Europe Healthcare Logistics Market Size, Share, Trends & Growth Forecast Report By Treatment, Distribution Channel and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Market Size, 2025

$33.57 BnMarket Estimate, 2026

$35.90 BnMarket Forecast, 2034

$61.46 BnCAGR, 2026–2034

6.95%Europe Healthcare Logistics Market Size

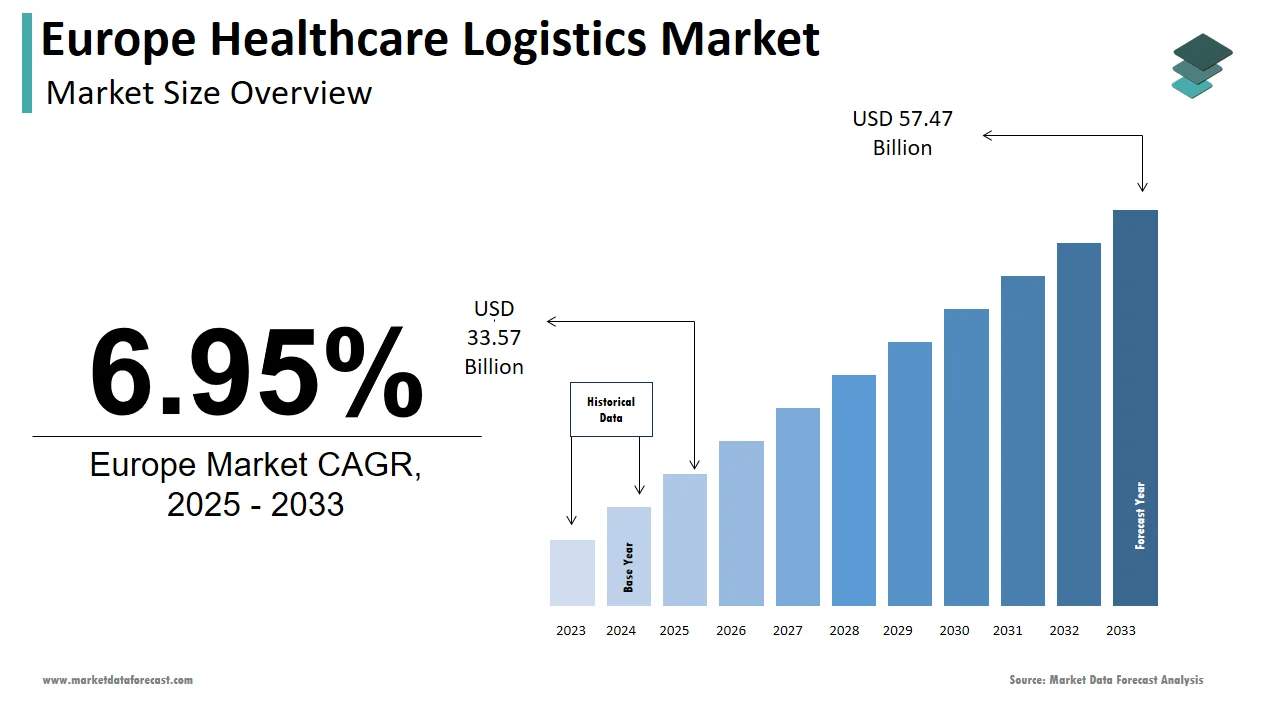

The healthcare logistics market size in Europe was valued at USD 33.57 billion in 2025. The European market is estimated to be worth USD 61.46 billion by 2034 from USD 35.90 billion in 2026, growing at a CAGR of 6.95% from 2026 to 2034.

Healthcare Logistics is the specialized transportation, warehousing, and distribution of temperature-sensitive and time-critical healthcare products, including pharmaceuticals, biologics, vaccines, medical devices, and hospital supplies across complex supply chains. Europe’s healthcare logistics infrastructure is shaped by fragmented national health systems, integrated cross-border supply requirements, and evolving regulatory frameworks under the European Medicines Agency and European Commission. As per the European Centre for Disease Prevention and Control, more than 1.2 billion vaccine doses were distributed across EU member states between 2020 and 2023, under emergency and routine immunization programs, highlighting the scale and precision required.

