Europe Medical Coding Market Size, Share, Trends & Growth Forecast Report By Component, Classification System, End-user and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) – Industry Analysis From 2026 to 2034.

Europe Medical Coding Market Size

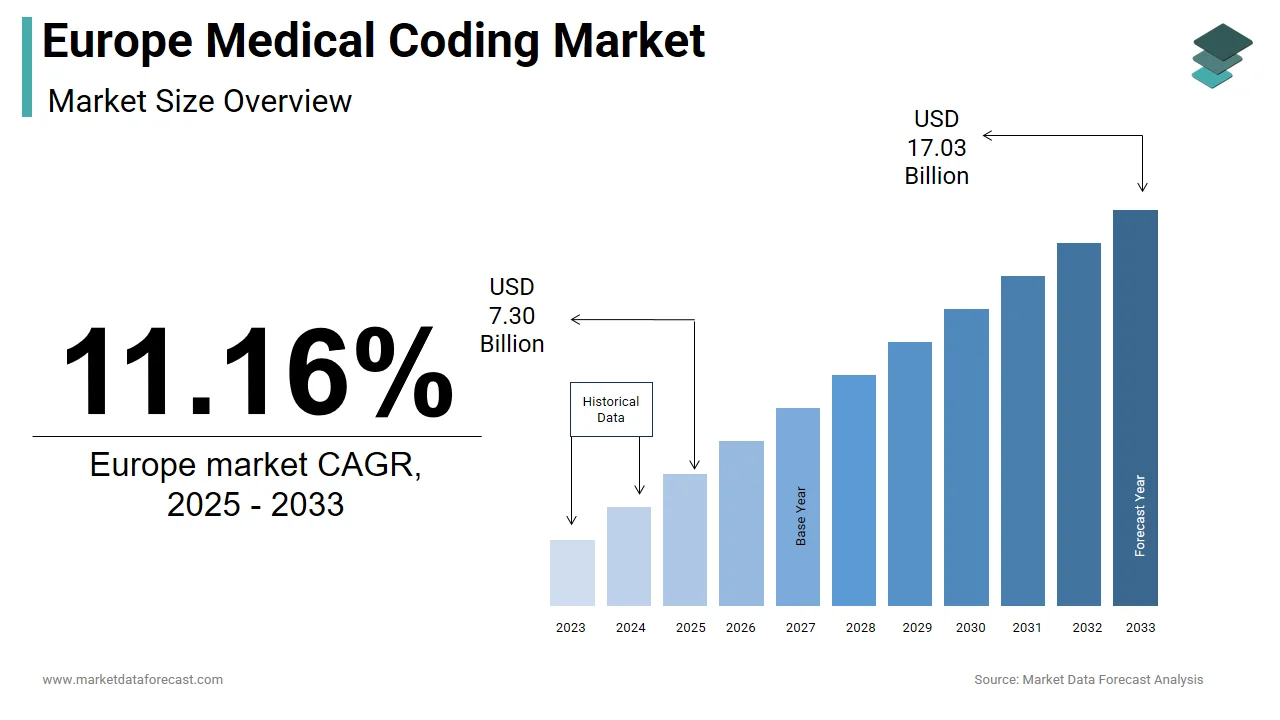

The medical coding market size in Europe was valued at USD 7.30 billion in 2025. The European market is estimated to be worth USD 18.92 billion by 2034 from USD 8.11 billion in 2026, growing at a CAGR of 11.16% from 2026 to 2034.

Medical coding entails the systematic conversion of clinical diagnoses, procedures, and healthcare services into standardized alphanumeric codes used for billing, reimbursement, data analytics, and regulatory compliance. These codes primarily follow the International Classification of Diseases (ICD) framework issued by the World Health Organization, often augmented by country-specific procedural classifications, such as Germany’s OPS, France’s CCAM, or the UK’s OPCS 4. The practice is foundational to the integrity of health information exchange across the European Union’s fragmented yet increasingly integrated healthcare systems.

European healthcare facilities manage large volumes of outpatient consultations annually, each generating codable clinical data. Many hospitals in the EU have implemented electronic health record systems, which further necessitate precise and auditable coding practices. Additionally, the EU Cross-Border Healthcare Directive mandates interoperable coding standards to facilitate treatment continuity and reimbursement across member states. Consequently, medical coding has transitioned from a back-office administrative task to a strategic component of health system efficiency, data governance, and fiscal accountability across Europe.

