Europe Meat Snacks Market Research Report Segmented By Product (Jerky, Meat Sticks, Pickled Sausages, Ham Sausages, And Pickled Poultry Meat), Meat Type (Poultry, Beef, Pork, And Others), Flavors (Original, Peppered, Teriyaki, Smoked And Others), Distribution Channel (Convenience Stores, Supermarket/Hypermarket, Grocery Stores, Restaurants, And Others), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Europe Meat Snacks Market Size

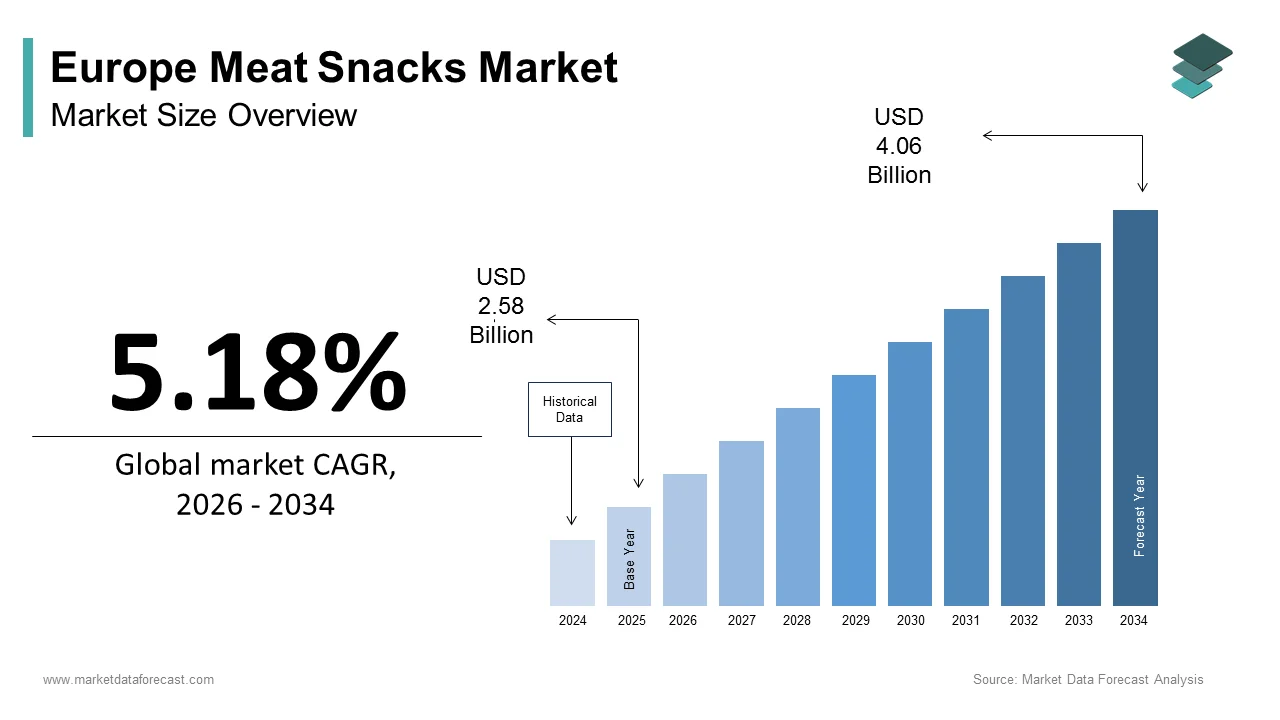

The size of the European meat snacks market was expected to be worth USD 2.58 billion in 2025 and is anticipated to be worth USD 4.06 billion by 2034, from USD 2.71 billion in 2026, growing at a CAGR of 5.18% during the forecast period.

