further complicated supply stability, impacting both residential and industrial consumers.

MARKET OPPORTUNITIES

Role of BioLPG in Decarbonizing the LPG Sector

One of the most promising opportunities in the Europe LPG market lies in the development and adoption of BioLPG is a renewable, drop-in substitute for conventional LPG derived from organic waste and residue materials. According to the European Biogas Association, BioLPG production capacity in Europe is expected to triple by 2030, driven by advancements in bio-refining and increased investment in circular economy initiatives. Several refineries in Scandinavia and the Netherlands have already begun integrating BioLPG into their supply chains, which is positioning it as a key enabler of decarbonization in off-grid heating and transport. Moreover, as per the European LPG Association (AEGPL), BioLPG is gaining traction among policymakers as a viable short-to-medium-term solution for reducing greenhouse gas emissions in sectors where electrification remains technically or economically unfeasible.

Integration of LPG in Hybrid Energy Systems for Rural and Remote Applications

Another significant opportunity for the Europe LPG market is the integration of LPG within hybrid energy systems tailored for rural and remote communities. As part of the broader effort to improve energy access while reducing emissions, LPG is increasingly being paired with solar, wind, and battery storage to provide reliable, flexible, and cleaner energy solutions. According to the International Energy Agency, hybrid systems incorporating LPG offer a balanced approach to managing intermittency issues associated with renewables, particularly in cold climates where continuous heating is essential. Pilot projects in Italy and Austria have demonstrated how LPG can complement solar thermal installations by ensuring an uninterrupted energy supply during periods of low sunlight or high demand.

Furthermore, as per the European Climate Foundation, decentralized LPG-fueled microgrids are being explored in Eastern Europe to support rural electrification and industrial activities without reliance on national grids. This trend reflects a broader shift toward integrated energy models that leverage the strengths of multiple energy carriers.

MARKET CHALLENGES

Public Perception and Environmental Concerns Regarding Fossil-Based LPG

A major challenge facing the Europe LPG market is the prevailing perception of LPG as a fossil-based fuel that conflicts with the region’s ambitious climate targets. According to the European Environment Agency, public sentiment toward fossil fuels, including LPG, has become increasingly negative, particularly among younger demographics advocating for rapid decarbonization. This perception influences both consumer behavior and policymaking, which is limiting the visibility and attractiveness of LPG in comparison to electric heat pumps and green hydrogen. Moreover, as per the European Consumer Organization (BEUC), misinformation about LPG’s carbon footprint and safety risks has contributed to hesitancy among homeowners and businesses considering LPG as an alternative energy source.

Fragmented Regulatory Framework Across European Countries

Another pressing challenge in the Europe LPG market is the fragmented regulatory framework across different member states, which complicates standardization, cross-border trade, and investment planning. According to the European LPG Association (AEGPL), disparities exist in taxation policies, vehicle conversion incentives, and infrastructure funding mechanisms, leading to inconsistent market development across the region. For instance, while Italy and Poland have robust autogas support programs, countries like Belgium and Denmark have scaled back incentives in recent years. Additionally, as per the European Commission, differing safety and technical standards for LPG storage, transport, and use hinder pan-European harmonization and limit economies of scale.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Source, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Repsol, China Gas Holdings Ltd., Saudi Arabian Oil Co., FLAGA GmbH, Kleenheat, Bharat Petroleum Corporation Limited, JGC Holdings Corporation, Phillips 66 Company, Chevron Corporation, Reliance Industries Limited, Exxon Mobil Corporation, Total, Royal Dutch Shell, Petronas, PetroChina, Petredec, Qatargas, Petrofac, Vitol, China Petroleum & Chemical Corporation, and BP Plc. |

SEGMENTAL ANALYSIS

By Source Insights

The associated gas-derived segment was the largest share of the Europe LPG market by accounting for prominent share in 2024 due to its extensive production as a byproduct of crude oil extraction and refining processes across key oil-producing regions within and beyond Europe.

According to the International Energy Agency, over 60% of global LPG supply comes from associated gas extracted during oil drilling operations, with major European refineries in countries like Germany, Italy, and the Netherlands playing a pivotal role in processing this feedstock. The region's reliance on imported crude oil further reinforces the availability of associated gas-based LPG, ensuring a steady domestic supply.

The non-associated gas-derived LPG is swiftly emerging with a CAGR of 8.4% during the forecast period. According to the European Biogas Association, increasing investments in biogas and biomethane projects have contributed significantly to this growth trajectory. Countries like Sweden, Denmark, and the Netherlands are leveraging anaerobic digestion and waste-to-energy technologies to produce renewable LPG-compatible fuels, which is reducing dependency on fossil-based sources. Additionally, as per the UK government’s Department for Business, Energy & Industrial Strategy, non-associated gas production has been bolstered by enhanced exploration activities in the North Sea and increased imports of liquefied natural gas (LNG), which contain extractable LPG fractions.