MARKET DRIVERS

Expansion of Cross-Border Healthcare and Health Tourism

The Cross Border Healthcare Directive of the European Union has catalysed demand for universally interpretable and nationally compliant medical coding, which is one of the key factors driving the regional market growth. This policy enables EU citizens to receive planned medical care in another member state and claim reimbursement from their home country’s insurer.

Across the EU, patients access cross-border care, with Germany, France, and Spain serving as principal destinations. Germany reports substantial volumes of cross-border treatments each year. Every episode demands dual coding competence, applying both ICD-10 for diagnoses and local procedural codes for services rendered. Discrepancies in coding between origin and destination countries can impede reimbursement, trigger audits, or result in financial loss. As a result, hospitals catering to international patients are investing in multilingual coders and hybrid coding platforms capable of mapping between national systems. This regulatory and demographic trend has institutionalized medical coding as a critical enabler of pan-European health mobility, thereby driving sustained market demand.

Regulatory Emphasis on Coding Accuracy and Audit Readiness

European health authorities have intensified oversight of medical coding to combat billing inaccuracies and ensure public fund accountability, which is further contributing to the regional market expansion.

Coding errors and inappropriate upcoding result in significant annual misallocated reimbursements across the EU. In response, several countries have mandated external coding audits: France and the Netherlands require them for hospitals managing large inpatient volumes. Germany’s Institute for the Hospital Remuneration System mandates certified coder validation for all Diagnosis-Related Group submissions. Furthermore, the European Health Data Space initiative, launched in 2022, stipulates that all secondary-use health data, including research and policy analytics, must be coded using standardized terminologies. Many medium to large hospitals in Western Europe have increased their coding department budgets to meet compliance requirements. This regulatory tightening transforms coding from a transactional function into a compliance cornerstone, reinforcing market growth.

MARKET RESTRAINTS

Inconsistent National Coding Systems Across Member States

Despite shared adoption of ICD-10 for diagnoses, European countries maintain disparate procedural coding frameworks, which are undermining interoperability and inflating administrative costs, and inhibiting the medical coding market growth in Europe.

The Organisation for Economic Co-operation and Development notes that this fragmentation impedes cross-national health data comparability and complicates pan-European health policy formulation. Many cross-border reimbursement claims require manual recoding due to incompatibilities between national systems. This recoding increases processing time and adds notable administrative overhead per claim. Smaller providers in Eastern Europe often lack the resources to maintain dual coding capabilities, limiting their participation in EU health initiatives. The absence of a unified procedural nomenclature not only complicates workforce training but also deters scalable coding service deployment, serving as a structural market restraint.

Shortage of Certified Medical Coders and Training Gaps

A significant deficit in certified medical coding professionals is also impeding the European medical coding market expansion.

Europe faces a shortage of certified medical coders, with workforce demand exceeding available supply. The shortage is especially acute in Central and Eastern Europe, where countries such as Romania and Bulgaria report very limited coder availability. Unlike the United States, Europe lacks a centralized accreditation body, resulting in inconsistent training standards and limited credential portability. Many EU hospitals experience claim submission delays due to coding staff shortages. Compounding the issue, curricula in many vocational institutions have not evolved to integrate electronic health record literacy or clinical reasoning. This human capital bottleneck impedes coding accuracy, audit preparedness, and system modernization, acting as a pronounced operational restraint.

MARKET OPPORTUNITIES

Adoption of Artificial Intelligence in Clinical Documentation

Artificial intelligence-powered coding tools offer a promising opportunity by automating code assignment from unstructured clinical notes, which is one of the promising opportunities for the European medical coding market. These systems use natural language processing to interpret physician documentation and map it to relevant ICD and procedural codes.

AI-assisted coding reduces manual effort and improves first-pass accuracy. Pilot programs in Sweden and the Netherlands demonstrated reductions in coding backlogs, as confirmed by national health technology assessment units. The European Commission’s Digital Europe Programme has committed significant funding through 2027 to support AI integration in health documentation. Crucially, the European Health Data Space framework mandates that AI tools comply with GDPR and qualify under the EU Medical Device Regulation, ensuring trust and legal alignment. This convergence of regulatory support, proven efficacy, and funding creates a high-growth pathway for AI-enabled coding solutions across Europe.

Integration of Medical Coding into Value-Based Care Models

The shift toward value-based reimbursement is expanding the role of medical coding beyond billing to performance measurement and risk adjustment, which is another potential opportunity for the European medical coding market.

