Europe Machine Tools Market Size, Share, Trends, & Growth Forecast Report Segmented, By Product Type, Automation Type, Sales Channel (Direct Sales and Distributor Sales), End- User Industry, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$29.33 BnMarket Estimate, 2026

$31.17 BnMarket Forecast, 2034

$50.74 BnCAGR, 2026–2034

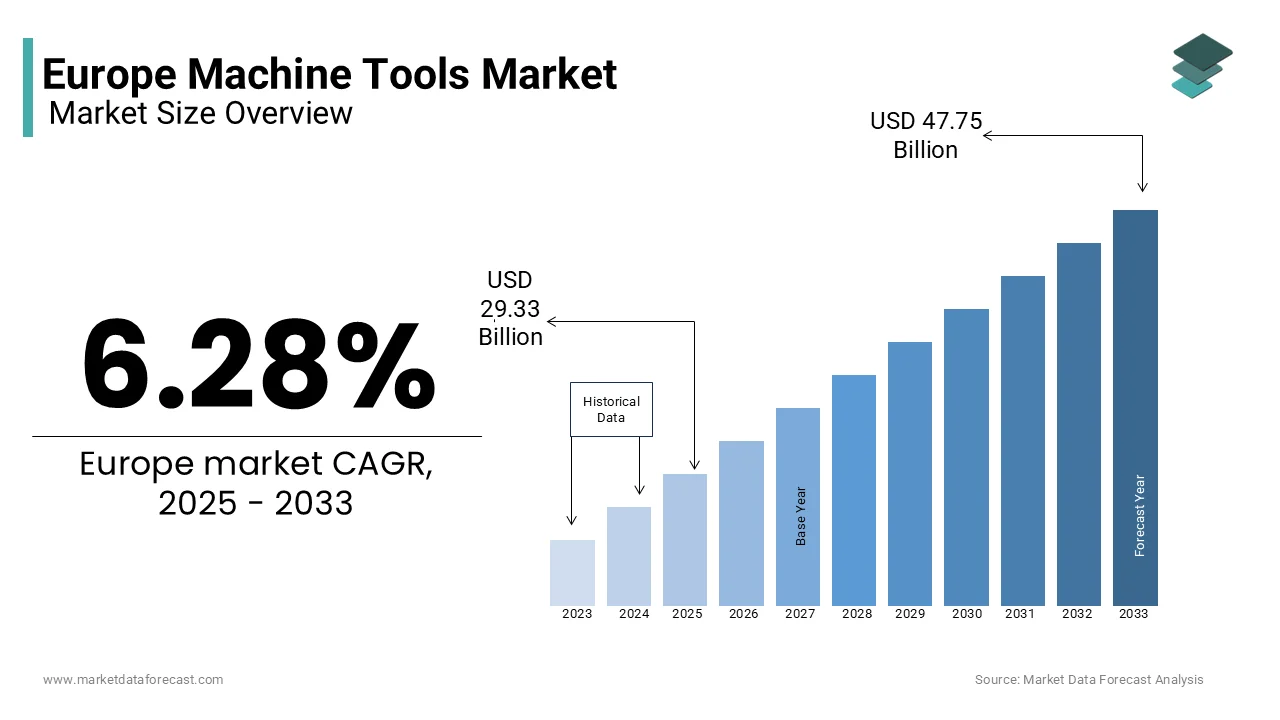

6.28%Europe Machine Tools Market Size

The European machine tools market was worth USD 29.33 billion in 2025 and is anticipated to reach USD 31.17 billion in 2026 and USD 50.74 billion by 2034. The European market is expected to grow at a CAGR of 6.28% from 2026 to 2034.

The resurgence of the automotive and aerospace industries post-pandemic has fueled demand for advanced machining solutions, which is greatly influencing the growth of the European machine tools market. Eurostat says over 60% of European manufacturers rely on high-precision CNC machines to meet stringent quality standards. Additionally, rising automation adoption across sectors like transportation and energy is propelling growth. As per the European Federation of Energy Traders, investments in renewable energy infrastructure have increased demand for specialized grinding and milling machines.

