Europe Medical Tourism Market Research Report – Segmented by Treatment Type (Cardiovascular Treatment, Orthopedic Treatment, Fertility Treatment, Neurological Treatment, Dental Treatment, Cancer Treatment, Cosmetic Treatment, Others), Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis From 2025 to 2033

Europe Medical Tourism Market Size

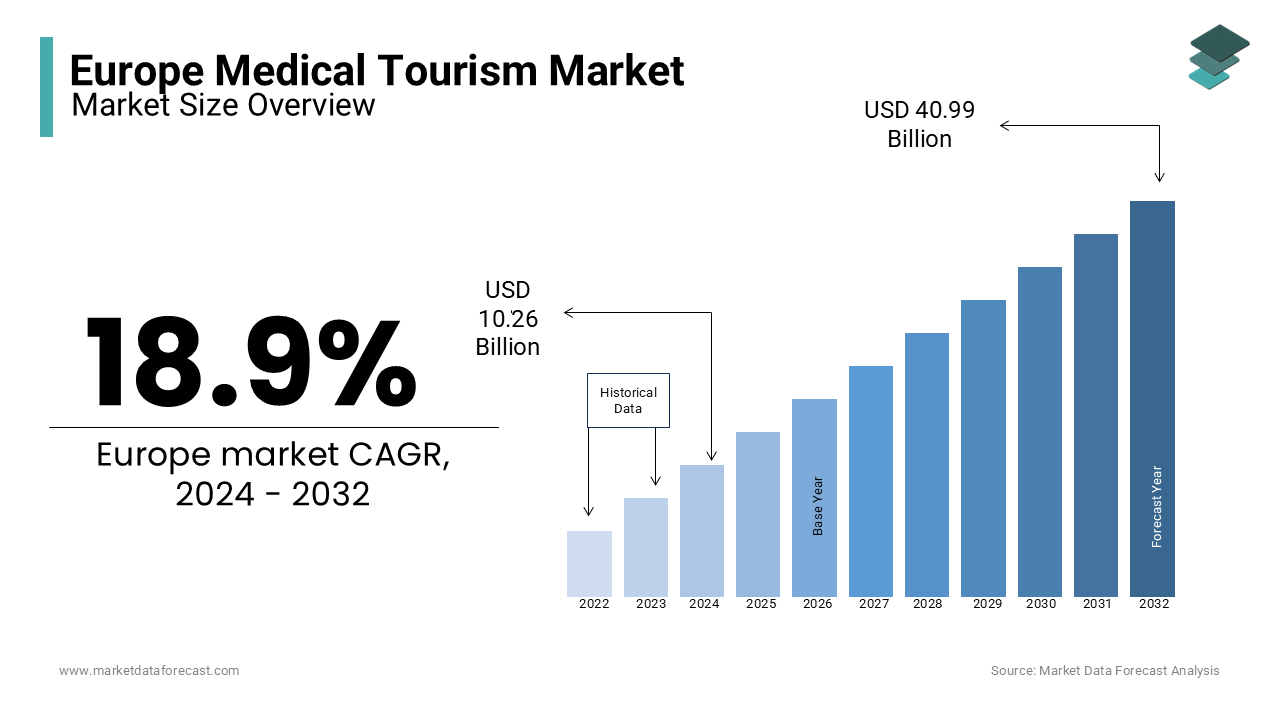

The European medical tourism market size was valued at USD 10.26 billion in 2024. The size of the market is expected to be worth USD 48.73 billion by 2033 from USD 12.20 billion in 2025, growing at a CAGR of 18.9% during the forecast period.

The Europe medical tourism market is experiencing steady growth, driven by advancements in healthcare infrastructure and increasing demand for cost-effective treatments. This expansion is fueled by cross-border patient mobility from neighboring regions seeking high-quality care at competitive prices. Additionally, the European Commission reports that over 60% of medical tourists in Europe prioritize destinations offering cutting-edge technology and personalized care. Sustainability and digital health innovations are also becoming key focus areas, reshaping the dynamics of the market.

