Europe Healthcare BPO Market Research Report - Segmented By Provider Service, Payer Service, Pharmaceutical Service & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2024 to 2033)

Europe Healthcare BPO Market Summary

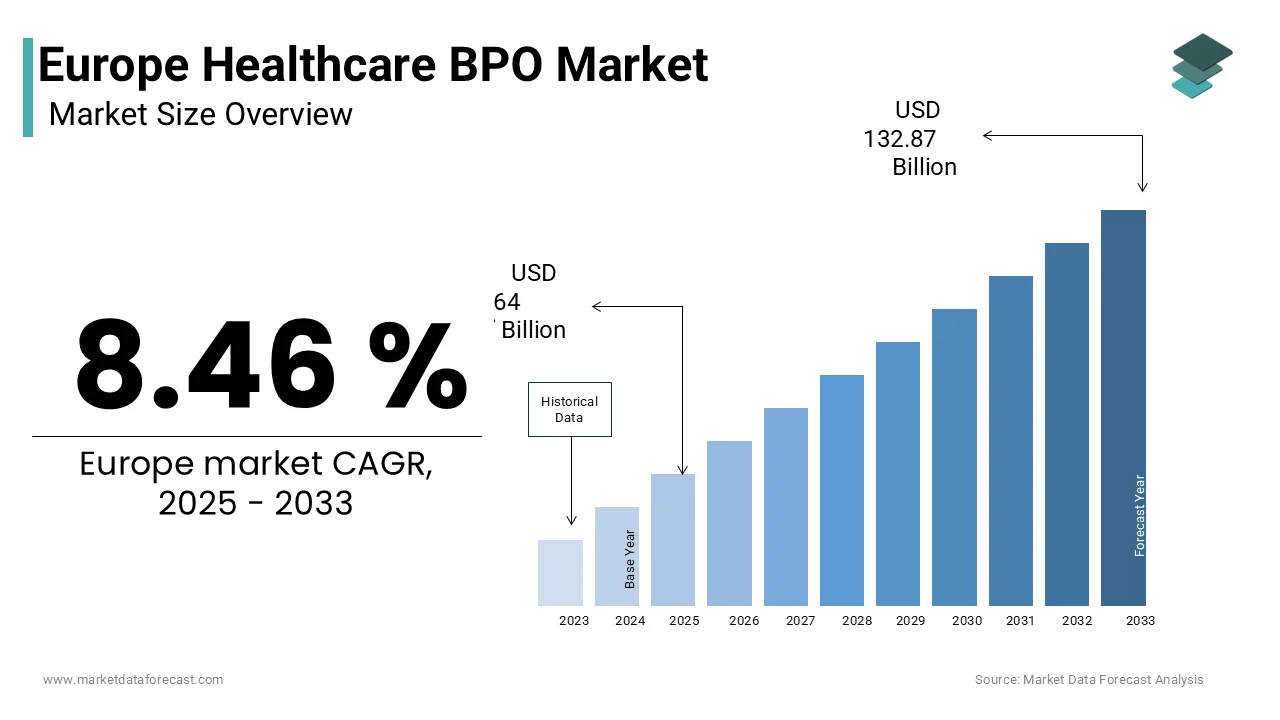

The Europe healthcare BPO market was valued at USD 58.42 billion in 2024, is estimated to reach USD 64.0 billion in 2025, and is projected to grow at a CAGR of 9.56% from 2025 to 2033, reaching USD 132.87 billion by 2033, driven by mounting administrative burdens, workforce shortages, GDPR-compliant outsourcing demand, and the expansion of value-based and digital healthcare models across Europe.