MARKET DRIVERS

Expansion of Biologics and Cell and Gene Therapies Demands Advanced Cold Chain Solutions

The rapid growth of temperature-sensitive biologics and cell and gene therapies is a primary driver of Europe's healthcare logistics markets. According to the European Medicines Agency, over 70% of new drug approvals in 2023 were biologics requiring storage between 2°C and 8°C or ultra-cold conditions below minus 70°C. Cell-based therapies such as CAR T treatments must be delivered within 24 to 72 hours from manufacturing to bedside with minimal thermal deviation. These products cannot be frozen or exposed to temperature excursions exceeding 2°C without loss of viability. Consequently, logistics providers invest in active refrigerated containers with real-time GPS and temperature telemetry compliant with EU GDP Annex 1. Companies like World Courier and Kuehne+Nagel now operate dedicated biologics lanes with validated thermal packaging and direct hospital handoff protocols. This clinical urgency transforms logistics from a support function into a critical determinant of therapeutic success, driving demand for high-fidelity-controlled supply chains.

EU Regulatory Harmonization Under the Falsified Medicines Directive Strengthens Track and Trace Requirements

The implementation of the European Falsified Medicines Directive has significantly elevated the role of logistics in ensuring pharmaceutical authenticity and patient safety, which is prompting the growth of the Europe healthcare logistics market. As per the European Commission, since February 2019, all prescription medicines placed on the EU market must carry a unique identifier and an anti-tampering device enabling verification at every supply chain node. This mandates seamless data exchange between manufacturers, wholesalers, pharmacies, and logistics providers through the European Medicines Verification System. Healthcare logistics operators must now integrate serialization scanning and data logging into every warehouse and transport process. Companies like DB Schenker and DHL Supply Chain have deployed automated verification gates at distribution hubs capable of processing 10,000 units per hour while maintaining GDP compliance. This regulatory framework not only combats counterfeit drugs but also transforms logistics into a data-driven compliance checkpoint, reinforcing the need for digitized and auditable distribution networks across Europe.

MARKET RESTRAINTS

Fragmented National Healthcare Systems Impede Standardized Logistics Protocols

The operational friction due to the lack of harmonized procurement, delivery, and regulatory practices across member states is impeding the growth of the Europe healthcare logistics market. According to the European Observatory on Health Systems and Policies, each of the 27 EU countries maintains distinct hospital tendering cycles, delivery windows, and documentation requirements for medical products. For instance, while Germany mandates delivery of hospital supplies between 6 AM and 10 AM, pharmacies in Southern Italy often accept shipments until 6 PM. This inconsistency complicates route planning and increases last-mile costs by up to 30% as per the European Logistics Association.

High Capital Investment Requirements for Temperature-Controlled Infrastructure Limit Market Participation

The capital intensity of building and maintaining GDP-compliant cold chain infrastructure additionally inhibits the growth of the Europe Healthcare Logistics Market. According to the European Cold Chain Federation, establishing a single temperature-controlled warehouse with 2°C to 8°C and minus 20°C zones requires an average investment of 12 to 18 million euros, including validation testing and real-time monitoring systems. These costs are prohibitive for regional or mid-sized logistics firms, particularly in Central and Eastern Europe, where public funding for health infrastructure remains limited. This disparity creates a two-tier market where large multinational 3PLs dominate high-value biologics while local players handle non-temperature-sensitive goods often without full regulatory oversight.