MARKET DRIVERS

Rising Healthcare Costs in Neighboring Regions

Escalating healthcare costs in neighboring regions like North Africa and the Middle East are a primary driver of the Europe medical tourism market. According to the World Health Organization, treatment expenses in these regions have surged by 20% annually since 2020, that is helping patients to seek affordable yet high-quality alternatives. According to the Turkish Ministry of Health, over 70% of international patients traveling to Turkey for treatments cite cost savings as their primary motivation. European countries like Spain and Hungary have capitalized on this trend by offering bundled packages that include travel, accommodation, and medical services at competitive rates. As per the European Travel Commission, over 40% of medical tourists opt for destinations offering transparent pricing models by enhancing Europe’s appeal as a global hub for affordable healthcare.

Technological Advancements in Healthcare

Technological advancements in healthcare are also propelling the market forward. According to the European Federation of Pharmaceutical Industries and Associations, innovations such as robotic surgeries and telemedicine have improved treatment outcomes and attracted patients seeking cutting-edge care. For example, Germany’s adoption of AI-driven diagnostic tools has reduced recovery times by 30%, as reported by the German Medical Association. Additionally, the rise of digital health platforms has streamlined patient experiences by enabling seamless coordination between providers and travelers. As per Eurostat, over 50% of medical tourists now use online portals to schedule treatments and access post-operative care.

MARKET RESTRAINTS

Stringent Visa Regulations

Stringent visa regulations pose a significant restraint for the Europe medical tourism market. According to the European Migration Network, visa processing delays and complex documentation requirements deter patients from non-EU countries for those in Asia and Africa. According to the French Ministry of Foreign Affairs, visa rejections for medical travelers increased by 15% in 2023 by limiting accessibility to European healthcare facilities. This issue is compounded by varying policies across member states by creating confusion among patients. As per the International Organization for Migration, over 60% of rejected applicants cited administrative hurdles as the primary barrier. While some countries have introduced medical visas to ease entry that inconsistencies remain a challenge for market expansion.

High Out-of-Pocket Expenses

The high out-of-pocket expenses for uninsured patients act as another restraint. According to the European Health Insurance Card (EHIC) Authority, uninsured medical tourists face costs up to 40% higher than insured patients by discouraging cross-border travel. For example, Italian hospitals reported a 25% decline in uninsured patients in 2023 due to rising treatment fees, as stated by the Italian National Institute of Health. Furthermore, limited insurance coverage for international treatments exacerbates affordability concerns. As per the European Consumer Organisation, only 30% of private health insurers offer reimbursement for overseas procedures is hindering wide spread adoption of medical tourism.

MARKET OPPORTUNITIES

Expansion of Digital Health Services

The growing adoption of digital health services presents a significant opportunity for the Europe medical tourism market. Their ability to enhance patient convenience and reduce travel costs is to propel the growth of the market. For instance, Sweden launched a telehealth platform in 2023 by enabling pre- and post-treatment consultations for international patients. As per the European Telemedicine Alliance, over 60% of medical tourists prefer destinations offering virtual follow-ups by reducing the need for prolonged stays. Innovations in wearable health devices have further expanded this segment is positioning digital health as a key growth driver.

Growing Demand for Cosmetic and Wellness Treatments

The increasing demand for cosmetic and wellness treatments offers another promising opportunity. For example, Switzerland’s luxury clinics attracted over 50,000 international patients seeking premium facelifts and skin rejuvenation treatments, as reported by the Swiss Medical Tourism Board. Additionally, government incentives for wellness tourism have encouraged investments in spa and rehabilitation centers by aligning with the rising preference for holistic care. These developments promote the potential of cosmetic and wellness treatments to expand the market growth in the next coming years.

MARKET CHALLENGES

Competition from Emerging Markets

Intense competition from emerging markets poses a pressing challenge for the Europe medical tourism market. According to Deloitte, countries like Thailand and India captured over 40% of the global medical tourism market share in 2023 by offering comparable treatments at lower costs. For instance, Indian hospitals provide cardiac surgeries at 50% less than European facilities, as reported by the Indian Medical Tourism Council. This shift is further amplified by aggressive marketing strategies adopted by Asian providers, who emphasize affordability and cultural inclusivity. The international patients now prefer destinations offering competitive pricing by creating hurdles for European providers striving to retain market share.

