Europe Medicated Feed Additives Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Type, Livestock, Mixture Type, And By Region (The UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis, (2026 to 2034)

Europe Medicated Feed Additives Market Size

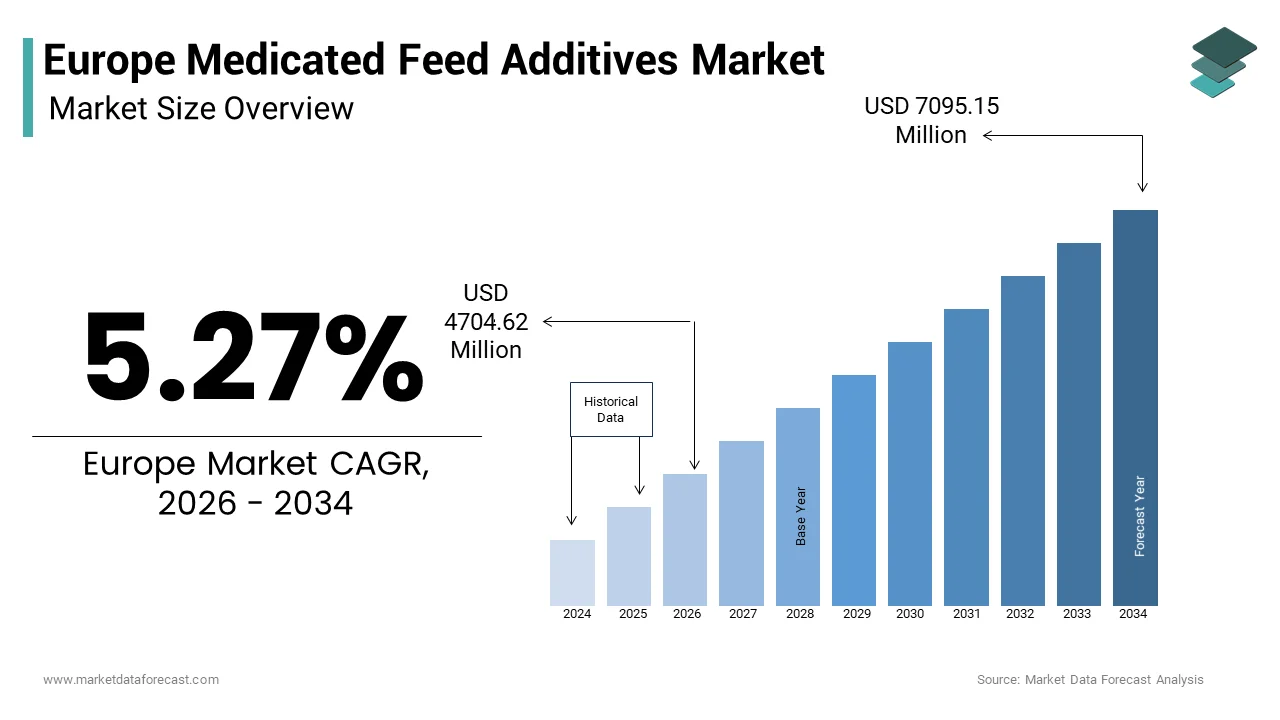

The European medicated feed additives market was valued at USD 4469.10 million in 2025 and is anticipated to reach USD 4704.62 million in 2026 from USD 7095.15 million by 2034, growing at a CAGR of 5.27% from 2026 to 2034.