Over 30% of healthcare payments in Germany, France, and the Netherlands are linked to quality or outcome metrics. These models require granular coding of comorbidities, complications, and social risk factors to calculate accurate risk scores. Germany’s morbidity-oriented risk structure compensation system, for instance, depends on Hierarchical Condition Category coding that demands greater clinical specificity than standard DRG coding. Enhanced coding granularity can improve risk adjustment accuracy, ensuring fair provider compensation. This evolution necessitates advanced coder training, real-time validation tools, and longitudinal data capture, all of which expand the scope and value of coding services. Consequently, coding vendors can develop new offerings in audit support, documentation improvement, and predictive coding analytics, unlocking significant market potential.

MARKET CHALLENGES

Data Privacy and Compliance Risks in Outsourced Coding

Outsourcing coding functions introduces substantial data governance and legal risks under the General Data Protection Regulation, which is one of the significant challenges to the European medical coding market.

The European Data Protection Board stipulates that violations involving health data can incur penalties of up to 20 million euros or 4% of global annual turnover. Such precedents have heightened institutional caution. Many EU healthcare providers now restrict coding outsourcing to vendors within national borders or those certified under the EU-US Data Privacy Framework. The absence of standardized contractual templates for health data processing across member states further complicates vendor agreements. These compliance burdens increase due diligence costs, limit access to global talent, and hinder the scalability of third-party coding services, posing a persistent market challenge.

Complexity of Multilingual Clinical Documentation

The linguistic diversity of Europe significantly complicates medical coding accuracy and efficiency, which further challenges the expansion of the medical coding market in Europe.

With 24 official EU languages and numerous regional dialects, clinical documentation varies widely in language and terminology even within single countries. In multilingual regions like Belgium and Switzerland, healthcare facilities often attribute coding errors to misinterpretation of non native clinical notes. Institutions managing three or more primary documentation languages face higher coding error rates. In Luxembourg, for example, records may be written interchangeably in French, German, or Luxembourgish. Few certified coders in the EU are proficient in more than two official EU languages. This linguistic fragmentation prolongs coding cycles, increases training complexity, and elevates compliance exposure, representing a deep-rooted operational and strategic challenge across the European medical coding landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Classification System, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | AT&T, BCE Inc., Charter Communications, Hughes Network Systems, LLC, Comcast, CenturyLink, KT Corp., LG Uplus Corp., Singtel, SK Broadband CO.LTD., T‑Mobile USA, Inc., Verizon, Viasat, Inc., and others. |

| Market Leaders Profiled | 3M, Health Information Systems, Optum, Cerner Corporation, McKesson Corporation, Dolbey, Nuance Communications, and Precyse Technologies |

SEGMENTAL ANALYSIS

By Component Insights

The in-house segment accounted for the major share of the European medical coding market in 2024 due to a strong preference among European healthcare providers for maintaining direct control over sensitive patient data and ensuring compliance with the General Data Protection Regulation. Hospitals, particularly in Germany, France, and the Nordic countries, prioritize internal coding teams to align documentation with national reimbursement frameworks and reduce audit risks. The regulatory complexity of country-specific coding systems, such as Germany’s OPS or France’s CCAM, further incentivizes reliance on in-house staff who possess contextual clinical and linguistic expertise. Many large hospitals in Western Europe retain full-time certified coders on payroll, citing data sovereignty and coding accuracy as key rationales. Additionally, national health authorities often mandate internal validation of coding outputs for Diagnosis-Related Group submissions, which entrenches the in-house model as the operational standard across the region.

The outsourced segment is on the rise and is estimated to register the fastest CAGR of 9.7% over the forecast period in the European medical coding market. The rising operational pressures on healthcare providers to reduce administrative costs while managing increasing patient volumes are majorly propelling the growth of the outsourced segment in the European market. Smaller hospitals and private clinics, particularly in Southern and Eastern Europe, lack the budget to maintain full-time coding departments and increasingly rely on specialized third-party vendors. Many clinics with fewer than 50 beds in Italy, Spain, and Poland reported outsourcing at least part of their coding functions. Simultaneously EU EU-funded digital health transformation programs are enabling secure cloud-based coding platforms that comply with GDPR standards, thereby mitigating earlier privacy concerns. Furthermore, the emergence of AI-assisted remote coding services allows vendors to offer scalable, near-real-time support with multilingual capabilities. Vendor-managed coding solutions are now integrated into a growing share of new electronic health record deployments in the EU, which further fuels the adoption of outsourced models, particularly among resource-constrained providers, and drives the growth of the outsourced segment in the European market.