Supply Chain Disruptions for Medical Supplies

Supply chain disruptions for medical supplies also challenge the market for critical equipment and pharmaceuticals. According to the European Logistics Association, shortages caused by geopolitical tensions delayed elective procedures by up to six months in 2023. This issue is compounded by reliance on imports for essential materials. As per the European Raw Materials Alliance, over 90% of rare metals used in medical devices are sourced from foreign markets by making the supply chain vulnerable to external shocks. For example, tariffs imposed on Chinese imports raised production costs for manufacturers by limiting their ability to meet growing demand.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Treatment Type, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Helios Hospitals, The Royal Marsden, Cromwell Hospital, Institut de la Hernie Paris, Charité University Hospital, Grande Ospedale Metropolitano, Kolan International Hospital, Centre Hospitalier Universitaire Vaudois, Medistanbul Hospital, and Amsterdam University Medical Center. |

SEGMENTAL ANALYSIS

By Treatment Type

The cardiovascular treatments segment dominated the Europe medical tourism market by capturing 25.4% of share in 2024 due to the region’s expertise in advanced cardiac surgeries and minimally invasive procedures. For instance, the German Heart Center Berlin reports that over 60% of international patients travel to Germany for coronary artery bypass grafts, reflecting its reputation for excellence. Advancements in robotic-assisted surgeries have further enhanced the segment’s appeal. As per the European Society of Cardiology, modern techniques now reduce recovery times by 40%, boosting demand. Additionally, government initiatives promoting early detection have increased patient inflows is amplifying the cardiovascular treatments’ dominance.

The fertility treatments segment is anticipated to register a CAGR of 10.5% throughout the forecast period. This growth is fueled by rising infertility rates and the increasing acceptance of assisted reproductive technologies. According to the Spanish Fertility Society, over 50% of IVF cycles in Spain are performed for international couples by reflecting its global appeal. Innovations in genetic screening have accelerated adoption. For instance, Denmark introduced next-generation sequencing in 2023 by improving success rates by 20%. These developments position fertility treatments as a key growth driver in the coming years.

REGIONAL ANALYSIS

Germany was the largest contributor to the Europe medical tourism market by accounting for 25.9% in 2024. This dominance is fueled by the country’s robust healthcare infrastructure and expertise in specialized treatments. For instance, over 70% of international patients cite Germany’s advanced cardiac and orthopedic facilities as their primary reason for choosing the destination. A key factor propelling Germany’s growth is its emphasis on innovation. According to the Climate Neutral Healthcare Initiative, German hospitals lead Europe in adopting eco-friendly practices with over 60% of facilities powered by renewable energy sources.

Spain is lucratively growing with an anticipated CAGR of 14.3% during the forecast period. The country’s growth is driven by its thriving fertility and dental tourism sectors, which account for nearly 40% of total revenue. For example, Barcelona-based clinics attract over 50,000 international patients annually for IVF treatments, reflecting their global reputation. Another contributing factor is the rise of wellness retreats.

COMPETITIVE LANDSCAPE

The Europe medical tourism market is marked by intense competition, with established giants and emerging players vying for supremacy. According to the European Hospital Federation, the top five companies account for over 60% of total revenue, reflecting the market’s oligopolistic structure. Helios Health Group, Fresenius Medical Care, and Bupa Global dominate the landscape by leveraging their technological expertise and extensive distribution networks. Smaller players, however, are gaining traction through niche offerings, such as wellness retreats and cosmetic treatments. The rise of digital platforms has leveled the playing field, enabling smaller brands to reach wider audiences. Price wars and promotional campaigns are common in the fertility segment. Despite these challenges, innovation remains a key differentiator, with companies continuously introducing advanced solutions to meet evolving consumer demands.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe medical tourism market include

- Helios Hospitals

- The Royal Marsden

- Cromwell Hospital

- Institut de la Hernie Paris

- Charité University Hospital

- Grande Ospedale Metropolitano

- Kolan International Hospital

- Centre Hospitalier Universitaire Vaudois

- Medistanbul Hospital

- Amsterdam University Medical Center

Top Players in the Market

Helios Health Group

Helios Health Group leads the Europe medical tourism market by contributing significantly to the global market through its extensive network of hospitals and specialized treatment centers. Its focus on advanced cardiac and oncology treatments shall promote its position in the marketplace. The company’s global reach extends to over 50 countries is additionally making it a dominant player worldwide.