Current Introduction of the Europe Medicated Feed Additives Market

Medicated feed additives are pharmaceutical substances incorporated into animal feed under veterinary supervision to prevent or treat diseases, improve feed efficiency, and support animal health in livestock production systems. In Europe, these additives are strictly regulated under Regulation (EC) No 1831/2003 and can only be used when authorized for specific therapeutic purposes, reflecting the region’s precautionary stance on antimicrobial use. Unlike growth promoters, medicated additives serve targeted clinical functions, primarily in poultry, swine, and cattle sectors. According to the European Medicines Agency, veterinary antimicrobial consumption is closely monitored through the European Surveillance of Veterinary Antimicrobial Consumption project, which reported on sales of antimicrobial medicines used in animals across the European Union in 2023, all requiring prescription and batch traceability. As per Eurostat, the European Union housed approximately 133 million pigs and 74 million bovines in 2023, which is underpinning sustained demand for disease management tools in concentrated production environments. Outbreaks of endemic diseases such as swine dysentery and necrotic enteritis in poultry further necessitate controlled therapeutic interventions. The European Commission’s One Health Action Plan against Antimicrobial Resistance reinforces the principle of prudent use, mandating that medicated feed be deployed only when non antibiotic alternatives are insufficient. This tightly governed yet essential segment bridges veterinary pharmacology and animal nutrition, operating within a framework that prioritizes public health, animal welfare, and food safety.

MARKET DRIVERS

Stringent Animal Disease Outbreaks Necessitate Targeted Therapeutic Interventions

Recurrent and region-specific epizootics in European livestock populations drive consistent demand for medicated feed additives as a controlled delivery method for veterinary therapeutics, which is a major factor propelling the growth of the European medicated feed additives market. According to the European Food Safety Authority’s EU One Health Zoonoses Report 2023, Salmonellosis remained one of the most frequently reported zoonoses in poultry, with thousands of confirmed cases across member states, while Porcine Reproductive and Respiratory Syndrome continued to be a major swine health concern. These outbreaks often occur in high density farming systems where rapid pathogen transmission necessitates mass medication via feed to contain spread and limit economic losses. Necrotic enteritis caused by Clostridium perfringens is recognized as a widespread and costly poultry disease, affecting broiler production across Europe, though precise prevalence rates vary and are not consistently reported. Similarly, swine dysentery outbreaks in countries such as Germany and Spain have prompted targeted use of tiamulin in medicated premixes. The European Medicines Agency emphasizes that oral administration through feed remains the most practical route for treating large groups where individual dosing is unfeasibleema.europa.eu. This operational reality, coupled with mandatory veterinary oversight under EU Regulation 2019/6, ensures that medicated additives retain a critical role in outbreak mitigation despite broader antimicrobial reduction goals.

Regulatory Mandates for Veterinary Oversight Ensure Controlled Utilization

The European Union’s robust regulatory architecture governing veterinary medicinal products directly shapes the demand for medicated feed additives by institutionalizing prescription-based use and traceability, which is further contributing to the European medicated feed additives market expansion. Under Regulation (EU) 2019/6 on veterinary medicinal products, which became fully applicable in January 2022, all medicated feed must be prepared based on a veterinary prescription following a clinical diagnosis. As per the European Commission, this regulation prohibits prophylactic mass medication and mandates that medicated premixes be produced in licensed feed mills with full batch documentation. This legal framework ensures that medicated additives are not used arbitrarily but as part of defined treatment protocols, thereby sustaining demand within a tightly controlled clinical context. Furthermore, the cascade system allows veterinarians to prescribe specific antibiotics in feed when authorized products are unavailable, provided no suitable alternative exists. In countries like the Netherlands and Denmark, national action plans require electronic recording of all antimicrobial use in livestock, including feed-based medications, which is creating auditable demand streams.

MARKET RESTRAINTS

Antimicrobial Reduction Policies Limit Prophylactic and Routine Use

Europe’s aggressive antimicrobial reduction agenda significantly constrains the application scope of medicated feed additives, particularly for preventive purposes, which is a significant restraint to the European medicated feed additives market growth. The European Union’s commitment to cutting antimicrobial sales for food producing animals by 50% by 2030 as outlined in the Farm to Fork Strategy has led to stringent national action plans that discourage routine medication via feed. According to the European Medicines Agency’s ESUAvet 2023 surveillance report, overall sales of veterinary antimicrobials in the EU decreased by 37% between 2011 and 2022. Countries like Sweden and the Netherlands now prohibit all forms of prophylactic group medication, allowing medicated feed only for confirmed clinical cases under individual animal assessment. The European Food Safety Authority’s 2022 guidance explicitly states that antimicrobials in feed should be a last resort after biosecurity and vaccination measures fail.