Meat snacks encompass a diverse array of savory, protein-rich convenience foods derived from cured, dried, or cooked animal sources designed for immediate consumption without preparation. This category includes traditional delicacies such as beef jerky, salami sticks, prosciutto slices, and biltong alongside modern innovators like meat chips and protein bars infused with cured meats. The cultural significance of these products runs deep in European gastronomy, where regions like Italy and Spain have perfected artisanal curing techniques over centuries. According to the European Commission, the agri-food sector remains a cornerstone of the European economy, with meat products accounting for a substantial portion of household expenditure on processed foods. The shift toward high-protein diets is evident, as per data from the European Food Safety Authority, which indicates that protein intake recommendations are increasingly influencing consumer purchasing behavior across all age groups. Urbanization trends have altered eating patterns significantly, with the Organisation for Economic Co-operation and Development noting that a majority of Europeans now live in urban areas where demand for portable and shelf-stable nutrition is paramount. The rise of outdoor activities and travel further fuels the need for non-perishable food options that do not require refrigeration. Manufacturers are responding by blending traditional recipes with contemporary packaging solutions to extend shelf life while preserving authentic flavors that resonate with local palates.

MARKET DRIVERS

Surging Demand for High-Protein Dietary Regimens

The escalating consumer preference for high-protein diets is fuelling the growth of the European meat snacks market. Individuals are increasingly recognizing protein as essential for muscle maintenance, weight management, and sustained energy levels, leading to a deliberate shift away from carbohydrate-heavy snacks. As per the International Protein Board, protein consumption in Western Europe has risen significantly over the last decade, with athletes and fitness enthusiasts driving much of this growth. Meat snacks offer a convenient source of complete proteins containing all nine essential amino acids, which plant-based alternatives often struggle to provide in comparable bioavailability. The trend extends beyond gym goers to include busy professionals and older adults seeking to prevent sarcopenia. National health campaigns in countries like Germany and the United Kingdom emphasize adequate protein intake, reinforcing consumer confidence in meat-based products. Retailers have responded by dedicating more shelf space to protein-rich snack options, often positioning them near checkout counters for impulse purchases. The perception of meat snacks as a satiating option that curbs hunger longer than sugary treats further amplifies their appeal among weight-conscious consumers.

Influence of Traditional Culinary Heritage on Product Innovation

The rich tapestry of European culinary traditions provides a unique foundation for innovation within the European meat snacks market. Regions renowned for specific meat products, such as Parma in Italy for prosciutto or Jabugo in Spain for Iberico ham, serve as benchmarks for quality. As per European Union quality schemes, thousands of meat products hold Protected Geographical Indication status, which guarantees authenticity and fosters consumer trust. Artisanal producers are introducing gourmet snack versions of traditional charcuterie items that appeal to discerning palates. The fusion of time-honoured methods with modern convenience formats like single-serve sticks or vacuum-sealed slices bridges the gap between fine dining and on-the-go consumption. Consumer surveys conducted by Eurobarometer reveal that a majority of Europeans prioritize food origin and traditional production methods when making purchasing decisions. This cultural affinity encourages brands to highlight regional sourcing and family recipes in their marketing narratives. The export potential of these culturally rooted products also drives domestic production as international demand for authentic European meat snacks grows.

MARKET RESTRAINTS

Stringent Regulatory Frameworks on Food Safety and Additives

The rigorous regulatory environment governing food safety and additive usage in Europe presents a significant restraint on the European meat snacks market. The European Food Safety Authority enforces strict limits on nitrates, nitrites, and other preservatives commonly used in cured meats. As per recent assessments, permissible levels of these additives have been under continuous review due to potential health risks. Manufacturers face challenges in reformulating products to meet evolving standards without compromising shelf life or taste, often increasing production costs. Detailed labeling requirements regarding allergens and nutritional content add complexity, particularly for small and medium-sized enterprises. Cross-border trade within the EU is further complicated by varying national interpretations of directives. Consumer awareness of these regulations has heightened scrutiny on ingredient lists, causing some buyers to avoid heavily processed products. The cost of maintaining compliance with frequent updates diverts resources from innovation, slowing market momentum.