MARKET OPPORTUNITIES

Digital Integration of Logistics Platforms with Hospital Procurement Systems Enhances Efficiency

The integration of healthcare logistics with digital hospital supply chain ecosystems to reduce waste, improve inventory accuracy, and ensure just-in-time delivery is creating new opportunities for the growth of the Europe healthcare logistics market. As per the European Hospital Association, major EU hospitals now use electronic procurement platforms, such as GHX or Inmar, that integrate directly with logistics providers’ transport management systems. This interoperability enables automatic order triggering, real-time shipment tracking, and predictive arrival notifications. Additionally, the EU’s Digital Europe Programme allocated 95 million euros in 2024 to pilot blockchain-enabled logistics networks for high-cost orphan drugs, ensuring end-to-end provenance and temperature integrity.

Growth of Hospital at Home and Home-Based Care Models Expands Last Mile Complexity

The strategic shift toward decentralized care delivery for patient-centric last-mile logistics solutions is surging the growth of the Europe healthcare logistics market. According to the Organisation for Economic Co-operation and Development, over 1.8 million Europeans now receive hospital-level care at home, including intravenous antibiotics, chemotherapy, and advanced wound dressings. This trend necessitates a new logistics paradigm: smaller batch sizes, flexible delivery windows, and direct-to-patient handoff with identity verification. Companies like UPS Healthcare and GEODIS have launched white glove services featuring GPS-tracked couriers trained in basic healthcare protocols and equipped with portable cold boxes maintaining 2°C to 8°C for up to 72 hours.

MARKET CHALLENGES

Geopolitical Instability and Trade Disruptions Threaten Supply Chain Resilience

The growing risk from geopolitical tensions and trade volatility that jeopardize the continuity of essential medical supplies is a challenging factor for the growth of the Europe healthcare logistics market. As per the European Commission, over 60% of active pharmaceutical ingredients used in EU-manufactured medicines are sourced from outside the bloc, primarily from India and China. The 2022 Red Sea shipping crisis caused average transit delays of 14 to 21 days for sea freight from Asia, increasing air freight costs by 200% according to the International Air Transport Association. Furthermore, the war in Ukraine disrupted overland routes for medical products destined for Eastern Europe, forcing rerouting through congested Western hubs.

Shortage of Skilled Workforce in GDP-Compliant Cold Chain Operations Hampers Scalability

The acute shortage of personnel trained in Good Distribution Practices and temperature-controlled handling procedures is also expected to limit the growth of the Europe Healthcare Logistics Market. Unlike general freight logistics, healthcare transport requires knowledge of regulatory documentation, thermal mapping, and emergency response for excursions. Vocational training programs remain limited, with only six EU countries offering certified healthcare logistics curricula.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Supply Chain, Service Type, Product, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | FedEx, ADAllen Pharma, CRYOPDP, SF Express, Alloga, DB Schenker, Deutsche Post DHL Group, World Courier, Biosensors International Group, Ltd, Kuehne+Nagel International AG, and Entero Healthcare. |

SEGMENTAL ANALYSIS

By Supply Chain Insights

The cold chain logistics segment held a dominant share of the Europe healthcare logistics market in 2024, with the exponential growth of temperature-sensitive biologics, vaccines, and advanced therapy medicinal products requiring uninterrupted thermal control. The second factor is regulatory enforcement. The European Commission’s Good Distribution Practice guidelines mandate strict temperature monitoring and validation for all medicinal products susceptible to thermal degradation. Additionally, the rollout of cell and gene therapies across EU oncology centers has created demand for cryogenic logistics with dry vapor shippers maintaining minus 150°C for up to ten days.

The cold logistics segment is estimated to grow at the fastest CAGR of 5.2% from 2026 to 2034, with the rising volume of personalized medicines requiring cryogenic transport and real-time condition monitoring. As per the European Commission, over 120 hospital-based advanced therapy centers now operate across the EU, administering time-critical treatments that must reach patients within 72 hours of manufacturing. Companies like World Courier and Kuehne+Nagel have deployed IoT-enabled packaging that transmits location, temperature, and shock data to cloud platforms accessible by manufacturers and clinicians. Furthermore, EU funding under Horizon Europe has allocated 110 million euros to develop passive cold boxes using phase change materials that maintain 2°C to 8°C for 120 hours without power, enabling reliable last-mile delivery in remote regions.