Complex Authorization and Manufacturing Compliance Increases Operational Barriers

The production and distribution of medicated feed additives in Europe are encumbered by multifaceted regulatory requirements that elevate costs and restrict market participation. Under Regulation (EC) No 183/2005, facilities producing medicated feed must obtain specific manufacturing authorizations and implement Hazard Analysis and Critical Control Point based quality systems. As per the European Commission, only a limited number of feed mills across the EU hold valid medicated feed manufacturing licenses, reflecting a decline compared to earlier years due to compliance burdens. Each batch requires full traceability from active pharmaceutical ingredient to final delivery, with mandatory retention samples and veterinary prescription linkage. Furthermore, cross contamination prevention mandates separate production lines or extensive cleaning validation, which small and medium enterprises often cannot afford. The European Medicines Agency’s inspections have noted recurring non-compliance issues, including inadequate segregation of medicated and non-medicated batches.

MARKET OPPORTUNITIES

Advancement of Precision Livestock Farming Enables Targeted Medication Delivery

The integration of digital monitoring technologies in European livestock operations is creating new pathways for the precise application of medicated feed additives, which is aligning therapeutic use with individual animal needs and is a promising opportunity in the European medicated feed additives market. According to the European Commission’s Digital Europe Programme, large scale pig and poultry farms in Germany, France, and the Netherlands have increasingly deployed sensor-based health monitoring systems by 2024, capable of detecting early signs of disease such as changes in feed intake or body temperature. These systems trigger automated dispensing of medicated feed to specific pens or subgroups, minimizing blanket treatment. In Denmark, trials using RFID tagged pigs coupled with smart feeders demonstrated reductions in antimicrobial use while maintaining treatment efficacy as per the Danish Veterinary and Food Administration. Similarly, the European Innovation Partnership for Agricultural Productivity and Sustainability has funded projects like SmartMed that integrate electronic veterinary prescriptions with on farm feed automation to ensure compliance and dosing accuracy.

Expansion of Veterinary Pharmacy Networks Facilitates Access and Compliance

The professionalization of veterinary supply chains across Europe is improving the availability and correct use of medicated feed additives through specialized distribution channels, which is another potential opportunity in this regional market. As per the Federation of Veterinarians of Europe, thousands of veterinary practices in the EU now operate integrated pharmacy services that dispense or coordinate the delivery of prescribed medicated premixes directly to farms. In countries like Belgium and Austria, national laws require that all medicated feed be sourced through licensed veterinary wholesalers, ensuring product integrity and prescription adherence. This structured distribution model reduces reliance on general feed mills and minimizes the risk of unauthorized use. Furthermore, the European Medicines Agency’s 2023 survey found that veterinarians in Western Europe reported improved compliance with withdrawal periods when medicated additives were supplied through veterinary pharmacies due to build in tracking systems.

MARKET CHALLENGES

Fragmented National Interpretations of EU Regulations Create Market Inconsistencies

Despite a harmonized legal framework, divergent national implementations of EU veterinary medicine rules generate operational uncertainty and uneven access to medicated feed additives across member states, which is challenging the growth of the European medicated feed additives market. According to the European Court of Auditors’ 2023 special report on antimicrobial use, significant discrepancies exist in how countries define “metaphylaxis” and apply prescription requirements, leading to inconsistent availability of the same medicated product in neighbouring markets. For example, while France permits short term group treatment for respiratory outbreaks in calves under defined conditions, Italy requires individual clinical signs before authorizing medicated feed. The European Medicines Agency has documented numerous national variations in labeling and withdrawal period requirements for identical active substances, increasing formulation complexity. Additionally, language specific dossier submissions and differing inspection frequencies by national competent authorities further fragment the market.