By Classification System Insights

The International Classification of Diseases segment commanded the largest share of the European medical coding market in 2024. The dominance of the segment in the European market is rooted in the EU legal mandate that all member states use ICD-10 for morbidity and mortality reporting to ensure epidemiological consistency and public health surveillance. The European Centre for Disease Prevention and Control requires ICD-coded data for disease monitoring, pandemic response, and health policy formulation. Furthermore, national reimbursement mechanisms across the EU are intricately linked to ICD-based diagnosis coding, especially within Diagnosis-Related Group systems. Germany’s morbidity-oriented risk structure compensation model for outpatient care relies entirely on ICD-10-G codes to calculate risk-adjusted payments. As per a 2023 audit by the European Commission, 96% of inpatient claims submitted across 22 EU countries used ICD as the primary diagnostic coding standard. Additionally, the impending transition to ICD-11, which the WHO endorsed in 2022, is being actively piloted in countries like France and Sweden, further entrenching ICD’s structural role. This regulatory, institutional, and operational embeddedness makes ICD the de facto backbone of European medical coding.

By End User Insights

The hospital segment holds the largest share at 77% as reported by the European Hospital Association in 2024. Hospitals dominate due to their high volume of inpatient and outpatient encounters, complex billing requirements, and stringent regulatory obligations. Each inpatient discharge in the EU typically generates multiple codable events, including primary diagnosis, secondary conditions, procedures, and comorbidities. According to Eurostat, the average European hospital manages over 35,000 inpatient cases annually, necessitating a robust coding infrastructure. National reimbursement systems such as Germany’s G-DRG or France’s T2A are entirely dependent on accurate coding for payment calculation. According to the European Commission’s 2023 Hospital Compliance Review, 89% of public hospitals employ dedicated coding units to ensure audit readiness and prevent revenue leakage. Furthermore, hospitals serve as the primary sites for training and certification of coding professionals, with partnerships established with national health information management bodies. The integration of coding into hospital-based electronic health records and clinical documentation improvement programs further institutionalizes their central role. This combination of volume complexity, regulation, and infrastructure is primarily contributing to the dominance of the hospitals segment in the European market.

The diagnostic centers segment is predicted to register a CAGR of 10.8% over the forecast period in the European market, owing to the rapid expansion of outpatient care, decentralization of diagnostics, and the rise of specialized ambulatory centers. According to the Organisation for Economic Co-operation and Development, the number of independent diagnostic facilities in the EU increased by 18% between 2020 and 202,3, with significant growth in Spain, Italy, and Poland. These centers now conduct advanced imaging, molecular testing, and chronic disease screening, all of which require precise procedures and diagnosis coding for insurance claims. The European Commission’s 2024 Ambulatory Care Strategy emphasizes standardized coding for outpatient diagnostics to enable cross-regional data pooling and quality benchmarking. Additionally, private diagnostic chains are increasingly adopting cloud-based coding services to maintain compliance without incurring full-time staffing costs. As diagnostic care shifts away from hospitals toward community-based models, coding demand in this segment will continue to outpace the broader market.

COUNTRY LEVEL ANALYSIS

Germany Medical Coding Market Analysis

Germany occupied the largest share of the European medical coding market in 2024. Germany’s coding ecosystem is among the most advanced in Europe, driven by its mandatory Diagnosis-Related Group system, which ties hospital reimbursement directly to coded data. Germany processes over 20 million inpatient cases annually, with each case requiring up to 20 diagnosis and procedure codes. Germany’s Institute for the Hospital Remuneration System mandates that all DRG submissions be validated by certified coders who must complete 40 hours of continuing education every two years. The nationwide adoption of the OPS procedural classification alongside ICD-10 ensures granular documentation of medical interventions. Furthermore, Germany has pioneered the integration of coding into clinical workflows through hospital-based documentation improvement programs. Many German hospitals use real-time coding validation tools embedded within their electronic health records. This tight regulatory, technical, and educational infrastructure not only ensures coding accuracy but also establishes Germany as the benchmark for coding excellence and market scale in Europe.