MARKET DRIVERS

Rising Automation Adoption Across Industries

Automation is transforming Europe’s industrial landscape, driving demand for advanced machine tools. CNC machine tools, integral to automated production lines, enable manufacturers to achieve higher precision and efficiency. Automation adoption reduces production costs by 20%, making machine tools indispensable. Furthermore, small and medium enterprises (SMEs), which constitute 99% of European businesses, are increasingly adopting automated solutions, further fueling market growth.

Resurgence of Automotive and Transportation Sectors

The automotive and transportation sectors are pivotal drivers of the European machine tools market. This resurgence is underpinned by the shift toward electric vehicles (EVs) and lightweight materials, both of which require specialized machining solutions. For example, turning and milling machines are essential for fabricating EV components like battery casings and motor housings. As per the European Transport Safety Council, investments in rail and aviation infrastructure are also boosting demand for large-scale grinding and drilling machines.

MARKET RESTRAINTS

High Initial Investment Costs

The substantial upfront costs associated with advanced machine tools pose a significant barrier to adoption. The financial burden is particularly challenging for SMEs. Smaller organizations often delay upgrades by hindering overall market growth, while larger enterprises can absorb these costs. Additionally, maintenance and training expenses further exacerbate the financial strain by creating resistance to adoption.

Supply Chain Disruptions and Raw Material Shortages

Supply chain disruptions and raw material shortages continue to challenge the European machine tools market. The global semiconductor shortage has impacted the production of CNC machines, which rely heavily on electronic components. Similarly, fluctuations in steel and aluminum prices have increased manufacturing costs by reducing profit margins for suppliers. As per the European Metals Trade Association, raw material prices surged by 25% in 2023, forcing manufacturers to pass on costs to end-users.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

Eastern European countries present untapped opportunities for the European machine tools market. According to the European Bank for Reconstruction and Development, nations like Poland, Romania, and Hungary are witnessing rapid industrialization, with manufacturing output growing at an average annual rate of 8%. These regions are investing heavily in automotive and machinery production, driving demand for milling and turning machines. As per the Central European Economic Review, collaborations with local distributors and government incentives make these markets highly attractive for machine tool manufacturers seeking to expand their footprint.

Integration with Smart Manufacturing Technologies

The integration of machine tools with smart manufacturing technologies offers immense growth potential. According to the European Digital Innovation Hub, over 50% of European manufacturers are adopting IoT-enabled machines to enhance productivity and reduce downtime. Electrical discharge machines (EDMs) equipped with real-time monitoring systems, for example, allow operators to optimize performance and predict maintenance needs. As per the European Technology Observatory, smart manufacturing solutions can increase operational efficiency by 30% by making them indispensable for industries like aerospace and energy. The manufacturers can unlock new revenue streams while addressing evolving customer demands by leveraging AI and machine learning.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.28% |

| Segments Covered | By Product Type, Automation Type, Sales Channel, End-User Industry, and Country |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled | Komatsu, Chiron Group SE, Spinner Machine Tools, Schuler AG, DMG Mori Aktiengesellschaft, Georg Fischer Ltd., Trumpf Group, Gleason Corporation, Flow International und Gebr. und Heller Maschinenfabrik GmbH. |

SEGMENTAL ANALYSIS

By Product Type Insight

The milling machines segment dominated the European machine tools market with 28.3% of the market share in 2024 due to their versatility, enabling the precise shaping of complex components used in the automotive and aerospace industries. According to Eurostat, milling machines accounted for €7.8 billion in sales in 2023, driven by their compatibility with lightweight materials like aluminum and composites. Additionally, advancements in multi-axis milling technology have enhanced their efficiency, making them indispensable for high-precision applications.

The electrical discharge machines segment is likely to achieve a CAGR of 6.2% in the foreseeable years, with their ability to handle intricate designs and hard materials. According to the European Advanced Manufacturing Institute, EDMs are increasingly adopted in mold-making and die-casting industries, where precision is paramount. Their integration with IoT systems allows for predictive maintenance, reducing operational costs by 25%. As per the European Machinery Directive, this segment’s growth is further fueled by rising demand for customized components in the medical and defense sectors.