Limited Pipeline of Novel Active Substances Constrains Therapeutic Options

The scarcity of newly approved antimicrobial or antiparasitic compounds for veterinary use in feed severely restricts the therapeutic arsenal available to European livestock producers, which is also challenging the expansion of the European medicated feed additives market. According to the European Medicines Agency, only a few new active substances for medicated feed were authorized between 2018 and 2023, compared to significantly more in the preceding decade, reflecting pharmaceutical companies’ retreat from veterinary antimicrobial development. This stagnation is driven by stringent efficacy and resistance risk assessments under Regulation (EU) 2019/6, which require extensive environmental and public health impact data. Consequently, veterinarians often rely on older molecules like tetracyclines or sulfonamides, despite rising resistance concerns documented by the European Centre for Disease Prevention and Control, which reports that Salmonella isolates from poultry in Southern Europe show notable levels of multidrug resistance. The lack of innovation is particularly acute for alternatives to critically important antibiotics, leaving few options for diseases like swine dysentery where resistance to tiamulin is emerging.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.27% |

| Segments Covered | By Type, Livestock, Mixture Type, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | Zoetis Inc., Archer Daniels Midland Company, Zagro, CHS Inc., Cargill, Purina Animal Nutrition (Land O’ Lakes), Alltech Inc. (Ridley), Adisseo France SAS, Biostadt India Limited, Hipro Animal Nutrition. |

SEGMENTAL ANALYSIS

By Type Insights

The antibiotics segment led the market by holding 33.5% of the European medicated feed additives market share in 2025. The dominance of antibiotics segment in the European market is attributed to their irreplaceable role in treating bacterial infections in high density livestock operations. This dominance is sustained not by growth promotion but by targeted therapeutic use under veterinary prescription. According to the European Medicines Agency, antibiotics such as tiamulin, lincomycin, and sulfadimidine are still authorized in feed form for specific indications including swine dysentery and necrotic enteritis in poultry. As per the European Food Safety Authority, bacterial enteric diseases in pigs remain among the most common reasons for medicated feed prescriptions in Southern Europe, which is reflecting persistent pathogen pressure in intensive systems. Furthermore, the lack of equally effective non antibiotic alternatives for acute outbreaks ensures continued reliance on these compounds. National action plans in countries like Spain and Italy permit short term metaphylactic use during confirmed disease incursions, creating legally sanctioned demand channels. Thus, while overall antibiotic use declines, the clinical necessity for feed-based delivery in group housed animals maintains antibiotics as the leading type segment.

The probiotics segment is the fastest growing segment and is estimated to grow at a CAGR of 10.5% over the forecast period. The growth of probiotics segment in the European market can be attributed to its dual role as both a performance enhancer and a strategic tool in antimicrobial reduction programs endorsed by European authorities. As per the European Commission’s Farm to Fork Strategy, replacing routine antibiotics with microbiome modulators is a key pillar of sustainable livestock production. In Denmark, probiotic strains such as Bacillus subtilis and Lactobacillus reuteri are widely incorporated into starter feeds to reduce post weaning diarrhea, as documented by the Danish Agriculture and Food Council. Similarly, EFSA has issued multiple positive opinions since 2020 for specific probiotic strains demonstrating efficacy in improving gut health and immune modulation in poultry. Major integrators in the Netherlands and Germany have integrated probiotics into their antibiotic free production protocols, supported by consumer demand for responsibly raised meat. With rising scientific validation and regulatory acceptance, probiotics are rapidly transitioning from supplements to core components of European medicated and functional feed strategies.

By Livestock Insights

The swine segment held the major share of 36.9% of the European market in 2025. The dominating position of swine segment in the European market is driven by driven by high disease susceptibility in intensive production systems and the logistical necessity of group medication. According to Eurostat, the European Union maintained a pig inventory of approximately 133 million head in 2023, with a significant proportion housed in large operations where individual treatment is impractical. Endemic pathogens such as Brachyspira hyodysenteriae continue to challenge farms in Germany, Spain, and Poland, necessitating medicated feed interventions. According to the European Medicines Agency, tiamulin medicated premixes accounted for a large share of antibiotic based feed authorizations in 2023, with swine being the primary target species. Furthermore, the weaning phase remains a critical window for enteric disorders, prompting widespread use of medicated or functional additives under veterinary supervision. National disease control programs, including France’s Swine Health Contract, mandate coordinated use of feed-based therapeutics during outbreak responses, reinforcing the segment’s centrality in the European landscape.