Market Snapshot

- 2024 Market Size: USD 58.42 billion

- 2025 Estimate: USD 64.00 billion

- 2033 Forecast: USD 132.87 billion

- CAGR (2025–2033): 9.56%

Quick Growth Drivers

- Rising administrative complexity in fragmented European healthcare systems

- Chronic shortages of healthcare and administrative staff

- Expansion of value-based care and integrated delivery networks

- Rapid digitization of healthcare workflows and EHR adoption

- Increasing demand for GDPR-compliant revenue cycle and claims management

Principal Restraints

- Stringent GDPR rules limiting offshore outsourcing models

- High costs of onshore and nearshore BPO delivery within the EU

- Restrictions on cross-border health data transfers

- Limited scalability compared to global BPO hubs

High-Value Opportunities

- GDPR-compliant analytics and fraud detection services

- AI-driven claims integrity and revenue cycle optimization

- Pharmacovigilance and real-world evidence services for life sciences

- Value-based care analytics, risk adjustment, and patient engagement

- Interoperable BPO platforms integrated with national EHR systems

Key Market Challenges

- Persistent shortage of skilled healthcare administrative professionals

- Fragmented national reimbursement, coding, and regulatory frameworks

- Rising cybersecurity and data-privacy risks

- High customization costs for multi-country service delivery

Fastest-Growing Segments

- Analytics & Fraud Management: 13.6% CAGR — AI-driven anomaly detection

- Pharmaceutical R&D Services: 11.8% CAGR — real-world evidence demand

- Claims Management: Largest segment (28.5% share in 2024)

- Non-Clinical Pharma Services: 62.3% share — pharmacovigilance & compliance

Regional Leadership & Dynamics

- Germany (22.4%) — complex multi-payer system, strict data laws

- United Kingdom (16.7%) — centralized NHS, strong digital health adoption

- France — aggressive anti-fraud focus, staffing shortages

- Netherlands — advanced health data interoperability, patient-centric care

- Sweden — value-based care leadership and national health registries

What Wins Commercially

- Onshore and nearshore EU delivery centers

- Deep expertise in country-specific DRG, ICD, and billing systems

- Multilingual service capabilities

- AI-enabled automation with human oversight

- Proven audit readiness and GDPR compliance

Top Strategic Ask for Executives

- Invest in AI-driven claims, fraud, and compliance analytics

- Build pan-European capabilities with strong local customization

- Prioritize data sovereignty, security, and interoperability

- Expand value-based care and life-sciences BPO offerings

- Develop continuous regulatory and coding upskilling programs

Leading Players

Some of the companies that are playing a dominating role in the Europe healthcare BPO market include:

- Infosys BPO Ltd.

- Cognizant Technology Solutions Corporation

- Genpact Limited

- Tata Consultancy Services Ltd.

- Accenture PLC

- Xerox Corporation

Europe Healthcare BPO Market Size

The European Healthcare BPO Market was valued at USD 58.42 billion in 2024, is expected to have 9.56% CAGR from 2025 to 2033, and be worth USD 132.87 billion by 2033 from USD 64 billion in 2025.

Healthcare business process outsourcing (BPO) is the practice of medical organizations hiring third-party service providers to manage specific administrative, financial, and clinical tasks. These services are designed to enhance operational efficiency, reduce administrative burden, and improve compliance within Europe’s complex and highly regulated healthcare ecosystems. Unlike generic BPO, healthcare BPO in Europe operates under stringent data protection mandates, most notably the General Data Protection Regulation, which requires strict controls over the processing of personal health information, including mandatory data processing agreements and restrictions on cross-border data transfers outside the European Economic Area. Healthcare systems throughout the European Union face persistent and significant staff shortages, particularly among core medical professions like doctors and nurses, a challenge exacerbated by an aging workforce and increasing demand for services. Efficiency improvements are a key focus for European healthcare systems. Reports suggest that leveraging digital innovation and health data could help substantially reduce administrative workloads for health professionals. The market is further shaped by aging populations, digital health adoption, and the integration of electronic health records, all of which increase demand for scalable, compliant, and technologically enabled support services that allow providers to focus on patient care rather than paperwork.

MARKET DRIVERS

Rising Administrative Burden in Fragmented European Healthcare Systems

The growing complexity and fragmentation of European healthcare delivery systems have significantly increased administrative workloads for providers, which boosts the growth of the European healthcare BPO market. This drives the demand for specialized outsourcing solutions. According to sources, clinicians in various European nations, including France and Italy, devote a significant amount of their work time to administrative tasks rather than direct patient care. Germany maintains a large number of statutory health insurance funds, each operating with variations in their specific procedures, which contributes to complexity in the healthcare system. Studies indicate that hospitals in Southern Europe frequently experience substantial delays in receiving reimbursement, often linked to challenges with medical coding accuracy and incomplete administrative documentation. This inefficiency not only strains resources but also impacts cash flow and care quality. Healthcare BPO providers address this by offering standardized revenue cycle management with trained coders fluent in national DRG systems ICD 10 and local billing protocols. The professionalization and centralization of administrative services assist providers in minimizing claim rejections and maximizing collection rates. This efficiency allows for staff to be reassigned to patient-facing roles, a move that aligns with Europe's overarching goal of value-based care.