Health Concerns Regarding Processed Meat Consumption

Persistent health concerns surrounding processed meats act as a formidable barrier to the growth of the European meat snacks market. The classification of processed meat as a Group 1 carcinogen by the International Agency for Research on Cancer has had a lasting impact on consumer perception. As per the World Health Organization, regular consumption of processed meats is associated with increased risk of colorectal cancer. Public health campaigns in nations like France and Sweden promote reduced intake of salty and cured meats, contributing to a shift toward fresh or plant-based alternatives. High sodium content, typical of many meat snacks, exacerbates health worries given the prevalence of hypertension and cardiovascular diseases. Medical associations frequently advise limiting processed meat intake to occasional treats rather than staple snacks. This negative health narrative forces manufacturers to invest in cleaner label products with reduced salt and no added nitrates, though achieving comparable taste remains challenging. The stigma associated with processed meats continues to dampen enthusiasm among younger demographics who prioritize holistic wellness and preventive health measures.

MARKET OPPORTUNITIES

Expansion into Clean Label and Natural Formulations

The development of clean-label meat snacks offers a substantial opportunity for the European meat snacks market. By eliminating artificial preservatives, colors, and flavors, manufacturers can align their offerings with the values of health-conscious shoppers who scrutinize ingredient lists meticulously. As per the European Consumer Organisation, a majority of European consumers prefer products with short and recognizable ingredient lists, indicating a strong market pull for transparency. Innovations in natural preservation methods, such as celery powder, fermented extracts, and high-pressure processing, allow producers to maintain safety and shelf life without synthetic additives. Brands that successfully communicate their commitment to natural ingredients often command premium prices and foster strong loyalty among discerning customers. The trend extends to sourcing practices, with consumers favoring meats from animals raised without antibiotics or hormones and fed on organic diets. Retailers are increasingly creating dedicated sections for clean-label snacks, providing visibility and accessibility. Collaborations between food technologists and agricultural experts are driving novel textures and flavors that mimic traditional cured meats while adhering to strict natural standards.

Utilization of Alternative and Sustainable Protein Sources

Exploring alternative protein sources and sustainable production methods presents a transformative opportunity for the Europe meat snacks market. The rising interest in insect-based proteins and lab-grown meats offers a pathway to diversify product portfolios while reducing ecological footprints. As per the European Alternative Proteins Platform, investment in alternative protein startups has surged, with companies producing cricket flour and cultured meat snacks. These novel ingredients often boast superior nutritional profiles with significantly lower greenhouse gas emissions compared to beef or pork. Regulatory approvals for novel foods in the European Union are gradually expanding, enabling commercialization. Consumers, particularly millennials and Gen Z, are increasingly willing to try sustainable alternatives that align with environmental values. Manufacturers can leverage this sentiment by launching hybrid products blending traditional meats with plant or insect proteins. Partnerships with biotechnology firms and research institutions accelerate the refinement of taste and texture.

MARKET CHALLENGES

Volatility in Raw Material Prices and Supply Chain Disruptions

The instability of raw material prices and frequent supply chain disruptions pose a critical challenge to profitability in the Europe meat snacks market. Fluctuations in livestock feed, energy, and transportation costs directly impact production expenses. As per Eurostat, agricultural producer prices in the EU have experienced significant volatility due to geopolitical tensions, climate impacts, and disease outbreaks. The outbreak of African Swine Fever in several European countries has reduced pig populations, driving up pork prices unexpectedly. Supply chain bottlenecks, labor shortages, and logistical delays hinder the timely delivery of finished goods, resulting in stockouts. Small and medium-sized producers lack bargaining power compared to large conglomerates, forcing some to exit the market or raise prices disproportionately. Reliance on imported spices and packaging materials further exposes manufacturers to global currency fluctuations and trade barriers. Mitigation requires diversified sourcing strategies and contingency planning, though these are capital-intensive.