By Service Type Insights

The transportation segment was the largest by accounting for 48.2% of the Europe healthcare logistics market share in 2024, with the time-bound and temperature-controlled movement in ensuring product integrity from manufacturer to end user. As per Eurostat, over 45% of EU pharmaceutical trade occurs intra-regionally, requiring seamless cross-border coordination with minimal customs delays. Companies like DHL and UPS have responded with dedicated healthcare fleets featuring GPS-tracked vehicles, refrigerated compartments, and trained couriers certified in Good Distribution Practices. National health systems in Germany and the Netherlands reimburse logistics costs for home-delivered therapies, reinforcing transportation as a reimbursable care component. This operational centrality ensures transportation remains the backbone of healthcare logistics despite advances in warehousing and monitoring technologies.

The monitoring segment is anticipated to register the fastest CAGR of 15.7% in the coming years, with the regulatory mandates for real-time condition tracking and the integration of logistics data into clinical decision-making. As per the European Medicines Agency, since 2023, all clinical trial shipments of investigational medicinal products must include continuous temperature and location monitoring with automated excursion alerts. The second catalyst is hospital demand for supply chain transparency. Companies like Sensitech and Controlant have introduced single-use Bluetooth-enabled loggers that cost under 8 euros and sync data directly to hospital procurement platforms. Additionally, the EU’s Digital Product Passport initiative, set for 2026, will require all high-risk medical products to carry embedded sensors transmitting lifecycle data. These regulatory and operational shifts transform monitoring from an optional add-on into a core compliance and quality assurance function.

By Product Insights

The pharmaceutical products segment was the largest and held a significant share of the Europe healthcare logistics market in 2024, owing to the high-volume temperature sensitivity and stringent regulatory oversight governing drug distribution. The second driver is the complexity of modern drug formats. Monoclonal antibodies, cell therapies, and mRNA vaccines demand ultra-cold storage, real-time monitoring, and rapid transit to maintain efficacy. National health systems treat these products as critical infrastructur,e with Germany’s Paul Ehrlich Institute requiring a full chain of identity documentation for every CAR T therapy shipment. Additionally, the Falsified Medicines Directive mandates serialization and verification at every logistics node, creating data-intensive workflows that elevate pharmaceutical logistics beyond simple transport.

The medical devices segment is expected to register a CAGR of 11.9% from 2026 to 2034, with the rising volume of high-value implantable and diagnostic devices requiring secure time-definite delivery to operating rooms and imaging centers. The EU Medical Devices Regulation 2017/745 mandates unique device identification and full supply chain traceability, increasing the need for logistics providers with integrated scanning and data management capabilities. Companies like GEODIS and DB Schenker now operate sterile validated lanes for implant delivery featuring tamper-evident packaging and surgeon-notified arrival windows. Additionally, the growth of robotic surgery has created demand for kitted instrument trays delivered weekly to hospitals with zero tolerance for errors. These precision requirements transform device logistics into a high-touch touch specialized service with premium margins and strong hospital partnerships.

COUNTRY LEVEL ANALYSIS

Germany Healthcare Logistics Market Analysis

Germany was the top performer in the Europe healthcare logistics market by accounting for 22.3% of share in 2024, with a dense network of pharmaceutical manufacturers, world-class hospital infrastructure, and stringent regulatory enforcement. The country also operates 1,940 public hospitals that rely on just-in-time delivery for critical care products, with 95% requiring GDP-certified logistics partners. Additionally, the national “Hospital at Home” program reimburses logistics costs for home-delivered therapies, creating a robust last-mile ecosystem.

France Healthcare Logistics Market Analysis

The French healthcare logistics market was positioned second by holding 16.3% of the share in 2024 from centralized procurement through the National Agency for Hospital Procurement, which manages over 25 billion euros in annual medical product purchases. This system mandates standardized logistics protocols across 1,300 public hospitals, creating scale and predictability for providers. The second driver is the rapid expansion of advanced therapy centers. Additionally, the national “Ma Santé 2022” plan promotes home care, with over 420,000 patients receiving weekly deliveries of biologics and medical devices. French logistics firms like GEODIS have invested in GDP-certified hubs in Lyon and Paris, equipped with real-time monitoring and serialization verification. These coordinated policy and infrastructure initiatives position France as a high-volume high high-compliance market for specialized healthcare logistics.