The aquaculture segment is the fastest growing livestock segment and is expected to register a CAGR of 11.3% over the forecast period. According to Eurostat, EU aquaculture production volume reached 1.1 million metric tons in 2023, with sea bass, sea bream, and salmon accounting for the majority of output. Bacterial outbreaks such as vibriosis and furunculosis frequently necessitate oral medication, and medicated feed remains the only viable delivery method in aquatic environments. The European Medicines Agency has authorized new antimicrobial medicated feed products for aquaculture, reflecting growing regulatory recognition of therapeutic needs. Moreover, the EU’s Strategic Guidelines for Sustainable Aquaculture emphasize health management through feed-based interventions as a means to reduce environmental impact. With investments in recirculating aquaculture systems and offshore farming accelerating, demand for medicated and functional additives in this segment is poised for sustained, above average growth.

By Mixture Insights

The premix feeds segment accounted for the highest share of 41.4% of the European market in 2025. The growth of premix feed segment in the European market is driven by their primary legal and logistical vehicle for delivering regulated veterinary medicinal products in feed. Under Regulation (EC) No 1831/2003, active pharmaceutical ingredients must be incorporated into feed via authorized premixes produced in licensed facilities, ensuring dosage accuracy and traceability. As per the European Commission, the majority of medicated feed in the EU is manufactured by first blending the active substance into a concentrated premix, which is then diluted at the mill or on farm. This two-step process complies with Good Manufacturing Practice requirements and minimizes cross contamination risks. Countries like the Netherlands and Germany maintain centralized premix production hubs that supply regional feed mills under strict veterinary prescriptions. Additionally, the European Medicines Agency mandates that each premix batch carry a unique identifier linked to the prescribing veterinarian, reinforcing accountability. The regulatory architecture itself thus entrenches premix feeds as the dominant mixture type, making them indispensable in the compliant delivery of medicated additives across the European livestock sector.

The supplements segment is the fastest growing mixture type and is estimated to witness a CAGR of 11.5% over the forecast period owing to the rising integration of non-antibiotic medicated and functional ingredients such as organic acids, phytogenics, and immune modulators into specialized supplement formulations for precision nutrition. Unlike premixes, which are tied to veterinary prescriptions, supplements often fall under feed additive regulations, allowing greater flexibility in use. According to the European Feed Manufacturers’ Federation, the number of authorized zootechnical and coccidiostat supplements has increased in recent years, reflecting innovation in alternatives to antimicrobials. In Sweden and Denmark, many pig and poultry farms now use daily supplement blends containing probiotics and enzymes to support gut health without triggering prescription requirements. Furthermore, the rise of on farm feed mixing in Southern Europe has boosted demand for easy to handle, small batch supplements that can be added manually. This regulatory agility and functional versatility position supplements as the most dynamic mixture segment in the evolving European landscape.

COUNTRY ANALYSIS

Top Countries In The Market

Germany Medicated Feed Additives Market Analysis

Germany dominated the medicated feed additives market in Europe in 2025 by holding 20.8% of the regional market share. The dominance of Germany in the European market can be credited to its role as Europe’s largest livestock producer and most advanced veterinary pharmaceutical market. The country housed ~20.7 million pigs and ~10.9 million cattle. A large proportion of swine operations are intensive, creating consistent demand for regulated therapeutic feed solutions. According to the Federal Office of Consumer Protection and Food Safety, Germany reports thousands of veterinary prescriptions annually for medicated feed, among the highest volumes in the EU. Strict adherence to the German Medicinal Products Act ensures only licensed feed mills produce medicated batches. Public research institutions such as the Friedrich Loeffler Institute collaborate with industry to validate alternatives to critical antibiotics, accelerating adoption of novel medicated and functional additives.

France Medicated Feed Additives Market Analysis

France captured 16.8% of the regional market share in 2025. The growth of France in the European market is attributed to its diverse livestock base and proactive antimicrobial stewardship framework. The country maintained ~12 million pigs and ~18 million cattle in 2023. According to the ANSES database, a 48% reduction in antibiotic sales between 2011 and 2022, followed by a 6.5% increase in 2023. The EcoAntibio 2 plan incentivizes targeted medicated premix use during outbreaks while promoting alternatives. France also hosts major feed additive manufacturers and EU reference laboratories, enabling rapid regulatory feedback and product development.