Intense Competition from Plant-Based Snack Alternatives

The rapid ascent of plant-based snack alternatives represents a formidable challenge to the European meat snacks market. The proliferation of vegan jerky, nut-based bars, and legume snacks provides substitutes that mimic meat textures and flavors without health or ethical concerns. As per the Good Food Institute Europe, sales of plant-based meat products have grown exponentially, with snacks being a primary driver. Major food corporations are investing heavily in R&D to improve the sensory experiences of plant-based snacks, appealing to flexitarians and meat reducers. Marketing narratives emphasize sustainability, animal welfare, and health benefits, resonating with environmentally conscious consumers. Retailers are allocating prime shelf space to these alternatives, sometimes at the expense of meat snacks. The price gap between meat and plant-based snacks is narrowing, making the latter more accessible. To remain competitive, meat snack manufacturers must innovate aggressively to highlight unique value propositions such as nutrient density or authentic taste.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.18% |

| Segments Covered | By Product, Meat Type, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Jack Link’s, Conagra foods, Meat snacks Group, Hormel Foods, King Elite Snacks, Marfood USA, and Tyson Foods. |

SEGMENTAL ANALYSIS

By Product Insights

The meat sticks segment dominated the market by holding the highest share of the European meat snacks market in 2025. The dominance of the meat sticks segment in the European market is driven by their unparalleled convenience, portability, and alignment with the on-the-go lifestyle prevalent across the continent. These products, often sold in single-serve packaging, require no preparation or utensils, making them ideal for commuters, students, and outdoor enthusiasts. The primary driver for this dominance is the integration of meat sticks into the daily routines of busy Europeans who seek quick protein sources between meals. As per the European Convenience Food Association, sales of ready-to-eat savory snacks in stick format have surged as they fit perfectly into the lunchbox culture and vending machine ecosystems found in offices and schools throughout Germany and the United Kingdom. The versatility of meat sticks allows manufacturers to experiment with various flavor profiles ranging from traditional spicy chorizo to modern teriyaki beef. Furthermore, the extended shelf life of these dried and cured products reduces food waste for both retailers and consumers. Major retail chains have expanded their private label offerings in this category, driving volume through competitive pricing and prominent shelf placement near checkout counters. The perception of meat sticks as a healthier alternative to carbohydrate-heavy snacks like chips or crackers further solidifies their market leadership.

The jerky segment is a promising segment and is estimated to witness a CAGR of 9.12% over the forecast period. This rapid expansion is fueled by the shifting consumer perception of jerky from a niche outdoor accessory to a mainstream high-protein superfood suitable for urban lifestyles. As per the European Health and Fitness Association, the number of gym memberships in Europe has exceeded 60 million, creating a massive addressable market for post-workout nutrition solutions where beef and turkey jerky are becoming staples. Manufacturers are responding by introducing premium jerky varieties made from grass-fed beef, free-range turkey, and exotic meats, often highlighting natural ingredients. The influence of American snack culture via digital media has also popularized jerky among younger demographics. Retailers are dedicating more shelf space to specialized jerky brands that offer unique textures and global flavors such as Korean BBQ or Peri Peri. The development of softer, more tender jerky textures has broadened its appeal to older consumers, thereby expanding the consumer base significantly.

By Meat Type Insights

The pork segment led the market by capturing the leading share of the European meat snacks market in 2025. The leading position of the pork segment in the regional market can be driven by the continent's rich culinary heritage and widespread production capabilities. Pork remains the most consumed meat in many European nations, particularly in Germany, Spain, and Poland, where traditional curing methods have created iconic snacks like salami sticks, chorizo, and prosciutto. As per the European Commission, pork accounts for a significant share of total meat consumption in the European Union, providing a vast raw material base that ensures a consistent supply and competitive pricing. The versatility of pork allows for a wide array of textures and flavor profiles, catering to diverse consumer preferences. Established supply chains and localized processing facilities reduce logistics costs and carbon footprints. Furthermore, pork snacks often benefit from Protected Geographical Indication status, such as Jamón de Huelva or Salame Felino, which enhances perceived quality and justifies premium pricing.

The poultry segment is emerging as the fastest growing meat type in the Europe meat snacks market and is projected to progress at a CAGR of 10.4% over the forecast period, owing to the perception of poultry, particularly chicken and turkey, as leaner and lower-fat alternatives to red meats. As per the European Food Safety Authority, consumers are increasingly seeking protein sources with reduced saturated fat content to manage cardiovascular health and maintain optimal body weight. The rise of flexitarian diets has significantly boosted demand for poultry snacks. Manufacturers are launching innovative poultry jerky and sausage sticks infused with herbs and spices to mimic the robust flavors of red meat snacks. Religious diversity in Europe, including significant Muslim and Jewish populations adhering to Halal and Kosher dietary laws, further expands the market. Additionally, the lower environmental impact of poultry farming appeals to eco-conscious buyers. Ready-to-eat grilled chicken strips and turkey roll-ups in convenience stores have made poultry snacks more accessible and appealing.