United Kingdom Medical Coding Market Analysis

The United Kingdom captured the second-highest share of the European medical coding market in 2024. The growth of the medical coding market in the UK is attributed to its centralized National Health Service that mandates the use of ICD-10 for diagnoses and OPCS 4 for procedures across all public hospitals. The NHS processes over 18 million inpatient episodes annually, each requiring detailed coding for clinical coding statistics and payment by results. The Health and Social Care Information Centre requires all acute trusts to submit coded data within 28 days of discharge, which is a policy that has driven investment in coding automation and workforce training. According to NHS England, over 12,000 certified clinical coders are employed nationally with standardized training delivered through the Institute of Health Records and Information Management. Recent initiatives under the NHS Long Term Plan have prioritized coding for population health analytics and integrated care systems. According to the NHS, most trusts consistently achieve high levels of coding completeness. This combination of central oversight, high volume, and data-driven policy cements the UK’s position as a major and highly structured market for medical coding.

France Medical Coding Market Analysis

France is anticipated to account for a promising share of the European medical coding market over the forecast period, owing to the dual coding system using ICD-10 for diagnoses and the Classification Communale des Actes Médicaux for procedures, which is mandatory for all public and private healthcare providers. The national T2A reimbursement model allocates over 70 billion euros annually to hospitals based entirely on coded data. In 2023, France recorded around 15 million inpatient discharges each requiring multiple diagnosis and procedure codes. The Haute Autorité de Santé conducts annual coding audits and publishes facility-level coding quality scores that directly impact hospital funding. To address chronic coder shortages, France has launched the National Coding Academy, which trained over 1,200 new coders in 2023 alone. Many private clinics in France now use AI-assisted coding tools to meet mandatory submission deadlines. France’s blend of rigorous regulation, performance-linked funding, and national upskilling initiatives sustains its position as a high-integrity, high-volume coding market.

Italy Medical Coding Market Analysis

Italy is expected to exhibit a prominent CAGR in the European medical coding market during the forecast period. Italy’s coding infrastructure is characterized by regional variation yet unified under the national Diagnosis-Related Groups system, which uses ICD-9-CM for historical reasons, though a transition to ICD-10 is underway. Italy manages over 12 million hospital discharges annually, with coding required for both public reimbursement and EU health data reporting. The National Institute of Statistics mandates that all regions submit coded data for national health accounts and public health surveillance. A 2023 reform by the Agency for Regional Healthcare Services introduced mandatory coder certification and centralized coding audits for hospitals with over 10,000 annual admissions. Many large hospitals in Italy have integrated natural language processing tools to accelerate coding turnaround. Despite initial fragmentation, Italy’s recent standardization efforts and digital health investments under the National Recovery and Resilience Plan are consolidating its coding capabilities and market relevance.

Spain Medical Coding Market Analysis

Spain is projected to grow at a healthy CAGR in the European medical coding market during the forecast period. Spain’s coding system operates under the national CMBD database, which collects ICD-10 and NOMESCO-based procedural codes from all public hospitals. The country processes over 9 million inpatient episodes annually, with coding essential for autonomous community funding and EU health indicator reporting. The Spanish Agency for Health Quality requires hospitals to maintain high levels of coding completeness for inclusion in national performance dashboards. In 2023, the Ministry launched the National Coding Excellence Program, which trained 900 new coders and deployed AI coding assistants in reference hospitals. Many new electronic health record contracts in Spain now include integrated coding modules. Spain’s focus on regional coordination, coding quality, and public health analytics has elevated its coding maturity and solidified its role among Europe’s top five markets.

COMPETITIVE LANDSCAPE

The Europe Medical Coding Market features a competitive landscape shaped by both global health information firms and regional specialists. Competition centers on technical accuracy, regulatory alignment, and linguistic adaptability rather than price alone. Global players leverage AI-driven platforms and cross-border experience while local vendors offer deep knowledge of national coding rules and clinical documentation norms. The absence of a unified procedural coding system across the EU creates opportunities for niche providers who specialize in country-specific frameworks. At the same time, rising demand for audit readiness and value-based reimbursement intensifies pressure on vendors to deliver real-time coding validation and analytics. New entrants face high barriers due to stringent data privacy laws and certification requirements, yet innovation in cloud-based and multilingual coding tools continues to disrupt traditional models. This dynamic fosters a market where technological sophistication and regulatory fluency determine competitive advantage.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe medical coding market include

- 3M

- Health Information Systems

- Optum

- Cerner Corporation

- McKesson Corporation

- Dolbey

- Nuance Communications

- Precyse Technologies

TOP 3 PLAYERS IN THE MARKET

- 3M Company is a prominent participant in the Europe Medical Coding Market through its Health Information Systems division, which delivers advanced coding and documentation integrity solutions. The company provides AI-enabled computer-assisted coding platforms that support ICD-10 and country-specific procedural classifications across European healthcare systems. In recent years, 3M has deepened its integration with European electronic health record vendors and launched localized coding advisory services in Germany, France, and the UK. The company also collaborates with national health agencies to align its tools with regulatory audit requirements and reimbursement frameworks. These initiatives underscore 3M’s strategic commitment to enhancing coding accuracy and operational efficiency for European providers while reinforcing its global leadership in health information management.