Spain Medicated Feed Additives Market Analysis

Spain is estimated to witness a promising CAGR in the European medicated feed additives market during the forecast period owing to its large pig and poultry sectors and recurring disease challenges in Mediterranean climates. Pork production was just under 5 million metric tons in 2023 (USDA/Spanish Ministry of Agriculture), making Spain the EU’s top exporter. The Spanish Agency for Medicines and Health Products records thousands of medicated feed authorizations annually, primarily for swine enteric and respiratory conditions. High summer temperatures and dense stocking amplify pathogen transmission, increasing reliance on feed‑based therapeutics. Spain’s participation in the EU’s antimicrobial monitoring network ensures alignment with reduction goals while permitting necessary therapeutic use.

Netherlands Medicated Feed Additives Market Analysis

The Netherlands is expected to hold a notable share of the European medicated feed additives market over the forecast period due to the precision livestock farming and leadership in antimicrobial reduction. Antibiotic use in farm animals has fallen by over 76% since 2009. Despite this, medicated feed remains essential for acute outbreaks in high‑density pig and poultry systems. The mandatory electronic registration system (IKB) requires real‑time reporting of all veterinary medicinal product use, including feed‑based medications. Dutch feed mills are among the most advanced in Europe, with segregated lines ensuring compliance with EU cross‑contamination rules.

Denmark Medicated Feed Additives Market Analysis

Denmark is predicted to register a healthy CAGR in the European medicated feed additives market over the forecast period. Denmark is globally recognized for its “Yellow Card” system monitoring antimicrobial use at farm level. The country maintained ~11.6 million pigs in 2023 (Eurostat/Statistics Denmark), nearly double its human population. Farms exceeding thresholds for antibiotic consumption—including medicated feed—are subject to mandatory action plans and veterinary oversight. A significant proportion of medicated feed prescriptions target post‑weaning diarrhea control, often using zinc oxide alternatives and targeted antibiotics. Denmark’s integrated cooperative production model enables rapid deployment of medicated and functional feed solutions across the supply chain.

COMPETITIVE LANDSCAPE

The Europe medicated feed additives market features a competitive environment defined by stringent regulation scientific rigor and a clear demarcation between therapeutic necessity and growth promotion. Competition is not driven by price but by regulatory expertise manufacturing integrity and alignment with national antimicrobial reduction plans. Established global animal health companies dominate due to their ability to navigate complex authorization processes under Regulation (EU) 2019/6 and maintain compliant production infrastructure. Smaller players struggle with the high costs of licensing feed mills and conducting required residue and efficacy studies. Geographic variation in disease pressure and prescribing practices creates fragmented demand patterns requiring localized strategies. Transparency mandates such as electronic prescription logging in Denmark and the Netherlands further raise operational standards. Innovation is increasingly focused on narrow spectrum antibiotics and targeted delivery systems that minimize resistance risk. As the EU advances its Farm to Fork objectives the market rewards companies that balance clinical efficacy with public health responsibility reinforcing a high barrier to entry and a premium on compliance.

KEY MARKET PLAYERS

Some of the major companies competing in the market for their share include

- Zoetis Inc.

- Archer Daniels Midland Company

- Elanco Animal Health Incorporated

- Phibro Animal Health Corporation

- Zagro

- CHS Inc.

- Cargill

- Purina Animal Nutrition (Land O’ Lakes)

- Alltech Inc. (Ridley)

- Adisseo France SAS

- Biostadt India Limited

- Hipro Animal Nutrition.

Top Players In The Market

- Zoetis Inc. is a global animal health leader with a significant footprint in the Europe medicated feed additives market through its portfolio of veterinary pharmaceuticals and medicated premixes. The company supplies antibiotics and antiparasitic compounds authorized for use in swine and poultry feed across multiple European countries under strict regulatory compliance. In 2024 Zoetis enhanced its European capabilities by expanding its medicated feed manufacturing facility in Belgium to meet heightened demand for prescription-based additives under the EU Veterinary Medicinal Products Regulation. The company also collaborates with national veterinary authorities to support antimicrobial stewardship programs while ensuring therapeutic access during disease outbreaks. Through scientific engagement and regulatory alignment Zoetis reinforces its role as a trusted partner in responsible livestock health management across the region.