By Distribution Channel Insights

The supermarkets and hypermarkets segment occupied the major share of the European meat snacks market in 2025. The growth of the supermarkets and hypermarket segment in the European market is attributed to their extensive reach, diverse assortments, and competitive pricing. These large-format retailers serve as the primary shopping destination for most European households. As per Eurostat, supermarkets and hypermarkets account for over 60% of food and beverage retail sales in the European Union. Strategic placement of meat snacks in checkout aisles and healthy snacking sections maximizes visibility. These retailers stock a wide variety of brands, including premium artisanal options and private labels. Promotional activities such as buy-one-get-one-free offers and loyalty program discounts further incentivize purchases. The integration of online shopping platforms by major supermarket chains allows customers to order meat snacks for home delivery, blending physical presence with digital convenience.

The convenience stores segment is expected to witness the fastest CAGR of 8.14% over the forecast period in this regional market, owing to the increasing demand for immediate consumption and urbanization trends. As per the European Convenience Food Association, the number of convenience store visits has risen sharply as consumers prioritize time-saving shopping experiences. Meat snacks fit perfectly into the convenience store model as they are shelf-stable, portable, and require no preparation. Extended operating hours cater to non-traditional eating schedules. Fuel station convenience stores along highways provide lucrative avenues for travel-sized meat snacks targeting motorists and tourists. As urban density increases and the pace of life accelerates, convenience stores are becoming critical touchpoints for instant gratification food items.

REGIONAL ANALYSIS

Germany Meat Snacks Market Analysis

Germany stood as the largest market for meat snacks in Europe by commanding a share of 24.4% of the regional market in 2025. The leading position of Germany in the European market is driven by its deep-rooted sausage culture and high per capita meat consumption. The country's market status is defined by a strong tradition of Wurst culture, where meat snacks are not merely occasional treats but integral components of daily diets and social gatherings. As per the German Federal Ministry of Food and Agriculture, the average German consumes nearly 60 kilograms of meat annually, with a significant portion derived from processed and cured products like Bockwurst and Landjäger. The robust network of butcher shops and bakeries alongside modern retail chains ensures widespread availability. The rising trend of fitness and health consciousness has prompted manufacturers to introduce low-fat and high-protein variants of traditional snacks. The presence of major meat processing giants fosters innovation and efficient distribution networks. Furthermore, Germany’s strong export orientation influences domestic standards and product diversity.

Spain Meat Snacks Market Analysis

Spain held the second largest position in the Europe meat snacks market in 2025. The growth of Spain in the European market is attributed to its globally renowned cured meat industry and vibrant tapas culture. As per the Spanish Ministry of Agriculture, Fisheries and Food, Spain is the world leader in pig herd numbers within the EU, providing an abundant supply for iconic products like Jamón Ibérico and Chorizo. The social habit of tapeo or going for tapas, drives significant consumption of sliced cured meats in bars and restaurants. Protected Designation of Origin labels associated with Spanish hams and sausages enhance their value proposition. Tourism plays a crucial role as millions of visitors annually experience Spanish gastronomy and subsequently seek out these authentic products abroad. Local manufacturers are increasingly focusing on sustainable farming practices and modern packaging formats to expand accessibility.

Italy Meat Snacks Market Analysis

Italy is anticipated to record a prominent CAGR in the European meat snacks market during the forecast period, owing to its reputation for artisanal quality and diverse regional specialties. As per the Italian National Institute of Statistics, cured meats such as Prosciutto di Parma, Salame Milano, and Bresaola are staple items in Italian households. The strong presence of SMEs specializing in charcuterie creates a fragmented yet dynamic market. The Slow Food movement reinforces traditional production methods and local sourcing. Export demand for Italian meat snacks remains robust, encouraging rigorous quality standards. Retailers are offering pre-sliced and vacuum-packed versions to meet convenience demand.