By Automation Type Insight

The CNC machine tools segment was the largest and held 65.4% of the European machine tools market share in 2024. Their dominance is attributed to their ability to deliver unparalleled precision and repeatability, essential for industries like automotive and aerospace. Additionally, advancements in software integration have enhanced their usability by making them accessible even to SMEs.

The conventional machine tools segment is likely to grow with a CAGR of 5.8% throughout the forecast period. According to the European Manufacturing Federation, this growth is driven by their affordability and simplicity, by appealing to smaller workshops and repair facilities. As per the European Industrial Policy Framework, government subsidies aimed at modernizing traditional industries have further boosted adoption in Eastern Europe.

By Sales Channel Insights

The direct sales segment accounted for a dominant share of the European machine tools market in 2024, with the need for technical expertise and after-sales support, which manufacturers provide directly. According to the European Business Association, direct sales ensure seamless customization and faster resolution of issues by enhancing customer satisfaction.

The distributor sales segment is expected to register a CAGR of 7.3% in the coming years, with its ability to reach underserved regions. According to the European Retailers’ Association, distributors play a crucial role in expanding market access in Eastern Europe. Their localized presence and flexible payment options make them an attractive choice for SMEs.

By End-User Industry Insights

The automotive industry held 35.4% of the European machine tools market share in 2024, with the transition to EVs and lightweight materials, which require advanced machining solutions. The automotive manufacturers invested huge amounts in upgrading machining capabilities in 2023, which is attributed to fueling the growth of the segment.

The energy sector is projected to grow at a CAGR of 6.8% during the forecast period, with investments in renewable energy infrastructure. The wind turbine and solar panel production relies heavily on grinding and milling machines, which contribute to the growth of the market.

REGIONAL ANALYSIS

Germany Market Analysis

Germany dominated the European machine tools market with a 32.4% share in 2024. The growth of the market in this country is attributed to the robust manufacturing base in the automotive and machinery sectors, where over 70% of global machine tool innovations originate. According to Eurostat, German manufacturers invested €12 billion in advanced machining solutions in 2023, with their commitment to precision engineering. The country’s strong R&D ecosystem and government support for industrial modernization further fuel its position as the market leader.

Spain Market Analysis

Spain is projected to grow at a CAGR of 6.5% during the forecasted years, driven by investments in renewable energy and transportation infrastructure. The rise of smart manufacturing initiatives, supported by EU funding, has accelerated adoption. As per the European Renewable Energy Council, Spain’s emphasis on green technologies positions it as a key growth driver by making it the fastest-growing market in Europe.

COMPETITIVE LANDSCAPE

The Europe machine tools market is highly competitive, characterized by the dominance of established players like DMG Mori, Trumpf Group, and Haas Automation, alongside emerging firms focusing on niche segments. DMG Mori’s dominance is due to its specialization in high-precision CNC machines, while Trumpf’s focus on laser-based tools differentiates it from competitors. Haas’s affordability strategy appeals to budget-conscious clients, particularly SMEs. Regional fragmentation allows smaller innovators to carve out niches, fostering innovation. Pricing wars occasionally arise, particularly in cost-sensitive markets like Eastern Europe. Regulatory frameworks further intensify rivalry, as manufacturers must continuously adapt to evolving compliance requirements. Despite challenges, collaboration opportunities exist, especially in integrating green technologies and IoT-driven solutions. Overall, the competitive landscape reflects a balance between innovation-driven growth and strategic positioning by ensuring dynamic evolution over the forecast period.

KEY PLAYERS MARKET

A few of the notable companies in the European machine tools market are

- Komatsu

- Chiron Group SE

- Spinner Machine Tools

- Schuler AG

- DMG Mori Aktiengesellschaft

- Georg Fischer Ltd.

- Trumpf Group

- Gleason Corporation

- Flow International

- Gebr

- Heller Maschinenfabrik GmbH.

Top Players In the Market

- DMG Mori leads the market with a specialization in CNC milling and turning machines by catering to industries like automotive and aerospace. Its global footprint and focus on digitalization have strengthened its position in the marketplace.