MARKET RESTRAINTS

Stringent EU Data Privacy Regulations Limit Offshore Outsourcing Models

The European Union’s robust data protection framework, particularly the General Data Protection Regulation, acts as a major restraint on traditional offshore BPO models that rely on low-cost labor in non-EU jurisdictions. Consequently, this limits the expansion of the European healthcare BPO market. Under GDPR, personal health data may only be transferred outside the European Economic Area if the recipient country ensures an adequate level of protection or if specific safeguards such as standard contractual clauses are in place. Recent enforcement actions by data protection authorities show a notable focus on penalizing healthcare organizations for inadequate oversight of international data transfers and vendor compliance. This regulatory pressure has forced many European hospitals and insurers to either bring processes back in-house or shift to nearshore or onshore BPO providers located within the EU. An increasing number of healthcare organizations demonstrate a strong preference for business process outsourcing partners located within the EU, driven by a desire to reduce data transfer risks, even if it entails a higher cost. Consequently, the market is characterized by higher service costs and limited scalability compared to global BPO hubs like India or the Philippines, restricting the ability of providers to achieve significant cost savings through labor arbitrage.

MARKET OPPORTUNITIES

Accelerated Adoption of Digital Health and Interoperability Initiatives

The rapid digitization of the region’s healthcare infrastructure opens the way for advanced healthcare BPO services that integrate with electronic health records and national health information exchanges. This rapid digitization is thereby expected to fuel the growth of theEuropeane healthcare BPO market. The European Union is increasingly focused on developing a harmonized framework for electronic health records to facilitate secure and seamless cross-border health data exchange, moving away from paper-based systems and fragmented national approaches. This digital foundation generates vast volumes of structured and unstructured data requiring sophisticated management analytics and compliance oversight. BPO providers are evolving beyond transactional tasks to offer value-added services such as clinical documentation improvement, natural language processing for transcription,n anAI-powereded claims auditing that leverage these digital assets. In the Netherlands and Estonia, BPO firms collaborate with national health agencies to manage patient portal inquiries and appointment scheduling through secure digital channels. The European Investment Bank is providing substantial and diverse financial support, through loans and venture debt, to boost the research, development, and market expansion of digital health companies and infrastructure projects across the EU. Europe's maturing interoperability enables BPOs to transform from simple support to vital strategic allies in data-driven healthcare and administrative efficiency.

Expansion of Value-Based Care and Integrated Delivery Networks

The shift toward value-based care models across the region is creating new demand for specialized BPO services that support performance measurement, risk adjustment,t and patient engagement. This shift provides expansion possibilities for the European healthcare BPO market. Unlike fee-for-service systems, which prioritize transaction volume,e value-based contracts require accurate risk scoring, quality reporti,ng and proactive care coordination—functions that generate significant administrative complexity. Across Europe, there is an increasing policy emphasis on developing and implementing various integrated care approaches to improve health systems, though specific data on the number of operational models and patient coverage is not maintained by the ECDC. National health systems, such as those in Sweden and Denmark, often have robust mechanisms for monitoring and publicly reporting comprehensive sets of quality indicators related to healthcare performance and public health initiatives. Healthcare BPO providers are responding by offering bundled services that include data aggregation from disparate sources, risk stratification algorithm application,n and patient outreach via multilingual call centers. Recent pilot programs within various health systems, including in Germany, have explored the use of patient navigation services and have shown promising results in improving care coordination and reducing potentially preventable hospital readmissions. The expansion of value-based contracts within the EU's Chronic Disease Strategy elevates the strategic importance of BPO firms capable of delivering analytics-driven population health support, helping providers satisfy contractual requirements and improve outcomes.

MARKET CHALLENGES

Persistent Shortage of Skilled Healthcare Administrative Workforce

The chronic shortage of trained administrative professionals across the region’s healthcare sector remains a barrier for thEuropeanpe healthcare BPO market. This is a critical challenge limiting internal capacity and amplifying reliance on BPO. Projections indicate a considerable future shortage of healthcare administrative staff in the region. Factors contributing to this trend include an aging workforce, increasing early retirements, and competition from the private sector for skilled personnel. Certain nations are experiencing high vacancy rates for specific roles, leading to delays in processing and revenue issues, with audits revealing many departments are understaffed, resulting in extended claim submission times. You can read the full report at the European Commission’s website. This human resource gap is exacerbated by the increasing complexity of coding systems such as ICD 11 and the need for continuous training on evolving payer rules. The BPO model provides an answer, but the challenge of finding qualified staff persists, impacting the ability of service providers to fill roles. The administrative bottleneck will continue to hinder system efficiency and maintain dependence on external partners, who are themselves unable to scale skilled teams, until comprehensive, EU-wide training programs and defined career paths are created.