France Meat Snacks Market Analysis

France is projected to account for a notable share of the European meat snacks market during the forecast period due to its sophisticated palate and strong appreciation for gourmet charcuterie. As per the French Agency for Food, Environmental and Occupational Health and Safety, charcuterie remains a beloved category despite health debates, with consumers willing to pay a premium for Label Rouge and Organic certified meats. The tradition of apéritif or pre-dinner drinks accompanied by sliced sausages and cured hams is deeply embedded in French social life. The rise of organic farming and free-range livestock rearing has led to a surge in demand for natural and additive-free meat snacks. Major retail chains have expanded their organic sections to include a wide variety of meat snacks. The influence of celebrity chefs and culinary media continues to elevate the status of charcuterie. Collaborative efforts between producers and tourism boards promote meat snacks as souvenirs.

United Kingdom Meat Snacks Market

The United Kingdom is expected to exhibit a healthy CAGR in the European meat snacks market during the forecast period due to a rapidly evolving consumer landscape and increasing adoption of global snack trends. As per the Department for Environment, Food and Rural Affairs, the UK has seen a notable rise in the consumption of beef jerky and turkey sticks, influenced by American snack culture and the growing popularity of low-carb diets. The presence of a diverse multicultural population has introduced a variety of flavored meat snacks ranging from peri-peri to teriyaki. The convenience store sector has expanded significantly, providing ample shelf space for innovative brands. Health concerns regarding processed meats have prompted reformulation with reduced salt and natural preservatives. The strong e-commerce infrastructure allows niche and premium brands to reach consumers directly. Government initiatives promoting healthy eating have also encouraged the development of balanced snacks.

COMPETITION OVERVIEW

The competition in the Europe meat snacks market is intense and characterized by a mix of global giants and strong regional players vying for consumer attention. Major international brands leverage their scale and marketing prowess to introduce innovative products and secure prime shelf space in large retail chains. Local artisans and specialized producers differentiate themselves through authentic recipes, premium ingredients, and geographical indications that appeal to discerning palates. The landscape is shifting as health consciousness drives demand for cleaner labels and lower-sodium options, forcing all participants to reformulate existing products. Price competition remains fierce, particularly in the mass market segment where private label offerings from supermarkets gain traction. Companies are increasingly investing in sustainability initiatives and transparent sourcing to build brand loyalty among eco-aware consumers. The rise of e-commerce has opened new channels for niche brands to reach direct consumers, bypassing traditional retail barriers. This dynamic environment fosters continuous innovation and strategic collaborations as firms strive to maintain relevance and capture market share in a rapidly evolving sector.

KEY MARKET PLAYERS

A few major players of the Europe meat snacks market include

- Jack Link’s

- Conagra foods

- Meat Snacks Group

- Hormel Foods

- King Elite Snacks

- Marfood USA

- Tyson Foods

Top Strategies Used by Key Market Participants

Key players in the Europe meat snacks market primarily focus on product innovation to meet evolving consumer preferences for healthy and convenient options. Companies frequently launch clean label variants with reduced sodium and no artificial preservatives to address health concerns. Strategic acquisitions of local artisanal brands allow large corporations to expand their portfolios with premium and authentic offerings. Investment in sustainable sourcing and ethical production practices helps firms build trust with environmentally conscious consumers. Expanding distribution networks through partnerships with convenience stores and online platforms ensures greater product accessibility. Marketing campaigns emphasizing high protein content and fitness benefits target active lifestyles and drive demand. These strategies collectively enable market participants to navigate regulatory challenges and capture growth opportunities in a dynamic, competitive landscape.

Leading Players in the Market

- Jack Link's Protein Snacks stands as a dominant force in the Europe meat snacks market by introducing premium beef jerky and protein-rich snacks to a wide audience. The company contributes significantly to the global market by setting standards for taste, texture, and protein content in savory snacks. Recent actions include the expansion of its manufacturing facilities in the United Kingdom to meet surging local demand and reduce import dependencies. The firm has also launched innovative product lines featuring clean label ingredients and reduced sodium content to align with European health trends. Strategic partnerships with major retail chains across Germany and France have increased shelf visibility and accessibility for consumers. By investing in sustainable sourcing practices and animal welfare initiatives, the brand strengthens its reputation among environmentally conscious shoppers. These efforts ensure continued growth and solidify its position as a leader in the high-protein snack category throughout the region.