United Kingdom Healthcare Logistics Market Analysis

The United Kingdom healthcare logistics market is likely to grow with a significant CAGR throughout the forecast period, with a fully integrated public health system that centrally coordinates medical supply distribution across 1,200 hospitals and 7,000 primary care facilities. The NHS Supply Chain manages over 500,000 product lines, with 90% requiring temperature-controlled transport for at least part of their journey. The Medicines and Healthcare products Regulatory Agency launched the UK Medicines Verification System in 2023, which processed over 800 million verification events in its first year. Additionally, the NHS Long Term Plan targets a 30% increase in home-based care by 2028, driving demand for patient-centric last-mile services. Companies like Movianto and DHL have established NHS-accredited delivery networks with real-time tracking and identity-verified handoffs.

Italy Healthcare Logistics Market Analysis

Italy healthcare logistics market growth is likely to grow prominently in next coming years owing to a high prevalence of chronic diseases, a fragmented regional healthcare system, and growing demand for biologic therapies. The Italian Ministry of Health allocated 220 million euros in 2024 to upgrade hospital logistics centers with GDP-compliant cold rooms and automated verification gates. Additionally, Italy serves as a key entry point for Mediterranean distribution, with ports in Genoa and Trieste handling over 30% of EU pharmaceutical imports from Asia. Logistics providers like Biotec and DHL have established validation hubs in Milan to recertify shipments before onward distribution.

COMPETITIVE LANDSCAPE

The Europe Healthcare Logistics Market features a highly specialized and capital-intensive competitive landscape dominated by global integrated providers with deep regulatory expertise and extensive certified infrastructure. Competition is not price-driven but centers on compliance, reliability, technological integration, and clinical proximity. Large players like DHL, Kuehne+Nagel, and World Courier maintain significant advantages through pan-European GDP-compliant networks, real-time monitoring systems, and long-standing relationships with regulators and health authorities. The market is characterized by high barriers to entry due to the cost of cold chain infrastructure validation requirements and the need for skilled personnel trained in Good Distribution Practices. While regional players serve local hospital networks, they struggle to compete for pan-EU or biologics contracts without digital and thermal capabilities. Differentiation increasingly hinges on data intelligence, with leading firms offering predictive analytics, exception management, and end-to-end visibility as value-added services.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe healthcare logistics market include

- FedEx

- ADAllen Pharma

- CRYOPDP

- SF Express

- Alloga

- DB Schenker

- Deutsche Post DHL Group

- World Courier

- Biosensors International Group, Ltd

- Kuehne+Nagel International AG

- Entero Healthcare

TOP PLAYERS IN THE MARKET

- DHL Supply Chain is a global leader in healthcare logistics with an extensive integrated network across Europe dedicated to pharmaceutical and medical device distribution. The company operates over 40 GDP-compliant facilities in the region, featuring temperature-controlled warehousing, real-time monitoring, and serialization capabilities aligned with the EU Falsified Medicines Directive. In Europe, DHL supports national immunization programs, hospital group procurement, and direct-to-patient delivery models. It also launched a dedicated cell and gene therapy logistics service with cryogenic packaging validated for minus 150°C transport. These initiatives reinforce DHL’s position as a strategic partner for both public health systems and biopharma innovators requiring end-to-end supply chain integrity across complex therapeutic landscapes.