Fragmented National Regulations and Reimbursement Systems

The lack of harmonization in healthcare regulations, reimbursement policies, and coding standards across European Union member states poses a formidable operational challenge to the European healthcare BPO market. Consequently, this complexity hinders healthcare BPO providers seeking to deliver pan-European services. Each country maintains its own diagnosis-related group system, billing codes, pre-authorization requirements, and payer rules, creating a highly fragmented landscape that defies standardization. A provider serving clients in Germany, France, and Spain must maintain three separate teams trained in local regulations, each with its own compliance protocols and quality assurance metrics. This fragmentation increases operational cost,s reduces economies of scale,, le and limits the ability of BPO firms to leverage centralized technology platforms. While the European Commission has initiated efforts toward coding harmonization through the eHealth Net, progress remains slow due to national sovereignty over health systems. A lack of consistent regulatory standards across Europe results in significant customization expenses and service inconsistencies for BPO providers, challenges likely to persist without greater alignment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Payer Service, Pharmaceutical Service, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Infosys BPO Ltd., Cognizant Technology Solutions Corporation, Genpact Limited, Tata Consultancy Services Ltd., Accenture PLC and Xerox Corporation. |

SEGMENTAL ANALYSIS

By Payer Service Insights

The claims management segment remained the largest segment in the European healthcare BPO market by capturing a 28.5% share in 2024. Factors such as the complexity of multi-payer reimbursement systems and the high cost of claim errors across fragmented European health insurance landscapes have contributed to the prominence of the claims management segment. In countries like Germany and France, statutory health insurers operate alongside private funds,s each with distinct coding rules, documentation requirements, and payment timelines. Claim denial frequency shows consistency across various regions within the consortium. A significant portion of these rejections is often linked to issues arising from administrative processes. The frequency of these denials presents challenges to the consistent flow of funds for service providers. Analysis of data suggests that billing inefficiencies contribute to a noticeable reduction in the average annual revenue of healthcare facilities. The impact on revenue is a general pattern, not limited to a single type of facility or region. BPO providers address this through specialized teams trained in national DRG systems, CD 10 coding, and local insurer protocols offeringg end-to-end claim lifecycle management from submission to appeals. The integration of AI-powered audit tools further enhances accuracy by flagging inconsistencies before submission. As value-based care expands and documentation requirements intensify, claims management remains amission-criticall function where even marginal improvements in accuracy yield significant financial returns for both payers and providers across Europe.

The analytics and fraud management segment is predicted to witness the highest CAGR of 13.6% between 2025 and 2033. The rapid acceleration of the analytics and fraud management segment is fueled by rising financial losses from fraudulent claims and the European Union’s intensified focus on healthcare integrity. Healthcare fraud results in substantial financial losses across European public healthcare systems. In response, national health authorities are mandating advanced analytics for real-time anomaly detection. German statutory insurers are increasingly adopting advanced data analytics and predictive modeling to enhance their fraud detection capabilities. BPO firms are deploying machine learning algorithms that analyze billions of historical claims to identify patterns indicative of fraud, waste or abuse. Pilot programs employing machine learning for fraud detection have demonstrated significant improvements in identifying fraudulent claims more accurately and efficiently. The European Union's comprehensive data regulation facilitates secure, cross-border access to and pooling of health data for public interest purposes, while implementing strict privacy and security controls. This segment is evolving its approach from reactive auditing to proactive integrity assurance in response to mounting regulatory pressure and maturing AI, proving crucial in safeguarding Europe's public and private health funds.