- Elanco Animal Health Incorporated maintains a strong presence in the Europe medicated feed additives market by offering a range of therapeutic feed medications primarily for swine and poultry. The company leverages its global R and D network to develop formulations that comply with European Union regulatory standards including withdrawal period requirements and residue controls. In 2023 Elanco launched a digital prescription tracking platform in partnership with feed mills in Germany and Spain to ensure traceability and compliance with EU Regulation 2019/6. This system links veterinary prescriptions to batch production records enhancing audit readiness and reducing misuse. Elanco also participates in European research consortia focused on alternatives to critically important antibiotics further solidifying its commitment to sustainable animal health solutions within the European regulatory framework.

- Phibro Animal Health Corporation operates a specialized segment in the Europe medicated feed additives market with a focus on antimicrobial and performance enhancing products for intensive livestock systems. The company’s medicated premixes containing bacitracin and other authorized actives are used under veterinary prescription in key markets such as France and the Netherlands. In early 2024 Phibro completed validation of a new European manufacturing line dedicated exclusively to medicated feed additives to prevent cross contamination and meet Good Manufacturing Practice requirements under EU law. The company also invests in on farm training programs to educate veterinarians and producers on correct dosing and withdrawal protocols. These initiatives demonstrate Phibro’s commitment to regulatory excellence and responsible use in alignment with Europe’s One Health antimicrobial resistance strategy.

Top Strategies Used by the Key Market Participants

Key players in the Europe medicated feed additives market adopt regulatory compliance innovation in manufacturing and strategic partnerships as core strategies to maintain competitiveness. Companies invest in dedicated production lines to prevent cross contamination and meet stringent EU Good Manufacturing Practice standards. They align product development with the European Medicines Agency’s guidelines on antimicrobial use ensuring all formulations support therapeutic rather than growth promotion purposes. Digital solutions such as prescription tracking and batch traceability systems are increasingly deployed to satisfy national monitoring requirements. Collaboration with veterinary authorities and participation in antimicrobial stewardship initiatives further enhance credibility. Additionally, firms diversify into non antibiotic functional additives like probiotics and organic acids to address market demand for alternatives while retaining relevance in medicated segments through compliant therapeutic offerings.

MARKET SEGMENTATION

This research report on the Europe medicated feed additives market is segmented and sub-segmented into the following categories.

By Type Insights

- Antioxidants

- Antibiotics

- Probiotics

- Prebiotics

- Enzymes

- Amino Acids

- Others

By Livestock

- swine

- cattle

- poultry

- pet foods

- aquaculture

- others

By Mixture Type

- supplements

- premix feeds

- concentrates

- base mixes

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe medicated feed additives market?

It refers to the regional industry for feed ingredients containing therapeutic substances used to prevent, treat, or control animal diseases.

Why are medicated feed additives used in livestock?

They help control infections, improve animal health, and support growth by delivering medication directly through feed.

What animals benefit from medicated feed additives?

Poultry, swine, cattle, and aquaculture species are major beneficiaries of medicated feed products.

What types of medicated feed additives are common?

Antibiotics, coccidiostats, anti-inflammatory agents, and growth promoters are among widely used medicated additives.

What drives growth in the Europe medicated feed additives market?

Rising animal health awareness, disease prevalence, and regulated livestock production drive market demand.

How do EU regulations influence medicated feed additives?

Strict EU veterinary and feed safety standards govern approval, usage limits, and withdrawal periods for medicated additives.

Are alternatives to antibiotics gaining interest?

Yes, probiotics, prebiotics, enzymes, and organic acids are increasingly used as non-antibiotic alternatives.

How do medicated additives improve animal performance?

By reducing disease impact and improving gut health, they enhance feed efficiency and weight gain.

What challenges does the medicated feed additives market face?

Antibiotic resistance concerns, regulatory restrictions, and public scrutiny are key challenges for the market.

How is animal welfare affecting medicated additive use?

Better welfare practices and reduced stocking densities lower disease incidence, influencing medicated additive strategies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com