By Application Insights

The chemical industry application segment held 42.3% of the Europe LPG market share in 2024. LPG, particularly propane and butane, serves as a crucial feedstock in petrochemical manufacturing, used extensively in producing polymers, solvents, and synthetic materials. According to PlasticsEurope, the European chemical sector relies on LPG for nearly half of its olefin production, with major facilities in Belgium, Germany, and France driving demand. Propane dehydrogenation (PDH) plants have expanded in recent years by enhancing the region’s capacity to convert LPG into valuable chemical intermediates.

The autogas segment is likely to register a CAGR of 7.2% throughout the forecast period, owing to the continued use of LPG as an affordable, low-emission fuel for vehicles in Eastern and Southern Europe, where electric vehicle adoption lags behind Western counterparts. According to the International Association for Liquefied Petroleum Gas (World LPG), more than 10 million autogas-powered vehicles were registered in Europe in 2023, with Poland, Italy, and Turkey leading in fleet numbers. Moreover, as per ACEA (European Automobile Manufacturers’ Association), several automakers continue to offer factory-fitted dual-fuel vehicles that run on both petrol and LPG, which is catering to budget-conscious consumers seeking reduced fuel costs without compromising performance.

COUNTRY-LEVEL ANALYSIS

Germany was the largest contributor in the Europe LPG market with a 23.4% share in 2024. Germany utilizes LPG extensively in petrochemical production, metalworking, and food processing, where high calorific value and portability make it indispensable. According to the German LPG Association (DVFG), industrial and chemical applications account for over 50% of LPG consumption in the country, supported by a dense distribution network and strong manufacturing output.

Italy was positioned second with 215.4% of the Europe LPG market share in 2024. According to Federmetano, Italy had over 2.5 million autogas vehicles on its roads in 2023, with more than 3,000 refueling stations ensuring broad accessibility. Government incentives historically favored LPG conversions, which fostered widespread consumer acceptance even before EV incentives gained prominence. Beyond transportation, LPG plays a vital role in residential heating, especially in rural areas not connected to natural gas pipelines. Over 6 million Italian households rely on bottled or bulk LPG for cooking and space heating, according to the Italian LPG Association (Assogasliquidi).

Poland's LPG market is lucratively growing with the strong autogas adoption and rising industrial consumption. Poland’s reliance on coal for power generation and heating has made LPG an attractive cleaner alternative, prompting both government and private-sector initiatives to promote its use. Residential LPG demand remains robust in rural areas, where centralized gas pipelines do not extend. Additionally, as per the Central Statistical Office of Poland, LPG-based micro-refineries have emerged in several regions to support local industrial needs, including drying processes in agriculture and small-scale chemical production.

The Netherlands' LPG market growth is due to its strategic location and advanced logistics infrastructure to serve both domestic and international demand. According to Statistics Netherlands (CBS), the Dutch chemical industry remains a primary consumer, utilizing LPG as a feedstock for ethylene and propylene production. Rotterdam’s status as Europe’s largest port enables efficient import and re-export of LPG, strengthening its influence in the continent’s supply chain.

KEY MARKET PLAYERS

Companies playing a prominent role in the European LPG market profiled in this report are Repsol, China Gas Holdings Ltd., Saudi Arabian Oil Co., FLAGA GmbH, Kleenheat, Bharat Petroleum Corporation Limited, JGC Holdings Corporation, Phillips 66 Company, Chevron Corporation, Reliance Industries Limited, Exxon Mobil Corporation, Total, Royal Dutch Shell, Petronas, PetroChina, Petredec, Qatargas, Petrofac, Vitol, China Petroleum & Chemical Corporation, and BP Plc.

MARKET SEGMENTATION

This Europe LPG market research report is segmented and sub-segmented into the following categories.

By Source

- Refinery

- Associated Gas

- Non-Associated Gas

By Application

- Residential/Commercial

- Chemical

- Industrial

- Autogas

- Refinery

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the main drivers for the Europe liquefied petroleum gas market?

The Europe liquefied petroleum gas market is driven by rising demand for clean heating and cooking in rural areas, growth in autogas vehicles, and the need for a reliable, portable energy source for industry and households.

2. What challenges does the Europe liquefied petroleum gas market face?

The Europe liquefied petroleum gas market faces challenges from regulatory focus on electrification, volatile global LPG prices, fragmented policies across countries, and negative perceptions of LPG as a fossil-based fuel.

3. What opportunities exist in the Europe liquefied petroleum gas market?

Opportunities in the Europe liquefied petroleum gas market include BioLPG adoption, integration with hybrid renewable systems, rural microgrids, and expanding infrastructure for cleaner, flexible off-grid energy solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com