Fresenius Medical Care

Fresenius Medical Care ranks second, renowned for its expertise in dialysis and chronic disease management. As per the German Medical Association, Fresenius’ European operations is generating huge revenue bolstered by its partnerships with leading research institutions. The company’s commitment to innovation strengthens its competitive edge globally.

Bupa Global

Bupa Global holds the third position, leveraging its strong brand presence and focus on personalized care. Company’s investment in telemedicine and digital health solutions are major factor that is expanding the share in the market. Its contributions to the global market include tailored packages for international patients by positioning it as a key player in the Europe medical tourism market.

Top Strategies Used by Key Players

Key players in the Europe medical tourism market employ diverse strategies to strengthen their positions. One prominent approach is geographic expansion. Helios Health Group opened new facilities in Eastern Europe in 2023 to tap into emerging markets. Another strategy is technological innovation. Fresenius Medical Care partnered with AI developers to enhance diagnostic accuracy by resulting in a 20% increase in patient satisfaction. Strategic collaborations also play a crucial role. In 2023, Bupa Global collaborated with airlines to offer bundled travel packages that is boosting accessibility for international patients. Additionally, companies like Helios are investing in sustainability initiatives to align with environmental regulations.

RECENT MARKET DEVELOPMENTS

- In February 2024, Helios Health Group launched a new telemedicine platform. This initiative aimed to streamline cross-border consultations and improve patient accessibility.

- In April 2024, Fresenius Medical Care partnered with a leading AI firm. This collaboration aimed to enhance diagnostic accuracy for chronic diseases by resulting in a 25% improvement in treatment outcomes.

- In June 2024, Bupa Global introduced bundled travel and health packages. This initiative was intended to attract international patients by reducing logistical barriers and offering cost-effective solutions.

- In August 2024, Spain’s Quirónsalud opened a state-of-the-art fertility clinic in Barcelona. This launch aimed to cater to the growing demand for IVF treatments among international couples, boosting Spain’s position as a global hub for reproductive care.

- In October 2024, Germany’s Asklepios Hospitals unveiled a solar-powered medical facility. This initiative aimed to align with environmental regulations and appeal to eco-conscious patients seeking sustainable healthcare options

MARKET SEGMENTATION

This research report on the European medical tourism market has been segmented and sub-segmented into the following categories

By Treatment Type

- Cardiovascular Treatment

- Orthopedic Treatment

- Fertility Treatment

- Neurological Treatment

- Dental Treatment

- Cancer Treatment

- Cosmetic Treatment

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Medical Tourism Market?

The Europe Medical Tourism Market refers to cross-border travel within or to European countries for medical, dental, or wellness treatments, where patients seek high-quality healthcare at competitive costs compared to their home countries.

What factors are driving the growth of medical tourism in Europe?

Key drivers include cost-effective healthcare, advanced medical infrastructure, high treatment quality, and reduced waiting times compared to domestic healthcare systems.

Which are the major medical tourism destinations in Europe?

Top destinations include Germany, Spain, Hungary, Poland, Turkey, the Czech Republic, and Switzerland, known for their world-class hospitals and specialized treatments.

What types of treatments are most popular among medical tourists in Europe?

The most sought-after treatments include cosmetic surgery, dental care, fertility treatments, orthopedic procedures, and cardiac surgeries.

How does Europe compare with other global medical tourism regions?

Europe stands out for its clinical excellence, patient safety, and regulatory standards, unlike Asia, which emphasizes cost savings, or the Middle East, which focuses on luxury care.

What role does the European Union play in supporting medical tourism?

The EU promotes cross-border healthcare regulations, ensuring patients can receive treatments across member states with standardized medical practices and insurance coverage.

What are the main challenges faced by the Europe Medical Tourism Market?

Challenges include regulatory differences between countries, language barriers, visa restrictions, and lack of unified insurance frameworks across the region.

What are the future opportunities for Europe’s medical tourism market?

Opportunities include AI-assisted diagnostics, integrated health travel packages, government-led medical visa policies, and partnerships between healthcare and hospitality sectors.

How do European healthcare providers attract international patients?

Providers use digital marketing, partnerships with travel agencies, international accreditation, and multilingual websites to reach potential medical tourists globally.

What is the long-term outlook for the Europe Medical Tourism Market?

The market is expected to witness steady double-digit growth, driven by technological innovation, affordability, and expanding government support, positioning Europe as a global hub for premium medical and wellness travel.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com