By Pharmaceutical Service Insights

The non-clinical services segment held the majority share of 62.3% of the European healthcare BPO market in 2024 because of the industry’s strategic shift toward outsourcing administrative and commercial support functions. These services include pharmacovigilance, medical information management, drug safety reporting, regulatory documentation, and customer support for patient assistance programs. According to the European Medicines Agency, there has been an increase in the number of individual case safety reports submitted by pharmaceutical companies. The EU’s Good Pharmacovigilance Practices mandate 24/7 monitoring and rapid signal detection, requiring scalable multilingual teams that most manufacturers lack internally. BPO providers with EU-based delivery centers offer certified expertise in EudraVigilance reporting, ICSR processing, ng and aggregate safety report preparation, ion ensuring compliance with EMA and national competent authority requirements. Additionally, the expansion of specialty drugs with complex administration protocols has increased demand for outsourced patient support services, including reimbursement navigation and adherence counseling. More pharmaceutical companies are outsourcing at least one non-clinical function to maintain compliance and control costs.

The research and development segment is estimated to register the fastest CAGR of 11.8% during the forecast period. The rapid surge of the research and development segment is propelled by the rising complexity and cost of drug discovery, compounded by regulatory demands for real-world evidence and advanced analytics. The European pharmaceutical industry maintains a high level of investment in research and development, reflecting an ongoing commitment to innovation and drug discovery across Europe. BPO providers are increasingly engaged in early-phase data management, biostatistics, clinical trial monitoring,g and real-world data curation from electronic health records and wearables. The European Medicines Agency (EMA) actively encourages the use of real-world evidence and data sharing through ongoing initiatives to support regulatory decision-making and accelerate the approval of new medicines. Companies like IQVIA and Parexel have established dedicated EU data hubs in Ireland and the Netherlands,s compliant with GDPR and EMA standards, ds to support decentralized trials aAI-drivenven target identification. Furthermore, the European Union's comprehensive Horizon Europe program provides substantial funding for collaborative health research and innovation projects, often involving extensive partnerships and the use of external data management and strategy support. R&D business process outsourcing (BPO) is transforming into a strategic scientific partnership as drug development requires more data and collaboration, which enables faster and more efficient innovation cycles.

COUNTRY LEVEL ANALYSIS

Germany Healthcare BPO Market Analysis

Germany was the dominant country in the European healthcare BPO market and accounted for a 22.4% share in 2024. The supremacy of the German market is attributed to its complex multi-payer system, stringent data laws, and high administrative cost base. The country’s statutory health insurance framework comprises numerous sickness funds, each with distinct billing protocols, ls creating immense demand for specialized claims management and provider enrollment services. The German healthcare system is actively pursuing efficiency gains by encouraging hospitals and insurers to streamline operations and focus on core medical services, often leading to a reduction in non-essential in-house functions. The Federal Data Protection Act imposes additional constraints beyond GDPR, requiring BPO providers to maintain onshore data centers and undergo annual audits. Major players like Deutsche Telekom Healthcare and Swiss Post Solutions have established large German delivery centers staffed with certified coders and legal experts. The German Digital Healthcare Act and related regulations are accelerating the push for a comprehensive digital infrastructure, including the widespread adoption of electronic health records and mandatory electronic billing, to enhance efficiency and connectivity across the healthcare system. This combination of regulatory complexity, operational scale, ale and digital transformation makes Germany the cornerstone of Europe’s healthcare BPO ecosystem.

United Kingdom Healthcare BPO Market Analysis

The United Kingdom was the second largest region in Europeanrope healthcare BPO market by capturing a share of 16.7% in 2024. The growth of the UK market is supported by its centralized National Health Service structure and leadership in digital health integration. A significant majority of healthcare organizations have transitioned administrative functions, such as revenue cycle management and patient access, to specialized external partners. The adoption of these partnerships serves as a strategic response to persistent workforce constraints while facilitating the modernization of legacy back-office systems. The shift toward integrated care models has necessitated more robust frameworks for data sharing across primary, secondary, and social care sectors. This requirement for interoperability has generated increased reliance on external expertise for data harmonization and the management of population health analytics. Strategic initiatives now favor the implementation of centralized navigation hubs to streamline patient pathways across large geographic regions. The use of dedicated service providers for medical transcription and documentation continues to be a standard approach for improving operational efficiency within clinical settings. The UK’s post Brexit data regime aligns closely with GDPR but allows greater flexibility for domestic data processing, enabling local BPO growth. Additionally, the Medicines and Healthcare products Regulatory Agency’s real-world evidence framework drives pharmaceutical R and D outsourcing. This blend of system-scale policy innovation and regulatory clarity positions the UK as a high-value market for advanced healthcare BPO services.