- Hero Group plays a pivotal role in the Europe meat snacks market through its diverse portfolio of cured meats and savory snacks under various beloved regional brands. The company leverages its extensive distribution network to deliver high-quality meat products to millions of consumers across the continent. Recent initiatives involve the acquisition of niche artisanal producers to broaden its range of premium and organic meat snacks. This strategy allows Hero Group to cater to the growing demand for authentic and locally sourced delicacies. The firm is also investing heavily in research and development to create novel flavor profiles that appeal to younger demographics while maintaining traditional quality. Expansion into emerging markets within Eastern Europe further diversifies its revenue streams and reduces reliance on saturated Western markets. By focusing on innovation and strategic acquisitions, Hero Group enhances its competitive edge and reinforces its status as a key player in the European savory snack landscape.

- Campofrío Food Group maintains a significant presence in the Europe meat snacks market by offering a wide array of cured sausages and ready-to-eat meat products. The company is renowned for its commitment to quality and tradition, which resonates deeply with consumers in Spain and beyond. Recent actions include the launch of new product lines focused on health and wellness, such as low-fat and high-protein snack options. Campofrío has also strengthened its supply chain by integrating vertical farming practices to ensure consistent raw material quality. The firm actively engages in marketing campaigns that highlight the Mediterranean diet benefits of its products to attract health-conscious buyers. Expansion of its export capabilities has allowed Campofrío to reach new customers in Northern Europe, where demand for premium Iberian products is rising. Through continuous innovation and a focus on sustainability, Campofrío solidifies its leadership position and drives growth in the competitive meat snacks sector.

MARKET SEGMENTATION

This research report on the Europe market has been segmented and sub-segmented based on product, meat type, distribution channel, & region.

By Product

- Jerky

- Meat sticks

- Pickled Sausages

- Ham Sausages

- Pickled Poultry Meat

By Meat Type

- Poultry

- Beef

- Pork

- Others

By Distribution Channel

- Convenience stores

- Supermarket/Hypermarket

- Grocery stores

- Restaurants

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe meat snacks market?

Key drivers include rising health awareness, demand for protein-based diets, busy lifestyles, increasing on-the-go consumption, product innovation, and premiumization trends.

2. What are the key challenges faced by meat snack manufacturers in Europe?

Major challenges include strict EU food safety regulations, high raw material costs, growing vegan and plant-based competition, and concerns over processed meat consumption.

3. Which countries dominate the Europe meat snacks market?

Germany, the UK, France, Spain, and Italy are leading markets due to strong retail distribution networks and high demand for convenient protein snacks.

4. What are the most popular types of meat snacks in Europe?

Popular products include jerky, meat sticks, sausages, salami bites, and dried cured meat strips.

5. How is consumer preference for high-protein diets influencing the market?

The rising adoption of fitness-focused and ketogenic diets has significantly boosted demand for protein-rich meat snacks as a healthier alternative to traditional chips and sugary snacks.

6. What role does clean-label demand play in the market?

Consumers increasingly prefer meat snacks with natural ingredients, minimal preservatives, no artificial additives, and transparent sourcing, encouraging manufacturers to reformulate products.

7. How are private label brands impacting the market?

Private label offerings from major European retailers are increasing competition by offering affordable meat snack options, expanding market penetration.

8. What distribution channels dominate the Europe meat snacks market?

Supermarkets and hypermarkets hold the largest share, followed by convenience stores, specialty stores, and rapidly growing online retail channels.

9. What impact do EU food safety regulations have on production?

Strict labeling, traceability, hygiene standards, and animal welfare regulations increase compliance costs but ensure high-quality and safe products in the market.

10. What are the future trends expected in the Europe meat snacks market?

Future trends include premiumization, clean-label products, sustainable packaging, expansion of e-commerce sales, and hybrid meat-protein innovations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com