- Kuehne+Nagel International AG is a Switzerland-based logistics giant with a specialized healthcare division that plays a pivotal role in Europe’s temperature-sensitive supply chains. The company manages a pan-European network of certified Life Science Competence Centers equipped for 2°C to 8°C frozen and cryogenic shipments. Kuehne+Nagel leverages its air and ocean freight expertise to ensure seamless global inbound and intra-EU distribution for major pharmaceutical manufacturers. The company also partnered with seven European hospital networks to implement just-in-time implant delivery systems with surgeon-notified arrival windows. These actions highlight its commitment to precision compliance and clinical integration, positioning it at the forefront of high-value healthcare logistics in Europe.

- World Courier, a subsidiary of Marken and part of the UPS Healthcare network, is a specialized provider of time-critical and temperature-controlled healthcare logistics with deep roots in Europe. The company focuses exclusively on clinical trials, commercial biologics, and advanced therapy medicinal products requiring chain of identity and chain of custody assurance. In Europe, it operates over 25 GDP-certified depots offering 24/7 dispatch and direct-to-site delivery for investigational medicinal products. It also expanded its last-mile network to cover 98% of EU hospital and home care addresses for cell therapy delivery. These capabilities make World Courier a preferred partner for precision medicine logistics, where speed, compliance, and traceability are non-negotiable.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Healthcare Logistics Market invest heavily in GDP-certified infrastructure, including temperature-controlled warehouses and validated packaging systems to meet stringent regulatory requirements. Companies deploy digital visibility platforms with real-time monitoring, predictive analytics, and blockchain-enabled traceability to ensure compliance with the Falsified Medicines Directive and EU Medical Devices Regulation. Strategic partnerships with national health systems, hospital groups, and biopharma firms enable integrated end-to-end supply chain solutions from manufacturing to bedside. Expansion of last-mile networks supports the growth of hospital-at-home and direct-to-patient models with identity-verified handoffs and flexible delivery windows. Additionally, firms prioritize sustainability by optimizing multimodal transport routes and adopting reusable thermal containers to align with EU Green Deal objectives while maintaining product integrity across complex healthcare supply chains.

MARKET SEGMENTATION

This Europe healthcare logistics market research report is segmented and sub-segmented into the following categories.

By Supply Chain

- Non-Cold Logistic

- Cold Chain Logistics

By Service Type

-

Warehouse And Storage

-

Transportation

- Sea Freight

- Air Freight

- Overland Transportation

- Monitoring Components

By Product

- Medical Devices

- Pharmaceutical Devices

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the europe healthcare logistics market?

The europe healthcare logistics market focuses on transporting and storing medical products, pharmaceuticals, and biopharmaceuticals efficiently and safely across europe

2. Which countries lead the europe healthcare logistics market?

Germany, France, and the UK dominate the europe healthcare logistics market, thanks to their advanced infrastructure and strong pharmaceutical industries

3. What drives growth in the europe healthcare logistics market?

Growth drivers include increasing chronic diseases, demand for temperature-controlled logistics, growth in biopharma, and government regulatory support

4. How important is cold chain logistics in the europe healthcare logistics market?

Cold chain logistics is vital for transporting temperature-sensitive drugs, vaccines, and biologics, driving significant growth within the europe healthcare logistics market

5. What services are offered in the europe healthcare logistics market?

Services include transportation, warehousing, packaging, labeling, inventory management, and integrated end-to-end supply chain solutions

6. Who are the major players in the europe healthcare logistics market?

Leading companies include DHL, DB Schenker, Kuehne + Nagel, Marken Ltd, and Cavalier Logistics in the europe healthcare logistics market

7. How does digitalization affect the europe healthcare logistics market?

Digital solutions improve tracking, visibility, and operational efficiency, transforming the europe healthcare logistics market

8. What challenges does the europe healthcare logistics market face?

Challenges include regulatory compliance, high costs, complex cross-border logistics, and maintaining product integrity in transit

9. How important is sustainability in the europe healthcare logistics market?

Sustainability initiatives focus on reducing carbon emissions and waste, increasingly adopted in the europe healthcare logistics market

10. What is the role of third-party logistics in the europe healthcare logistics market?

Outsourcing to third-party logistics providers boosts efficiency and allows pharma companies to focus on core activities in the europe healthcare logistics market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com