France Healthcare BPO Market Analysis

France holds a noteworthy position in the European healthcare BPO market, which is driven by its dual public-private insurance model and aggressive anti-fraud initiatives. The volume of claims processed annually by the French health insurance system remains consistently high, while the estimated financial losses due to healthcare fraud represent a significant and ongoing challenge that authorities are actively addressing. This has spurred investment in outsourced analytics and audit services. Authorities in France are increasingly focusing on modernizing fraud detection methods, including exploring data-driven and predictive techniques as part of a broader push to reduce financial losses in the healthcare system. France also faces severe administrative staffing shortages. Recent reports from the French Hospital Federation highlight persistent and widespread staffing shortages across various hospital departments, contributing to significant operational challenges and increased delays in patient care and administrative processes. BPO providers like Atos and Capgemini have developed specialized centers in Lyon and Toulouse offering multilingual claims adjudication and medical coding compliant with the CCAM classification system. The government’s digital health strategy further fuels demand for patient portal management and telehealth support services. France’s unique mix of fraud pressure, workforce gaps, and digital ambition makes it a critical market for compliance-driven BPO innovation.

Netherlands Healthcare BPO Market Analysis

The Netherlands grew steadily in the European healthcare BPO market due to its integrated health data infrastructure and patient-centered care philosophy. The use of electronic patient records in the Netherlands is widespread among healthcare providers, with an increasing emphasis on a secure, national infrastructure for electronic data exchange. Recent legislative efforts, such as the Wekiz act, aim to make electronic data exchange obligatory and standardize the systems used for greater interoperability. Dutch health insurers routinely outsource member management, patient engagement,t and chronic disease support to specialized firms that operate multilingual contact centers with real-time access to health records under strict privacy protocols. Health insurers and healthcare providers are increasingly implementing personalized coaching and medication adherence programs to manage chronic conditions like diabetes. These initiatives are part of a broader trend toward leveraging eHealth solutions to improve patient outcomes and potentially reduce hospitalizations. The Netherlands also hosts major pharmaceutical BPO hubs serving the Benelux region with expertise in EU regulatory submissions and pharmacovigilance. The government’s Health Data Strategy emphasizes ethical AI and data reuse, creating opportunities for BPO firms offering compliant analytics and real-world evidence generation. This ecosystem of data integration, patient empowerment,t and regulatory sophistication positions the Netherlands as a model for next-generation healthcare BPO in Europe.

Sweden Healthcare BPO Market Analysis

Sweden is likely to grow in the European healthcare BPO market from 2025 to 2033, owing to its advanced value-based care models and universal health registry infrastructure. The country’s 21 regional health authorities operate under contracts that tie provider payments to over 50 quality and outcome metrics requiring robust data collection, analytics, and reporting, functions increasingly outsourced to specialized BPO partners. Healthcare regions in Sweden frequently engage external organizations and utilize a mix of public and private providers to manage aspects of their health services and support quality and data collection. Sweden’s national patient register links diagnoses and outcome data for the entire population, enabling BPO firms to deliver predictive analytics for chronic disease management and hospital readmission prevention. Regional healthcare systems are increasingly implementing digital tools and data-driven initiatives to improve patient outcomes and streamline care coordination for complex conditions. The Swedish Data Protection Authority enforces strict GDPR compliance but supports domestic data processing for public health purposes, creating a favorable environment for local BPO growth. This focus on outcomes,s data transparency,cy and preventive care makes Swedenhigh-impactact market for strategic rather than transactional healthcare BPO services.

COMPETITIVE LANDSCAPE

The European healthcare BPO market features intense competition among global IT services giants, specialized healthcare outsourcers,s and regional players, all operating within a highly regulated and fragmented environment. Competition is defined not by cost arbitrage but by regulatory compliance,e linguistic proficiency,,ncy and a deep understanding of national healthcare systems. Large firms like Accenture and TCS leverage scale technology and EU-based delivery centers to serve pan-European clients, while niche providers focus on specific domains such as pharmacovigilance or medical coding. The market is highly sensitive to data pprivacywith GDPR acting as a de facto barrier to offshore models and favoring providers with local infrastructure. Differentiation stems from value-added services such as predictive analytics, fraud detection,n and patient navigation, rather than basic transaction processing. Provider selection is driven by proven expertise in country-specific workflows, audit readiness,s and ability to integrate with national digital health infrastructures. As value-based care and data-driven decision making expand,d demand is shifting toward strategic partners who can deliver insights and outcomes, es not just administrative efficiency. Success requires balancing technological innovation with unwavering adherence to Europe’s complex legal and cultural healthcare landscape.