- Trumpf Group is leveraging its expertise in laser-based machine tools. Trumpf’s innovations in electrical discharge machines (EDMs) have made it a preferred choice for mold-making and die-casting industries. Its collaborations with EU-based manufacturers further expand its reach.

- Haas Automation is focusing on affordability and reliability. As per the European Manufacturing Federation, Haas’s distributor network ensures accessibility across Europe in emerging markets like Eastern Europe, where cost-effective solutions are in high demand.

Top Strategies Used By Key Players

Key players employ strategies like product innovation, strategic partnerships, and sustainability initiatives. DMG Mori focuses on integrating AI into CNC machines, enhancing precision and efficiency. Trumpf emphasizes R&D, launching advanced laser cutting tools tailored for aerospace applications. Haas prioritizes affordability, targeting SMEs through cost-effective solutions. Additionally, all three companies align with EU sustainability goals, ensuring compliance with environmental regulations while meeting evolving customer needs.

RECENT MARKET NEWS

- In March 2024, DMG Mori launched its next-generation CNC milling machine in Europe. This initiative aims to enhance precision and efficiency for automotive manufacturers.

- In May 2024, Trumpf Group partnered with Siemens AG. This collaboration seeks to integrate IoT-enabled systems into laser cutting machines by improving real-time monitoring capabilities.

- In July 2024, Haas Automation announced a distribution agreement with TechData in Italy. This move enhances accessibility to affordable CNC machines, particularly for SMEs in underserved regions.

- In September 2024, DMG Mori expanded its Leipzig R&D center. This development ensures localized innovation for European clients by accelerating product customization.

- In November 2024, Trumpf initiated a training program for machine operators in France. This action addresses the talent gap in advanced machining technologies by fostering long-term industry growth.

MARKET SEGMENTATION

This European machine tools market research report has been segmented and sub-segmented into the following categories.

By Product Type

- Milling Machines

- Drilling Machines

- Turning Machines

- Grinding Machines

- Electrical Discharge Machines

By Automation Type

- CNC Machine Tools

- Conventional Machine Tools

By Sales Channel

- Direct Sales

- Distributor Sales

By End-User Industry

- Automotive

- Transportation and Machinery

- Sheet Metals

- Capital Goods

- Energy

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe machine tools market?

The Europe machine tools market comprises mechanical devices and systems—such as CNC machines, turning centers, milling machines, and grinders—used in metalworking and manufacturing processes across industries.

Why is the machine tools market important in Europe?

Machine tools are critical for automotive, aerospace, industrial equipment, precision engineering, and energy sectors, enabling automated, precise manufacturing and boosting productivity.

What are the main types of machine tools?

Key types include CNC machine tools, turning machines, milling machines, drilling machines, grinding machines, and specialized fabrication tools.

What drives growth in the Europe machine tools market?

Growth drivers include industrial automation, smart factory adoption, reshoring of manufacturing, investment in advanced production systems, and demand for precision parts.

Which industries use machine tools most?

Major end users include automotive, aerospace, defense, heavy machinery, electronics, medical devices, and general metal fabrication sectors.

How does technology influence the machine tools market?

Technologies such as CNC automation, robotics, IoT, AI-driven predictive maintenance, and digital twin systems improve accuracy, efficiency, and machine uptime.

What are key trends shaping the machine tools market?

Important trends include smart machining, additive manufacturing integration, hybrid production systems, energy-efficient machines, and AI-assisted tool path optimization.

What challenges does the European market face?

Challenges include cyclical demand fluctuations, high equipment costs, skills shortages, global supply chain disruptions, and pressure to adopt digital manufacturing.

How do regulations impact the machine tools market?

Regulations on workplace safety, energy efficiency, machine safety standards (CE marking), and emissions influence design, usage, and machine tool compliance.

Who are major players in the Europe machine tools market?

Leading companies include DMG MORI, TRUMPF, GROB-WERKE, Mazak Europe, Haas Automation, Okuma, and Bosch Rexroth, known for advanced machining solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com