- HIMSS Global is actively engaged in the Europe Medical Coding Market by promoting standardized health data practices and workforce development. While not a traditional coding vendor, HIMSS influences the market through policy advocacy, educational accreditation, and interoperability frameworks that shape coding adoption across the EU. The organization recently expanded its European Health Information Management certification programs to include country-specific coding modules for Italy, Spain, and the Netherlands. HIMSS also partners with the European Commission on the European Health Data Space initiative to ensure coding standards support secondary data use. These actions position HIMSS as a critical enabler of coding maturity and governance across the region, contributing to global efforts in health data standardization and workforce capacity building.

- Optum, a subsidiary of UnitedHealth Group, has extended its medical coding footprint into Europe by offering outsourced coding services and analytics platforms tailored to EU regulatory environments. The company leverages its global coding expertise to support cross-border billing for private hospitals and international patient programs, primarily in Switzerland, the UK, and the Netherlands. Optum recently deployed a multilingual natural language processing engine that interprets clinical notes in French, German, and Spanish and maps them to national coding systems. It also launched a GDPR compliant cloud coding platform in 2023, enabling European clinics to access real-time coding support without data residency concerns. These innovations reflect Optum’s strategy to adapt its global capabilities to Europe’s fragmented yet digitizing healthcare landscape.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Medical Coding Market employ several strategic approaches to strengthen their position. They invest heavily in artificial intelligence and natural language processing to automate coding and improve accuracy. Companies localize their platforms to comply with national coding systems such as Germany’s OPS and France’s CCAM. Strategic partnerships with electronic health record vendors ensure seamless integration into clinical workflows. Firms also expand multilingual support to address Europe’s linguistic diversity. Workforce development through certified training programs builds trust with healthcare institutions. Additionally, they align solutions with EU data privacy regulations like GDPR to enable secure outsourcing. Participation in policy dialogues with bodies like the European Commission enhances regulatory relevance. These strategies collectively drive differentiation, scalability, and compliance in a complex regional market.

MARKET SEGMENTATION

This Europe medical coding market research report is segmented and sub-segmented into the following categories.

By Component

- In-house

- Outsourced

By Classification System

- International Classification of Diseases (ICD)

- Healthcare Common Procedure Code System (HCPCS)

By End-User

- Hospitals

- Diagnostic Centers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the europe medical coding market?

The europe medical coding market involves coding patient data for diagnoses, procedures, and billing to improve healthcare documentation accuracy and reimbursement processes

2. What drives growth in the europe medical coding market?

Growth is fueled by rising healthcare digitization, ai integration, increased demand for coding accuracy, and expanded healthcare services across europe

3. Which countries lead the europe medical coding market?

Germany, the UK, France, and Italy lead the europe medical coding market due to advanced healthcare infrastructures and increasing coding service adoption

4. What coding systems are used in europe medical coding?

ICD-10 and the emerging ICD-11 are primary coding systems used in the europe medical coding market for standardizing global healthcare data

5. What is the role of outsourcing in the europe medical coding market?

Outsourced coding services dominate the europe medical coding market due to cost efficiency and access to skilled coders

6. How does ai impact the europe medical coding market?

AI improves coding accuracy, speeds up processes, and reduces errors, significantly advancing growth in the europe medical coding market

7. What challenges does the europe medical coding market face?

Challenges include regulatory complexity, shortage of skilled coders, and integration issues with healthcare systems in europe

8. How critical is training in the europe medical coding market?

Training is vital to ensure coding accuracy and compliance, supporting robust growth in the europe medical coding market

9. What trends shape the europe medical coding market?

Trends include increased cloud adoption, ai-driven automation, stricter regulations, and increased demand for remote coding services

10. How do regulations affect the europe medical coding market?

Strict healthcare data regulations shape market growth by enforcing standards for coding accuracy and patient data security

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com