KEY MARKET PLAYERS

The top companies that occupied the majority of the shares in the European healthcare BPO Market in the recent past are

- Infosys BPO Ltd.

- Cognizant Technology Solutions Corporation

- Genpact Limited

- Tata Consultancy Services Ltd.

- Accenture PLC

- Xerox Corporation

TOP LEADING PLAYERS IN THE MARKET

- Accenture plc plays a pivotal role in tEuropeanope healthcare BPO market through its intelligent operations platform that integrates automation, artificial intelligence,ce and deep healthcare domain expertise. The company serves national health systems, private insurers,s and pharmaceutical firms across the continent with services spanning revenue cycle management,nt patient engagement, and real-world data analytics. Accenture emphasizes GDPR compliant data handling through its EU-based delivery centers in Ireland, Poland, and the Netherlands. It also expanded its pharmacovigilance analytics hub in Dublin to support EMA regulatory requirements for life sciences clients. Accenture is reinforcing its standing as a key strategic partner in the European healthcare administrative landscape by merging scalable technological solutions with in-depth knowledge of local regulations.

- Infosys Limited contributes significantly to the European healthcare BPO market by delivering end-to-end administrative and clinical support services tailored to European data sovereignty and compliance standards. The company operates dedicated EU delivery centers in the Czech Republic and Ireland, staffed with multilingual teams certified in ICD-10-DRG and national billing protocols. Infosys leverages its Topaz AI platform to automate prior authorization claims adjudication and patient scheduling while ensuring full adherence to GDPR and national health data laws. It also partnered with a leading Dutch health insurer to develop a fraud detection engine that analyzes cross-provider utilization patterns to flag anomalies in real time. These initiatives underscore Infosys’s commitment to localized innovation within Europe’s complex healthcare ecosystem.

- Tata Consultancy Services Limited is a key player in the European healthcare BPO space, offering specialized services in medical coding,n pharmacovigilancee ande revenue cycle management and health data analytics. The company maintains GDPR compliant delivery operations in Spain and Hungary with teams trained in country-specific coding systems, such as Germany’s G-DRG and France’s CCAM. TCS integrates its Machine First delivery model with healthcare workflows to automate repetitive tasks like claim scrubbing and eligibility verification while maintaining human oversight for complex cases. It also expanded its medical information management center in Barcelona to handle multilingual inquiries for specialty drug launches across Southern Europe. TCS is solidifying its presence in Europe's stringent BPO sector through a strategic combination of regulatory alignment, technological sophistication, and linguistic proficiency.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in theEuropeane healthcare BPO market prioritize strict adherence to GDPR and national data protection laws by establishing onshore or nearshore delivery centers within the European Economic Area. They invest in multilingual teams certified in country-specific coding, billing, and regulatory frameworks to ensure local compliance and accuracy. Companies integrate artificial intelligence and automation into core workflows to enhance efficiency while maintaining human oversight for complex clinical and compliance decisions. Strategic partnerships with national health agencies, integrated care systems,s and pharmaceutical firmenable thele development of tailored solutions for claims integrity, patient engagement, and real-world evidence generation. Firms expand specialized capabilities in high-growth areas such as fraud analytics, pharmacovigilance, and value-based care reporting to move beyond transactional outsourcing. Continuous training programs ensure staff remain updated on evolving EU regulations, coding standards, and payer policies. Additionally, they leverage secure cloud platforms that enable interoperability with electronic health records and national health information exchanges while preserving data sovereignty and auditability across Europe’s fragmented healthcare landscape.

EUROPE HEALTHCARE BPO MARKET NEWS

- In February 2024, Accenture plc launchedAI-poweredered claims integrity solution for German statutory health insurers that reduced processing errors by 34 percent and accelerated reimbursement cycles while maintaining full compliance with GDPR and national billing protocols.

- In April 2024, Infosys Limited deployed a conversational AI platform for a major UK integrated care system that handles 70 percent of routine patient inquiries in six European languages,s enhancing accessibility and reducing administrative burden on clinical staff.

- In June 2024, Tata Consultancy Services Limited introduced a real-world evidence generation platform for European pharmaceutical clients that securely aggregates and anonymizes data from electronic health records, digital wearables, and patient registries to support EMA regulatory submissions.

- In August 2024, Accenture expanded its pharmacovigilance analytics hub in Dublin with additional multilingual medical reviewers and AI-powered signal detection tools to meet growing EMA requirements for post market safety monitoring across the EU.

- In October 2024, Infosys partnered with a leading Dutch health insurer to develop areal-timee fraud detection engine that analyzes cross-provider utilization patterns and flags anomalies using machine learning while ensuring full compliance with Dutch and EU data protection laws.

MARKET SEGMENTATION

This research report on the weurope healthcare BPO market has been segmented and sub-segmented into the following categories.

By Payer Service

- Claims Management

- Integrated Front-end Services

- Back-office Operations

- Member Management

- Provider Management

- Billing and Accounts Management

- Analytics and Fraud Management

- HR Services

By Pharmaceutical Service

- Research and Development

- Manufacturing

- Non-clinical Services

- Sales and Marketing services

- Supply Chain Management

- Other Non-Clinical Applications

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Healthcare BPO Market?

Key drivers in the Europe Healthcare BPO Market include cost reduction, productivity gains, and access to global talent for tasks like medical coding and HR management. Emphasis on digital transformation and value-based care boosts demand, particularly in payer services; despite challenges like data privacy, the market thrives on offshore efficiencies and tech advancements in nations like Italy and France.

2. Who are the top companies in the Europe Healthcare BPO Market?

Leading companies in the Europe Healthcare BPO Market include Cognizant, Infosys, Accenture, and regional players like ANI Healthcare Solutions, focusing on revenue cycle and claims services. Acquisitions like EnableComp's in 2024 highlight consolidation; these firms dominate via compliance, tech innovation, and tailored solutions for NHS and Krankenkasse standards across Germany and the UK.

3. What services are offered in the Europe Healthcare BPO Market?

Services in the Europe Healthcare BPO Market cover provider functions like revenue cycle management and patient enrollment, payer services including claims and care management, plus pharmaceutical R&D and sales support. Non-clinical tasks like medical transcription and telehealth dominate, helping optimize efficiency while adhering to EU regulations.

4. How does Germany contribute to the Europe Healthcare BPO Market?

Germany drives the Europe Healthcare BPO Market with its public-private model, outsourcing revenue cycle and data processing amid labor shortages and rising costs. Strict privacy rules spur demand for compliant partners; the market here benefits from digital health pushes, positioning it for significant growth in administrative and coding services.

5. What role does the UK play in the Europe Healthcare BPO Market?

The UK bolsters the Europe Healthcare BPO Market via NHS outsourcing for transcription, claims, and patient support to manage budgets and demands. Post-Brexit shifts and digital initiatives accelerate adoption, with private providers relying on BPO for non-clinical ops, projecting USD 20.2 billion valuation by 2026.

6. How does GDPR impact the Europe Healthcare BPO Market?

GDPR profoundly shapes the Europe Healthcare BPO Market by enforcing strict data protection, favoring domestic partners in Germany and the UK for analytics. It raises compliance costs but drives premium pricing for certified vendors, limiting offshore while promoting EU Cloud standards and secure outsourcing.

7. What is revenue cycle management in the Europe Healthcare BPO Market?

Revenue cycle management (RCM) in the Europe Healthcare BPO Market handles billing, coding, claims processing, and denials to cut revenue loss. Outsourced widely for efficiency, it leverages tech in payer-provider models, especially in high-cost regions like France, reducing errors and boosting cash flow.

8. Why outsource to the Europe Healthcare BPO Market?

Organizations outsource to the Europe Healthcare BPO Market for cost savings, skilled talent access, and focus on core care, outsourcing admin tasks amid chronic disease burdens. It offers scalable solutions for claims and HR, with offshore options in compliant regions enhancing productivity across the EU.

9. What trends shape the Europe Healthcare BPO Market?

Trends in the Europe Healthcare BPO Market include digital health adoption, telehealth support, and AI-driven claims auditing amid rising expenditures. Value-based care and patient data spaces foster specialized BPO, with southern Europe modernizing reimbursements via regional integrators.

10. How does France influence the Europe Healthcare BPO Market?

France impacts the Europe Healthcare BPO Market with 14.5% CAGR growth through 2028, driven by payment reforms and provider consolidation for sustainable systems. BPO manages data entry to claims, capitalizing on regulatory pressures for efficient outsourcing in a complex healthcare landscape.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com